Three AI Medical Firms Go Public, Seven File Prospectuses, and Industry Leaders Report Surging Revenues: Is the AI Healthcare Profitability Era Here?

Last year, medical AI remained brilliant yet was marked by mixed fortunes.

That year, IBM’s “Watson Doctor” (Watson), once hailed as the “spark igniter” of AI in healthcare, faded into obscurity. It was also the year that the AI healthcare sector weathered the capital winter and approached the eve of initial public offerings (IPOs). Airdoc, Yidu Tech, and Jiahe Meikang successfully went public, with the head effect beginning to emerge. Deepwise and Winning Health respectively acquired Yitu Technology and Chuangye Huikang (Winning Health and Chuangye Huikang “terminated their merger”), marking the onset of mergers and acquisitions among enterprises.

It is evident that the commercialization of AI in healthcare has achieved a breakthrough from zero to one, with the sector gradually maturing. The submission of prospectuses by leading companies has further enabled the disclosure of real operational data from the AI healthcare industry, which had long remained a “black box,” thereby clarifying its application prospects, commercialization pathways, and technological development directions.

The Dawn of Large-Scale Commercialization in AI Healthcare Appears to Be Becoming a Reality.

However, risks persist. The adage “a large ship is hard to turn” has long illustrated the principle that even minor changes can trigger significant repercussions in a scaled-up development context. As the industry matures, practitioners should remain increasingly cautious and rational.

For the AI healthcare industry, which has one foot in the door of an IPO, many issues remain unresolved, such as the difficulty in achieving break-even and unclear business models.

Drug R&D, medical imaging, and health informatics constitute the primary domains of AI in healthcare. This article analyzes companies that have filed prospectuses for AI-based medical imaging solutions, aiming to gain insights into the future trajectory of AI healthcare through this specific segment.

Surge in Revenue, Widespread Narrowing of Losses

Artificial intelligence is a capital-intensive business, and losses remain a lingering cloud over the AI healthcare sector. In the field of AI medical imaging, whether it is Airdoc, which gained an early-mover advantage, or other companies striving for listings on the Hong Kong Stock Exchange, the series of figures disclosed in their prospectuses all reveal the reality of corporate losses.

Despite multiple rounds of industry discussion on how AI companies can achieve profitability, the “curse” of losses appears difficult to break. The withdrawal of Watson Health serves as a testament to this reality.

Fortunately, AI has cleared the hurdle of registration and market access overseen by the National Medical Products Administration (NMPA).

Since the first Class III medical device registration certificate was granted to an AI medical imaging product in 2020, regulatory approvals for such products have continued to increase, with multiple companies securing successive approvals for their respective offerings.The successful navigation of the approval process has become the core driver enabling AI medical imaging companies to achieve exponential revenue growth, laying the foundation for artificial intelligence enterprises to turn losses into profits.

Approval Status of Class III Medical Device Certificates for AI Medical Imaging Products

Data source: Artery Orange Database

Last year, Airdoc, Keya Medical, Infervision, and Shukun Technology, all players in the AI medical imaging sector, made a push for listings on the Hong Kong Stock Exchange. An examination of the prospectuses filed by these companies revealsIt can be seen that the sales revenue of most companies in the AI medical imaging sector has doubled.

Sales Revenue of Companies in the AI Medical Imaging Sector That Have Filed IPO Prospectuses

(Growth rate calculated based on sales revenue in 2020 and 2019)

Data Source: Prospectuses of Various Companies

Data shows that Airdoc’s full-year revenue in 2020 increased significantly compared to 2019. In the first half of 2021 alone, the company’s sales reached RMB 49.477 million, surpassing its total revenue for the entire year of 2020. Infervision achieved a year-on-year growth rate of 318.3%. Shukun Technology’s sales volume increased 31-fold in 2020, and its revenue in the first half of 2021 exceeded RMB 50 million.

Losses are a fact, but with the approval process being streamlined and policies promoting high-quality development in public hospitals advancing AI adoption, revenue has surged and losses are generally narrowing.

However, the resolution of regulatory approval challenges does not mean that the commercialization of AI medical imaging has been fully validated.Approval for registration and market access merely signifies that the AI is permitted to enter the healthcare market and be sold outside the hospital system.

Dr. Zheng Yefeng once stated, “From the perspective of the overall AI industry, there are certain issues with both the business models and technological capabilities of AI. The commercialization of medical AI in the United States has been highly successful, with many AI products gaining reimbursement approval. This is partly because equipment fees and diagnostic fees for radiological examinations are billed separately in the U.S., where labor costs are particularly high. In contrast, in China, radiological examination fees are relatively low, not itemized separately, and predominantly consist of equipment charges. This explains why AI solutions in the U.S. can currently be billed and reimbursed as independent services.”

Therefore,For AI-powered medical products to achieve large-scale commercialization, they must secure pricing approvals and health insurance reimbursement eligibility, thereby attracting a broader user base willing to pay for these solutions.

Commercialization and R&D Investment Continue to Increase; Turning a Profit Will Take Time

Faced with the “bottleneck period” in the AI race, Fourth Paradigm founder Dai Wenyuan once raised a thought-provoking issue: AI has reached a new tipping point—after being implemented across various industries, how can it bring about qualitative transformation for enterprises?

This question metaphorically reflects the current predicament of AI companies and also reveals the approach to solving the problem—bringing about qualitative change.

What remains for AI companies is to identify the irreplaceability of this technology.To identify new growth opportunities and market entry points, it is essential to leverage artificial intelligence as a strategic tool, enabling healthcare institutions to achieve a qualitative leap driven by quantitative advancements. This ensures that AI becomes an indispensable, rather than optional, component of healthcare delivery. This transformation is the key for AI enterprises to turn losses into profits.

However, to achieve profitability, AI companies still need to overcome at least two major hurdles.

First,Companies need to continuously achieve technological breakthroughs, strengthen their pipeline layout and R&D efforts to identify new growth opportunities, and ensure profitability amid significant investments.

Second,AI companies must also address the challenge of low market penetration. To achieve large-scale commercialization, AI solutions must sequentially obtain regulatory approval for registration, pricing approval, and inclusion in medical insurance coverage.

This means that as medical AI products gain approval one by one, companies will accelerate commercialization while simultaneously expanding their product pipelines. Sales and marketing expenses, along with R&D costs, will continue to rise, making upfront strategic investments seemingly unavoidable. Consequently, it remains challenging for AI healthcare enterprises to achieve profitability in the short term.

The financial data on sales and R&D investment disclosed in the aforementioned companies’ IPO prospectuses further corroborate this view.

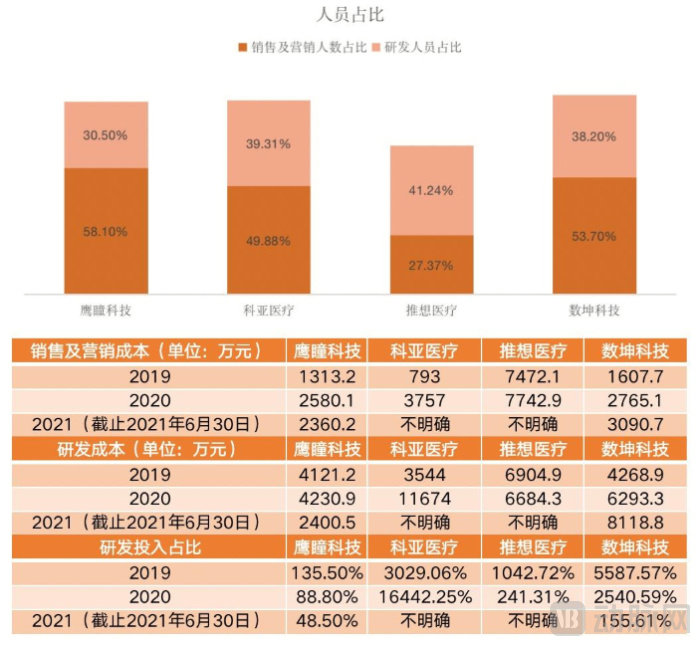

By analyzing the risk factors disclosed in the prospectuses of Airdoc, Keya Medical, Infervision, and Shukun Technology, we found thatWhen addressing the question of whether they can generate profits from operating activities in the future, companies primarily attribute their potential success to the successful development of pipeline products, regulatory approvals, portfolio success, and commercialization.At this stage, R&D and sales are the focal points for AI medical imaging companies, which are channeling investments into these two areas to overcome technical and commercialization challenges, with the aim of achieving a qualitative leap.

Source: Prospectuses of respective companies

Between 2019 and 2020, Airdoc’s R&D costs increased from RMB 41.212 million to RMB 42.309 million, while its R&D intensity decreased from 135.5% to 88.8%; Keya Medical’s R&D costs rose from RMB 35.44 million to RMB 116.74 million, with its R&D intensity continuing to climb from 3,029.06% to 16,442.25%; Infervision’s R&D costs declined from RMB 69.049 million to RMB 66.843 million, and its R&D intensity dropped sharply from 1,042.72% to 241.31%; Shukun Technology saw an increase in R&D costs, while its R&D intensity was nearly halved, decreasing from 5,587.57% to 2,540.59%.

From a commercialization perspective, with the exception of Infervision, Airdoc, Keya Medical, and Shukun Technology all have a higher proportion of sales personnel than R&D staff, while their sales and marketing costs have been rising year by year.

Through the financial data of various companies, it can be seen thatWith the AI approval process successfully streamlined, products are gradually maturing. As hospitals’ acceptance and awareness of AI technologies continue to rise, companies need to participate in various exhibitions and academic conferences during the early sales phase to identify potential clients and make commercial investments centered on an increasingly rich and mature product pipeline. Meanwhile, by engaging deeply with hospitals to assess their needs and enhance product penetration, enterprises can strive to rapidly capture market share in the initial commercialization stage, achieving multiplicative revenue growth. This will also lay a solid foundation for future AI enterprises in securing pricing approvals and inclusion in medical insurance coverage.

Technical issues are somewhat linked to the commercialization challenges of AI.

Dr. Zheng Yefeng once stated, “Judging from the AI products currently approved by the NMPA, AI can only address specific, limited issues. AI with single-point functionality may not necessarily reduce physicians’ workload and could even prove counterproductive. In other words, AI requires comprehensive development and all-around upgrades.”

Despite the decline in R&D expenditure as a percentage of revenue driven by enhanced corporate commercialization capabilities, most companies have still seen an increase in absolute R&D costs.

According to industry insiders,: “Products are the core competitiveness of an enterprise. To enhance its future self-sustaining growth capability and achieve scalable profitability, a company must inevitably build a robust product pipeline as support. However, the process from research and development to commercialization takes approximately two years, which means that product R&D will always be ongoing, and the company’s absolute investment in this area will inevitably continue to increase.”

Therefore, we can anticipate that AI companies will continue to increase their investments in commercialization and product development. For the AI healthcare sector, achieving profitability may still take some time.

Where Does the Path to Large-Scale Commercialization Lie?

According to Frost & Sullivan data, the market size of AI medical imaging will continue to grow in the future, and is expected to reach RMB 50.01 billion by 2030. It can be seen that with the increasing awareness of artificial intelligence among medical institutions, the revenue scale of AI in medical imaging may experience exponential growth within ten years.

Source: Airdoc’s Prospectus

However, from a practical standpoint, if the industry continues to operate solely under the traditional model of hospitals making one-time purchases of medical AI software, it will remain difficult to achieve exponential growth in revenue scale. AI enterprises need to identify new sources of growth potential.Inclusion in pricing catalogs with billing based on the number of diagnoses, along with the development of parallel new application scenarios, may become viable means to help artificial intelligence companies effectively scale up.

So, as we enter the era of pricing approval and medical insurance reimbursement listing, how should the business models of AI companies currently in the market access phase adapt? We can analyze this by examining the current models of four companies: Airdoc, Keya Medical, Infervision, and Shukun Technology.

Airdoc integrates hardware, software, algorithms, and services to provide comprehensive solutions. Its product portfolio consists of three main components: Artificial Intelligence Software as a Medical Device (SaMD) for detection and assisted diagnosis, health risk assessment solutions, and proprietary hardware devices.

In August 2020, after Airdoc-AIFUNDUS (1.0) obtained the Class III medical device certificate from the National Medical Products Administration, Airdoc Technology embarked on its commercialization journey and began generating revenue in the first quarter of 2021. In January this year, Airdoc Technology’s registration application for standalone medical device software for cataract detection was approved, further bolstering its product R&D capabilities and continuing its commercialization efforts.

Overall, Airdoc has built its competitive advantages from two aspects:

First, it lies in the self-developed deep learning algorithms that are widely applicable to the detection and diagnosis of various chronic diseases. This not only lays the foundation for Airdoc’s product R&D capabilities and regulatory approvals but also further raises the entry barriers for the industry.

Second, the product’s diverse application scenarios empower the company with strong commercialization capabilities. Airdoc’s product pipeline primarily supports the diagnosis of diseases such as diabetic retinopathy and hypertensive retinopathy. This extensive portfolio creates a wide range of implementation scenarios, enabling Airdoc to meet the varied healthcare service needs of hospitals, community clinics, health examination centers, insurance companies, optometry centers, and pharmacies. Furthermore, collaborations with this broad customer base help expand the company’s real-world user database, establishing a feedback loop that facilitates the optimization of existing algorithms and the development of new ones.

Airdoc, by simultaneously addressing commercialization scenarios and data barriers, has built a virtuous cycle. With its product lines integrated, what lies ahead for Airdoc may well be a larger AI medical imaging ecosystem.

Although Keya Medical’s sales revenue did not show significant growth last year, this may only be the tip of the iceberg. Data such as revenue figures and the proportion of R&D investment clearly indicate that Keya Medical adopts a different strategy from its peers. Instead of starting with AI development for pulmonary nodules and fundus imaging, where public data is abundant, Keya Medical has directly delved into the cardiovascular and cerebrovascular fields.

From the perspective of its product portfolio,Keya Medical designs and develops a comprehensive portfolio of products covering the entire patient care journey, from early screening, diagnosis, and treatment to post-treatment rehabilitation., and establish an AI medical device platform encompassing R&D, manufacturing, and commercialization capabilities. Meanwhile, Keya Medical has designed a suite of deep learning-based medical device products and products under development to address the unmet clinical needs of patients with cardiovascular diseases. Currently, multiple Keya Medical products have been submitted for NMPA registration review, while the company continues to expand the indications for its DeepVessel Stroke Intelligent Imaging Analysis System.

On the other hand, after receiving NMPA approval for its CT-FFR DeepPulse Fraction, Keya Medical took the lead in applying for pricing reimbursement approval, aiming to provide AI-driven medical services directly to patients through hospitals.

Infervision’s core lies in developing and deploying hospital-wide AI medical products, serving physicians across multiple departments to enable disease screening, diagnosis, intervention, treatment, management, and research, with a particular focus on lung cancer therapy.

In fact, Tuixiang has established a matrix comprising 15 medical AI products.

From the perspective of its product pipeline layout, it is expanding its product capabilities both horizontally and vertically to capture a larger target market.

Overall, Infervision’s strength lies in its diversified product portfolio.By conducting in-depth R&D on its flagship product, the AI pulmonary nodule detection system, Infervision has secured a first-mover advantage, obtained regulatory approvals in multiple countries, and successfully achieved commercialization. Building on this foundation, the company has expanded vertically to explore the value of AI in screening for liver cancer, breast cancer, pneumonia, tuberculosis, stroke, and other diseases. This strategy creates synergies for its R&D and commercialization efforts, reinforcing Infervision’s first-mover advantage in the AI medical device industry.

Leveraging its first-mover advantage, Tuixiang Medical will undoubtedly capture a larger market share, further enhancing the deep learning capabilities, product performance, and market penetration of its offerings.

Shukun Technology has a platform-based vision for imaging AI: the "Digital Human."

In addition to offering individual advanced products targeting specific therapeutic areas, the company also provides “platform-based products” comprising one or more standalone products from its pipeline. If a single product gains adoption and validation in a therapeutically challenging area with high technical barriers, it can earn physicians’ brand recognition and trust in the company’s technological capabilities. Hospitals will then be more inclined to continue using the company’s related products in other therapeutic areas. Shukun Technology’s extensive product portfolio built around the human body, combined with its platform-based product strategy, creates commercialization opportunities for other products in its lineup. This approach helps activate the existing customer base, generating recurring revenue, while rapidly expanding the customer base through innovative products.

Shukun Technology's product pipeline is being progressively refined, while the company continues to expand into overseas markets.

From the development models of the four companies that have submitted their prospectuses,All four companies have established overseas operations. This not only helps diversify risks associated with reliance on a single market, but also enables them to secure early market access, laying a solid foundation for leveraging their technological and pricing advantages. Such global presence will undoubtedly provide stronger support for future corporate development and revenue growth.

In terms of product R&D, companies continue to strengthen the competitiveness of their core products while expanding their product pipelines and accelerating regulatory approvals, with the aim of building a more comprehensive ecosystem. On another front, these enterprises have established their own closed-loop systems, leveraging their core competencies as the central axis to explore additional commercialization scenarios. In commercialization, all four companies have made significant strides; by advancing product development and market access, they are continuously creating richer application scenarios, thereby opening up new value spaces for future revenue growth.

Final Remarks

Witnessing AI medical imaging and healthcare big data overcome hurdle after hurdle, moving from a chaotic phase to the eve of an IPO sprint; listening to the melodies of listings and mergers and acquisitions being played out; and seeing artificial intelligence achieve its zero-to-one breakthrough in commercialization—much like witnessing the moment when stars begin to shine—amply demonstrates the achievements made by AI medical imaging along its journey.

However, as AI in healthcare enters the era of price approval and national medical insurance reimbursement, critical questions remain: how should companies adapt their business models, and how can they identify the tipping point where returns exceed investments to achieve a qualitative leap driven by quantitative accumulation?

For the AI industry, which is still in a growth phase, the R&D input-output ratio remains unimpressive due to factors such as the research ceiling in neural networks within academia, limited capacity for converting industrial talent into productivity, and the need for continued investment in early-stage market education. Meanwhile, current products largely focus on risks associated with specific diseases rather than achieving multi-disease coverage, thereby failing to realize “closed-loop value.” These constraints have made it difficult for AI to break the “curse” of financial losses.

However, judging from the development of product pipelines and adjustments to commercial strategies across various companies, practitioners have clearly identified their direction. While expanding the range of diseases covered by their products, they are also striving to broaden their market segments. From in-hospital treatment and surgical planning to broader health and wellness scenarios, they are exploring the wider possibilities of artificial intelligence (AI). At the same time, extensive collaborations with enterprises are being established to rapidly expand the scope of AI applications through integrated hardware and software solutions. A profitable future may well be within reach.

A practitioner with over a decade of experience in the AI field told VCBeat: ““Many products currently on the market may not yet provide users with ‘closed-loop value’ in specific scenarios, particularly in terms of functionality. However, as future products become more deeply integrated into specific scenarios, their business models will gradually become clearer.”

With the accelerated approval of AI medical imaging products, breakthroughs in bottlenecks, and corporate IPOs, artificial intelligence has undoubtedly entered a new era.