Top 10 Leading Investment Firms Survey: These Medical Sub-sectors Set to Boom in 2022

As the Year of the Ox comes to a close and the Year of the Tiger begins, the healthcare and wellness industry has turned a new page amidst this transition.

As we usher in a new year, countless individuals begin to envision, plan, and take action, all seeking answers to the same question:

Where Are the Opportunities in the Healthcare and Wellness Industry in 2022?

This is because the overall market sentiment in the industry cooled last year, the pace of primary market activities slowed down, IPO companies frequently broke their issue prices, and the market capitalization in the secondary market evaporated by nearly 400 billion yuan. Many projects that relied on concept hype gradually exited the scene.Amidst this great upheaval, industry participants seek to understand the new trends in order to re-anchor their value coordinates.

As deep participants in the industry, investors in the healthcare and wellness sector are undoubtedly among those most sensitive to the ebb and flow of market trends.

After conducting surveys with ten leading investment firms—Aurora Venture Capital, Changling Capital, Hillhouse Ventures, Huagai Capital, China Renaissance, Matrix Partners China, Mingfeng Capital, SoftBank China, Shenzhen Capital Group, and Joy Capital (listed in alphabetical order by pinyin)—VCBeat has found that the underlying logic of the healthcare and wellness industry is undergoing new evolution, with a structural opportunity beginning to emerge.

Next, this article will reveal the logical threads behind this transformation from both macro and micro perspectives, as well as the investment trends in 2022.

Next, you will learn:

1. Macro Trends: A Gold Rush in Early-Stage Healthcare Projects, with Scientists Becoming Highly Sought-After;

2. Investment Rationale: The viability of the project's industrialization prospects and business logic is key;

3. Biopharmaceutical Sector: Synthetic biology, cell and gene therapy are highly favored; global competitiveness is the core focus;

4. Innovative Medical Devices Sector: The cardiovascular track remains highly active, while niche segments such as ophthalmology and medical aesthetics are emerging rapidly;

5. Digital Healthcare Sector: Digital therapeutics and insurtech emerge as hotspots, with commercial monetization capability serving as a key test factor;

6. Medical Services Sector: Critical and Emergency Care Specialties Enter a Period of Opportunity, with Online-Offline Integration Becoming Essential.

In 2021, “there is a shortage of professors and scientists” became a widespread consensus among investment firms.

Since the beginning of last year, a large number of investment institutions have begun seeking out projects led or participated in by professors and scientists. At the peak of this trend, it was not uncommon to witness the rare spectacle of dozens of firms fiercely competing for a single professor-led project.An investment manager stated that he spent over half a year visiting various research institutes to connect with experts across different fields, thereby facilitating the acquisition of early-stage equity when they decide to launch startups.

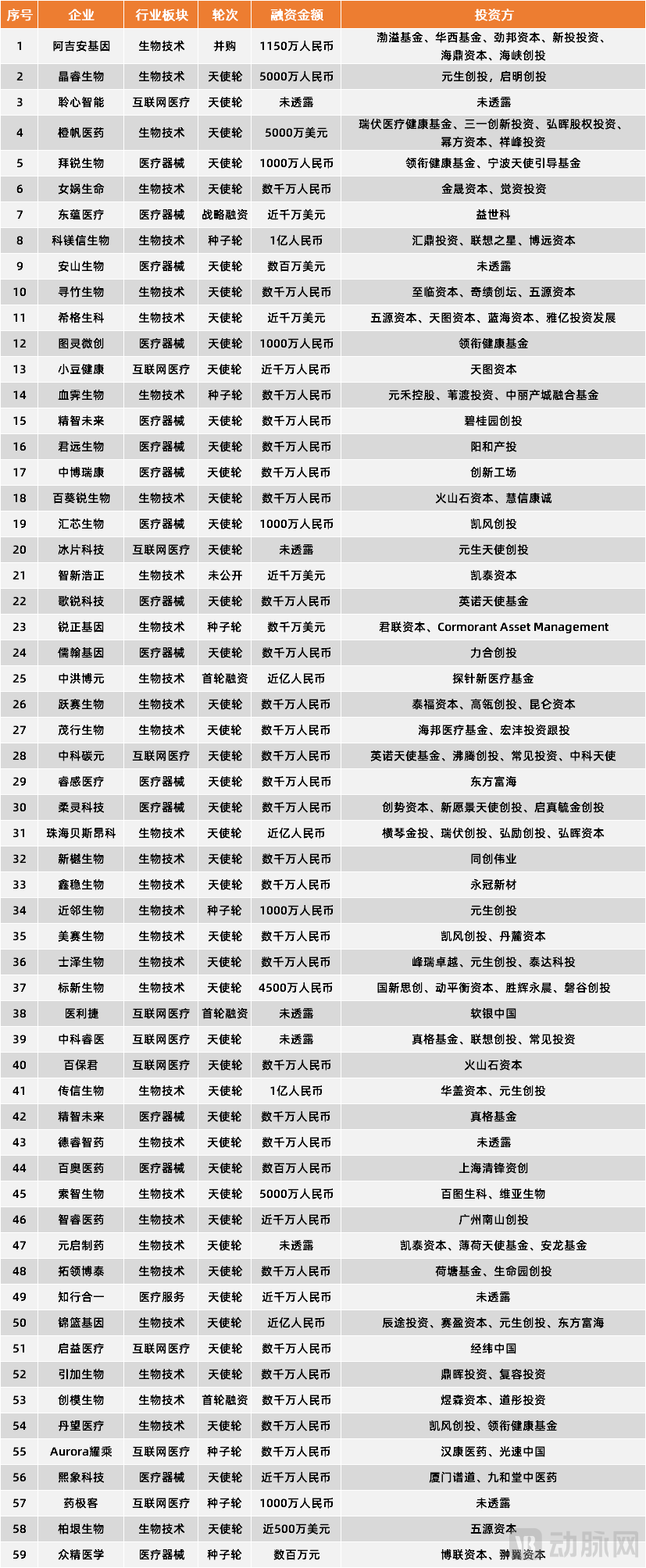

The data offers a glimpse into investors’ enthusiasm for early-stage projects. According to statistics from VCBeat’s Orange Fruit Bureau,In 2021, a total of 59 early-stage investment and financing events (seed and angel rounds) occurred in China’s healthcare sector., with total financing reaching a record high of RMB 2.5 billion.

(Table of Early-Stage Project Financing Events in 2021, compiled by VCBeat)

In this process, star startups founded by scientists have played a demonstrative role, thereby driving this trend. For instance, Wang Xiaodong, founder of BeiGene—the first domestic biopharmaceutical company to achieve triple listing on the U.S., Hong Kong (H-share), and mainland China (A-share) stock exchanges—serves as Director of the National Institute of Biological Sciences, Beijing. Additionally, Dr. Shi Yigong, an academician of the Chinese Academy of Sciences, is the co-founder behind InnoCare Pharma, which recently filed its prospectus for a secondary listing on the STAR Market.

“Beyond the national policy incentives that have led to growing emphasis on foundational innovation, another key factor driving investors toward early-stage opportunities is the valuation inversion between primary and secondary markets, which has made it increasingly difficult for late-stage investment firms to generate profits,” Song Gaoguang, Partner at Northern Light Venture Capital, told VCBeat.The earlier the stage, the greater the risk.”

Hillhouse is also heavily betting on this path. Hillhouse Ventures has invested in 10 startups in the field of synthetic biology, more than half of which are founded by scientists or are projects for the commercialization of scientific achievements. As their earliest investor, Hillhouse can be described as the “first love” of scientist-founded startups. “Putting scientists in the spotlight and becoming their best co-creation partner” has become its ongoing mission.

“Huagai Capital has always placed great emphasis on early-stage investment and has recently upgraded and refined its strategies and service capabilities for such investments,” said Xu Xiaolin, Chairman and Founding Partner of Huagai Capital. “Last year, we completed the fundraising for our healthcare early-stage fund, raising RMB 800 million. With a portfolio that includes early-stage funds, growth funds, and PIPE funds, Huagai Healthcare has initially established a ‘full-stage + full-industry-chain’ investment layout, enabling us to provide continuous support to innovative enterprises at every stage of their development.”

Matrix Partners China is also ramping up its efforts. Last December, it announced the launch of “Matrix Sci-Tech Innovation Hub,” aiming to make its empowerment initiatives more practical and substantive. The platform provides scenario-based guidance for founders with research or technical backgrounds in the healthcare sector, addressing common startup challenges such as equity and stock options, fundraising, business models, talent development, organizational structure, and macroeconomic trends.

“We have observed that investors are actively shifting their focus toward ‘investing early, investing in small-scale ventures, and investing in technology.’ In addition to traditional healthcare venture capital firms, some large buy-side investors that previously focused primarily on the private equity stage have also begun to engage in early-stage projects,” said China Renaissance’s Healthcare and Life Sciences Division to VCBeat.

The influx of capital into the market has prompted a large number of scientists and professors to leave research institutes and universities to embark on entrepreneurial ventures, thereby enriching the investment pipeline in the primary market and accelerating the commercialization of medical research achievements.

Yet even under such circumstances, scientists and professors remain in short supply, gradually giving rise to greater investment risks.

“Not every professor and scientist can become an outstanding entrepreneur,” an investor who wished to remain anonymous told VCBeat. “The current market fervor has spawned numerous so-called emerging niche sectors, yet very few projects are truly capable of industrialization and commercialization.”

Song Gaoguang, a partner at Northern Light Venture Capital, also noted that as investment firms flock to early-stage projects, the scientific risks faced by investors are rising rapidly. “Within less than two years, the average valuation of early-stage rounds in this sector has increased three- to fourfold, while business progress has not shown a corresponding trend. Therefore, I believe that over the next two to three years, institutions investing in early-stage companies may face higher risks than those currently investing in mid-to-late stage projects. This could even lead to a significant number of technology-based companies failing, particularly in the biopharmaceutical field, which is characterized by long and challenging translation cycles. Hence, investment institutions must become more specialized.”

In the face of the current situation,How to better serve scientists and professors, and improve the success rate of early-stage projects, became a common concern for investment institutions in 2022.

From the perspective of multiple investors, there are three major core pain points for professors and scientists starting businesses.

First, scientific research achievements and commercial successes belong to two distinct systems; once one enters the industry, a shift in mindset is required.

Second, most professors and scientists find it difficult to devote themselves full-time to entrepreneurship, as they cannot completely disengage from their official duties in universities and research institutions.

Third, managing and communicating with startup teams poses a significant challenge for professors and scientists.

In response, investment institutions are each building new service systems tailored to their unique characteristics.

"For instance, Aurora Venture Capital places particular emphasis on post-investment value creation. 'Our strategy is to invest early, invest in high-potential ventures, and invest in differentiated opportunities. In terms of post-investment support, we conduct extensive in-depth work for early-stage projects, such as helping companies optimize their teams, establish product lines, and connect with upstream and downstream partners as well as local government resources, thereby growing alongside our portfolio companies,' stated Song Gaoguang."

“As one of the pioneers among state-owned capital players in the venture capital community, we are able to provide strong endorsements for our portfolio companies through our established relationships with local governments and within the financial system. For early-stage projects, Shenzhen Capital Group (SCGC) has continuously increased its investment and service efforts in recent years, offering comprehensive support in areas such as corporate operations management, capital market access, and industrial ecosystem synergy. We emphasize the principle of ‘30% investment, 70% service,’ leveraging SCGC’s large platform as a central hub to efficiently connect with various resource partners and jointly build an entrepreneurial and venture capital ecosystem with powerful empowerment advantages,” said Lin Guanyu, Investment Director of the SCGC Hongtu Healthcare Industry Fund.

Hillhouse has established a platform for the commercialization of scientific research outcomes, linking industrial and investment resources with technological R&D, and has initially formed market-oriented mechanisms for talent attraction and development. Additionally, it has created the DVC (Deep Value Creation) system, which bundles various post-investment services for entrepreneurs and scientists into a toolkit to achieve deep empowerment. This includes seven service capabilities: global executive search, digital transformation, lifelong learning platforms, innovation ecosystem resources, M&A/strategic empowerment, lean manufacturing, and supply chain management.

Post-investment enablement should not adopt a nannying approach; it also requires striking the right balance.

“In the early stages, projects are relatively small, and investors have the capability and resources to coordinate or resolve related issues. However, as companies grow larger in later stages, the scope of assistance investors can provide diminishes.” In Song Gaoguang’s view, the core role of investment firms is to help entrepreneurs identify effective learning approaches and methodologies, supplemented by certain resources, so that companies can build their own competitive moats.

Jiang Min, a partner at SoftBank China Capital, told VCBeat: “When selecting portfolio companies, investment firms must also choose the right people. For instance, scientist-entrepreneurs must possess two key traits: resilience and inclusiveness. The founder of BioAI, which we have invested in, is Professor Zhang Zemin from the Biomedical Pioneering Innovation Center (BIOPIC) at Peking University, who has achieved significant academic accomplishments in the field of single-cell analysis. Beyond his scientific expertise, his management capabilities, resilience, and inclusiveness were crucial factors in our decision to invest.”

“Huagai Capital places particular emphasis on industry research, which leads us to favor an active investment approach. When we identify exceptional scientists, we engage early and collaborate with medical professionals to discuss strategies and provide empowerment. For instance, beyond financial support, we assist early-stage companies in formulating tactical objectives and phased implementation plans, while also helping to build their core executive talent pool,” said Zhang Yi, Managing Partner of Huagai Medical’s Early-Stage Fund. “For example, Lanma Medical is a company we proactively incubated by inviting a highly seasoned industry expert from overseas to participate. Within just over six months, it achieved remarkable growth.”

Of course, as investment gradually shifts toward early-stage projects, the overarching direction remains unchanged: identifying new technological breakthroughs to address unmet clinical needs.

In interviews with investment firms,Key areas of focus include shifts in the disease spectrum driven by demographic changes and lifestyle habits, as well as upstream and downstream industry opportunities enabled by new technology platforms.

Due to the distinct “DNA” of each institution—for instance, some analyze the healthcare and wellness industry through the lens of the new economy, while others focus on how digital technologies transform the sector—it is difficult to reach a consensus on judgments regarding specific subsectors.

However, it is clear that advanced technologies with preliminary validation of their industrialization capabilities and safety by startup teams are factors of widespread interest.

How to understand? It isInnovation must be “grounded”: it should be truly driven by clinical needs, possess strong potential for industrialization, and feature a sound business logic for the startup project.

“Some projects enlist renowned scientists in the field as figureheads and adopt emerging concepts to highlight their cutting-edge nature, aiming to secure financing, yet they often struggle with practical implementation. As investment trends shift toward earlier-stage ventures, the ability to identify such projects has become an essential competency for investment firms,” said a senior investor in the healthcare industry.

Beyond commercial potential, insufficient industrialization experience has also become a major challenge for many startups. “In the biopharmaceutical sector, it is common for founding teams to overlook the druggability of candidate drugs, particularly among founders with backgrounds in basic research. We have seen cases where candidate drugs showed no toxicity in safety assessments, yet their area under the curve (AUC) failed to increase significantly even at high doses; we have also encountered situations involving central nervous system (CNS) drug development where the compounds exhibited virtually no blood-brain barrier penetration,” said Lin Guanyu, Investment Director of Shenzhen Capital Group’s Hongtu Healthcare Industry Fund.

Based on the above factors,As investment firms extend their reach into early-stage projects, the feasibility of implementation and the industry’s growth prospects will shape their investment decisions in the healthcare sector in 2022.

Following this line of thought, this article will separately discuss the key sub-sectors and underlying logic that investment institutions focused on in 2022 across four major segments: biopharmaceuticals, innovative medical devices, healthcare services, and digital health.

Biopharmaceutical Sector: Synthetic Biology, Cell and Gene Therapy Garner Strong Interest; Global Competitiveness Is Key

In recent years, China's biopharmaceutical sector has been extremely vibrant, though specific sub-sectors have experienced varying dynamics.

Last year, small-molecule drugs and large-molecule drugs began to enter a bottleneck period, whileFrontier biotechnology sectors such as synthetic biology, cell therapy, gene therapy, and nucleic acid drugs have attracted significant capital interest, a trend expected to continue in 2022.

“From the early days of me-too drugs to fast-follow strategies and license-in deals, and now to the current wave of global expansion, the market’s understanding and valuation of innovative drugs have undergone several rounds of deconstruction and reconstruction, with significant shifts in the specific criteria considered at each stage,” said Lin Guanyu, Investment Director of the Hongtu Healthcare Industry Fund at Shenzhen Capital Group.

ButThe unchanging logical thread is: cutting-edge biotechnology.

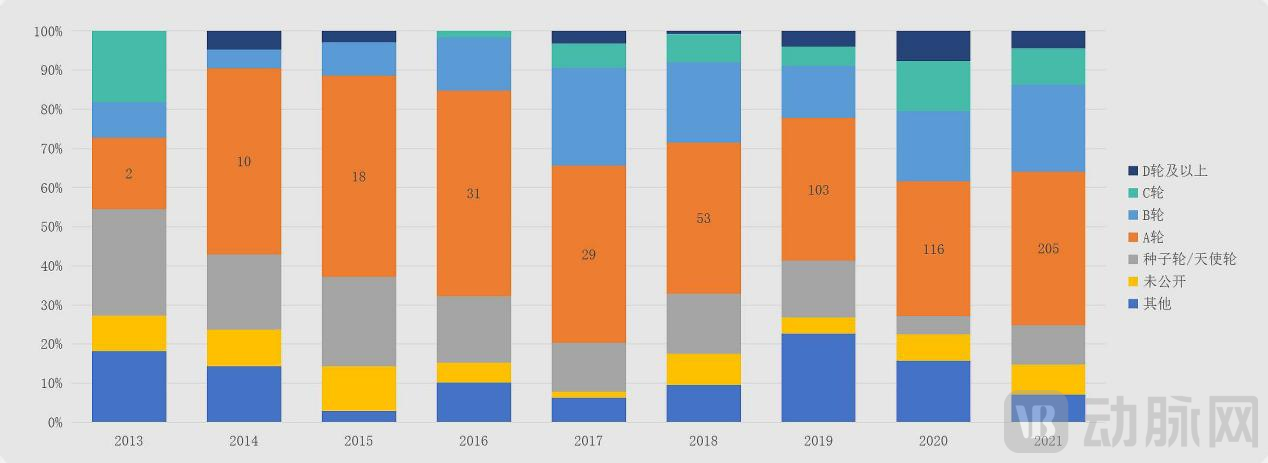

According to VCBeat’s observations, the global biopharmaceutical sector has long been dominated by Series A financing rounds. In 2020 and 2021, Series A deals accounted for 30.2% and 34.3% of all financing activities, respectively, with the proportion estimated to rise by 2 to 5 percentage points in 2022. It is worth noting that companies at the Series A stage are predominantly focused on cutting-edge areas of biotechnology.

(Distribution of Financing Rounds in China’s Primary Market in 2021; Data Source: VCBeat Orange Database)

(Distribution of Financing Rounds in China’s Primary Market in 2021; Data Source: VCBeat Orange Database)

From the perspective of development milestones, a typical characteristic of current frontier technologies is interdisciplinary integration. Synthetic biology lies at this intersection and has experienced rapid growth in recent years due to increasing attention from capital investors. A 2021 research report by McKinsey Global Institute (MGI) predicts thatThe synthetic biology technology revolution will generate $2–4 trillion in direct economic benefits globally each year over the next 10–20 years.

“A significant value of synthetic biology lies in providing technological innovation solutions for the overarching goal of carbon neutrality,” stated Hillhouse. “In January this year, Hillhouse led the Pre-A round financing for Shanghai Changjin Bio, a company specializing in microbial synthetic proteins. In our view, breakthroughs in alternative protein technologies can transform the supply and production methods of human dietary protein. Currently, Changjin Bio is identifying microbes from nature that can serve as novel food sources for humans. By leveraging high-throughput screening, directed mutagenesis, and gene editing, the company has established unique cell factories to enable the synthesis of essential nutrients such as proteins.”

Matrix Partners China stated, “In the field of synthetic biology, we remain optimistic about the broad application prospects enabled by the efficient engineering of cellular pathways in new drug development, cell engineering, and high-end biomanufacturing. We entered the synthetic biology sector early on and have cumulatively invested in more than 10 startups, including Bota Bio, RootPath, Senti Bio, Zhouzi Future, and YuanYu Biologics.”

Policy support has also served as a key catalyst driving the surge of frontier technologies in the capital markets.In November 2021, the Beijing Municipal Committee of the Communist Party of China and the Beijing Municipal People’s Government issued the “Plan for Building Beijing into an International Science and Technology Innovation Center During the 14th Five-Year Plan Period,” aiming to promote research and development of frontier biotechnologies in key areas such as novel antibody technologies, gene editing, novel cell therapies, and stem cells and regenerative medicine.

VCBeat’s analysis reveals that, in addition to Beijing, multiple provincial and municipal governments—including those in Shanghai, Jiangsu, Zhejiang, Guangzhou, Tianjin, Shenzhen, and Dalian—issued guiding plans for the development of the pharmaceutical industry last year, channeling resources toward frontier technological subsectors such as synthetic biology, cell therapy, and gene editing.

“In the field of gene therapy, there is a gradual shift in focus from rare diseases to common diseases.“This is because, as we mature in gene therapy technology overall—particularly with advances in vector development—we will gradually achieve breakthroughs in addressing tissue and organ targeting during delivery, as well as resolving safety concerns related to vectors. Subsequently, as treatment costs decline, more patients will benefit, thereby expanding the market,” said Luo Xi, Executive Director of the Healthcare Technology Group at Huaxing New Economy Fund.

Matrix Partners China has invested in companies such as Qihan Bio and Useen Bio in the field of cell and gene therapy. “We place great emphasis on globally leading, breakthrough technologies in this sector,” stated Matrix Partners China. “For instance, Useen Bio, a company specializing in allogeneic universal CAR-T cell therapy, boasts investigator-initiated trial (IIT) data that is among the most advanced worldwide.”

In addition to being at the technological forefront, products with global competitiveness have also become highly sought-after targets for investment institutions.This is because changes in medical insurance policies in recent years have shown that the main battlefield for China's innovative drugs remains overseas.

“In early 2021, we recognized that the growth potential of innovative drug companies was being squeezed by downstream volume-based procurement and national reimbursement drug list (NRDL) negotiations, as well as upstream capital bubbles and homogeneous competition. Consequently, we began seeking out sectors with relatively stable and moderate competitive landscapes, minimal exposure to NRDL policies, and genuine international competitiveness,” said Lin Guanyu, Investment Director of the Shenzhen Capital Group’s Hongtu Healthcare Industry Fund.

Taking Desano Biopharma, a recent investment by Shenzhen Capital Group (SCGC), as an example, the company has been dedicated to the field of anti-HIV medications for over two decades. Its integrated industrial chain—spanning raw materials, intermediates, active pharmaceutical ingredients (APIs), and finished formulations—has established high entry barriers. Long-term collaboration with overseas regulatory agencies and multinational pharmaceutical companies has also laid a solid foundation for its international API and formulation businesses, as well as its CDMO operations. Furthermore, the company boasts the most extensive pipeline of anti-HIV formulations among domestic peers, with more than ten formulated products approved for market launch by the NMPA, FDA, or WHO. This has secured its leading position in China’s anti-HIV drug market, particularly amidst the industry trend of upgrading from single-agent therapies to innovative fixed-dose combination regimens.

“Seventy-four percent of the domestic market for anti-HIV drugs is funded through fiscal expenditures, rather than relying on medical insurance. The long-term cost-oriented market has established a relatively stable competitive landscape and has also mitigated the risk of commercial bribery, which often raises questions when many pharmaceutical companies launch their products,” said Lin Guanyu. “We believe that by investing in such outstanding enterprises and leveraging Shenzhen Capital Group’s portfolio resources in the field of innovative drugs, we can better provide patients both domestically and internationally with more effective and accessible medications.”

Furthermore, many investors agree that disruptions to overseas supply chains during the pandemic have constrained the supply of imported products, thereby further boosting demand for domestically produced alternatives. The implications for the biopharmaceutical sector in 2022 are as follows:Upstream industries linked to the entire biopharmaceutical sector, including reagents, consumables, and instruments and equipment such as culture media, enzymes, recombinant proteins, and single-use reaction systems, will also continue to attract sustained capital interest.

Innovative Medical Devices Sector: The Cardiovascular Track Remains Hot, While Niche Fields Such as Ophthalmology and Medical Aesthetics Are Emerging Rapidly

2022 Will Be a Pivotal Year for the Domestic Substitution of Innovative Medical Devices in China.

“Sub-sectors with potential for domestic substitution are a key focus for us,” stated Matrix Partners China. Taking its investment in the endoscopy company Sinovision Medical as an example, the company has reached or surpassed the standards of foreign giants in next-generation categories such as 3D, ultra-high-definition, and single-use endoscopes. “The current localization rate in this field is less than 5%, indicating substantial potential for import substitution.”

The underlying reason is that centralized volume-based procurement over the past two years has begun to drive differentiation in the industry landscape, constraining the development of some companies, slowing the expansion pace of foreign enterprises, and creating a critical window for growth for domestic companies.

(Image source: China Renaissance)

(Image source: China Renaissance)

From the perspective of various sectors, the cardiovascular sector will continue to remain hot, while medical aesthetics with consumer attributes will rise rapidly, and ophthalmology will also usher in a new wave of enthusiasm driven by policy incentives.

Specifically, in the cardiovascular sector, new technologies and products such as Pulsed Field Ablation (PFA), Ventricular Assist Devices (VADs), and shockwave balloons will continue to attract attention in the primary market.

In terms of new technologies and products, taking pulsed field ablation (PFA) as an example, this next-generation disruptive ablation technology offers advantages such as enhanced safety, faster procedure times, lower requirements for catheter-tissue contact, and greater continuity and uniformity of transmural lesions. It is highly likely to become the mainstream treatment for atrial fibrillation in the future. Just last month, Medtronic announced its acquisition of Affera, a cardiac ablation company specializing in PFA technology, for $925 million.Recent months’ transactions signal that electrophysiology will emerge as a new growth highlight.

“Policies such as medical insurance reimbursement and centralized volume-based procurement have significantly impacted the profits of companies in niche sectors where market structures are already well-established. Conversely, these policies present development opportunities for niche segments that previously suffered from limited market acceptance or penetration. Take Xinuopu Medical, a cardiac electrophysiology company in our investment portfolio, as an example. It boasts strong competitiveness in product R&D and domestic and international marketing networks, and its products have gained high recognition from clinical experts, breaking the monopoly held by imported products. Such companies have long lacked opportunities for rapid market expansion, and now that opportunity has arrived,” stated Xu Xiaolin, Chairman and Founding Partner of Huagai Capital.

“Over the next 5 to 10 years, the core drivers of development in the medical aesthetics industry will be materials and technology.“Mingfeng Capital stated that upstream materials and technologies can turn potential demand into reality. We believe that collagen and botulinum toxin will be the next investment hotspots. Collagen technology is advancing and will lead”Injectable fillers are gradually entering the era of regeneration."As an irreplaceable category, botulinum toxin—along with newly approved products and novel bioengineered botulinum toxins—represents a promising investment opportunity."

Beyond technological advancements, the growing prominence of ophthalmology is driven more significantly by supportive policies. Early this year, China’s 14th Five-Year National Plan for Eye Health emphasized the importance of early detection and treatment of ophthalmic diseases, particularly myopia in adolescents, cataracts in the elderly, and other eye conditions affecting younger populations. “The ophthalmology sector comprises numerous subsegments, including optical coherence tomography (OCT) devices and orthokeratology lenses, all presenting promising opportunities. However, the greatest uncertainty lies in the potential spillover effect from last year’s centralized volume-based procurement (VBP) of dental implants into the ophthalmology field, likely spurred by public demands for affordable healthcare,” noted a senior investor.

On the other hand, once-hot niche sectors are being tested by shifts in commercialization and valuation frameworks., such as high-value consumables for vascular intervention and surgical robots.

“After surveying a range of domestic manufacturers of high-value vascular interventional consumables, we found that while these products command valuations typical of high-value medical consumables in the market, the gross profit margins of the major Chinese players stand at only around 40%. In our view, this margin level does not qualify as high-end manufacturing,” Yi Hongxiang, Partner at SCGC Hongtu Medical Health Industry Fund, told VCBeat. “This indicates that vascular interventional consumables are essentially manufacturing-driven, with relatively low technological barriers but higher demands on processing craftsmanship. For the manufacturing sector, we place greater emphasis on corporate maturity, particularly a company’s operational capabilities in the global market.”

Surgical robots, which have garnered significant market attention in recent years, are also facing growing skepticism. Some investors point out that the valuation or market capitalization of surgical robot companies does not necessarily reflect their true value, as the primary challenge for current surgical robots remains their prohibitively high costs. Although domestic surgical robot startups are experiencing a financing boom, market expansion is still in its early stages. Taking Stryker’s Mako robotic-arm assisted orthopedic joint surgery system as an example, while Mako has performed well internationally, China had only 17 such joint surgery robots in 2020, with approximately 250 procedures completed.

“From an industry perspective, obtaining a registration certificate for a product is merely the starting point; there remains a long road ahead of iterative development and optimization.“Drawing on the development trajectory of Mindray, a leading domestic medical device manufacturer, it took the company over three decades to elevate its patient monitors to a position where they could compete head-to-head with imported products. Therefore, regardless of how hot a sector may be, capital enthusiasm cannot mask the challenges of marketization,” said Yi Hongxiang, Partner at SCGC Hongtu Healthcare Industry Fund.

Therefore, the domestic innovative medical device industry requires sufficient patience to support innovative enterprises as they progress from technical validation to industrialization.

Furthermore, according to Luo Xi, Executive Director of the Healthcare Technology Group at China Renaissance New Economy Fund,The healthcare value chain is extending in both directions from treatment.: The front end encompasses health management for healthy populations, as well as disease prevention and screening, while the back end covers patient rehabilitation and follow-up care; all of these will generate structural investment opportunities.

“Taking Kangliming Biotech, in which we invested last year, as an example, our assessment is that increasing efforts will be directed toward early screening and detection in the diagnosis and treatment of cancer. This is because, within the continuum of cancer care, early-stage investment yields greater efficiency than late-stage intervention. Health economics studies have shown that every yuan invested in prevention and screening can save up to nine yuan in subsequent treatment costs,” stated Luo Xi.

"Commercially, ClearMed Biotech has deeply cultivated hospital testing channels, establishing robust barriers to entry within hospitals. Its existing early-stage colorectal cancer detection products, along with a rich pipeline of products under development, will provide customers with comprehensive tumor screening solutions."In 2022, the diagnostics industry will witness greater cross-sector integration, with digitalization and intelligence becoming key drivers of innovative transformation.”

Digital Healthcare Sector: Digital Therapeutics and InsurTech Emerge as Hotspots, with Commercial Monetization Capability as a Key Test

Since the outbreak of the COVID-19 pandemic, digital health projects have remained highly favored by investors in the capital market. Most investment institutions assert that the wave of new technologies—such as big data, artificial intelligence (AI), cloud computing, and the internet—will reshape every traditional industry, healthcare included. This constitutes the long-term rationale for betting on this sector.

However, significant changes have occurred in the popularity of niche sectors over the past two years. Internet healthcare has cooled down from its previous peak, while AI-driven drug discovery has entered a consolidation phase after an initial surge.In 2022, digital therapeutics and insurtech will become hotspots.

The surge in popularity of Digital Therapeutics (DTx) is primarily driven by two factors. First, at the regulatory level, there has been continuous promotion by agencies such as the U.S. Food and Drug Administration (FDA). Second, at the industry level, various companies have actively advanced the field and achieved certain breakthroughs; for instance, domestic DTx enterprises including Miao Health, Weimai, Shuyu Technology, MedSci, Wangli, Good Doctor Hui, and Jianhai Technology joined the Digital Therapeutics Alliance (DTA) in 2021. Incomplete statistics indicate that, to date, nearly 30 DTx products have received approval from authoritative bodies such as the FDA.

(Digital Therapeutics Disease Spectrum Blueprint, Chart by VCBeat)

(Digital Therapeutics Disease Spectrum Blueprint, Chart by VCBeat)

“Improving healthcare accessibility has always been our focus,” said Jiang Xiaodong, Managing Partner at Changling Capital. He noted that the emergence of digital therapeutics has effectively enhanced healthcare accessibility. Taking Wangli Technology, in which Changling Capital invested in mid-2025, as an example, the company has established a diversified product pipeline in the field of mental health disorders, including depression, addiction, and PTSD.

The rise of insurtech is closely tied to the growing importance of payers in the healthcare and wellness industry. Straddling both the insurance and healthcare sectors, insurtech has established a dominant market position: data from the China Banking and Insurance Regulatory Commission (CBIRC) shows that the health insurance segment of insurtech achieved an annualized growth rate of 31.4% over the past five years, with its market size doubling. Based on this growth trajectory, the health insurance industry was projected to surpass the RMB 1 trillion mark in 2021. The continuously expanding market will create greater opportunities for future growth, thereby driving sustained financing for insurtech companies.

Of course, for all digital health projects, the ability to be implemented is an important test factor.

“The maturation of China’s new infrastructure is reshaping mega-industries, thereby giving rise to a series of new corporate species. In the health and life sciences sectors, we are witnessing an increasing integration of technology-enabled solutions that address industry challenges,” said Liu Erhai, Founding and Managing Partner of Joy Capital. He noted that intelligent technologies can not only assist in tackling cutting-edge, frontier, world-class medical challenges and diseases but also, more importantly, serve the broadest segments of the population.

As of the end of March 2021, there were 1.026 million medical and health institutions across China, including 973,000 primary care institutions. These primary care facilities handled 4 billion patient visits in 2020, with 80% of cases involving common diseases. Complete blood count (CBC) testing covers up to 83.6% of diagnoses for these common conditions—representing one of the most widespread and fundamental healthcare needs of the population.

Following this logic, Joy Capital led the Series A investment in Yihong Health. Currently, Yihong Health’s handheld blood cell analyzer, “Palm Test,” along with its related services, has reached more than 20,000 primary-care clinics and health centers across China.

Digital healthcare is also a top priority in SoftBank China Capital’s layout of the healthcare sector. Representative companies include Taimei Medical Technology, which is racing toward an IPO this year; Dingdang Kuaiyao, a “digital + pharmaceuticals” enterprise; and EDDA, a company focused on “AI + precision diagnostics” and robotics.

“Our understanding of digital health may differ from that of many investment firms. For instance, while some investors categorize Keya Robotics, a company we have invested in, as a medical device manufacturer, we approached the investment from a digital health perspective. This is because the core of a surgical robot lies in its ‘brain,’ with the robotic arms merely executing the commands issued by this ‘brain.’ The intelligence of the ‘brain’ ultimately tests a company’s digital capabilities,” Jiang Min, Partner at SoftBank China Capital, told VCBeat. “We have integrated digital empowerment with five key dimensions of the healthcare and wellness industry: hospitals, pharmaceuticals, medical devices, doctor-patient interactions, and innovative payment models.”

“In digital health, who pays is also critically important."Jiang Min stated, 'A good project must balance technology with commercialization.'"

Taking Keya Medical Robotics as an example, the company has become a leading domestic manufacturer of orthopedic joint surgical robots in China. It has completed clinical trials for hip replacement surgery, which demands higher technical precision, and is also expanding indications for knee replacement procedures, placing its technological capabilities at the forefront of the industry.

“In terms of commercialization, there is currently a significant gap in joint replacement penetration rates between China and the United States. The domestic joint replacement market boasts promising growth prospects. We are optimistic that Keya Medical’s robotic systems will help address unmet clinical needs for joint replacements in China, thereby serving the vast population of patients suffering from joint diseases.” In Jiang Min’s view, Keya Medical has united a group of outstanding physicians and leading experts, while also accumulating substantial resources in areas such as channel expansion. “From the beginning to the end of this year, Keya Medical’s valuation has increased several-fold.”

“The cooling of internet healthcare stems from challenges in commercial monetization. It is evident that since the year before last, numerous leading companies have rushed toward initial public offerings (IPOs), yet their financial performance has generally been lackluster due to overly simplistic revenue models. These companies rely either on pharmaceutical sales or on selling SaaS solutions; however, SaaS is not a critical necessity for hospitals and pharmacies, making it difficult to generate substantial revenue. The lack of recognition in the secondary market has naturally led to a shift in sentiment within the primary market.”Future digital health enterprises must clearly define the closed-loop construction of their business models to sustainably attract capital investment.“An investor who has long followed digital healthcare stated.”

Medical Services Sector: Critical Care Specialties Enter a Period of Opportunity, with Online-Offline Integration Becoming Essential

China’s private healthcare services sector is undergoing a structural transformation. Throughout 2021, more than ten companies in the healthcare services sector filed for initial public offerings (IPOs) or successfully completed their IPOs.

It is worth noting that, in addition to consumer-oriented specialties such as ophthalmology and dentistry, financing for niche specialties including neurology, oncology, and traditional Chinese medicine has been accelerating in recent years. Evidently, major specialties dealing with critical and severe conditions are entering a period of opportunity.

(Data source: Artery Orange Database; Graphic by VCBeat)

(Data source: Artery Orange Database; Graphic by VCBeat)

“Specialties such as plastic surgery, ophthalmology, dentistry, and obstetrics and gynecology have become highly mature, with regional leaders emerging and competition intensifying to a white-hot level,” said a senior investor.With the nationwide implementation of DRG/DIP payment reforms and deepening measures such as volume-based procurement, the role of public hospitals in providing basic healthcare has become increasingly clearly defined, while private healthcare, as a market supplement, is poised for greater growth opportunities.

Within this landscape, opportunities for non-public healthcare providers are gradually emerging in critical care specialties—such as cardiology, oncology, and neurology—that were once absolutely dominated by public hospitals.

“These specialized companies have actually been accumulating experience for many years. For instance, Hygeia Healthcare has been cultivating its business for ten years, and Sanbo Brain Hospital has been developing for nearly 20 years,” said Jiang Xiaodong, Managing Partner of Changling Capital.The robust growth of leading enterprises, including successful financing rounds and initial public offerings (IPOs), has served as an exemplary model.“Previously, companies focused on these sectors have discovered that they can also leverage external resources to scale up and strengthen their operations amid standardized development, prompting more enterprises to emerge into the spotlight.”

In addition, multiple investors unanimously agreed that,The emergence of new technologies is a key variable that emboldens capital to invest in major specialties for critical and severe care, beyond the influence of policy.

“Take oncology as an example. To enter this sector, we typically assess the founder’s academic and clinical capabilities, preferably with a leading oncology specialist at the helm, supported by top-tier specialized personnel. Technologically, it is essential to equip facilities with the most advanced medical devices or therapeutic drugs. This can be summarized as the ‘strong specialty, limited general practice’ model,” said a senior investor. “Caution is also warranted regarding some pseudo-concepts or immature technologies in the market.”

Jiang Xiaodong, Managing Partner at Changling Capital, stated that oncology diagnosis and treatment is a capital-, talent-, and technology-intensive industry with high barriers to entry. Outstanding private hospitals can establish a virtuous cycle among these three elements and foster a relationship with public hospitals that involves both competition and collaboration. Technological and model innovations—such as precision medicine, data-driven approaches, and robotic surgery—are gradually reducing the reliance of diagnostic and treatment protocols on expert experience while enhancing their standardization. This trend presents new opportunities for the development of private medical services.

According to the 2021 China Health and Health Statistical Yearbook, there were a total of 150 oncology hospitals nationwide in 2020. Among them, 78 were public and 72 were non-public, with this number expected to continue rising in the future.

In terms of future trends, Jiang Xiaodong believes thatAnother innovative opportunity in the healthcare services sector is OMO, which represents the integration of online and offline channels., which is also one of the reasons for its investment in Gushengtang and Hygeia Healthcare.

Taking Gushengtang as an example, it is a pioneer in adopting the “OMO” (Online-Merge-Offline) business model. Operationally, the development of Gushengtang’s online healthcare services has enabled the company to utilize medical resources more effectively and expand its customer reach. On the other hand, Gushengtang has been able to strategically select cities for expanding its offline presence based on metrics of online physician and customer engagement.

For instance, in the area of customer acquisition—a key concern for healthcare service providers—Gushengtang has launched its official WeChat account and mini-program to offer online appointment booking, consultations, diagnoses, and prescription services. Leveraging its extensive network of physicians, rich operational experience, and proprietary IT infrastructure, Gushengtang serves a larger, cross-regional customer base through both its own and third-party online platforms. Furthermore, thanks to its proprietary platform, Gushengtang stores customers’ electronic medical records (EMRs) in a cloud-based Hospital Information System (HIS), thereby creating comprehensive customer profiles to facilitate follow-up services and long-term health management. According to Gushengtang’s prospectus, the cumulative number of patient visits had exceeded 7 million as of December 31, 2020, with steadily improving customer loyalty and retention; the customer return rate reached as high as 62% in 2020.

Of course,Healthcare services are a “slow industry,” requiring investment firms to possess the patience and perseverance of long-termism.

“I believe that value creation for healthcare service providers, whether in terms of adapting to the broader trend of common prosperity or strengthening internal capabilities, will be a tough and labor-intensive endeavor—relatively slow and challenging, yet it is the right path,” said Jiang Xiaodong.

During our research into top-tier investment institutions, we have deeply felt thatMoving to the forefront of R&D has become an irreversible trend.

This aligns perfectly with China’s development direction. At the national level, innovation has been placed at the core of China’s modernization efforts. Relevant data show that China’s expenditure on basic research has long accounted for approximately 5% of total R&D investment. In 2019, it surged by 22.5%, exceeding 6% for the first time; it reached 8% in 2020, with a target of 15% by 2025. By then, China’s total R&D spending is also projected to surpass that of the United States. Under this trend, the industrialization wave of China’s frontier technologies is poised to enter a period of significant dividends.

For enterprises, investment institutions, or individuals, there is an opportunity to ride the trend, step into the spotlight, and usher in a chance for non-linear growth.

In this process, waves of scientists and professors have begun to step into the industrial forefront, and primary innovation has become an industrial hallmark for a considerable period ahead.

At the same time, innovative enterprises also face numerous challenges. In response, China Renaissance’s Healthcare and Life Sciences Division has offered six recommendations:

1: Return to rationality, prioritize the market, and consider long-term growth within the limits of market capacity, not just the hype of the sector;

2: Differentiated positioning to avoid involution and homogenization; ensure that differentiation is implemented in product design and clinical validation.

3. Product portfolio strategy should be outcome-oriented, aligning with clinical needs and commercial accessibility, while prioritizing products with relative scarcity. For products in high-demand therapeutic areas, consider innovations in business models or strategically position low-cost products to maintain competitiveness under volume-based procurement (VBP).

4. Regarding financing, it is advisable to maintain cash reserves to withstand economic downturns and volatility, while improving capital efficiency. Financing should be initiated proactively when the company still has ample liquidity, thereby allowing the enterprise to actively control its development pace. Additionally, optimization of the equity structure should be considered from the outset of the fundraising process., while predefining the timing of financing and alternative options;

5. Team: At each stage, the team must be complete and demonstrate strong execution capabilities. By breaking down and implementing internal milestones, the team should validate its hypotheses in the shortest possible time. Whether the outcome confirms the hypothesis or results from trial and error, the team can rapidly move forward, fully leveraging the agility advantage of startups.

6: Finally, it is recommended that regardless of their position in the competitive landscape, companies should actively monitor their competitors, keep abreast of industry developments from both business and capital perspectives, and respond in a timely manner.

Amid the rising tide of innovation moving to the forefront, both investors and industry stakeholders are propelling Chinese innovative enterprises to shape the future of the healthcare and wellness sector.

What you and I have witnessed together is precisely the new starting point of this era’s great tide, as well as the new Chinese story that is gradually unfolding.

Special Thanks:

Partner at Northern Light Venture Capital | Song Gaoguang

Managing Partner, Changling Capital | Jiang Xiaodong

Hillhouse Ventures

Xu Xiaolin │ Chairman and Founding Partner, Huagai Capital

Managing Partner, Huagai Medical Early-Stage Fund | Zhang Yi

Luo Xi | Executive Director, Healthcare Technology Group, Huaxing New Economy Fund

China Renaissance Healthcare and Life Sciences Division

Matrix Partners China

Mingfeng Capital

Partner, SoftBank China Capital | Jiang Min

Partner, SCGC Hongtu Medical and Health Industry Fund | Yi Hongxiang

Investment Director, Shenzhen Capital Group Hongtu Medical Health Industry Fund | Lin Guanyu

Joy Capital Founding and Managing Partner | Liu Erhai

(The above ranking is in alphabetical order by Pinyin.)