Over RMB 10 Billion Across 288 Deals: Decoding Industrial Capital's Investment Logic in China's Healthcare Sector

It was once believed that the period from 2008 to 2018 constituted a “golden decade” for the development of domestic industrial capital.

The reasons can be broadly summarized into the following three points:

First, there has been a frequent rollout of policies encouraging industrial capital to serve the development of the real economy;

Second, the rapid development of China's economy, coupled with a surge in innovation and entrepreneurship, has generated substantial capital demand, making capital injection feasible;

Third, leading enterprises in the healthcare industry are also integrating their respective industrial chains through capital linkages.

Against that backdrop, VCBeat examined 159 healthcare industry funds established with the participation of listed companies between 2015 and 2017, analyzing the participating entities, investment sectors, and investment scales of these healthcare industry funds at the time. It summarized and put forward perspectives such as “funds involving general listed companies tend to focus on areas related to the core businesses of the listed companies” and “one of the reasons for the surge in healthcare industry funds is the need for ‘integration of industry and finance.’”

In May 2018, VCBeat once again reviewed the key developments in private healthcare investment by industrial capital, the policy environment, and emerging trends, stating that “healthcare asset operational capabilities and value-based care will become the focal points for the next phase of development in privately operated healthcare funded by industrial capital.”

Four Years On: Have the Key Players, Investment Logic, and Preferred Sectors of Industrial Capital in Healthcare Changed? To answer this question, VCBeat once again focuses on industrial capital in healthcare financing and investment. By analyzing 288 domestic healthcare investment and financing deals involving industrial capital in 2021, we explore what has changed—and what has remained constant—in their approach to investing in the healthcare sector.

Generally speaking, industrial capital invested in the healthcare sector can be broadly categorized into healthcare industry chain capital (hereinafter referred to as “industry chain capital”) and cross-sector capital. Industry chain capital primarily refers to enterprises that are themselves part of the healthcare industry chain, or funds established by such enterprises. Cross-sector capital refers to non-healthcare enterprises, or funds established by such enterprises.

According to previous reports by VCBeat, the main participants in industrial chain capital are primarily pharmaceutical companies and medical device manufacturers. Data on healthcare financing and investment in 2021 shows that this trend has largely remained unchanged.

After reviewing healthcare investment and financing events across the industrial chain in 2021, VCBeat found that investors included well-known pharmaceutical companies such as Huadong Medicine, China Biologic Products, Qilu Pharmaceutical, Yangtze River Pharmaceutical Group, Hengrui Medicine, and Junshi Biosciences, as well as medical device companies including Allsheng Medical, a leading domestic player in vacuum blood collection systems, and Blue Sail Medical, a leader with comprehensive coverage of the low-, mid-, and high-value consumables industry chain.

It is worth noting that among the participants in capital investment within the healthcare industry chain, certain CRO companies and a small number of healthcare service providers have also emerged.

Among them, CRO companies are represented by Tigermed and WuXi AppTec; healthcare service providers are represented by AliHealth, Medlinker, and Aier Eye Hospital. However, compared to the number of health-tech investment and financing deals involving pharmaceutical and medical device companies, these types of enterprises participate in fewer such transactions.

The participating entities have not changed significantly; has the investment logic of industrial chain capital shifted?

After reviewing the healthcare investment and financing data involving industrial chain capital in 2021, VCBeat found that the core investment logic of such capital—primarily focused on integrating industry chain resources and expanding their own businesses—remained unchanged.

Taking Tigermed as an example, the company participated in a total of nine investment and financing transactions in 2021. Six of the investee companies operated in the pharmaceutical sector, with areas of focus including innovative drug development, small-molecule anti-cancer novel drug development, cell therapy development, and vaccine product development. The remaining three investee companies were engaged in research and development and manufacturing outsourcing, which is closely aligned with Tigermed’s core business.

Nine Healthcare Investments Involving Tigermed in 2021, Chart by VCBeat

Note: All monetary amounts in the charts and tables of this article are denominated in Renminbi (RMB). Foreign currency amounts have been uniformly converted into RMB based on the average exchange rate for the year in which the event occurred; for instance, the USD/RMB exchange rate in 2021 was approximately 6.45.

It can be seen that Tigermed’s investment targets fall into two categories: biopharmaceuticals and research, development, and manufacturing outsourcing.

What are the underlying reasons for this fundamental investment logic? Customer and resource acquisition may be the core elements.

According to Tigermed’s 2021 semi-annual report, the company “drives the development of promising early-stage biotechnology and medical device companies through continuous investment and incubation, thereby securing potential clients and business opportunities; further expands its client base by continuing to invest in business development and marketing to enhance the expertise and customer reach of its business development team, while providing additional technical and service resources to attract new clients with innovative and differentiated product pipelines who have sustained business needs for multiple R&D projects and diversified services.”

As can be seen from the above statement, Tigermed’s investments—whether in early-stage pharmaceutical technology and medical device companies or in enterprises with business models similar to its own—are all aimed at acquiring new customers or business opportunities.

andIn China Biopharmaceutical’s investment in Yilian, the intent to integrate resources across the industrial chain is even more pronounced.

According to China Biopharmaceutical’s 2020 annual report, the company invested $514 million in Yilian, acquiring a 13.09% equity stake in the latter. The company described this financing round as a breakthrough in deploying its internet healthcare strategy. (Note: Although the investment and financing transaction was completed in 2020, it was not publicly disclosed until late 2021.)

The aggressive deployment of internet-based healthcare may be linked to reforms in pharmaceutical marketing models.

According to the aforementioned report by Sino Biopharmaceutical, as the scope of centralized drug procurement continues to expand, the profit margins of China’s generic drug industry have been significantly affected. Meanwhile, rising costs following the implementation of the registration and filing management system for medical representatives have made it increasingly difficult to sustain the traditional hospital-based marketing and promotion model for prescription drugs. Consequently, marketing and service models based on online platforms will assume a more prominent role in future pharmaceutical marketing. In response, Sino Biopharmaceutical has identified this trend and made corresponding strategic arrangements.

Additionally,In 2021, another noteworthy financing and investment event in the healthcare industry capital market was Aier Eye Hospital’s strategic investment in Shiva Imaging.

Shiwei Imaging is a developer of high-end ophthalmic equipment in China. Founded in Silicon Valley, USA, in 2014 by three Chinese PhDs educated in the United States, the company boasts a world-class R&D team with over a decade of experience in Silicon Valley-style engineering, semiconductor optics, and the development of high-end medical devices. Its first self-developed OCT product demonstrates superior performance in imaging quality, field of view, penetration depth, and blood flow algorithms.

Furthermore, concurrent with the completion of the financing round, Vision Medical’s “True Blood Flow” swept-source OCT will be deployed at Hainan Boao Lecheng Aier Eye Hospital.

“Visun OCT outperforms all imported and domestic counterparts in product performance, imaging quality, imaging range, imaging algorithms, and quantitative accuracy, significantly surpassing current mainstream imported brands,” stated Professor Liu Hansheng, Head of the Imaging Group at Aier Eye Hospital.

As the leading ophthalmology chain in China, Aier Eye Hospital boasts abundant medical resources and extensive experience in hospital management.Through this investment, Vision Medical Imaging has not only secured financial support from Aier Eye Hospital but can also leverage Aier Eye Hospital’s market position and extensive resources to expand its brand influence and enhance its competitiveness.

Aier Eye Hospital, positioned in the midstream of the ophthalmology industry chain, has broken through its previous horizontal M&A model focused on eye hospitals through this strategic move, which can be regarded as the beginning of vertical integration of industry resources.

Thus, it is evident that Tigermed’s investments in companies with business activities similar to its core operations, China Biopharmaceutical’s investment in Yilian Medical Group in response to reforms in pharmaceutical marketing models, and Aier Eye Hospital’s investment in Visunet Medical Imaging can all be regarded as horizontal and vertical integration of industrial resources.

In 2021, there were 100 investment and financing deals in the healthcare sector involving cross-industry capital. The participants in these cross-industry investments can be primarily categorized into three groups: internet giants represented by Xiaomi, Baidu, Tencent, and ByteDance; insurance capital represented by Sunshine Ronghui; and other industrial capital represented by Country Garden Venture Capital, Langzi Shares, and New Hope Group.

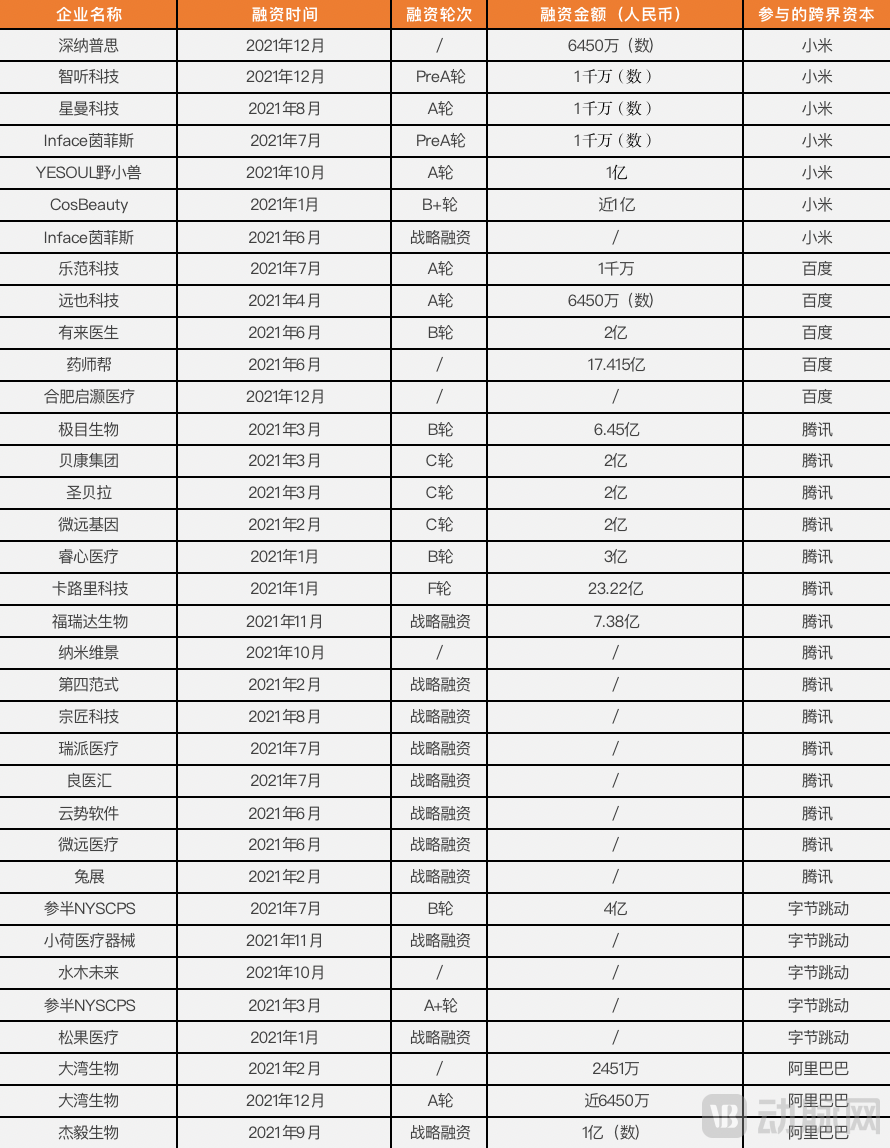

After reviewing investment and financing data, VCBeat found that major internet companies represented by Xiaomi, Baidu, Tencent, and ByteDance collectively participated in 35 investment and financing deals in the healthcare sector in 2021. Among them, Xiaomi participated in 7 deals, Baidu in 5, Tencent in 15, ByteDance in 5, and Alibaba in 3.

2021 Investments by Major Internet Companies in the Healthcare Sector, Chart by VCBeat

Note: The term “number” in the charts refers to financing amounts that may range from millions to tens of millions. In this article, after conversion into RMB, the figures are presented as the financing amount (in numbers).

AndThe investment logic followed by major internet companies in the healthcare sector largely stems from their core strengths, aiming to build their own healthcare ecosystem.

For example,VCBeat has found that among the healthcare investments made by major internet companies over the past year, medical devices have been the most favored. A further breakdown of the financing and investment data reveals that among these 11 medical device investment deals, one investor’s name appeared seven times: Xiaomi-affiliated capital (including Xiaomi Group, Xiaomi Technology, and Shunwei Capital).。

Furthermore, the seven companies that received investment from Xiaomi-affiliated capital in 2021 were predominantly in the hardware sector, including wearable devices, home medical equipment, and personal care and beauty instruments. This reflects an investment logic closely aligned with Xiaomi’s strategic focus on consumer-oriented attributes and its continued emphasis on its core hardware expertise within the healthcare sector.

If the investment logic of major internet companies in the healthcare sector is relatively clear and well-defined, what then is the rationale behind healthcare financing and investment by other cross-industry capital players?

Let’s first look at insurance capital.

In the process of sorting through investment and financing data, VCBeat identified an active insurance capital investor—Sunshine Ronghui.

It is reported that Sunshine Ronghui Capital, established in January 2015, is among the first private equity fund management companies in China’s insurance industry to be initiated and set up with insurance funds. With assets under management nearing RMB 30 billion, the firm primarily focuses on healthcare, emerging industries, and new consumer sectors.

According to incomplete statistics, 2In 2021, Sunshine Ronghui participated in investments in six healthcare companies, with its focus spanning medical consumables, biopharmaceuticals, healthcare informatics, and medical imaging. The investment rounds were primarily early-stage, such as Pre-A, Series A, and Series B.

Investment Deals in Healthcare Involving Sunshine Ronghui in 2021, Chart by VCBeat

Therefore,From the perspectives of track selection and timing of entry, Sunshine Ronghui appears to prefer early-stage involvement in “hard tech” projects.

This point has been somewhat corroborated in interviews related to Sunshine Fusion.

At the beginning of 2022, Sunshine Ronghui announced the first closing of its Innovation and Growth Fund II. After the new fund completed its final closing,Yangguang Ronghui has stated that it will continue to focus on structural opportunities in the healthcare industry, prioritizing clinical value, health economics, and industrial innovation and upgrading. It will also pay attention to trend-driven opportunities in breakthroughs of bottleneck technologies in the tech sector and innovations in domestically produced technologies.

However, three years ago, Sunshine Insurance Group’s investment strategy in the healthcare and medical sector was markedly different.

As revealed by Huang Shengxuan, Managing Director of Sunshine Ronghui Capital, in a 2018 interview, “Sunshine Ronghui’s DNA is that of an insurance capital investment platform, and its mission is to make life better. The way to achieve this is by focusing on consumption and service upgrades, moving from basic consumer needs to a more beautiful, healthier, and happier life. This also determines that Sunshine Ronghui’s investment focus will be on healthcare and consumer sectors, while avoiding traditional, manufacturing-oriented industries.”

Specifically in the field of healthcare,At that time, VCBeat focused its investment attention primarily on service-oriented and consumer-driven healthcare sectors such as dentistry, ophthalmology, and medical aesthetics. “Our investment strategy is to invest in ‘youth-oriented healthcare services’—shifting from traditional disease treatment to meeting demands for healthier and more beautiful lifestyles.”

According to Huang Shengxuan, Sunshine Ronghui is an insurance-capital-backed investment platform with a focus on late-stage investments; therefore, at that time, the companies it chose to invest in were all those that had established a leading advantage within their respective sectors.

“We would rather miss out than blindly invest in projects that are essentially bets on probability. We choose projects whose industrial trends are already well-established,” Huang Shengxuan stated at the time, emphasizing that Sunshine Ronghui places great importance on risk control. “Downside risks must be controlled; as long as we reduce the probability of failure, we already have a fifty percent chance of success.”

From today’s perspective, Sunshine Ronghui’s investment strategy in the healthcare sector has undergone a shift—moving from a preference for medical services to a focus on breakthroughs in core bottleneck technologies within the medical field.

Furthermore, it is worth noting that among cross-sector investors, there is one rather surprising entrant: Country Garden Ventures.

As a capital arm with its parent company in the real estate sector, Country Garden Ventures has not followed the traditional path of real estate companies entering healthcare through hospital acquisitions or Medical Mall development. Instead, it has focused on investing in “hard tech.”

Country Garden Ventures was established on January 4, 2019. In just three years since its inception, it has invested in over 60 companies and more than 90 projects, averaging 2.5 investments per month.

Furthermore, according to a January 2022 report by Zhitong Finance, among the companies invested in by Country Garden Ventures, 26 have reached valuations of US$1 billion, eight have reached valuations of US$10 billion, and ten have completed initial public offerings (IPOs).

Behind the swift execution and keen insight lies not only the substantial financial strength and industry resources provided by its parent company, Country Garden, but also the essential cultivation of capital expertise.

According to Niu Ruolei, Managing Partner of Country Garden Ventures, the firm has adopted the investment strategies of top-tier investors such as Sequoia Capital, Hillhouse Capital, and Tencent Investment since its inception, establishing four major investment themes and specific operational approaches.

The four major investment themes revolve around technology, health, consumption, and industrial chain advancement, extending into multiple sectors including semiconductors, carbon neutrality, broad healthcare, and new consumption. The specific strategy places greater emphasis on both early-stage and late-stage companies. This approach allows for early engagement with innovative enterprises while ensuring that mature projects in later stages are not overlooked, thereby guaranteeing comprehensive sector coverage, speed of execution, and overall success rates.

Specifically in the healthcare sector, according to incomplete statistics, Country Garden Ventures participated in investments in five medical companies in 2021, covering areas such as wearable devices, medical robots, cardiovascular consumables, IVD (in vitro diagnostics), and skincare products, overall demonstrating characteristics of hard technology.

Healthcare Industry Investments Participated in by Country Garden Ventures in 2021, Chart by VCBeat

Take the Series B2 financing round of Bluepha, led by Country Garden Ventures in August 2021, as an example.

Bluepha is a company dedicated to molecular and material innovation through synthetic biology technology. It focuses on designing, developing, manufacturing, and selling novel bio-based molecules and materials, thereby helping B2B clients across various industries such as consumer goods, food, healthcare, agriculture, and industry to achieve differentiated competition within their sectors.

andThis investment in Bluepha marked the official commencement of Country Garden Venture Capital’s foray into synthetic biology. In January 2022, Bluepha announced another round of financing, with Country Garden Venture Capital prominently listed among the investors, further underscoring its sustained attention to and confidence in China’s synthetic biology sector.

In addition to synthetic biology, the investment in YuanYe Tech also reflects Country Garden Venture Capital’s preference for hard-tech innovations within the healthcare sector.

Yuanye Technology is the first company in China to develop a muscle exoskeleton. Its world-first muscle exoskeleton system, which is more flexible, lightweight, and intelligent, can predict motion intent through motion capture, enabling the exoskeleton to closely synchronize with body movements and provide real-time, on-demand assistance to corresponding joints. This enhances the wearer’s physical performance, helping them execute intended movements more stably, effortlessly, and accurately.

Overall, compared with industry-chain capital, cross-industry capital involves more complex and diverse participants (including internet giants, insurance funds, real estate capital, and apparel brands) and follows markedly different investment logics: Internet giants focus on extending their core competencies and leveraging their advantages to build their own healthcare ecosystems; whereas cross-industry investors such as insurance funds and real estate capital show a stronger preference for “hard” sectors with favorable development trends and broad growth prospects.

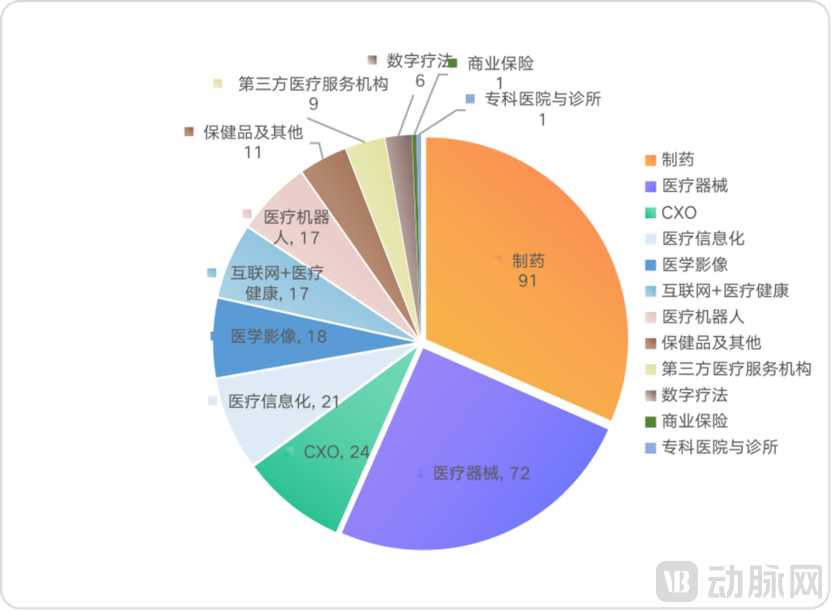

According to incomplete statistics from VCBeat, there were a total of 288 investment and financing events in the healthcare sector involving industrial capital in 2021. Among these, the pharmaceutical sector accounted for 91 events (including 70 in biopharmaceuticals, 19 in chemical pharmaceuticals, and 2 in traditional Chinese medicine); the medical device sector had 72 events; the R&D and manufacturing outsourcing sector had 24 events; the healthcare informatics sector had 21 events; the medical imaging sector had 18 events; the “Internet + Healthcare” sector had 17 events; the medical robotics sector had 17 events; the health supplements and other sectors had 11 events; the third-party medical service providers sector had 9 events; the digital therapeutics sector had 6 events; the commercial insurance sector had 1 event; and the specialized hospitals and clinics sector had 1 event.

Distribution Map of Industrial Capital’s Healthcare Investment by Sub-sector in 2021, Chart by VCBeat

As can be seen from the above data, in 2021, among industrial capital investments and financing in the healthcare sector, pharmaceuticals, medical devices, and contract research and manufacturing organizations (CRMOs) were the top three sectors favored by industrial capital.

After further refinement, what characteristics did industrial capital exhibit in investment and financing activities within the aforementioned three sectors in 2021?

Let's first look at the pharmaceutical sector.

According to the "2021 Global Biopharmaceutical Investment and Financing Report" released by VCBeat New Medicine, the small-molecule and large-molecule drug sectors gradually entered a bottleneck period in 2021. The primary drivers sustaining investment and financing growth in the biopharmaceutical sector in 2021 stemmed from frontier biotechnology tracks such as cell therapy, gene therapy, and nucleic acid drugs.

The report also points out that nucleic acid drugs represented by mRNA, cell therapies represented by TIL, TCR-T, and iPSC, gene therapies represented by gene therapy and oncolytic viruses, and large-molecule drugs represented by ADCs were the hot tracks in China’s biopharmaceutical sector in 2021.

Did investment and financing by industrial capital in the pharmaceutical sector also exhibit the same trend in 2021?

According to incomplete statistics, in 2021, industrial capital made a total of 13 investments in cell therapy, 7 each in small-molecule drugs and gene therapy, 3 in nucleic acid therapeutics, and 1 each in oncolytic viruses and antibody-drug conjugates (ADCs).

The above data indicate that, although the number of investment deals by corporate venture capital (CVC) in frontier biotechnology sectors—such as cell therapy, gene therapy, and nucleic acid-based drugs—is relatively small compared to the overall volume of financing and investment activities in the pharmaceutical industry, it is evident that CVC has already identified these emerging trends and begun to strategically position its investments accordingly.

Moreover, the amount of capital invested by industrial investors in the aforementioned hot sectors of the pharmaceutical industry is not to be underestimated.

The reason is that cell therapies, gene therapies, and nucleic acid drugs were all present in the pharmaceutical sector’s highest-value financing deals.

For example, Zhongshan Beisen Medical Industry Investment participated in the Series C financing of Alpha Regenerative Medicine, a developer and manufacturer of cell therapy products; Junshi Biosciences participated in the Series A financing of Zhi Shan Wei Xin, a gene drug research and development enterprise; and Sunshine Ronghui participated in the Pre-A round financing of Qichen Sheng Biotech, an innovative mRNA-based biopharmaceutical R&D company.

Beyond keenly capturing industry trends, what other characteristics have defined the investment activities of industrial capital in the pharmaceutical sector?

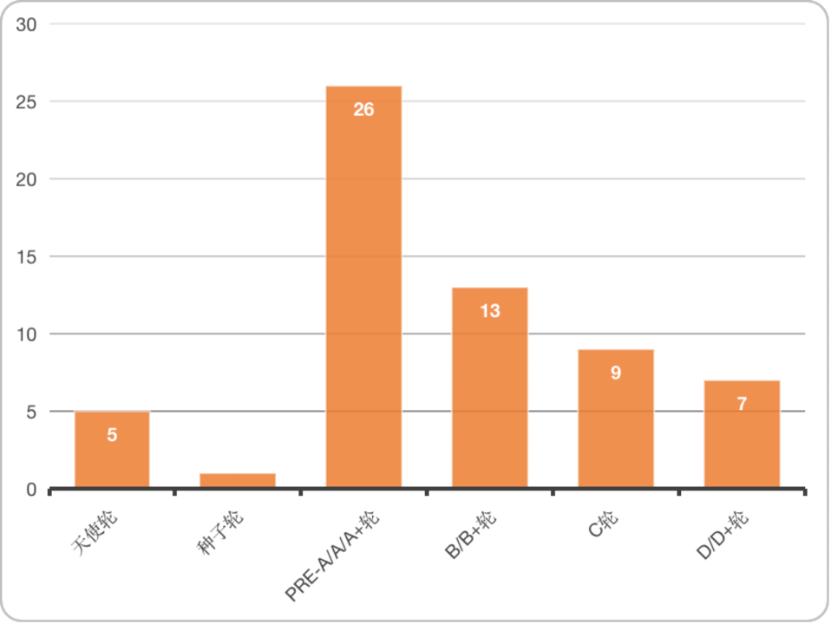

According to the 2021 investment and financing data in the pharmaceutical sector by industrial capital, the distribution of intervention rounds is as follows (a total of 61 public financing events): 5 angel rounds, 1 seed round; 7 pre-A rounds; 19 A rounds (including A+ rounds); 13 B rounds (including B+ rounds), 9 C rounds, and 7 D rounds (including D+ rounds).

As can be seen from the above data, in the pharmaceutical sector, industrial capital prefers to intervene at an early stage of projects, with Series A investments being the primary mode. This trend is largely consistent with the overall distribution of financing rounds across the biomedical industry.

Let’s now turn to medical devices.

According to 2021 industrial capital investment and financing data, IVD and consumer medical devices are the sectors preferred by industrial capital.

Among these, there were 28 industrial capital investment deals in the IVD sector and 15 in the consumer medical device sector; together, these figures already exceed half of the total number of industrial capital investment deals in the medical device industry in 2021 (72 deals). The number of investments in other sectors was as follows: 8 in cardiovascular consumables, and 21 in other consumables and equipment (including ENT, orthopedics, neuro-intervention, and minimally invasive surgery).

Furthermore,Notably, the primary source of industrial capital investing in the IVD sector is supply chain capital, whereas the main force behind investments in consumer medical devices is cross-industry capital.

The IVD sector has attracted significant attention from industrial capital, partly due to the industry’s unique characteristics: disease diagnosis and health management both generate substantial demand for IVD products. Particularly since the outbreak of the COVID-19 pandemic, Chinese IVD companies have not only expanded beyond their traditional boundaries but also gone global.

For example, as previously reported by VCBeat, BGI Genomics responded swiftly to the pandemic. It not only developed multiple test kits at the earliest opportunity and secured market access in numerous countries, but also rapidly enhanced testing capacity through its “Fire Eye Laboratory” total solution. In the first half of 2020, the company achieved a twofold increase in revenue and a sevenfold rise in net profit, successfully reversing its prior profit stagnation.

In the current era of normalized COVID-19 prevention and control, IVD companies are also contemplating their future direction. Mergers and acquisitions, partnerships, and expansion into overseas markets have become the primary avenues for most IVD enterprises to achieve breakthroughs.

External investment to establish a presence across the entire industrial chain is also one of the strategic directions being explored by leading IVD companies.

For example, in November 2021, Mingde Biology invested tens of millions of RMB in Nanjing Nuoyin Biology, a molecular diagnostics company that had been established for only one year at the time.

What was the rationale behind the investment? VCBeat found the answer in an external investment announcement by Mingde Biology.

Founded in 2020, Nuoyin Biology has built its core around two cutting-edge technology platforms: multiplex PCR and metagenomic next-generation sequencing (mNGS). The company has independently developed comprehensive solutions for the rapid detection of common pathogens and the thorough diagnosis of critical and severe infections. Leveraging a suite of breakthrough technologies—including proprietary cell lysis-based nucleic acid extraction, multiplex PCR primer design algorithms, and picogram-level nucleic acid amplification—Nuoyin Biology demonstrates exceptional capabilities in pathogen detection.

Through this investment, Mingde Bio not only enhances its product portfolio of in vitro diagnostic instruments and reagents but also leverages its channel and resource advantages to accelerate the R&D, regulatory registration, and rapid growth of Nuoyin Biotech’s pathogen detection business. By acquiring molecular diagnostic technologies such as multiplex PCR and high-throughput sequencing, Mingde Bio can swiftly increase its market share in pathogenic microorganism molecular diagnostics, expedite its strategic layout of pathogen detection products in the molecular diagnostics sector, and solidify its position in the in vitro diagnostics market.

On the other hand,The Advent of Centralized Procurement: Some Lament, While Others See Opportunity.

For instance, relevant media outlets have expressed optimism, viewing centralized procurement as a strategy of exchanging volume for price. With Anhui Province’s procurement cycle set at two years, winning bidders will secure 80% of the previous year’s usage volume, thereby boosting product sales for these companies. Furthermore, the article points out that as the trend of centralized procurement for in vitro diagnostics (IVD) takes hold, the value of an increasing number of new technologies and new test items will be recognized. In the future, more innovative IVD companies will receive support from industrial capital and venture investment.

Therefore, beyond industry-specific factors, the opportunities embedded in the centralized procurement of in vitro diagnostics (IVD) may also be one of the reasons it has attracted favor from industrial capital.

According to incomplete statistics from VCBeat, in 2021, the enthusiasm for medical aesthetics remained undiminished across the entire consumer healthcare investment community. Moreover, this fervor extended into the realm of industrial capital within the consumer healthcare sector.

Notably, apart from Pre-C round investor iBeauty Qingshi (co-founded by iBeauty Medical) and other investors belonging to the industrial chain capital for clear aligner developer Zhengli Technology, all other investors in consumer medical devices are cross-industry capital.

For example, one of the investors in Synapse+, a developer and manufacturer of wearable devices, is Xiaomi Group; Qingzhi Keyan, an oral health care brand, is backed by Inke, a mobile live-streaming platform; Zongjiang Technology, a manufacturer of beauty instruments and equipment, has Tencent as its strategic investor; and CosBeauty, a developer of home-use beauty devices, saw its Series B+ round led by Xiaomi Group.

Finally, we turn our attention to the CXO sector.

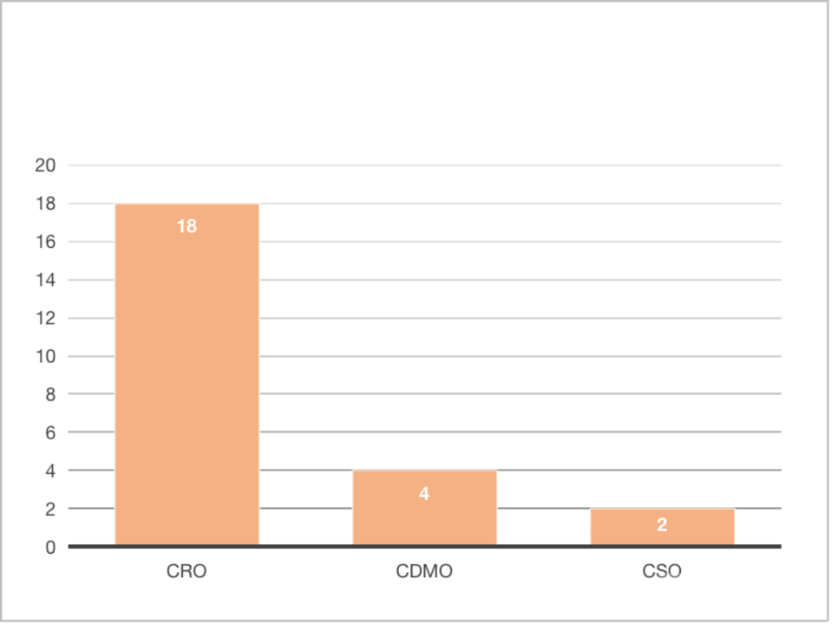

Upon review, VCBeat found that in 2021, among the 24 CXO investment and financing deals by industrial capital, the focus was primarily on the CRO sector, with 18 deals, followed by CDMO with 4 deals, and CSO with 2 deals.

Furthermore, in 2021, industrial capital investments in the CXO sector were primarily made at the early stages of projects.

Among the 17 investment activities that clearly disclosed the funding rounds, there were three angel rounds, three Pre-A rounds, six Series A rounds, two Series A+ rounds, and one each for Pre-B, Series B, and Series D rounds.

Additionally,Notably, from the perspective of participating capital, industry chain investors still account for the majority, with a total of 16 deals. In contrast, there were only eight financing and investment deals involving cross-industry capital, which were mostly led by well-funded internet giants such as ByteDance and Tencent, as well as insurance funds like PICC Capital.

Why Do CROs Remain a Hotspot in Industrial Capital Investment and Financing Activities?

The underlying reasons are inextricably linked to the investment and financing environment as well as the R&D landscape for China’s biopharmaceutical industry.

From the perspective of the investment and financing environment, in April 2018, the Hong Kong Stock Exchange introduced a listing regime for pre-revenue biotechnology companies (Chapter 18A); in July 2019, the STAR Market was launched, which also includes the fifth set of listing criteria applicable to companies with products not yet commercialized. As a result, biotech firms have established a complete capital cycle encompassing venture capital (VC), private equity (PE), and initial public offerings (IPO).

Moreover, according to relevant reports from Changjiang Securities on the CRO industry, investment and financing in China’s primary market have been continuously recovering over just three years. In 2018, China’s biopharmaceutical sector witnessed a peak in financing; although it declined somewhat in 2019, financing in this sector has been gradually rebounding in 2020 and 2021.

From the perspective of the R&D environment, according to the aforementioned report, as pharmaceutical reforms in China gradually enter deeper waters, domestic pharmaceutical companies are continuously increasing their investment in innovative R&D, leading to a significant rise in the number of Investigational New Drug (IND) applications and newly initiated clinical trials in China. In 2020 and 2021, the number of IND applications for Class 1 new drugs in China achieved year-on-year growth rates of 65% and 61%, respectively, indicating a marked acceleration.

Therefore, against the backdrop of strong investor preference for biomedicine in the primary market and an increasingly pronounced emphasis on R&D among domestic pharmaceutical companies, the CRO industry remains robust, brimming with immense opportunities and thereby attracting substantial investment from industrial capital.

A review of industrial capital’s investment activities in the healthcare sector in 2021 reveals that the primary participants remained largely unchanged. These included both industry-specific capital from within the healthcare supply chain itself and cross-industry capital from other sectors, such as real estate and insurance.

From an investment logic perspective, the approach of industrial chain capital is relatively straightforward—leveraging their inherent advantages to integrate industry resources and optimize industrial layout. In contrast, cross-sector capital employs a more diversified investment strategy, primarily focusing on the “hard tech” sector, while also showing a slight inclination toward the “consumer healthcare” segment.

In terms of popular sectors, pharmaceuticals, medical devices, and CXO were the top three most favored by industrial capital in 2021. Consistent with the overall investment and financing trends in healthcare, industrial capital primarily entered the pharmaceutical sector at Series A rounds. Some industrial investors also keenly identified hot trends in pharmaceuticals—such as cell therapy, gene therapy, and nucleic acid drugs—and began making corresponding strategic investments. In the medical device sector, in vitro diagnostics (IVD) was the most favored by industrial capital, followed by consumer medical devices. Data from 2021 shows that IVD was the main battlefield for industry-chain capital, while consumer medical devices attracted cross-industry capital, particularly from companies like Xiaomi. In the CXO sector, CROs were the most preferred segment, with participation dominated by industry-chain capital. Even when cross-industry capital was involved, it mainly came from well-funded internet giants or insurance funds.

Reviewing the past, understanding the present; as for how the future will unfold, please stay tuned.