Why Overseas Orders Have Become the 'Stock Surge Code' for Chinese API Companies Amid Triple Price Rallies

APIs Have Truly Caught Fire.

The third year of the COVID-19 era has arrived. During this period, the capital markets have witnessed countless myths of market capitalization expansion, ranging from alcohol and protective masks to COVID-19 vaccines and oral antiviral drugs.

Among these developments, the most powerful and enduring catalyst has been the continuous progress in oral COVID-19 therapeutics. On February 12, China saw the arrival of its first truly imported oral anti-COVID-19 drug. On that day, the National Medical Products Administration (NMPA), in accordance with the relevant provisions of the Drug Administration Law, announced the conditional approval of the import registration for Pfizer’s combination pack of nirmatrelvir tablets and ritonavir tablets (Paxlovid) for the treatment of COVID-19, through an emergency review and approval process. Starting from the next trading day, listed companies in the innovative drug and contract research organization (CRO) sectors bucked the market trend and experienced a surge in their stock prices.More than 10 stocks, including Porton Pharma, Chengda Pharmaceutical, Yaben Chemical, Tuoxin Pharmaceutical, and Hybio Pharmaceutical, have successively and repeatedly hit their daily upper price limits. On February 16, Chengda Pharmaceutical and Yaben Chemical once again closed at their daily upper price limits.

In fact, the capital market opportunities brought by the COVID-19 pandemic have emerged multiple times since 2022.

For instance, on January 21, the stock prices of Borui Medicine and Fosun Pharma both hit their daily upper limits. This surge was driven by an agreement reached one day earlier between the Medicines Patent Pool (MPP) and Merck & Co., which authorized 27 generic drug manufacturers to use Merck’s newly approved oral COVID-19 drug, Molnupiravir, without paying patent licensing fees. Five Chinese pharmaceutical companies—Fosun Pharma, Borui Medicine, Longze Pharmaceutical, Desano, and Lonhua Pharmaceutical—were included in this authorization. Among them, the first four were licensed to produce both active pharmaceutical ingredients (APIs) and finished drugs, while Lonhua Pharmaceutical was authorized to manufacture APIs only.

For another example, on January 13, Andon Health Co., Ltd. recorded its 26th daily price limit increase since November 2021. This surge was driven by billions of yuan worth of orders for iHealth test kits from the U.S. government. According to Andon Health’s announcement, its U.S. subsidiary signed a Purchase Agreement with American ACC on January 13, 2022 (local time), securing cumulative orders totaling RMB 2.1 billion from the New York State Department of Health, the Commonwealth of Massachusetts, and the Executive Office of the U.S. Department of Health and Human Services.

The COVID-19 pandemic has transformed many people’s lives and profoundly reshaped the global healthcare supply chain. Many domestic healthcare companies that benefited from this shift have adjusted their previously extensive management practices, yet the frenzy in secondary market sentiment has, to some extent, amplified the growth boundaries achievable by their core businesses.

The World’s Pharmaceutical Factory in Transition

When it comes to the global pharmaceutical industry, people first think of India, the largest supplier, which provides 60% of the world’s drug formulations.

However, if we move further up the industrial chain of India’s pharmaceutical industry, we will find the presence of Chinese companies. Data shows that India is China’s largest export market for active pharmaceutical ingredients (APIs), with 70% of its APIs sourced from China. In the API sector, which closely resembles the chemical industry, these enterprises from China’s coastal cities have been a force to be reckoned with in the global pharmaceutical industry during the years when domestic medical policies and ecosystems were still underdeveloped.

In the 1990s, mature pharmaceutical industrial powers in Europe and the United States leveraged globalization to transfer high-pollution, energy-intensive chemical manufacturing industries to the Third World. Capitalizing on China’s reform and opening-up policy, the country absorbed a portion of the global production capacity for active pharmaceutical ingredients (APIs). To facilitate exports, many production bases were established not in inland transportation hubs, but in eastern coastal cities. Subsequently, early-phase pharmaceutical companies represented by Hisun Pharmaceutical, Huahai Pharmaceutical, Xianju Pharmaceutical, Tianyu Pharmaceutical, and Starry Pharmaceutical began selling their manufactured APIs to markets worldwide.

By 2017, data from the China Food and Drug Administration (CFDA) showed that China had become the world’s second-largest pharmaceutical consumer market and the largest exporter of active pharmaceutical ingredients (APIs). At that time, there were nearly 5,000 API and finished dosage form manufacturers across China. The annual main business revenue of the pharmaceutical manufacturing industry exceeded RMB 2.5 trillion, with profits surpassing RMB 270 billion, making it one of the few industries whose growth rate outpaced that of GDP.

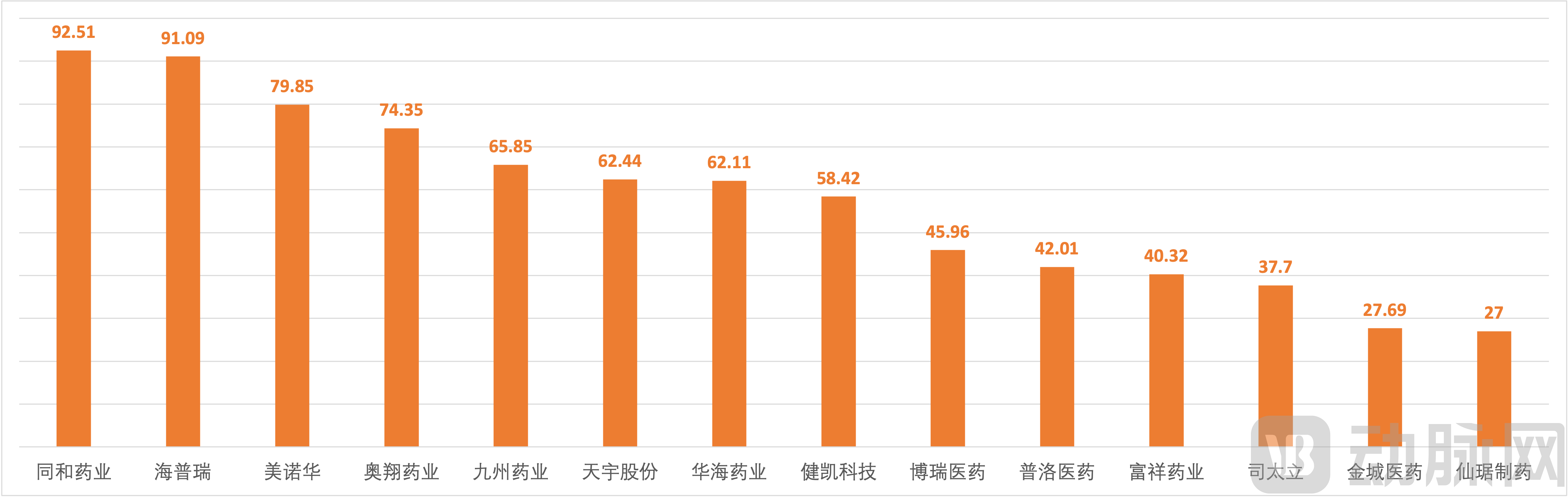

Proportion of Overseas Revenue (%) for Listed Chinese Companies Specializing in Active Pharmaceutical Ingredients (APIs) in 2019

Meanwhile, as the domestic pharmaceutical ecosystem continues to improve, API suppliers are increasingly extending their business capabilities downstream into finished dosage forms and CDMO services. This trend creates high barriers for ordinary enterprises in areas such as regulatory registration and certification capabilities, process development expertise, and GMP systems. Data shows that nearly 50 Chinese formulation manufacturers have obtained certifications or passed inspections in Europe and the United States, with pharmaceutical manufacturing exports exceeding $13.5 billion. Among these, products such as Huahai Pharmaceutical’s losartan and Hengrui Medicine’s cyclophosphamide have successively become popular items in the U.S. market.

Although the limited growth potential offered by upstream manufacturers is hardly exciting in an era marked by the continuous rise of innovative drugs, ongoing transformations are reshaping this industry and its position within the global industrial chain.

On one hand, in recent years, leading enterprises have been exploring automated, intelligent, continuous, and miniaturized production, as well as the iteration of cutting-edge technologies such as enzymatic catalysis and photochemistry, with the aim of achieving better product quality and lower manufacturing costs. The FDA has also issued guidance documents on continuous manufacturing, encouraging manufacturers of active pharmaceutical ingredients (APIs) and generic drugs to employ continuous reaction processes in the production of small-molecule chemical drugs to enhance product quality and reduce manufacturing costs.

On the other hand, the pace of transition from non-compliant to compliant operations is accelerating, leading to further consolidation in China’s active pharmaceutical ingredient (API) industry. With the implementation of the Environmental Protection Tax Law and the pollutant discharge permit system, along with the normalization of environmental inspections, leading manufacturers with strong financial capabilities have significantly increased their investments in this area. For instance, Huahai Pharmaceutical and Apeloa Pharmaceutical have each invested RMB 500–1 billion in environmental protection measures. Meanwhile, numerous small and medium-sized API and intermediate manufacturers unable to meet environmental standards are gradually exiting the market.

As the world’s pharmaceutical manufacturing hub, China’s active pharmaceutical ingredient (API) industry is advancing toward the high end after nearly three decades of iterative development.

Capacity Allocation Sparks Frenzy in Pharmaceutical Stocks

Therefore, when oral COVID-19 drugs finally hit the market and major pharmaceutical companies faced urgent capacity constraints, Chinese active pharmaceutical ingredient (API) manufacturers were thrust into the spotlight, driving a sharp surge in their market capitalizations.

To date, three specific anti-COVID-19 drugs have been granted emergency use authorization worldwide.

First, in late 2021, Merck’s Molnupiravir was launched in the UK for the treatment of adult patients with mild-to-moderate COVID-19. Subsequently, the U.S. Food and Drug Administration (FDA) granted emergency use authorization for two oral anti-COVID-19 drugs: Pfizer’s Paxlovid and Merck’s Molnupiravir.

As soon as these two oral COVID-19 drugs were launched, they became a powerful driver for the performance growth of their respective companies.

According to Pfizer’s 2021 annual report, the multinational pharmaceutical company generated $81.3 billion in full-year revenue, a 95% year-on-year increase. Excluding revenue contributed by its COVID-19 vaccine Comirnaty and oral antiviral drug Paxlovid, revenue amounted to approximately $44.4 billion, representing a 6% year-on-year growth. Regarding its 2022 performance outlook, Pfizer projects full-year revenue of $98 billion to $102 billion, raising its revenue forecast for Comirnaty to approximately $32 billion and preliminarily estimating Paxlovid revenue at around $22 billion.

Regarding Merck & Co., in the fourth quarter of 2021, when the first batch of Molnupiravir was delivered, the company’s sales increased by 24% year-over-year, significantly higher than the full-year growth rate of 17%. In its financial report, Merck disclosed that it would ship more than 4 million treatment courses to over 25 countries and regions, including approximately 3 million treatment courses supplied to the U.S. government. Furthermore, Merck has entered into a long-term supply agreement with UNICEF to provide more than 3 million treatment courses of Molnupiravir in the first half of 2022.

The third oral COVID-19 drug is of domestic origin. In November 2021, clinical trials for VV116, a small-molecule drug developed by Junshi Biosciences, were approved to commence. The following month, it received emergency use authorization in Uzbekistan, making it the only domestically approved small-molecule drug for COVID-19 treatment to enter clinical trials.

With nearly 100 million confirmed COVID-19 cases worldwide and only three oral antiviral drugs available, the production capacity pressures facing Merck, Pfizer, and Junshi Biosciences are self-evident.

At present, oral COVID-19 drugs are largely in short supply. For instance, Merck stated that most of the 10 million treatment courses produced by the end of 2021 had been purchased by governments worldwide. Subsequently, Merck agreed to allow other pharmaceutical manufacturers to produce molnupiravir, aiming to expand global production capacity and help millions of people in poorer countries access the medication. This limited global supply of oral COVID-19 drugs has undoubtedly become the “limit-up code” driving up the market capitalization of domestically listed pharmaceutical companies.

The consecutive stock price surges of Borui Medicine and Fosun Pharma, mentioned at the beginning of this article, stem from the hypothesis that the global allocation of Molnupiravir production capacity would drive substantial performance growth for upstream active pharmaceutical ingredient (API) manufacturers.

Pfizer’s Paxlovid has likewise sparked renewed enthusiasm in the secondary market. On November 16 and November 28, 2021, Asymchem announced that it had signed two major contracts with “a large pharmaceutical company,” with a total transaction value of RMB 5.778 billion—nearly twice Asymchem’s total revenue in 2020. Industry observers believe that the so-called “large pharmaceutical company” and the product covered by the orders refer to Pfizer and its blockbuster COVID-19 therapeutic. At the time, buoyed by this order, Asymchem, which had been experiencing a sustained decline in market capitalization, saw its valuation rise for several consecutive days.

In addition, on February 14, Ascletis Pharma announced that the company had submitted marketing authorization applications for ritonavir (100 mg film-coated tablets) to Germany, France, Ireland, and the United Kingdom through its European distributor. Meanwhile, marketing authorization applications for ritonavir in other regions, including European countries, North American countries, and Asia-Pacific countries, are also expected to be submitted in the near future. Oral ritonavir tablets are one of the components of Pfizer’s Paxlovid. On the same day, Ascletis Pharma’s stock price closed up 8.39%.

In fact, research on small-molecule drugs for COVID-19 treatment in China has been progressing vigorously. For instance, Kintor Pharmaceutical’s proclutamide is conducting Phase III global multicenter clinical trials for the treatment of patients with mild to moderate COVID-19 in the United States, Brazil, South Africa, Argentina, Malaysia, the Philippines, and other countries. Similarly, Azvudine, developed by Henan Real Biopharmaceutical Co., Ltd. (Real Biotech), is advancing through Phase III clinical trials for COVID-19 treatment in China, Brazil, and Russia. Meanwhile, FB2001 from Frontier Biotechnologies is undergoing Phase I clinical studies in the United States.

As more oral COVID-19 drugs enter clinical use, the competitive landscape on the pharmaceutical supply side is undoubtedly poised for another round of reshuffling. Interestingly, certain capital market mix-ups during this period are, in fact, witnessing the shifting status of Chinese active pharmaceutical ingredient (API) manufacturers within the global supply chain.

For instance, although some companies associated with the concept of oral COVID-19 drugs have clarified that they have not secured production orders for Pfizer’s oral COVID-19 medication, this has done little to dampen the enthusiasm of secondary market investors. Among these are Jinghua Pharmaceutical and Yaben Chemical, mentioned at the beginning of this article. On February 16, despite repeatedly emphasizing that they had not joined the global supply chain for oral COVID-19 drugs, both companies saw their stock prices surge significantly once again.

Certainly, we would prefer to see the rumored API manufacturers truly emerge as the white knights addressing the current global shortage of pharmaceutical production capacity, filling the gap in oral COVID-19 treatments while simultaneously strengthening and expanding their own businesses. However, not all API or intermediate manufacturers are capable of undertaking the production capacity for oral COVID-19 drugs. For instance, according to Merck’s agreements, licensed pharmaceutical companies are required to promote and sell the drug in countries where authorization has been granted. This means that a company’s sales volume after licensing depends on its ability to establish an international sales network and manage its supply chain effectively.

For instance, Fosun Pharma, which has recently received authorization, stated that the company already possesses a mature sales network and upstream and downstream customer resources in both English- and French-speaking regions of Sub-Saharan Africa. In October 2021, Tridem Pharma, a member enterprise of Fosun Pharma, officially commenced operations of its first regional pharmaceutical distribution center in Africa, located in Côte d’Ivoire. The establishment of this center helps ensure the sustained accessibility of pharmaceutical and healthcare products across the African region.

Advancement of Roles in the Global Industrial Chain

It must be acknowledged that,The shortage of demand triggered by the COVID-19 pandemic has already yielded substantial commercial returns for many active pharmaceutical ingredient (API) manufacturers.

For instance, in terms of financial performance, several pharmaceutical companies are projected to be the first to double their profits in 2021. According to incomplete statistics, among the COVID-19-related pharmaceutical companies that have issued 2021 annual forecasts, approximately 10 have projected a year-on-year increase in net profit of 100% or more. Among them, Haitai Bio recorded the highest growth, with the median projected net profit increasing by more than 2.2 times. The company stated that during the reporting period, the growth of CRO and CDMO services provided by its wholly-owned subsidiaries, Tianjin Hankang Pharmaceutical Biotechnology Co., Ltd. and Hanrui Pharmaceutical (Jingmen) Co., Ltd., drove increases in operating revenue and net profit compared to the same period last year. The company expects to turn losses into profits during the reporting period.

For another example, Pharmablock Sciences, which was expected to post strong full-year earnings, also achieved a doubling of its profits. The company projected its net profit for 2021 to range from RMB 479 million to RMB 497 million, representing a year-on-year increase of 160% to 170%. Pharmablock Sciences noted that in 2021, it further solidified its CDMO business layout and enhanced its drug discovery technology service platform. Despite no significant expansion in production capacity, the company expects its operating revenue to grow by 15%-20% compared with 2020, driven by continued scaling of operations.

But more importantly, perhaps what matters even more is the long-term value that this aggressive shift in supply and demand dynamics brings to corporate operations themselves.

On one hand, some astute domestic medical enterprises have made timely strategic deployments and are gradually establishing their global influence. Against this backdrop, it is worth noting that in the past, small-scale Chinese medical devices typically relied on hitching a ride with established major brands to enter the global market. However, the international expansion of COVID-19 antibody testing reagents has reversed this trend.

Among these cases, Andon Health has rapidly established its proprietary brand of COVID-19 test kits in overseas markets through a series of mergers, acquisitions, and integrations. In November 2021, Andon Health announced that its subsidiary, iHealth Labs Inc., had received Emergency Use Authorization (EUA) from the U.S. Food and Drug Administration for its novel coronavirus antigen home self-test OTC kit. Shortly thereafter, the company announced that iHealth had secured substantial orders from the U.S. market. It is understood that the iHealth test kits are part of Andon Health’s proprietary iHealth brand, manufactured in China, and have gained significant popularity in the U.S. market. This government contract, which attracted widespread attention from China’s capital markets, had a total value including tax and freight of US$1.275 billion (approximately RMB 8.1 billion), exceeding 50% of the company’s audited main business revenue for 2020 (RMB 1.004 billion). In a sense, this represents a rare instance of a Chinese IVD brand achieving genuine global expansion.

Some companies have also gradually expanded from the B2B market to the B2C market through steady penetration. For instance, Orient Gene has similarly established and strengthened its own overseas brand. According to Orient Gene’s 2021 interim profit forecast, the company reported revenue of RMB 6.382 billion and net profit of RMB 3.394 billion in the first half of the year, representing a year-on-year increase of 547.82%, making it the enterprise with the highest revenue and net profit in the IVD sector during that period. In this process, Orient Gene has enhanced cooperation with clients such as Siemens, McKesson, CVS, Walmart, and Walgreens, while continuously expanding the influence of its proprietary brands, “Orient Gene” and “Hengjian,” in overseas markets.

On the other hand, it is about achieving a customer structure that truly matches those of leading global players. For both active pharmaceutical ingredient (API) manufacturers and contract development and manufacturing organizations (CDMOs), their relatively low bargaining power within the industry chain has long been a constraint hindering their efficient expansion into overseas markets. These enterprises started by providing upstream products and services to major brands, and for a considerable period, their performance was largely dependent on unstable business relationships with a limited number of clients.

Driven by the COVID-19 pandemic, this situation is gradually changing. For instance, despite its highly successful transformation, Porton Pharma Solutions has struggled to break into the top tier of domestic CDMOs due to its heavily concentrated major customer structure. According to Porton Pharma Solutions, the scale of its business with Pfizer has continued to expand since 2019. In 2019, the company generated RMB 58.46 million in revenue from Pfizer, accounting for 3.77% of its total annual revenue; this figure rose to RMB 103.46 million the following year, representing 4.99% of that year’s total revenue. In the first nine months of 2021 alone, Pfizer placed orders worth over RMB 150 million with Porton Pharma Solutions, accounting for 7.46% of its revenue during that period. More recently, the company received a new batch of Purchase Orders totaling USD 681 million from a subsidiary of the multinational pharmaceutical giant Pfizer. This amount exceeds 50% of the company’s audited revenue for the most recent fiscal year, further diluting Porton Pharma Solutions’ reliance on major customers.

Admittedly, the novel coronavirus continues to mutate and wreak havoc. For domestic medical innovation enterprises that have already established a foothold in the global supply chain for COVID-19 diagnosis and treatment, COVID-19 remains a “limit-up code” that will continue to unlock a fast track to wealth. Yet more critical than their inflated market capitalizations and heightened market expectations is the correction of their growth trajectories.