Domestic Enterprises Break Through Multinational Giants in the Intraocular Lens Market Amid Aggressive Price Negotiations

Eyebright Medical

Ophthalmic Medical Product R&D Provider

Haohai Biological Technology

Medical Biomaterials R&D and Manufacturer

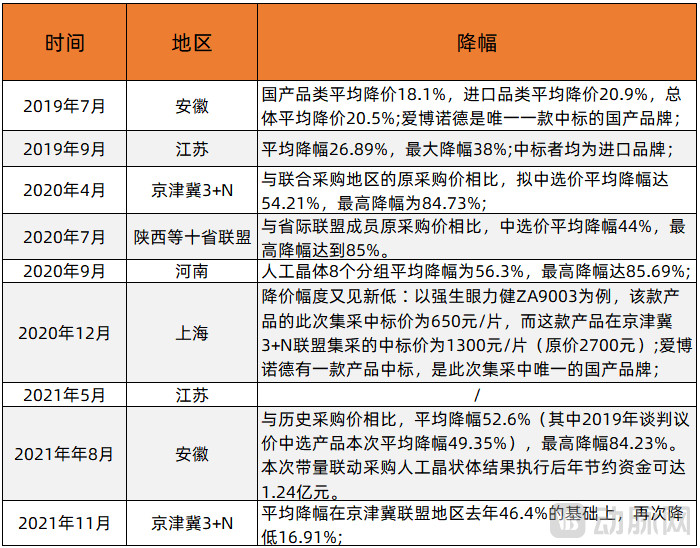

In January 2022, the Beijing-Tianjin-Hebei “3+N” Alliance successfully completed the centralized procurement of intraocular lens (IOL) medical consumables. A total of 14 provinces participated in this procurement round. As the alliance continues to expand its membership, the price-reduction effect driven by volume-based procurement has become increasingly significant. Building on the average price reduction of 46.4% achieved in 2021, IOL prices decreased by an additional 16.91%, resulting in an average price of RMB 2,347 per unit.

Subsequently, at the end of the month, the Shaanxi Provincial Drug and Medical Device Centralized Procurement Platform released the “Announcement on Volume-Linked Procurement of Intraocular Lens Medical Consumables by the Inter-Provincial Alliance,” announcing that Shaanxi Province would lead volume-linked procurement of intraocular lenses in the regions of Shaanxi, Gansu, Ningxia, Qinghai, Xinjiang, the Xinjiang Production and Construction Corps, Hunan, Guangxi, and Hainan. As the centralized procurement alliance continues to expand, there is a high probability that this nine-province/region alliance led by Shaanxi, Gansu, and Ningxia will once again set a new “national lowest price” for intraocular lenses, building upon the pricing established by the Beijing-Tianjin-Hebei “3+N” Alliance.

Amid the price reductions for intraocular lenses (IOLs) under China’s volume-based procurement (VBP) programs, domestic companies are more concerned with how to capture a significant share of the market from the four major multinational corporations represented by Alcon. After all, these four companies collectively hold nearly 65% of the market share. For Chinese firms to achieve breakthroughs in this industry, they must directly confront this competition.

Intraocular lenses, also known as artificial crystalline lenses, are implanted surgically to replace the clouded natural lens, which is a treatment for cataracts.Uniqueeffective measures. Intraocular lenses are the most widely used artificial organs and implantable medical devices worldwide.

Recently, the National Health Commission issued the "14th Five-Year National Eye Health Plan (2021-2025)," outlining key priorities for ophthalmic medical services over the next five years. The plan specifically highlights achieving a national Cataract Surgical Rate (CSR) of over 3,500 per million population and continuously improving the effective Cataract Surgical Coverage (eCSC).

Supported by various policies, the intraocular lens market is seizing the opportunity for rapid growth.

Cataracts are the leading cause of blindness and a common condition among middle-aged and elderly individuals. In recent years, the Chinese government has placed increasing emphasis on national eye health. In 2018, China’s cataract surgical rate (CSR) per million population was 2,662. By contrast, developed countries such as France and the United States had already achieved CSRs of 10,000 as early as 2011. Although China’s CSR increased by 148.32% from 2012 to 2018, it remains at a relatively low level. Consequently, the national target for CSR by 2025 has been set at above 3,500. Based on the growth rate observed during the previous five-year eye health plan, achieving this target should not be difficult. According to forecasts in the prospectus of Eyebright Medical, China’s CSR may exceed 4,200 by 2025. The demand for intraocular lenses is therefore poised to increase substantially.

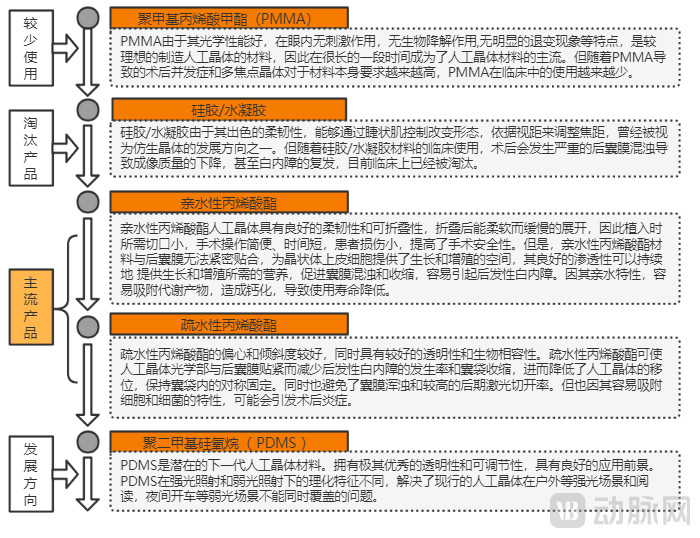

The materials used for intraocular lenses have undergone multiple stages of development. Currently, acrylic esters are the predominant material, with hydrophobic acrylic demonstrating superior advantages over hydrophilic acrylic in terms of reducing posterior capsule opacification, ensuring long-term stability after intraocular implantation, and providing greater mechanical strength.

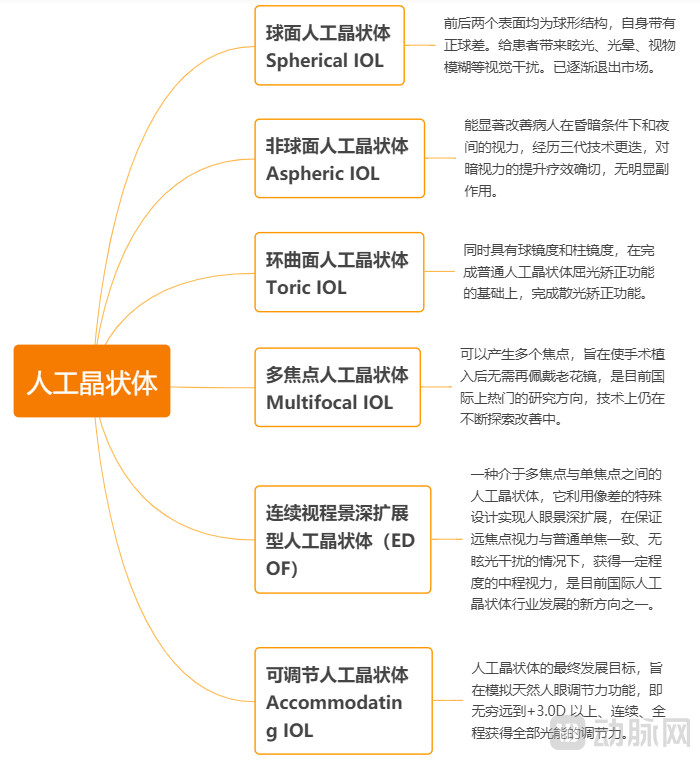

Optical design is the core technology enabling the functional application of intraocular lenses (IOLs). Over the past 5 to 10 years, development has focused on various refractive functionalities. The optical design of IOLs has evolved through the following stages: spherical → aspheric → toric → multifocal → accommodating.

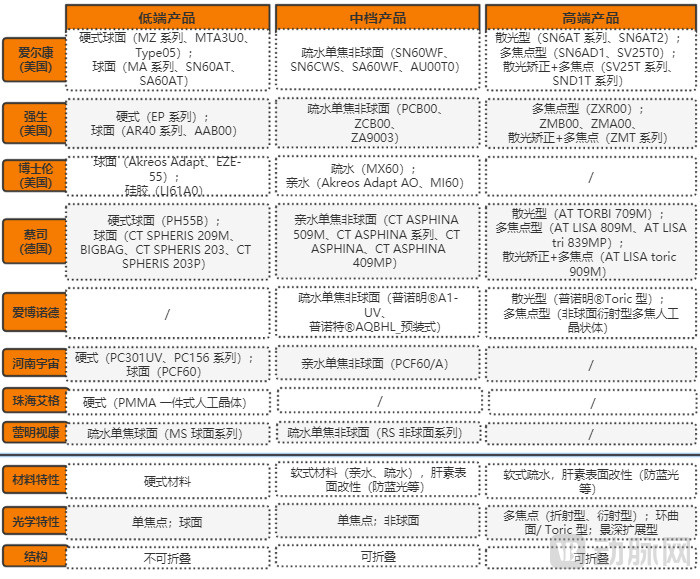

Based on clinical application scenarios and technological sophistication, intraocular lenses (IOLs) can be categorized into three major tiers: low-end, mid-range, and high-end. Low-end products are primarily used in vision-restoring cataract surgery and consist mainly of rigid IOLs and spherical IOLs. These products are associated with issues such as larger surgical incisions and average visual quality. Rigid IOLs have long been phased out in developed countries, yet some domestic Chinese companies still focus primarily on manufacturing this category. Mid-range products, namely conventional soft IOLs, represent the mainstream in clinical practice in China and are predominantly monofocal aspheric IOLs. High-end products are utilized in refractive cataract surgery and include functional IOLs such as toric IOLs, multifocal IOLs (providing full-range vision for distance, intermediate, and near), and toric-multifocal combination IOLs. Currently, Eyebright Medical is the only domestic manufacturer participating in this high-end segment, with the remainder dominated by multinational corporations.

As the mainstream soft intraocular lenses (IOLs) in the market, they have numerous subcategories: monofocal IOLs, bifocal IOLs, trifocal IOLs, IOLs combined with Extended Depth of Field (EDOF) technology, IOLs combined with anti-astigmatism (Toric) technology, and adjustable IOLs. Among them, trifocal IOLs are priced higher, and if additional functions such as anti-astigmatism are added, the price becomes even higher.

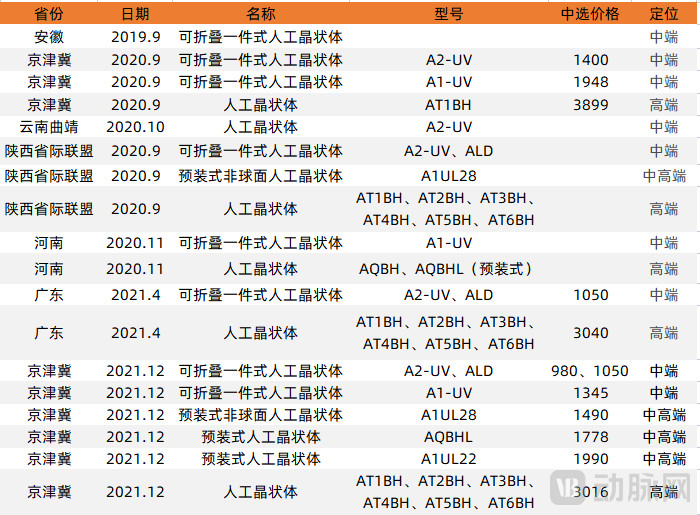

Currently, most provinces and municipalities in China have implemented centralized volume-based procurement (VBP) for intraocular lenses, achieving full coverage. The recently announced winning bid results of the Beijing-Tianjin-Hebei “3+N” Alliance, whose participating entities include 14 provinces (autonomous regions and municipalities directly under the Central Government)—namely Beijing, Tianjin, Hebei, Heilongjiang, Jilin, Liaoning, Inner Mongolia, Shanxi, Shandong, Sichuan, Chongqing, Henan, and Guizhou—account for nearly half of the national market and are thus representative. Therefore, we take these winning bid results as the primary subject of our analysis.

A total of 118 product groups were ultimately shortlisted in the “3+N” centralized procurement, with prices ranging from RMB 229 to RMB 22,999, representing a significant spread. According to Eyebright Medical’s prospectus, the industry categorizes products priced between RMB 200 and RMB 1,600 as basic and low-end, those priced between RMB 1,600 and RMB 4,500 as mid-range, and those above this range as high-end. In 2019, prior to the implementation of volume-based procurement, the domestic market shares for these three categories were 40%, 50%, and 10%, respectively. In the Beijing-Tianjin-Hebei “3+N” centralized procurement, the respective shares were 55%, 33%, and 11%.

It appears that the market share of low-end products is increasing, that of mid-range products is decreasing, while that of high-end products remains unchanged. However, given that intraocular lens (IOL) prices have been repeatedly reduced in recent rounds of volume-based procurement (VBP)—such as the average price reductions of 46.4% in the previous round and 16.91% in the current round of the “3+N” procurement—if assessed against pre-price-cut industry standards, the products currently dominating VBP are still primarily cost-effective mid-range options.

From a product perspective, the “3+N” volume-based procurement program selected a total of 118 product groups across 11 categories. Ranking these categories by average price clearly reveals that the focus lies on low- to mid-range products, with high-end products accounting for a relatively small proportion. Specifically, all shortlisted products are soft intraocular lenses (IOLs), with the lowest price being only RMB 229. Consequently, there is no longer a need to include technically outdated rigid IOLs (whose previous procurement prices ranged from RMB 80 to RMB 300). This development is unfavorable for some domestic companies specializing in such products.

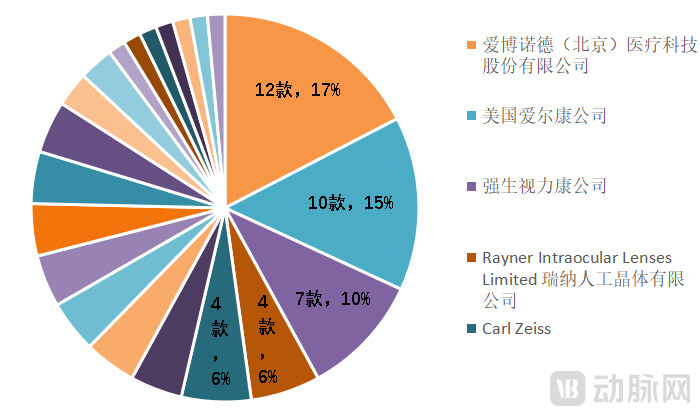

Product tiers can be simply categorized based on several dimensions: the number of focal points, whether they are spherical, the presence of astigmatism correction, and whether they are preloaded. First, single-focus products account for the largest share, with 34 spherical models comprising approximately 29% of the total volume. Unit prices range from RMB 229 to RMB 1,099, with an average price of approximately RMB 663. Products from 22 companies made the list, including about five domestic enterprises; even industry leader Alcon (USA) had only four models included. Due to low technical barriers, the basic product segment attracts competition from numerous brands, including many second- and third-tier foreign brands. The market is fragmented, and overall profit margins are limited by the low unit prices.

There are 69 models of higher-tier single-focus aspherical intraocular lenses, accounting for approximately 58% of the total volume. Their unit prices range from RMB 790 to RMB 3,191, with an average price of approximately RMB 1,934. In terms of scale, this category represents the primary area of competition in this volume-based procurement round. A total of 22 companies were shortlisted, including five domestic enterprises. Regarding the results, Eyebright Medical secured shortlisting for 12 products, capturing a 17% share in this category. It was followed by Alcon (USA), Johnson & Johnson, Rayner, and Zeiss (Germany). Eyebright Medical’s emergence as the leader in this niche segment is quite surprising, as it had only managed to get one product shortlisted in multiple procurements when volume-based procurement initially launched in 2019. Its remarkable progress over just three years has drawn significant attention.

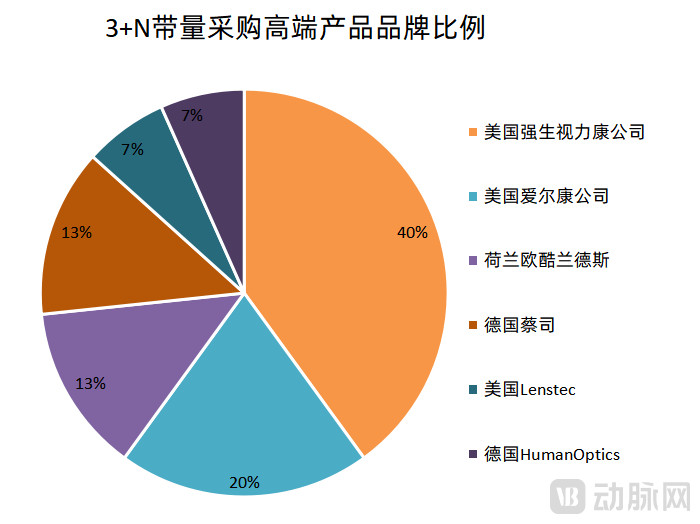

The remaining products are high-end and limited in quantity. A total of 15 products across three major categories were shortlisted, with prices ranging from RMB 4,199 to RMB 22,999. Six companies won the bids, yet no domestic enterprises made the shortlist. This indicates that, at this current stage, Chinese companies still have room for improvement in terms of technology.

Currently, the leading manufacturers in the international intraocular lens (IOL) market are Alcon (USA), Johnson & Johnson (USA), Bausch + Lomb (USA), and Zeiss (Germany). According to Alcon’s financial reports and estimates, Alcon holds a 31% global market share, Johnson & Johnson approximately 22%, Bausch + Lomb 6%, and Zeiss 4%, with these four companies collectively accounting for about 63% of the global market. The industry exhibits high concentration, characteristic of an oligopolistic market.

Generally, oligopolistic markets have high barriers to entry, which is a necessary condition for a few firms to capture the vast majority of market share. However, if we compare the international market shares of these four giants with their shares in the recent “3+N” procurement, although the four multinational giants still account for approximately 37% of the procurement volume, this figure lags significantly behind their 63% global market share. Domestic companies, represented by Eyebright Medical, are striving to catch up.

Although volume-based procurement has driven down prices, it places greater emphasis on product performance and quality rather than a brand’s historical market share. This has, to some extent, lowered market access barriers for qualified domestically produced products, thereby weakening the first-mover advantage that imported brands previously held in terminal coverage. How, then, can domestic companies break through the competition posed by numerous imported brands?

Eyebright Medical

As the most prominent domestic enterprise in the “3+N” centralized procurement initiative, what exactly did Eyebright Medical do right? The answer lies with Dr. Xie Jiangbing, the founder of Eyebright Medical. Dr. Xie previously held positions at leading global ophthalmic consumables companies, accumulating extensive experience in product research and development as well as management. Regarding his motivation for establishing Eyebright Medical, he stated, “China is a country with a high prevalence of cataracts, yet 30% of cataract surgeries in China still use outdated rigid intraocular lenses that have been phased out abroad, while soft foldable intraocular lenses are entirely dependent on imports. Only by achieving domestic production of high-end intraocular lenses can we reduce their prices and enable more people to access high-quality products.”

Driven by this vision, Eyebright Medical chose a cutting-edge starting point: foldable aspheric intraocular lenses (IOLs). Under the leadership of Xie Jiangbing, the team conducted numerous trials to identify the optimal material formulation. A significant portion of this effort was dedicated to navigating patent barriers, as foreign companies held first-mover advantages in the IOL industry, with over 1,600 relevant patents already in place. Throughout the R&D process, careful comparisons were made to ensure that the company’s products possessed fully independent intellectual property rights. It took a full year alone to synthesize a proprietary hydrophobic acrylic material with independent IP, followed by extensive validation periods.

Having the right materials is not enough; optical design is also required to transform them into functional intraocular lenses. To this end, Xie Jiangbing recruited Wang Zhao, a recent Ph.D. graduate in optics from Harbin Institute of Technology. He told her, “Most product designers in the ophthalmic industry abroad have medical training or clinical backgrounds; none come from a specialized optical engineering background like yours. If you join this field, you can apply your professional expertise to ophthalmology and potentially create something truly distinctive.” This vision deeply resonated with Wang Zhao, even though at the time she joined, the company had only six employees, including the cleaner.

Leveraging her solid professional expertise, Wang Zhao proposed her original higher-order aspheric design. However, when the product was manufactured and ready for clinical trials, it faced market skepticism. At that time, the intraocular lens (IOL) market was dominated by foreign brands, and medical institutions had reservations about adopting such a domestically produced product. Fortunately, Beijing Tongren Hospital extended an olive branch. After rigorous testing and evaluation, combined with the results of animal studies, they initiated the relevant clinical trials, which ultimately yielded excellent outcomes.

It took Xie Jiangbing a full four years, from the company’s founding to the completion of product registration, to launch China’s first foldable intraocular lens (IOL) for cataract surgery with independent intellectual property rights. Its emergence broke the monopoly held by foreign companies in this field. However, Eyebright Medical did not halt its R&D efforts. Since the first-generation product was designed based on universal ocular parameters derived from foreign user data, there were subtle differences compared to the Chinese population. In collaboration with Beijing Tongren Hospital, Eyebright Medical conducted large-sample statistical analysis on over 8,000 patients, established an aspheric corneal model specific to the Chinese population, and subsequently developed the Puno AQ series of intraocular lenses. This demonstrates that R&D is the core strategic path for Eyebright Medical.

VCBeat discovered from public information, including Eyebright Medical’s prospectus and annual reports, that the company has maintained high R&D investment over the years, with R&D expenditure accounting for more than 14% of its operating revenue in each period. In the first half of 2021 alone, R&D spending exceeded RMB 27 million, representing a year-on-year increase of 98.57%.

It is precisely due to these investments that Eyebright Medical has secured core technologies for intraocular lenses (IOLs) and complete independent intellectual property rights. The company independently masters key technologies encompassing material preparation, optical and structural design, and process manufacturing, enabling it to complete the entire R&D and production workflow within China. Another hallmark of its high R&D investment is the scale of its R&D personnel. From 2017 to the first half of 2021, the number of R&D staff was 39, 57, 78, 102, and 117, respectively, accounting for 17.5%, 17.2%, 19.8%, 24.4%, and 23.3% of the total workforce during the corresponding periods. These employees have filed a cumulative total of 81 invention patent applications for Eyebright Medical, with 39 granted; and 101 utility model patent applications, with 72 granted.

Sustained R&D investment has enabled Eyebright Medical to develop a portfolio of products, including the Prolens and Pronote series. Crafted from hydrophobic acrylic material, these intraocular lenses (IOLs) are foldable and can be implanted through a 2.2 mm micro-incision. They exhibit minimal adverse optical phenomena, excellent stability, blue-light filtering capabilities, and high biocompatibility. The “high-order aspheric” design not only compensates for corneal spherical aberration but also delivers superior image quality. The “posterior surface high-convexity” design prevents cell growth and migration onto the posterior lens surface, thereby reducing the incidence of postoperative posterior capsule opacification (PCO). Furthermore, the aspheric design based on Chinese eye models allows domestic cataract patients to achieve higher visual quality. These features exemplify the product competitiveness driven by Eyebright Medical’s R&D investments.

Of course, R&D alone is not sufficient for an enterprise; it must also understand the market. Eyebright Medical has established extensive connections with clinicians and experts by organizing or participating in industry conferences and academic seminars, thereby enhancing their awareness and recognition of domestic brands and achieving integration among industry, academia, research, and clinical practice. Through expert recommendations, its products have been included in government procurement for national foreign aid initiatives such as the “Africa Brightness Journey” and the “Belt and Road Brightness Journey.” Since 2017, the company has participated in dozens of such foreign aid projects. In this process, Eyebright Medical has not only been able to promptly collect user feedback on the clinical application of its products to update and iterate them, but also engage and strengthen relationships with numerous frontline clinicians.

Based on the winning bid results of the aforementioned “3+N” alliance, it is evident that Eyebright Medical’s shortlisted products are primarily mid-range monofocal aspheric intraocular lenses (IOLs), with prices ranging from RMB 980 to RMB 1,990. By incorporating toric functionality—notably making it the only domestically produced toric IOL currently available—the company has raised the unit price to RMB 3,016, thereby reaching the threshold of the high-end market segment.

Eyebright Medical initiated the R&D project for multifocal intraocular lenses several years ago, with cumulative investments approaching RMB 15 million, and the product has currently entered the registration phase. In addition, the R&D project for aspheric trifocal toric intraocular lenses has advanced to the clinical trial stage. Notably, both products are positioned at an internationally leading technological level, potentially paving the way for expansion into the high-end market segment in the future.

From a product perspective, there are currently dozens of domestically produced intraocular lens (IOL) products registered and marketed in China, predominantly consisting of mid- to low-end offerings. In terms of materials, some domestic products still utilize rigid PMMA (polymethyl methacrylate). Regarding optical design, certain domestic IOLs continue to employ spherical designs, which are less effective at correcting aberrations. Eyebright Medical is the only domestic manufacturer of high-end IOLs featuring additional functionalities such as astigmatism correction, preloaded delivery systems, blue light filtration, and heparin surface modification, placing its products in the first tier among Chinese enterprises.

With the assurance of product quality, domestic enterprises have been able to leverage their price advantages. Eyebright Medical develops and manufactures products with varying tiers and designs tailored to patients’ clinical conditions and willingness to pay. According to its prospectus, for products with equivalent performance, Eyebright Medical’s prices are only about 62% of those of imported brands. It is precisely this strong product foundation that has enabled the company to achieve volume growth through competitive pricing in centralized volume-based procurement programs. Eyebright Medical’s sales volume grew from 174,000 units in 2017 to 500,000 units in 2020, representing a compound annual growth rate (CAGR) of 42.1%. Driven by an increased proportion of mid-to-high-end intraocular lens (IOL) products in total sales, the average selling price rose from RMB 399 per unit in 2017 to RMB 447 per unit in 2020.

According to Eyebright Medical’s 2021 annual performance forecast, the net profit attributable to shareholders of the parent company for 2021 is expected to reach RMB 160 million to RMB 180 million, representing a year-on-year increase of RMB 63.4417 million to RMB 83.4417 million, or 65.7% to 86.42%. The change in performance is mainly attributed to an expected year-on-year sales volume growth of over 40% for its core product line of intraocular lenses (IOLs). In the domestic market, the company has been widely selected as a winner in centralized volume-based procurement programs for IOLs across various regions, leading to a continuous increase in the number of end customers. In the international market, with toric and extended depth of focus (EDoF) IOLs gaining customer recognition, sales volume is expected to grow by more than 50% compared to the same period last year.

Eyebright Medical’s strategic R&D approach, which has built a comprehensive product portfolio, serves as a key driver of its rapid performance growth.

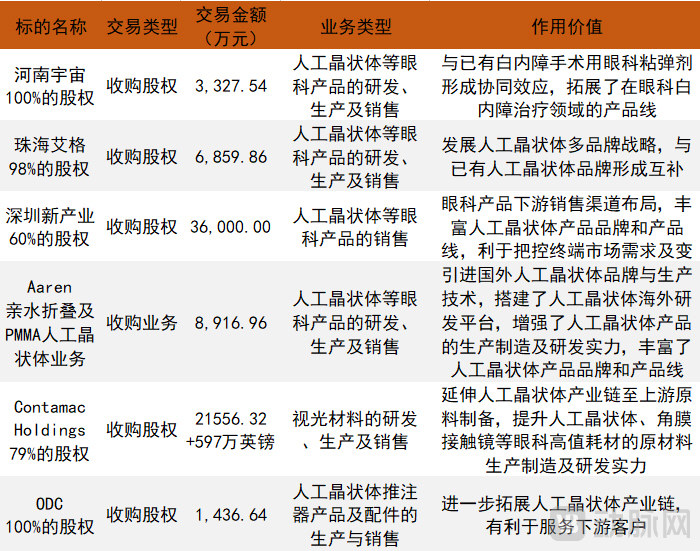

Haohai Biological Technology

Although this marks Haohai Biological Technology’s first appearance in this article, the company has actually been mentioned multiple times before, albeit through its brands acquired via its aggressive “buy-and-buy” strategy. Haohai entered the ophthalmology sector with ophthalmic viscoelastic devices used in cataract surgery. Over the past few years, it has successively acquired Henan Universe, Aaren, Shenzhen New Industries, Zhuhai Aiguo, Contamac, and ODC, establishing a business line that spans from upstream raw material production to specialized R&D, manufacturing, and sales of intraocular lenses (IOLs). The company also boasts R&D resources located in China, the United States, the United Kingdom, and France.

Among the numerous acquisitions, Aaren and Contamac are the most noteworthy. Aaren’s core business focuses on the development and manufacturing of basic blindness-prevention rigid intraocular lenses (IOLs), aspheric IOLs, and heparin-surface-modified IOLs. Its related products have obtained CE marking and registration certification from the China Food and Drug Administration (CFDA), along with qualifications for production and sales. Aaren’s IOL products are registered in China under its proprietary brands, Aaren and HexaVision, and have entered various regional markets through bidding processes and other channels. Aaren sells over 300,000 IOL units to China annually. With more than 3 million cataract surgeries performed in China each year, Aaren holds a market share exceeding 10%.

Contamac is a company incorporated in the United Kingdom in 1991. After nearly three decades of development, it has become one of the world’s largest upstream suppliers of ophthalmic materials, such as intraocular lenses (IOLs). Its business covers nearly 70 countries and serves more than 400 clients globally, with 24 patented technologies related to the processing, production, and testing of IOL materials. Through this acquisition, Haohai Biological Technology not only completed its industrial chain layout but also expanded its business scope globally, rapidly entering the high-value ophthalmic consumables sector.

Haohai Biological Technology’s comprehensive strategic layout has enabled it to establish a fully integrated industry chain, while also distributing Lenstec-brand intraocular lenses (IOLs) through its trading operations. Its basic-tier products are entirely self-manufactured. For the mid-to-high-end segment, the company differentiates its self-produced products from externally sourced ones by performance and price, thereby avoiding positioning overlap. The high-end market is expanded through the Lenstec brand.

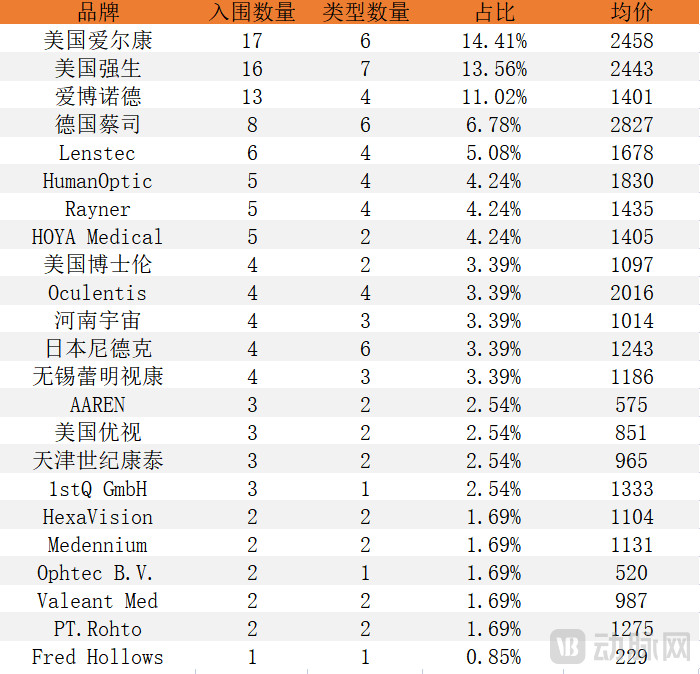

From the results of the “3+N” Alliance procurement, it can be observed that Haohai Biological Technology’s products cover a wider price range than those of Eyebright Medical. In terms of the number of selected items, Haohai Biological Technology had 15 products shortlisted, surpassing Eyebright Medical (13 products) and ranking just behind industry giants Alcon (17 products) and Johnson & Johnson (16 products). However, its portfolio is heavily weighted toward low- to mid-end products, indicating room for further expansion of its product line.

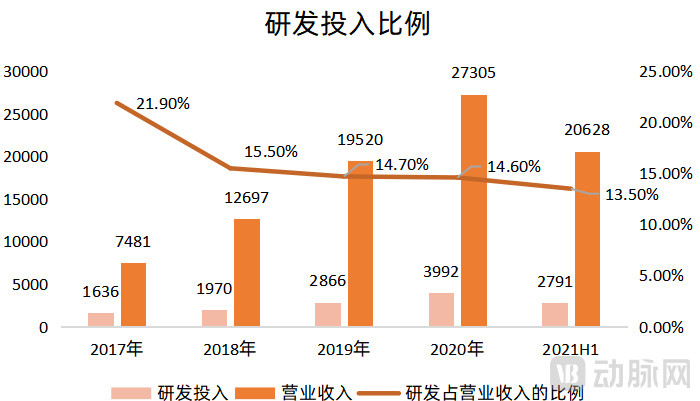

According to the 2021 semi-annual report disclosed by Haohai Biological Technology, the operating revenue for the period reached RMB 850 million, representing a year-on-year increase of 71.63%. Among this, the cataract product line generated RMB 250 million in operating revenue, a year-on-year growth of 71.90%. During the reporting period, R&D expenses exceeded RMB 73 million, an increase of 29.90% compared to the same period last year. These investments supported the strengthening of existing product lines, including hydrophobic molded aspheric intraocular lenses (in clinical trials), aspheric toric intraocular lenses (under registration testing), and aspheric multifocal intraocular lenses targeting the high-end market segment (in preclinical research). In addition, two products—pre-loaded aspheric intraocular lenses and heparin-surface-modified aspheric coated intraocular lenses—have already received regulatory approval and are expected to contribute to future revenue.

By combining organic growth with mergers and acquisitions, Haohai Biological Technology has continuously expanded and refined its product portfolio and integrated its industry chain, thereby securing a position in the first tier of domestic intraocular lens manufacturers through a distinct strategic approach.

Yan De Le

Is there no solution for companies with limited R&D scale and financial resources? Xi’an Yidele, a startup previously covered by VCBeat, has developed its own approach by focusing on fundamental intraocular lens (IOL) materials. Dr. Yang Zhou, head of the R&D team, explained, “For conventional optical materials, a high refractive index is typically accompanied by high dispersion, while a low refractive index corresponds to low dispersion. However, cross-linked polyolefins exhibit both a high refractive index and low dispersion.” This high-quality optical material outperforms mainstream hydrophobic acrylic materials in terms of maximum focal shift distance and maximum diameter of the blur circle, thereby reducing focal spread caused by chromatic aberration and improving image quality.

Furthermore, cross-linked polyolefin exhibits high elasticity and extensibility. The natural human crystalline lens has a diameter of approximately 8–10 mm, whereas commercially available intraocular lenses (IOLs) typically have a diameter of around 6 mm. At night, when the pupil dilates beyond the optical zone of the IOL, halos may appear in the visual field. The excellent extensibility of cross-linked polyolefin enables the implantation of an IOL with a diameter of 6.5 mm through the standard 2-mm incision used in mainstream cataract surgery. Currently, this cross-linked polyolefin IOL is undergoing multicenter clinical trials.

In addition to avoiding direct competition with rivals, the adoption of new materials serves another strategic purpose. According to Guo Guangxu, founder of YandeLe, “possessing independently developed intraocular lens (IOL) materials is the most effective approach to cost control. In the past, we purchased materials from third-party suppliers for further processing, leaving us dependent on their terms. Today, we hold patents covering all aspects of material synthesis and production, thereby retaining full control over our supply chain. With our proprietary materials, YandeLe’s IOL products not only deliver superior performance but also offer a significant price-to-performance advantage.”

For YandeLe, the inclusion of its self-developed intraocular lens (IOL) products, made from cross-linked polyolefin materials, in the centralized procurement program due to their cost-effectiveness is merely the first step in unlocking the domestic market. Expanding into overseas markets is YandeLe’s true objective. “In the future, YandeLe will position itself as a material supplier, establishing collaborations with international brands on the materials front, rather than competing head-on with giants like Alcon in the product market,” stated Guo Guangxu with clear strategic insight.

If Eyebright Medical can successfully pursue this path of product differentiation, it will undoubtedly secure a place in the intraocular lens market.

Currently, the competitive landscape for intraocular lenses (IOLs) in China is relatively fragmented, with a low level of domestic production. According to the recent “3+N” volume-based procurement program, a total of 23 brands participated, among which only five were domestic brands, indicating a dispersed market share. Even industry giants with highly concentrated international market shares have not established an absolute advantage.

According to the prospectus disclosed by Eyebright Medical, the overall localization rate of intraocular lenses (IOLs) in China was only 19%–20% in 2019, remaining at a relatively low level. China has attached great importance to the development of the domestically produced IOL industry. Since 2015, it has successively issued policies to encourage the growth of this sector, guide social resources toward this field, and create a favorable policy environment for the development of the IOL industry.

The future growth drivers for the intraocular lens (IOL) industry lie in import substitution. It is anticipated that, as seen in other sectors, domestic brands will rapidly replace imported products during the industry’s rapid growth phase by leveraging their price and channel advantages. In the subsequent maturity phase, following the completion of import substitution, leading domestic companies will drive terminal market expansion and achieve a second wave of growth by capitalizing on their technological advantages and channel development capabilities, while maintaining high profitability.

For domestic companies, how to stand out in the competition with multinational brands has become a question that must be considered. VCBeat has summarized the answers of three of them, but this is not enough. More participation and exploration by domestic enterprises are needed to arrive at their own solutions.