China Renaissance 2021 Annual Review: Medical Devices Sector in Healthcare and Life Sciences

In 2021, as the pandemic spread globally, China responded proactively. While gradually mitigating the impact of the Delta variant, the country also confronted the emergence of Omicron. Mirroring the fluctuating trajectory of the epidemic, China’s medical device industry experienced cyclical turbulence in 2021: from a surge of activity after the Spring Festival, with substantial financing rounds across multiple sectors and a wave of IPO filings in the second quarter, to a rapidly shifting landscape in the second half of the year that even sparked widespread apprehension toward IPOs. The Healthcare and Life Sciences Team at China Renaissance presents this annual review of the medical device sector in 2021, summarizing the past year and looking ahead to 2022.

Looking back at 2021, China’s medical device capital market was highly active. Compared with the previous two years, there was a significant increase in the number and volume of private equity financings, M&A transactions, and IPOs. Many innovative companies seized the tail end of the cycle to swiftly file for IPOs or secure critical financing rounds, thereby accumulating sufficient cash reserves to “weather the winter.”

In China’s healthcare landscape, volume-based procurement (VBP) has led to a divergence in industry structure, constraining the growth of some companies and slowing the expansion of foreign firms’ market share, while creating growth opportunities for domestic enterprises. Innovative companies have also diverged following the implementation of VBP, with medical device innovation returning to its fundamental value proposition. The sector has become increasingly diverse; cardiovascular, still a major focus of transactions, remains highly prominent, yet its competitive landscape has undergone significant changes. Orthopedics has seen investor confidence “frozen” due to the impact of VBP, whereas fields such as endoscopy, surgical robotics, and tumor ablation are gaining momentum. Meanwhile, consumer-oriented segments like dentistry and medical aesthetics are rising rapidly.

IPO Listing

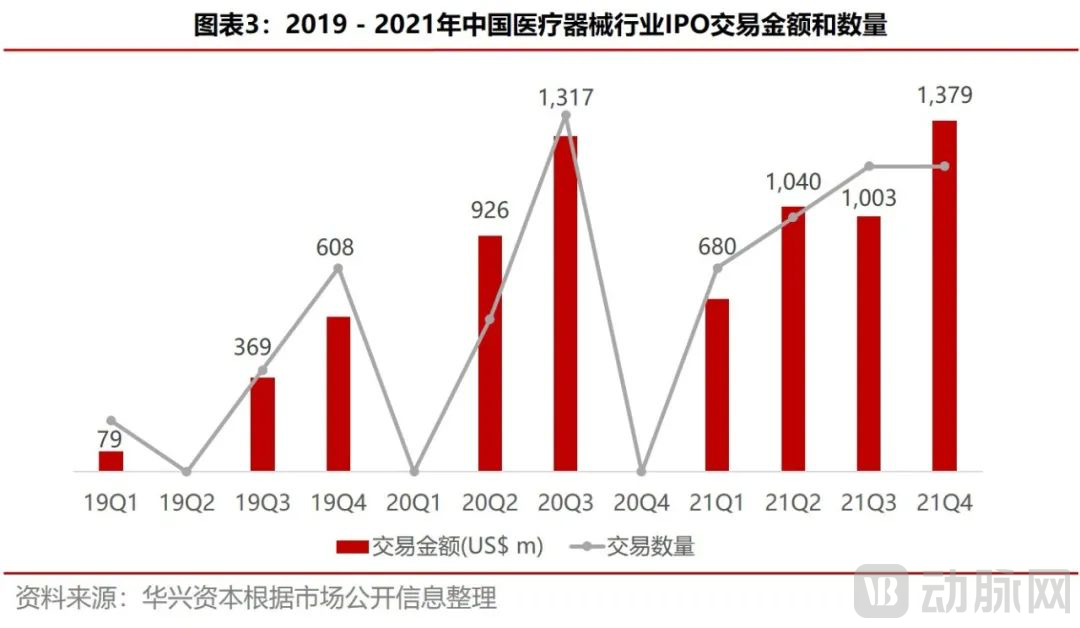

Diversification of IPO Pathways in 2021 Failed to Prevent Listed Medical Device Companies from Breaking Issue Price

The certainty of the HKEX Chapter 18A listing channel and the STAR Market’s encouragement of innovation drove a substantial surge in IPO volume in 2021, with the annual total far exceeding the combined figures for 2019 and 2020. However, in the second half of last year, companies making their HKEX debuts as “first stocks” in their respective categories repeatedly broke their issue prices, signaling that the market momentum was waning. Issues such as patent conflicts, insufficient sector scarcity, and revenue falling short of expectations diminished the luster of segments like TAVR and neurointerventional devices. Low liquidity and subdued sentiment dominated the secondary market, which in turn dampened activity in the private equity market during the second half of the year. Meanwhile, uncertainties surrounding China’s STAR Market listing channel and its review process left many applicants waiting indefinitely for approval, while even highly liquid segments continued to face upward resistance in the medical device sector.

2022 IPO: Approach with a Balanced Mindset and View Corporate Milestones Through a Developmental Lens

As the Year of the Tiger approaches, many investors are hesitating, making the identification of investment targets and the evaluation of industry sectors major themes for the new year. We have observed nascent signs of activity in the private equity market since December 2021. It is undeniable that emerging from cyclical undervaluation takes time. The medical device sector is characterized by long-term growth potential and sustained profitability, rather than offering opportunities for quick entry and exit. Following the rapid influx of capital, many other sectors have also undergone corresponding adjustments.

Regarding innovative enterprises, as the entrepreneurial environment matures and IPO pathways remain clear, entrepreneurs are adopting a more rational attitude toward going public. They are beginning to recognize the value of the secondary market for corporate development, carefully assessing their own stage of growth, selecting appropriate listing boards, and planning their capital strategies in advance to “accumulate resources.” On the investment front, investors are placing greater emphasis on the alignment between a company’s core value and its management team. Valuation and pricing in the primary market are becoming more rational and objective, while the role of investors in providing strategic support has become increasingly significant, with more comprehensive guidance and assistance expected in the coming year.

Centralized Procurement

In 2021, Cost Containment and Price Reductions: Meeting Citizens’ Basic Health Needs Through Universal HealthcareIn 2021, multiple medical devices were included in the scope of centralized procurement. The average price reduction for the 42 insulin products under specialized centralized procurement was 48%, while the average price reduction for artificially implanted hip and knee joints procured through centralized bidding reached 82%. These measures are expected to benefit nearly 11 million patients and reduce the financial burden by approximately RMB 30 billion annually. Throughout the year, the first five batches of nationally centralized drug procurements and coronary stents saved nearly RMB 170 billion in medication and medical expenses.

The two rounds of centralized procurement have focused on major market segments such as cardiovascular and orthopedics, which feature high domestic product penetration and widespread clinical usage. This procurement strategy benefits healthcare payers by alleviating pressure on the national medical insurance fund. From a trend perspective, price adjustments have become more moderate, leaving room for corporate development within these sectors in the post-centralized procurement era. An analysis of capital market dynamics in the cardiovascular sector in 2021 reveals that following the inclusion of coronary stents and balloons in centralized procurement, comprehensive procurement of guidewires and catheters may be imminent, with several provincial alliances already initiating such procurement activities. Meanwhile, centralized procurement has also accelerated the development of niche fields such as cardiovascular AI imaging, interventional robotics, electrophysiological ablation (including Pulsed Field Ablation, PFA), and novel coronary intervention therapies (such as shockwave balloons), all of which attracted significant investor interest in 2021.

2022: Policy-Driven Regulation Highlights the State’s Determination to Promote Innovation

On July 15, 2019, the State Council issued the “Opinions of the State Council on Implementing the Healthy China Action.”

The “Opinions” propose a comprehensive development plan for China’s health industry, spanning prevention, management, and treatment. The diagnosis and treatment of major diseases—such as cardiovascular and cerebrovascular disorders, cancer, respiratory diseases, diabetes, and infectious diseases—are highlighted as core conditions in the “Opinions.” These conditions are precisely the most prevalent in China, exert the most profound impact on residents’ health, and account for the largest share of medical insurance expenditures. Policy emphasis on these major diseases has encouraged investment in related diagnostic and therapeutic fields, providing strategic guidance for the direction of healthcare industry development.

In the 2026 centralized procurement, attention will still be focused on universal medical devices for chronic disease treatment.

On January 10, 2022, the State Council’s executive meeting decided to institutionalize centralized volume-based procurement (VBP) for pharmaceuticals and high-value medical consumables, expand the scope of VBP for high-value medical consumables, and launch VBP initiatives at both national and provincial levels for orthopedic consumables, drug-coated balloons, and dental implants—areas of significant public concern. This move underscores the policymakers’ firm resolve. Furthermore, non-reimbursed dental services, which represent a substantial out-of-pocket expense for the general public, have also been brought under the regulatory scope of VBP. Innovative enterprises must strike a balance between participating in VBP and fostering innovation, align with national policy directions, seek breakthroughs in advanced technologies, identify opportunities to replace imported monopolistic devices, and explore new pathways in quality control, manufacturing, and innovative marketing of medical devices.

Track

Major Tracks Remain “Robust” with Significant Market Appeal; Landscape Adjusts Post-Centralized Procurement

Annual Review: Cardiovascular Sector Remains the Cornerstone of the Private MarketInterventional heart valves, pulsed field ablation (PFA), ventricular assist devices (VADs), and intravascular lithotripsy balloons have set financing benchmarks in their respective sub-sectors. Multiple companies have completed critical funding rounds, with some even filing for IPOs on the Hong Kong Stock Exchange. VAD companies garnered significant attention from the capital market in the first half of the year, while electrophysiology start-ups saw a surge in activity toward year-end. These two sub-sectors are expected to witness further developments in the coming year.

● Interventional Valves

In January 2020, Abbott’s Tendyne transcatheter mitral valve replacement system received CE marking; in June 2020, Abbott’s MitraClip mitral valve repair system was approved in China, further fueling investment momentum in the valvular heart disease sector through 2021. Over the past year, leading domestic players in transcatheter valve interventions, such as Hanyu Medical, Jian Shi Technology, HeartCare Medical, and Nuomai Medical, have all filed for IPOs. Despite a broader market downturn, enthusiasm for this sector remains undiminished. In early 2022, Medtronic’s TAVR system obtained regulatory approval in China, marking the onset of a new round of competition between domestic and international companies. It remains to be seen whether TAVR commercialization will introduce new models and achieve high-speed growth in the next phase. In December 2021, Cardiovalve was acquired by Qiming Venture Partners for $300 million, accelerating the R&D of its tricuspid and mitral valve pipeline. Future competition in the valve sector is expected to intensify. Looking ahead to the emerging commercial competition in tricuspid and mitral valve interventions, companies with extensive pipeline portfolios, rapid R&D iteration, and stable regulatory progress will possess significant advantages in attracting investment.

● Pulsed Field Ablation (PFA)

On June 24, 2021, Boston Scientific announced its acquisition of Farapulse, a pioneer in pulsed field ablation (PFA) technology. This move sent shockwaves through the industry, prompting numerous Chinese startups to strategically position themselves in the PFA space early on. Innovative products from companies such as Denovo Electrophysiology, Jinjiang Electronics, and Ruidi have already entered clinical trials, while emerging players like Saihe, Zhouling, Xuanyu, and Aikemai are aggressively raising capital to catch up, highlighting the intense competition in this niche sector. In January 2022, Medtronic announced it would acquire cardiac ablation company Affera for $925 million; Affera also specializes in PFA technology. These transactions have sent a clear signal to the market: following the significant impact of centralized procurement on coronary interventions, electrophysiology is poised to become a new growth driver.

● Ventricular Assist Device (VAD)

Medical devices for heart failure treatment have remained a core focus of corporate R&D. In the global market, ventricular assist devices (VADs)—such as Medtronic’s HeartWare (approved by the FDA in 2018 but unfortunately withdrawn from the market in 2021 due to safety concerns) and Abbott’s HeartMate (approved by the FDA in 2020, with strong global sales to date)—have consistently attracted significant attention from capital markets. In China, companies including Tongxin, Xinqing, Core Medical, and Fengkai secured substantial financing in 2021, demonstrating strong commitment to advancing the commercialization and promotion of domestically developed VADs. With many innovative enterprises having achieved technological maturity and rapidly built up their teams, they entered 2022 with high confidence, poised to deliver upgrades and optimizations in device-based therapies for heart failure patients.

● Orthopedics

Beyond cardiovascular care, the orthopedics sector has been more significantly impacted by centralized volume-based procurement (VBP). In 2021, numerous startups focused on organizational growth, accelerating regulatory approvals and pipeline commercialization, while expanding their marketing teams. However, the sports medicine subsector maintained the momentum seen in the previous year. Demei Medical secured funding at the beginning of the year to strengthen hospital collaborations; Fangrun Healthcare gained support from new shareholders and signed a strategic partnership with Medtronic in November to accelerate the decentralization of medical resources; Tianxing Medical saw two rounds of increased investment from its shareholders, as the company continued to expand its team to build capacity for future growth. The development of sports medicine in the coming year is highly anticipated, and breakthroughs in innovative orthopedic materials will also bring new trends to the sector, with new materials and customization emerging as key themes. Although VBP covers joints, spine, and trauma products, under the new rules, companies with cost advantages, high service quality, and strong clinical collaborations will find “new life” and thrive.

Niche Segments Shine: Therapeutic Breakthroughs and Technological Iterations Capture Investment Spotlight

In the first half of last year, Xinguangwei, OptoMedix, and Ruipai Medical successively introduced prominent institutional investors, bolstering market confidence in the endoscopy sector. In the endoscopy market, where the imperative for domestic substitution is particularly strong, last year witnessed Xinguangwei’s phenomenal performance as it rapidly filed for an IPO following two rounds of financing; OptoMedix’s 4K fluorescence endoscopes secured a certain market share thanks to positive clinical feedback; and Ruipai’s single-use endoscopes, along with Xinguangwei’s products, each feature distinct design characteristics, making it promising to see Chinese enterprises break free from the “shackles” imposed by foreign companies such as Olympus.

The global continuous glucose monitoring (CGM) market is currently dominated by a triopoly of Dexcom, Abbott, and Medtronic, with Abbott holding nearly 50% of the global market share. Since 2021, a new generation of CGM products from companies such as MicroTech Medical, Yuyue Medical Technology, Sinocare, and Yuwell Medical has been launched consecutively, with product performance—particularly in terms of sensor lifespan, accuracy, and calibration requirements—rapidly catching up to global benchmarks. The domestic CGM market in China has taken shape, and MicroTech Medical’s successful market entry has intensified competition within the sector. The market is poised for explosive growth in the coming years, driven by the further rise of Chinese manufacturers. Companies such as Silicon Based and Jiunuo have obtained regulatory approvals to enter the market. In the future, key factors for competitive success will include continuous R&D iteration, high measurement accuracy, and well-established marketing teams.

In 2021, cataract treatment devices and intraocular lenses were included in the centralized procurement list.

Unlike coronary interventions, the rapid growth in cataract surgery volumes has accelerated the consolidation of leading enterprises through centralized procurement, creating clear investment opportunities in the ophthalmology sector. In a market where imports account for more than 80% of the share, the rise of domestic original innovation teams is beginning to take shape. Aier Eye Hospital Group, listed in 2020, focuses on mid-to-high-end brands and holds a leading position among domestic companies; it actively invested in innovative ophthalmic enterprises in 2021 to strengthen industrial synergy. Aier Eye Hospital concentrates on hospital management and strategic layout, solidifying its position as the leader in medical services. Both Akontec and Haohai Biological Technology have actively expanded into the orthokeratology (OK lens) market, highlighting the diversification and vibrancy of the ophthalmology track. In early 2021, the National 14th Five-Year Plan for Eye Health emphasized the need for early detection and treatment of ophthalmic diseases. Issues such as myopia in adolescents, cataracts in the elderly, and other eye conditions in younger populations will continue to stimulate entrepreneurial enthusiasm and boost investor confidence in 2022.

Product Innovation: From Imitation and Incremental R&D to Full Originality

In China, the medical device industry has evolved from the 1.0 era (localization of foreign products and establishment of domestic commercial channels) through the 2.0 era (incremental innovation), and is gradually advancing into the 3.0 era (fully original Chinese innovations). Mature medical devices are entering an iteration cycle: for instance, electrophysiology is shifting its R&D focus from radiofrequency ablation to pulsed field ablation; peripheral vascular interventions are expanding from arterial stents to venous stent therapies; and standardized orthopedic consumables are moving toward customized product innovation. Niche sectors are demonstrating distinctive characteristics and a widespread surge in innovation. For example, refractive diagnosis and treatment equipment in ophthalmology, surgical consumables compatible with robotic surgery, and miniaturized neuromodulation products are all poised to deliver surprises to the capital market in 2021 and beyond.

Outlook

Standing at the beginning of 2022, against the backdrop of national policies encouraging industrial innovation and development, the medical device industry is charging into its next phase with rapid momentum. The previously subdued capital market atmosphere is poised for a turning point toward renewed vitality. Companies in major market segments must undergo upgrades, optimize their business models, and accelerate the commercialization of innovative products. In niche segments, competition driven by innovation favors the strongest players, and products with significant clinical value will inevitably become the core focus. Original Chinese innovations are spreading like wildfire, presenting numerous emerging opportunities within the medical device sector. These advancements will increasingly expand into international markets, exerting a growing influence on the global landscape.

Disclaimer

This report is provided for your reference only and does not constitute, nor shall it be deemed as, an offer or invitation to sell, purchase, or subscribe for securities, nor does it constitute an invitation to any specific person. The investments mentioned in this report may not be available in certain jurisdictions. Any investment mentioned herein may involve significant risks; some investments may be illiquid and may not be suitable for all investors. The value of the investments mentioned in this report, or the income derived therefrom, may fluctuate due to exchange rate movements. Past performance is not indicative of future results. This report does not take into account the investment objectives, financial situation, or particular needs of any investor. Investors should not rely solely on this report but should make their own investment decisions based on their independent judgment. Before taking any investment action based on the recommendations in this report, investors should seek professional advice.

This report has been prepared by China Renaissance Holdings (“China Renaissance”). The sources of the information contained herein are believed by China Renaissance to be reliable. The opinions, analyses, forecasts, projections, and expectations set forth in this report are based on such reliable data but represent views only. China Renaissance, its holding companies and/or subsidiaries and/or related individuals do not warrant the accuracy or completeness of this report. The information, opinions, and estimates contained in this report reflect the judgments of China Renaissance as of the initial date of publication of this report and are subject to change without notice. China Renaissance, its holding companies and/or subsidiaries and/or related individuals shall not be liable for any direct, indirect, or consequential losses arising from the use of the materials contained in this report.

This report is fully protected by copyright and proprietary rights. No person may reproduce, distribute, or publish this report for any purpose without the authorization of China Renaissance Capital. China Renaissance Capital reserves all rights.