Ophthalmology Sector Surges: $1.2B+ in Funding and 4 IPOs—Can It Get Even Hotter?

The ophthalmology sector is racing ahead, with nearly 100 investors already making moves.

Since 2021, both top-tier investment firms such as Northern Light Venture Capital, Hillhouse Investment, Sequoia China, Legend Capital, and Origin Ventures, as well as the strategic investment departments or industrial capital arms of corporate giants including Tencent, Xiaohongshu, Aier Eye Hospital, Sunshine Life Insurance, and SND Venture Capital Group, have made investments in the ophthalmology sector.

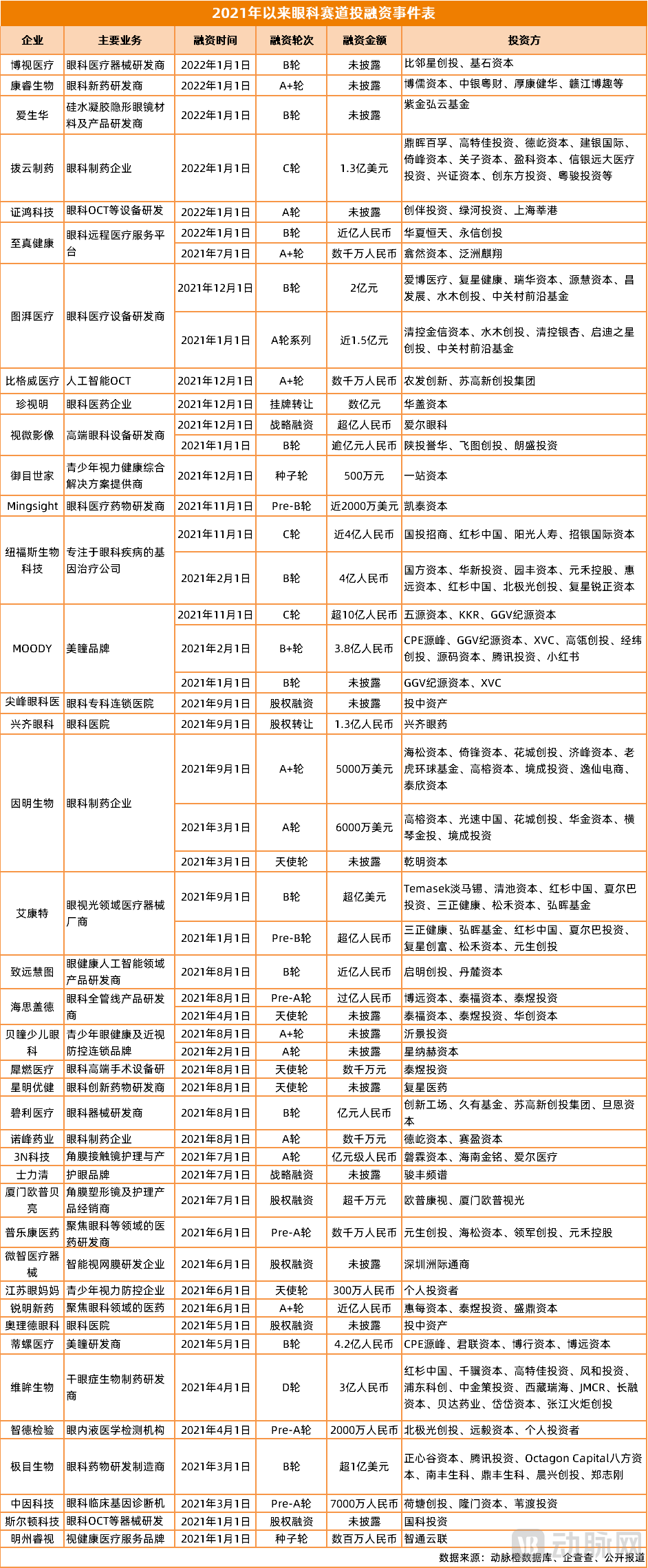

According to data from the VCBeat database, as of now, China’s ophthalmology primary market has seen a total of 51 financing events since 2021, with 40 companies securing funding. Nearly 100 investment institutions were involved, and the total amount raised exceeded RMB 8 billion, setting a new historical record.

In the secondary market, Gaoshi Medical, Clear Medical, and Huaxia Eye Hospital each filed prospectuses over the past year, while Zhaoko Ophthalmology, Chaoju Eye Care, Airdoc, and Mingyue Optical successfully completed their initial public offerings (IPOs), briefly sparking heightened interest in the ophthalmology sector.

As a veritable "golden track," ophthalmology has long been a key focus for capital investment: Currently, 400 million patients in China suffer from various eye diseases, with nearly 300 million of them being myopic. As population aging intensifies and modern lifestyles evolve, the burden of eye diseases in China will become increasingly prominent, revealing substantial growth potential in the market space.

Regrettably, apart from the ophthalmic medical services sector, which has given rise to mega-corporations with market capitalizations exceeding RMB 100 billion, such as Aier Eye Hospital,There is a significant shortage of innovative platform companies with global competitiveness in China, whether in the field of ophthalmic drugs or ophthalmic devices.

“Taking the ophthalmic medical equipment niche as an example, this market is characterized by an import monopoly. In terms of sales revenue, imported ophthalmic equipment suppliers account for 98% of the market share; even by sales volume, their share reaches 95%,” said Luo Xi, an investor who has long focused on the ophthalmology sector, in an interview with VCBeat.

Driven by recent policy support and technological innovation, the wave of domestic substitution is accelerating, and ophthalmology is approaching a critical turning point.

For example, in January this year, the National Health Commission issued the "14th Five-Year Plan for National Eye Health (2021-2025)." The plan points out that a five-tier ophthalmic medical service system at the national, regional, provincial, municipal, and county levels should be established and improved to optimize the allocation of medical resources. It also emphasizes strengthening the setup and development of ophthalmology departments in general hospitals at level II and above, addressing weaknesses in ophthalmology and its supporting disciplines. This means that the industry will increase its attention to and procurement of ophthalmology-related drugs and medical devices.

“The continuous introduction of favorable policies related to ophthalmology, coupled with heightened public health awareness, has driven capital attention toward innovative ophthalmic drugs and medical devices to unprecedented levels,” said Luo Xi.As a sector that combines both medical and consumer attributes, the ophthalmology track has begun to produce a number of high-quality innovative companies, thereby providing the industry with a broader range of investment targets.“This is the core reason why capital is flocking to enter the market.”

What niche opportunities have emerged in the ophthalmology sector, which has seen a surge of capital investment? What pain points remain? And what are the future evolutionary trends? To address these questions, VCBeat has conducted research and interviewed industry stakeholders to gain insights into the answers.

Ophthalmology is a healthcare sector characterized by the triad of “pharmaceuticals + medical devices + services,” with a market size nearing RMB 200 billion.

From the overall situation in ophthalmology over the past year,Financing events in ophthalmic services accounted for approximately 10% of the industry total, with the remaining 90% concentrated entirely in the field of ophthalmic pharmaceuticals and medical devices.

“Ophthalmic services were the first segment to gain momentum in the ophthalmology sector, and several regional leaders have already emerged, including Aier Eye Hospital, Chaoju Eye Care, Huaxia Eye Hospital, He’s Eye Hospital, and Purui Eye Hospital. However, these companies have generally encountered growth bottlenecks in sustaining their business expansion,” said Luo Xi. Therefore, from an investment value perspective, the ophthalmic pharmaceuticals and medical devices sector has become a promising direction for the near future.

On the one hand, this is because the mid-to-high-end ophthalmology market is predominantly dominated by foreign companies, presenting significant opportunities for domestic substitution.

Taking ophthalmic drugs as an example, statistical data on the usage of ophthalmic medications in public hospitals across key provinces and cities in China shows that imported drugs account for more than 50% of the market. The top four players in the ophthalmic drug market are Novartis (Switzerland) with a 25.35% share, Santen Pharmaceutical (Japan) with 14.24%, URSAPHARM (Germany) with 6.32%, and Shenyang Xingqi Eye Pharmaceutical with 4.71%. It is evident that only one domestic ophthalmic company ranks among the top four.

On the other hand, there are still gaps in therapeutic science and technology on the supply side of ophthalmic drugs and medical devices.

For instance, cataracts, the leading cause of blindness worldwide, are the most prevalent eye disease among the elderly in China. Currently, there are no curative pharmaceutical treatments available; patients primarily rely on surgical interventions and medical devices for management. This underscores a substantial market demand within ophthalmology for more effective drugs and superior medical devices.

More importantly, there is still market space and opportunity for the emergence of leading enterprises in the field of ophthalmic pharmaceuticals and medical devices.“Businesses that offer both a margin of safety and the ability to ensure high growth and long-term, sustainable profitability are what investors dream of most,” said Luo Xi. “The sustained rise in Aier Eye Hospital’s stock price over the past decade was largely driven by its consistent annual net profit growth of more than 30%. This growth has been fueled by the steady release of demand in the ophthalmology market, which also suggests that there is sufficient incremental market potential in ophthalmology to nurture new industry leaders in the future.”

In a nutshell,Driven by the major wave of domestic substitution, robust demand on the supply side, and the significant potential to cultivate industry-leading enterprises, China’s ophthalmology sector has entered a new stage of development in the research and development of pharmaceuticals and medical devices.

Over the past year, investment firms have poured more than 8 billion yuan into the sector, igniting a new wave of financing in ophthalmology.

“Every disease related to ophthalmology can even be considered a separate track.” In Luo Xi’s view, investing in ophthalmology requires an in-depth understanding of ophthalmic diseases.

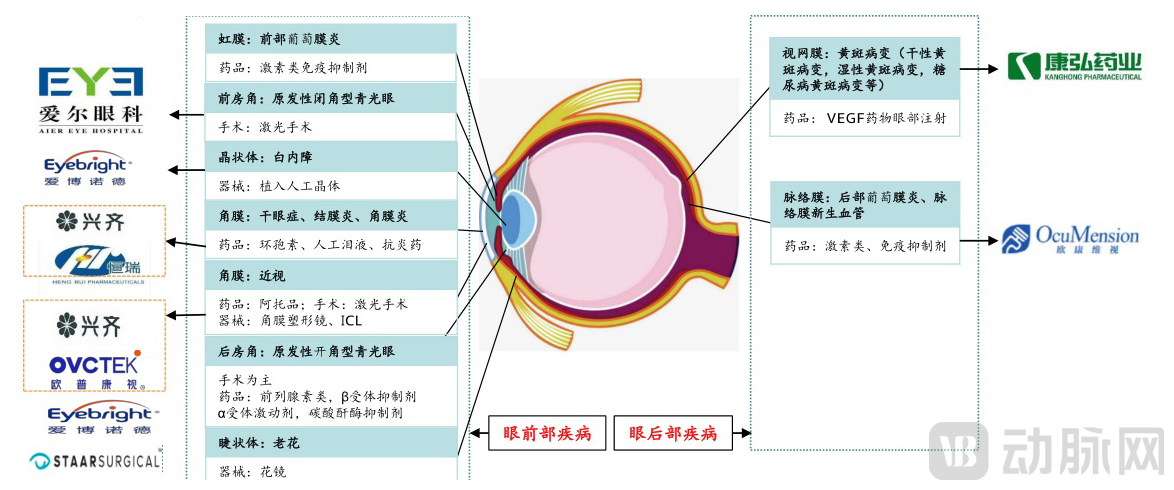

According to the report by Haitong Securities,Ophthalmic diseases can be classified into two major categories based on anatomical location: anterior segment diseases and posterior segment diseases.Among these, anterior segment diseases include cataracts, dry eye disease, myopia, glaucoma, conjunctivitis, and uveitis; posterior segment diseases include wet age-related macular degeneration, diabetic maculopathy, and posterior uveitis.

(Image source: Haitong International)

(Image source: Haitong International)

Focusing on these common ocular diseases, the ophthalmic device sector primarily encompasses subfields such as ophthalmic OCT, ICL (phakic intraocular lenses), IOLs (intraocular lenses), orthokeratology lenses, ultra-widefield fundus cameras, phacoemulsification and vitrectomy systems, femtosecond lasers, ophthalmic surgical microscopes, optical biometers, contact lenses (including cosmetic colored lenses), and spectacle frames.

In terms of financing frequency, the two sectors of ophthalmic OCT and cosmetic contact lenses have recently become hot favorites among investors.

“The inclusion of intraocular lenses in centralized procurement, along with the fact that sectors such as ultra-widefield fundus cameras, ophthalmic surgical microscopes, and prescription eyeglasses have already become highly saturated ‘red oceans,’ are the primary reasons for the relatively weak interest from capital,” said Luo Xi.

OCT (Optical Coherence Tomography) is the gold-standard imaging modality for the clinical diagnosis and management of fundus diseases. It enables visualization of retinal pathological changes and has been applied in ophthalmic clinical practice since the early 1990s, undergoing three generations of technological evolution: from time-domain OCT to spectral-domain OCT, and finally to swept-source OCT.

Currently, the mid-to-high-end market for ophthalmic OCT in China is almost monopolized by imported products, such as those from Germany's Zeiss and Heidelberg, Japan's Topcon, and the US's Optovue; domestically produced products still lag significantly behind their imported counterparts in terms of performance specifications.

“The complex operational procedures of traditional OCT and the reliance on highly specialized physicians for image interpretation have limited its widespread adoption at the primary care level. Consequently, domestic substitution and the development of higher-performance products present future opportunities for innovative enterprises.“said Luo Xi.”

In terms of strategic layout, Topai Medical, which secured financing twice within a year, focuses on high-end ophthalmic OCT products. The company has launched two ophthalmic OCT systems named “Beiming·Kun” and “Yaoguang·Xing.” Specifically, the “Beiming·Kun” features a sweeping speed of 400,000 A-scans per second, with a single-scan imaging length of 24 mm. At this 400,000 A-scan rate, its imaging depth remains at 6 mm, while the axial resolution reaches as high as 3.8 μm.

Zhenghong Technology, which secured financing this January, focuses on the R&D and manufacturing of optical imaging devices centered on ophthalmic OCT. Its anterior segment OCT product enables the measurement of multiple parameters in the anterior eye segment, offering advantages such as high measurement accuracy, multifunctional integration, and low cost.

Bigwei Medical, which completed its financing round at the end of last year, primarily focuses on AI-based analysis and computer-aided diagnosis systems for ophthalmic imaging. Its developed ophthalmic OCT image-assisted diagnostic software, MIAS 3000, has initiated the testing and certification process for a Class III medical device registration certificate.

“In clinical practice, the traditional diagnosis of most ophthalmic diseases requires the combined use of fluorescein fundus angiography (FFA) and optical coherence tomography (OCT). Although FFA is highly effective in diagnosing fundus diseases, it can cause adverse reactions in patients during the examination, such as nausea, dizziness, and allergic reactions, and may even be life-threatening,” said Luo Xi. “Optical coherence tomography angiography (OCT-A) provides an effective alternative, making it a major trend in the development of OCT.”

Turning to colored contact lenses, as a type of contact lens with strong cosmetic appeal, they possess significant consumer product attributes, making them a highly sought-after target for capital investment.

Specifically, there are two core driving forces. First, in terms of market size, Mob Research Institute predicts that the market size of China's colored contact lens industry will reach 50 billion yuan by 2025, with the potential to become the most significant market globally.

Second, in terms of market structure, “the total number of companies involved in the colored contact lens industry in China has exceeded 1,800, but no dominant market leader has yet emerged. Once a brand manages to break through first, it will capture a significant share of the market,” said Luo Xi. He noted that the colored contact lens sector is characterized by an extremely high repurchase rate, making it crucial to establish strong brand recognition and consumer mindshare.

According to data from Qianzhan Industry Research Institute, in 2020, the repurchase rate for lipstick products in China was 20%, while that for colored contact lenses reached 30%–50%, nearly twice the former.

In terms of its product portfolio, Diluo Medical, which completed a RMB 420 million Series B financing round last year, currently holds seven Class III medical device registration certificates. These cover a full range of contact lens products, including daily, monthly, semi-annual, and annual disposable lenses, comprising one certificate for clear lenses and six for colored contact lenses. Additionally, Diluo Group possesses industry-exclusive registration certificates for seven-color and pearlescent colored contact lenses.

MOODY, a colored contact lens brand founded by Ci Ran, a former Sequoia Capital investor born in the 1990s, has secured over RMB 1 billion in financing. The company has selected etafilcon A as the core material for its lenses. This material, specifically designed for sensitive eyes, has received triple certification from China’s NMPA, the U.S. FDA, and the EU CE. Building on this foundation, the MOODY team has incorporated hyaluronic acid and PVP factors into the lenses, employed a sandwich color-locking technology in the manufacturing process, and utilized high-precision automated production in its factories to ensure quality control.

“In the healthcare sector, centralized procurement has introduced uncertainty. For instance, the centralized procurement of intraocular lenses launched in Guangdong last year saw price cuts of up to 90%, significantly impacting the entire segment. However, colored contact lenses are unique in that they are virtually immune to centralized procurement, ensuring strong growth certainty and remaining a key focus for investors,” said Luo Xi.

Another ophthalmic device with immunity from centralized procurement is the orthokeratology lens (commonly known as “OK lenses”), which is essentially a highly oxygen-permeable contact lens made from synthetic polymer materials. However, unlike conventional glasses or contact lenses, OK lenses are worn only during sleep at night, allowing users to regain normal vision upon waking the next day.

(Evolution of Orthokeratology Lens Products; Image Source: Guosen Securities)

(Evolution of Orthokeratology Lens Products; Image Source: Guosen Securities)

“Orthokeratology lenses have high barriers to entry. Currently, only about 10 companies are approved in China, including four domestic brands: Autek China, Eyebright Medical, Hengtai Optical, and Tianjin Shidajia,” said Luo Xi.Orthokeratology (OK) lenses represent a highly attractive niche segment within the ophthalmic device market, characterized by high unit prices, high gross margins, strong customer stickiness, and a continuously rising penetration rate.“For latecomers, the primary competition lies in technological strength, product advantages, and the time window for obtaining regulatory approval.”

In the field of ophthalmic medications, three mainstream directions have currently emerged.

First, traditional pharmaceuticals, namely small-molecule chemical drugs; second, large-molecule biologics, with currently investigational ophthalmic drugs in China predominantly being large-molecule agents; and finally, gene and cell therapies, which have emerged in recent years.

Different drugs vary in their routes of administration. Macromolecular drugs and gene- or cell-based therapies are generally administered via injection, whereas small-molecule drugs are typically delivered locally as eye drops or orally.

“Drug development for the treatment of five mainstream diseases—dry eye disease, refractive errors, fundus vascular diseases, cataracts, and glaucoma—is a key focus of capital attention.“Luo Xi stated, ‘This presents both an opportunity and a challenge for innovative pharmaceutical companies, as large pharmaceutical firms are also entering this field.’”

Taking dry eye disease as an example, it has the largest patient population and significant market potential, attracting pharmaceutical companies such as Hengrui Medicine, Xingqi Eye Pharmaceutical, CMS, and Ocumension Therapeutics to invest in drug development for this indication, including both generic and innovative drugs. Therefore,For innovative enterprises in ophthalmic drug development, originality is the key to breaking through.

From the perspective of pipeline layout and development progress, R&D of novel ophthalmic drugs has reached a critical juncture among innovative companies that have recently secured financing. For instance, Boyun Pharma, which raised $130 million in January this year, focuses exclusively on independently developed products with global rights. Its portfolio largely consists of first-in-class novel drugs featuring internationally pioneered new indications and novel mechanisms of action, addressing major ophthalmic diseases such as ocular surface disorders, fundus diseases, and glaucoma. The company’s pipeline includes two international multicenter Phase III clinical trials for two indications, three Phase II clinical trials in the United States, two candidates at the stage of submitting clinical trial applications, and three preclinical research projects.

Kangrui Biopharma, which secured financing last month, currently has a Class 1 novel drug pipeline poised to complete Phase I clinical trials in both China and the United States. The company is also conducting multiple investigator-initiated trials (IITs) for various indications in China, with expectations to initiate Phase II clinical trials for two different indications in both countries by the end of the year. Reportedly, this novel drug has the potential to become the world’s first eye drop formulation for treating ocular neovascular diseases. Another pipeline focused on preventing and treating cataracts has entered the preclinical research stage and is expected to submit an Investigational New Drug (IND) application by year-end.

NR082 (rAAV2-ND4, NFS-01), the core product of Nuofo Biopharma backed by Sequoia China, is the first ophthalmic in vivo gene therapy drug in China to receive clinical trial approval. The first patient was enrolled and dosed in the Phase 1/2/3 clinical trials in June 2021.

Jimu Biopharma, backed by Tencent, currently has three licensed products in Phase III clinical development: ARVN001 (Fengmai®) for the treatment of uveitic macular edema, ARVN002 for the treatment of progressive myopia in children, and ARVN003 for the treatment of presbyopia.

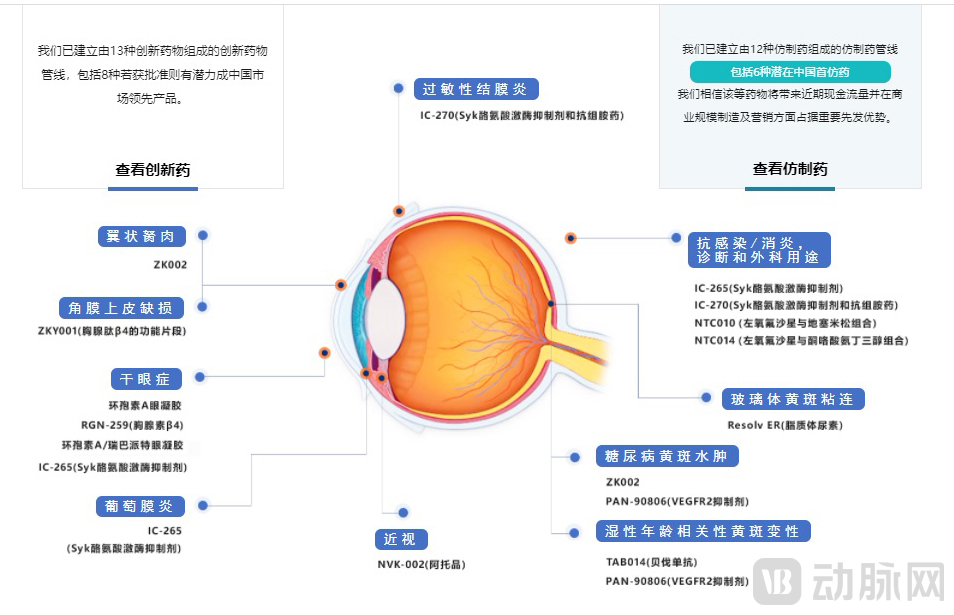

Zhaok Eye Care’s marketed pipeline is primarily focused on five major ophthalmic indications: dry eye disease (DED), wet age-related macular degeneration (wAMD), diabetic macular edema (DME), myopia, and glaucoma.

(Zhaoke Ophthalmology’s Innovative Drug Pipeline Layout. Image source: Company official website)

(Zhaoke Ophthalmology’s Innovative Drug Pipeline Layout. Image source: Company official website)

“The market size for ophthalmic pharmaceuticals in China is approximately RMB 20 billion, accounting for 10% of the entire ophthalmology sector, which represents a relatively low proportion. The core reason lies in the high difficulty of ophthalmic drug development, prolonged waiting periods due to clinical trials, and a high attrition rate even after regulatory approval. These factors have led many pharmaceutical companies to rely primarily on external licensing rather than independent innovation, resulting in few truly first-in-class drugs being developed,” said Luo Xi. He warned that if innovative enterprises fail to promptly address fundamental technical challenges, the sector will remain vulnerable to foreign control in the future. “The development of innovative ophthalmic drugs is a difficult yet worthwhile endeavor; in the long run, it is certain to deliver substantial returns to both companies and investors.”

In summary, within the ophthalmic device sector, optical coherence tomography (OCT) and cosmetic contact lenses are the key niche areas currently attracting significant capital investment, while orthokeratology (OK) lenses present substantial opportunities in the medium to long term. In the ophthalmic pharmaceutical sector, capital is primarily focused on the research and development of therapeutics for five mainstream conditions: dry eye disease, refractive errors, fundus vascular diseases, cataracts, and glaucoma, with originality serving as a critical evaluation metric.

China’s ophthalmology sector has long lacked high-quality investment targets, a fact evident from the secondary market’s enthusiastic reception of leading ophthalmic companies.

In January 2017, after Autek China, dubbed “the first stock in optometry and vision care technology,” listed on the A-share market, its shares surged in the secondary market. At last year’s peak, its market capitalization approached RMB 80 billion, representing a more than 50-fold increase in its share price.

In July 2020, Ocumension Therapeutics, an innovative ophthalmic pharmaceutical company, listed on the Hong Kong Stock Exchange. Riding on the halo of being the “leading player in ophthalmology,” its stock price surged by 152% on the day of its IPO.

In December 2021, Mingyue Lens listed on the ChiNext board of the A-share market, with its stock price surging 134% on the first day of trading and its market capitalization reaching nearly RMB 10 billion.

"Positive sentiment in the secondary market has spilled over into the primary market, leading to increasingly frequent investment and financing activities in the ophthalmology sector."The emergence of a cohort of innovative enterprises, coupled with capital infusion, has ignited intense activity across the ophthalmic pharmaceutical and medical device sector; however, it is crucial to acknowledge that we still face a substantial gap compared to global industry giants.“Luo Xi stated that, taking the R&D and manufacturing of ophthalmic medical devices as an example, this niche sector is a typical track characterized by ‘easy entry but difficult mastery’ and ‘low barriers at the low end but high barriers at the high end.’ Domestic enterprises are generally in a relatively weak position in terms of technical strength and industrial experience.”

Therefore,From the perspective of corporate development, ophthalmic pharmaceutical and medical device companies should identify a precise positioning and area of expertise to pursue in-depth technological advancement.

For instance, High Vision Medical, which is sprinting toward an IPO, is transforming its business model. According to its prospectus, the company’s product portfolio consists of distributed products and proprietary products, with distributed products (i.e., agency products) accounting for the majority. In other words, High Vision Medical operates more as a medical device intermediary, with its core revenue derived from price differentials; therefore, suppliers play a crucial role in its business model.

To reduce its reliance on suppliers, Gaoshi Medical has intensified its efforts in technological R&D in recent years, actively developing new proprietary products that cover its main ophthalmic product lines. According to the prospectus, total R&D expenditures from 2018 to 2020 were RMB 2.4 million, RMB 2.7 million, and RMB 3.1 million, respectively; for the first half of 2020 and the first half of 2021, they amounted to RMB 1.5 million and RMB 9.4 million, respectively. It is evident that Gaoshi Medical’s R&D spending surged significantly in 2021, reaching more than five times the level of the same period in the previous year. Nevertheless, Gaoshi Medical’s R&D expenditure remains low compared with similar companies abroad. To achieve profitability through its proprietary products, Gaoshi Medical may need to sustain long-term investment.

In assessing trends, Luo Xi believes that,In the field of ophthalmic devices, there are still opportunities for domestic substitution of implantable products, primarily intraocular lenses. Independent research and development of high-end ophthalmic medical equipment and core optoelectronic components will be the investment trend in the medium to long term. Investment in the ophthalmic pharmaceutical sector will focus on two niche segments: drug delivery systems and gene therapy.。

The emergence of this favorable trend has led to a surge in innovative ophthalmic enterprises, which are bound to join the global market competition and engage in direct “confrontation” with international giants.

Therefore, during this current phase of accelerated growth, ophthalmic innovation enterprises must solidify their foundations and master core competencies, thereby positioning themselves for explosive growth in the foreseeable future. This will not only benefit billions of patients with eye diseases but also generate greater incremental value for the industry.