Domestic Players Break Through in China's Ophthalmic Equipment Market, Where Imports Hold Over 90% Share

After experiencing a significant surge in financing deals in 2018, followed by a downturn in 2019 and 2020, the ophthalmology market is now undoubtedly advancing at an accelerated pace.

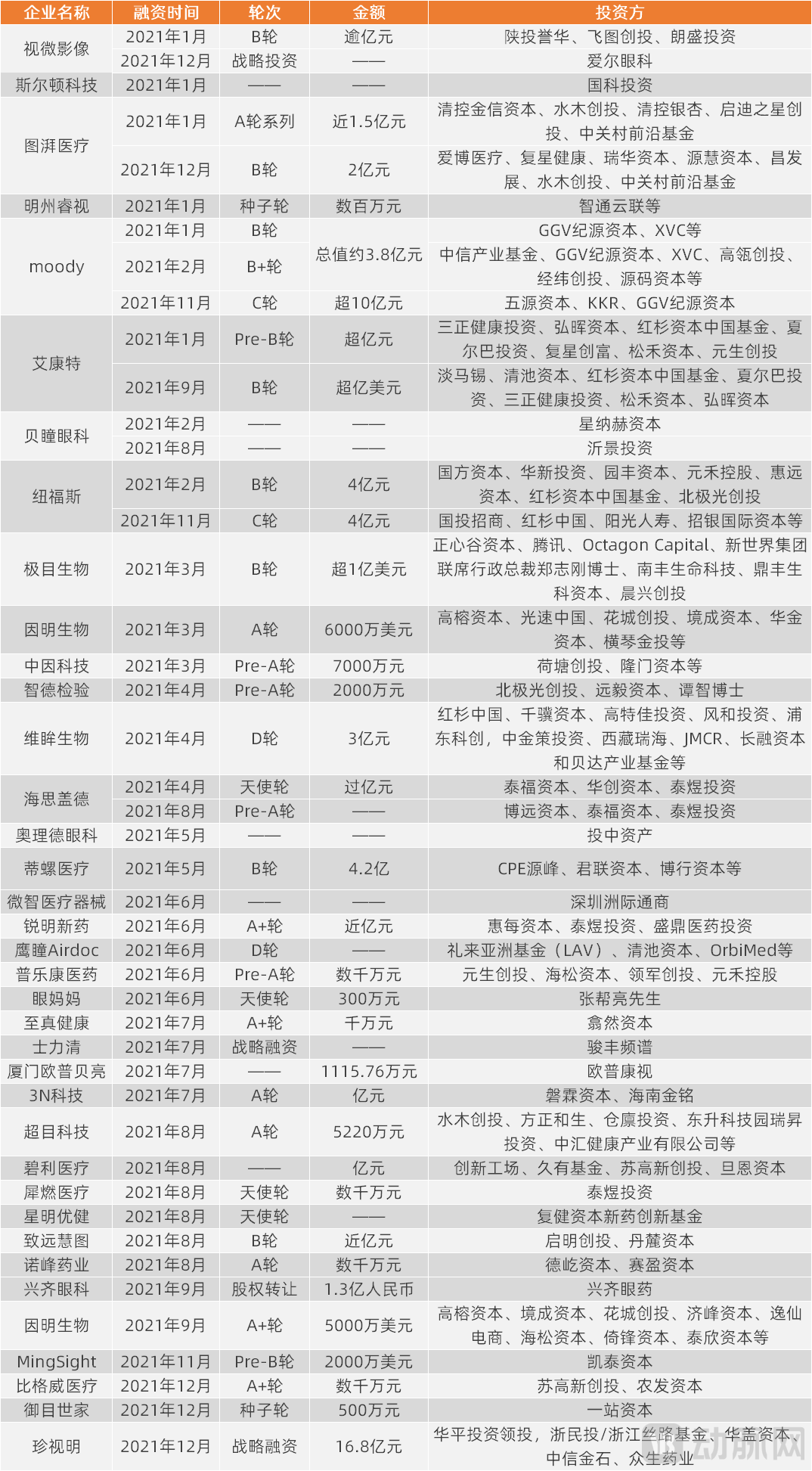

Taking the financing events in the ophthalmology market in 2021 as an example, according to incomplete statistics from VCBeat, a total of 37 companies in the ophthalmology industry secured funding in the primary market in 2021, involving 45 financing deals. This represents a significant doubling compared to the 17 financing deals recorded in 2020.

The influx of capital also reflects the market’s optimism toward ophthalmology. Ophthalmic diseases affect a vast patient population; for instance, according to the White Paper on Eye Health in China released by the National Health Commission, the overall prevalence of myopia among children and adolescents in China is 53.6%, while the rate among college students exceeds 90%.

In recent years, driven by factors such as the deepening aging of China’s population and changes in lifestyle, the prevalence of ophthalmic diseases including cataracts, glaucoma, and dry eye syndrome has been rising year by year. According to data from Menet, the number of cataract surgeries in China increased from 1.116 million in 2012 to 3.323 million in 2020, with the Cataract Surgical Rate (CSR) reaching 2,357 per million population in 2020.

In the treatment of ophthalmic diseases, since most conditions cannot be cured with medication alone and drugs typically only serve to slow disease progression, some patients prefer surgical interventions for definitive treatment. Furthermore, given the anatomical complexity of the eye, ophthalmic surgeries are highly dependent on specialized instruments; thus, ophthalmic devices play a more critical role than ophthalmic pharmaceuticals.

At present, ophthalmic medical devices primarily cover two major fields: ocular surgery and vision care. Within ocular surgery, medical equipment and medical consumables constitute key components. However, compared with medical consumables, the ophthalmic equipment market has historically maintained a relatively low profile. For instance, among the Class III ophthalmic devices approved for domestic use in China in 2021, all 34 approved products were either medical consumables or vision care products, while the number of approved ophthalmic equipment devices was zero.

However, in clinical practice, ophthalmology is among the medical specialties most heavily reliant on instruments and equipment, due to the wide variety of ocular diseases and the intricate complexity of eye anatomy. Nevertheless, the historical development of China’s ophthalmic medical device market has been less than satisfactory, constrained by high technological barriers to advanced equipment and the underdeveloped nature of lower-tier markets.

Given the current high level of attention in the ophthalmology market, what changes have occurred in the ophthalmic equipment market? What future trends are emerging?

Frequent Large-Scale Financing Rounds: What Is the Market Potential for Ophthalmic Equipment?

Early this year, the National Health Commission issued the “14th Five-Year Plan” for National Eye Health (2021–2025), drawing public attention to the development of eye health services.

Moreover, a recent assessment in the “Global Eye Health Report” published by The Lancet Global Health indicates that addressing preventable vision loss could generate $411 billion (approximately RMB 2.6248 trillion) in annual global economic benefits. This underscores the significant potential of the ophthalmology market.

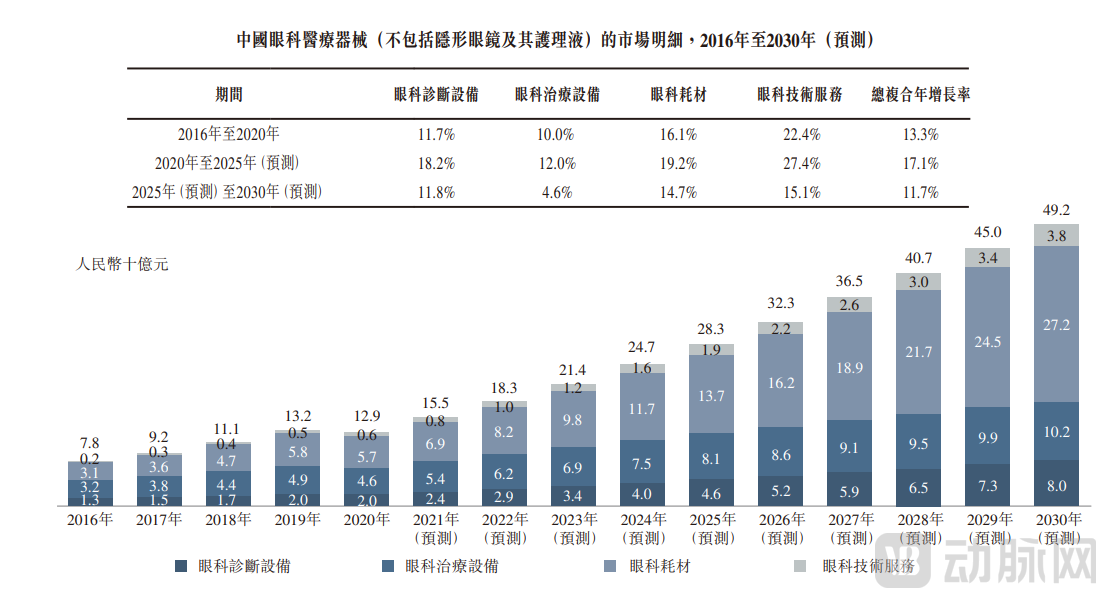

In fact, driven by a continuously growing population base and advancements in surgery-related technologies, the market size of ophthalmic devices in China increased from RMB 7.8 billion in 2016 to RMB 12.9 billion in 2020, representing a compound annual growth rate (CAGR) of 13.3%, which outpaced the growth rate of the global medical device market.

China’s Ophthalmic Medical Device Market (Image Source: Gaoshi Medical Prospectus)

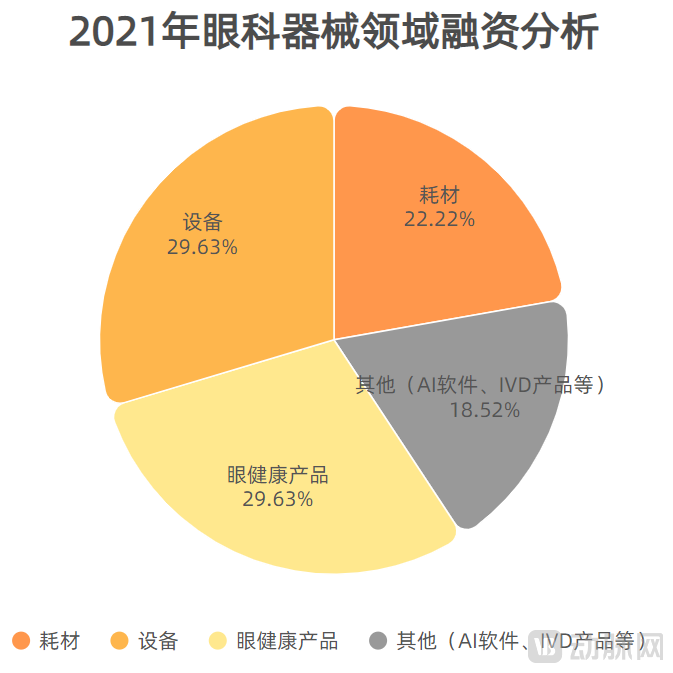

In terms of capital market performance, an analysis of ophthalmology sector financing in 2021 reveals that ophthalmic devices were undoubtedly the most frequently funded segment, with a total of 23 financing events. Among these, companies in the ophthalmic equipment and eye health products categories accounted for the majority of deals, while those in the consumables segment followed closely behind.

From the perspective of capital market performance, the ophthalmic equipment market is no weaker than the ophthalmic consumables market. Compared with 2020, the number of financing events in the ophthalmic equipment market is almost comparable to that in the ophthalmic device sector. Notably, Topcon Medical (Tupai Medical) and Vision Micro Imaging each secured two rounds of financing consecutively in 2021, with each round exceeding RMB 100 million.

Founded in Silicon Valley, USA, in 2014, Perfect Imaging primarily focuses on the field of high-end ophthalmic equipment. It is reported that the company’s first swept-source OCT, approved in 2019, outperforms imported counterparts in scanning speed, penetration power, imaging depth, imaging range, and blood flow algorithms. Furthermore, Perfect Imaging has also established a presence in the research and development of high-end ophthalmic devices for anterior segment disorders, cataracts, and refractive diseases.

Tupu Medical was established in October 2017, originating from the commercialization of technological achievements from the Department of Electronic Engineering at Tsinghua University. Its core team comprises more than ten Tsinghua University alumni and senior executives from globally renowned high-end manufacturing enterprises. The company was jointly incubated by the Beijing Tsinghua Industrial R&D Institute, the Global Health Industry Innovation Center (GHIC), and the Zhongguancun Life Science Park. Since its inception, Tupu Medical has been dedicated to the independent research, development, and manufacturing of a full range of high-end ophthalmic medical equipment and core optoelectronic components. At present, it has multiple product lines, including ultra-high-speed swept-source OCT for ophthalmology, swept-source optical biometers, and OCT endoscopes, achieving domestic breakthroughs in several fields.

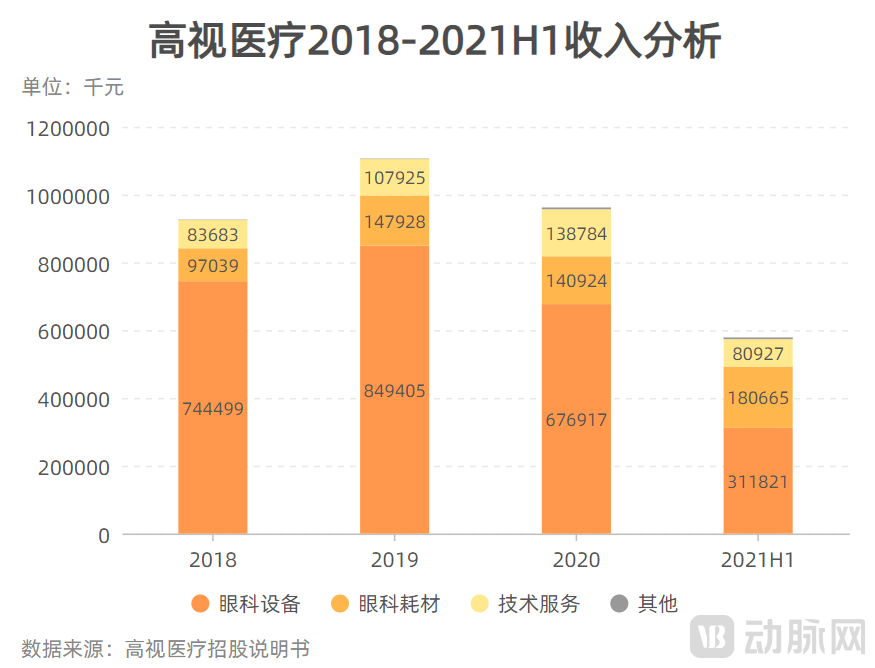

In addition to the frequent financing events, Gaoshi Medical, China’s third-largest ophthalmic medical device manufacturer, officially filed its prospectus with the Hong Kong Stock Exchange last November. According to the prospectus, ophthalmic medical equipment has been Gaoshi Medical’s primary source of revenue from 2018 to the first half of 2021.

Meanwhile, as can be seen from the chart above, the proportion of revenue derived from ophthalmic consumables has been increasing year by year, with a significant surge recorded in the first half of 2021 (1H 2021). This growth was, to some extent, driven by High Vision Medical’s acquisitions of Taijing and Roland.

However, at the current stage, the improvement in Gaoshi Medical’s gross profit margin (which stood at 40.9%, 41.9%, 45.3%, and 46.6% respectively from 2018 to 2020 and in the first half of 2021) is primarily driven by the increase in the gross profit margin of ophthalmic medical equipment sales (39.6%, 39.7%, 43.4%, and 44.9% respectively), while the gross profit margin of ophthalmic medical consumables has been fluctuating (50.7%, 52.5%, 51.8%, and 51.0% respectively). This also demonstrates to the external market the potential of ophthalmic equipment.

Within the field, participants continue to explore; outside the field, an increasing number of companies are gradually revealing their strategic layouts in the ophthalmology sector.

In March last year, MicroPort Vision received RMB 385 million in investment from MicroPort Investment, Wangdaotong Biotechnology, and other enterprises, further strengthening MicroPort Medical’s strategic layout in ophthalmology.

It is understood that MicroPort Vision was established in July 2020, with its core business focused on the research and development, manufacturing, and sales of ophthalmic medical products for diagnosis, treatment, and care. According to published patent information, MicroPort Vision currently holds multiple patents covering devices such as phacoemulsification systems, ultrasonic transducers, and intraocular lenses. From this perspective, MicroPort Vision clearly places greater emphasis on the research and development of ophthalmic equipment.

It is evident that, in terms of actual market performance, the ophthalmic equipment market is no less competitive than the ophthalmic medical consumables market. Moreover, both investors and entrepreneurs continue to increase their investments and efforts in this field. So, what challenges does this thriving sector face?

The Market Blocked by Imported Brands

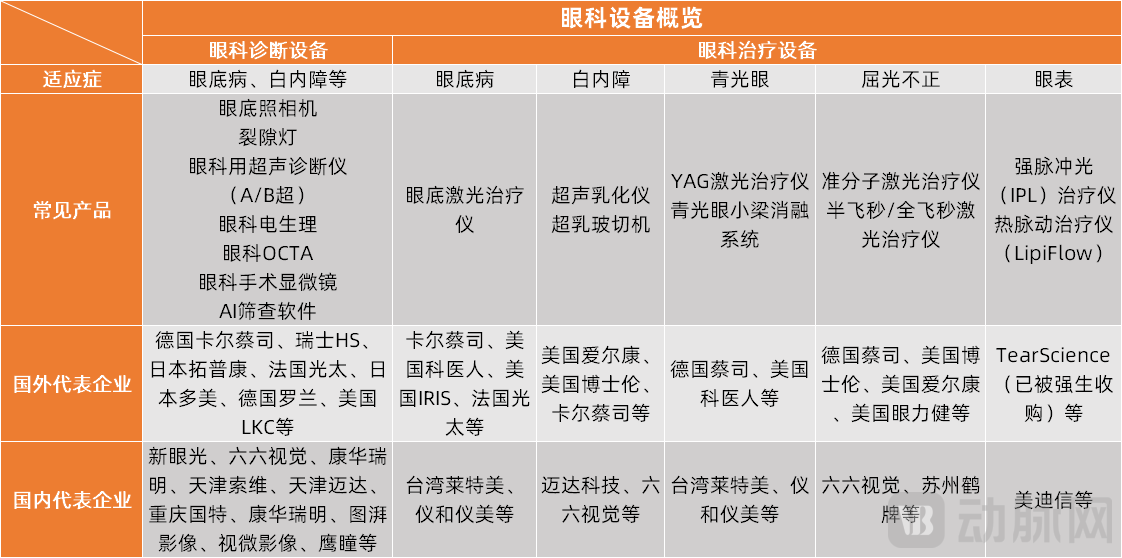

Generally, ophthalmic equipment typically includes ophthalmic diagnostic devices and ophthalmic therapeutic devices. Clinically, ophthalmology can be divided into seven major subspecialties: fundus diseases, cataracts, glaucoma, refractive errors, ocular surface diseases, and pediatric ophthalmology. Diagnosis and treatment within each subspecialty usually require medical devices, consumables, or both.

Given the wide variety of ophthalmic diseases, the diagnostic and therapeutic equipment involved is equally diverse. The number of domestic brands across various segments is also considerable, suggesting that the market landscape for these Chinese-made brands is not as challenging as it may appear.

In reality, ophthalmic equipment, particularly mid-to-high-end medical devices, has long been monopolized by imported brands due to high technical barriers. Meanwhile, challenges such as talent shortages and limited market penetration have also hindered the development of the mid-to-high-end ophthalmic equipment market. Specifically, the domestic ophthalmic medical equipment industry in China currently faces the following key issues.

First, there are extremely high technical barriers. Most domestic companies still lack capabilities in core areas of high-end ophthalmic equipment, such as algorithms, systems, optical software, and manufacturing processes. These formidable technical barriers not only make it exceedingly difficult for domestic enterprises to develop equipment but also result in a very high rate of import monopoly.

It is understood that the major causes of blindness in China have shifted from infectious eye diseases to conditions such as cataracts, myopic retinopathy, glaucoma, corneal diseases, and diabetic retinopathy. Among these, millions of cataract surgeries are performed annually. However, in clinical practice, most diagnostic and therapeutic equipment for common ophthalmic conditions like cataracts, glaucoma, and myopia relies on imports. For instance, A/B-scan ultrasound devices used for imaging and diagnosing ocular structural lesions, and femtosecond laser systems for refractive surgery, are predominantly supplied by imported brands such as Zeiss, Alcon, and Topcon.

Among the 18 imported Class III ophthalmic devices approved in 2021, five were high-end ophthalmic equipment such as femtosecond laser surgical systems and ultrasound diagnostic systems. This figure differs significantly from the number of ophthalmic devices among domestically approved Class III ophthalmic devices, reflecting to some extent China’s current reliance on imported brands for high-end ophthalmic equipment.

In terms of specific market share data, imported ophthalmic equipment suppliers accounted for a staggering 98% of the market by sales revenue. Even by sales volume, this proportion reached 95%. Furthermore, according to data from the General Administration of Customs of China, China’s trade deficit in ophthalmic optical instruments exceeded US$620 million in 2020, indicating substantial potential for domestic substitution.

Second, the lower-tier market remains untapped. Not only are most mid-to-high-end devices concentrated in hospitals at Level II and above, but imported products also dominate the market share for essential small-scale ophthalmic medical equipment in most hospitals. This indicates significant room for downward expansion in terms of both user base and product penetration.

Thirdly, in public perception, the market potential and purchasing power associated with medical equipment are considered weaker than those of ophthalmic medical consumables, resulting in relatively low attention to the ophthalmic equipment market. However, according to the prospectus of Gaoshi Medical, the market size generated by ophthalmic equipment has exceeded that of ophthalmic consumables in both the global and Chinese ophthalmic medical device markets in recent years, with an overall upward trend.

For the aforementioned reasons, although the lagging development of China’s ophthalmic equipment market is evident and widely recognized, this issue has proven difficult to resolve rapidly. In light of this reality, what exploratory measures can the industry undertake?

Learning from Global Best Practices to Identify Opportunities in China

Based on the preceding analysis, it is evident that import monopoly remains a significant challenge facing the ophthalmic equipment industry. However, by analyzing the strategic layouts of leading global enterprises in this sector, we may identify potential opportunities for the development of domestic companies.

In the field of ophthalmic equipment, Germany’s Carl Zeiss is an indispensable name. Its VisuMax femtosecond laser system is currently the only platform worldwide capable of performing “SMILE” (Small Incision Lenticule Extraction) all-femtosecond laser vision correction surgery, thereby establishing a monopoly in this sector. Data show that as of June 2021, more than 2.8 million SMILE procedures had been performed in China alone.

In fact, Carl Zeiss is not a company specializing solely in medical technology. It is understood that the Carl Zeiss Group comprises four business segments: Semiconductor Manufacturing Technology, Research and Quality Technology, Medical Technology, and Consumer Optics (including Vision Care). When Carl Zeiss was founded in 1846, it primarily manufactured precision instruments such as microscopes.

Not until 1911, when Carl Zeiss collaborated with a Swedish physician to develop a slit lamp, did the company lay the foundation for its entry into the medical sector, thereby paving the way for its subsequent focus on ophthalmology.

In 2002, after recognizing the immense potential of the ophthalmic market, Carl Zeiss established Carl Zeiss Meditec AG, which provides comprehensive diagnostic and therapeutic solutions for ophthalmic diseases. In the subsequent business development, to continuously supplement and strengthen its capabilities in the field of ophthalmology, Carl Zeiss Meditec gradually grew into a leading enterprise in the ophthalmic sector through a series of acquisitions and external collaborations.

Key Milestones in the Development of Carl Zeiss Meditec

For decades, Carl Zeiss has rapidly expanded its portfolio of ophthalmic solutions through acquisitions and external collaborations. Coupled with the company’s longstanding emphasis since its inception on innovation in optics, precision instruments, and microsurgical equipment, this strategy has laid a solid technological foundation for Carl Zeiss Meditec’s subsequent growth in the field of ophthalmology.

Throughout its development, Carl Zeiss Meditec has also placed significant emphasis on broad sector coverage, expanding into the intraocular lens business through acquisitions and thereby strengthening its capacity for scaled growth.

Furthermore, from a market perspective, its international footprint has been a key factor in Carl Zeiss Meditec’s current success. According to the company’s revenue data for the 2020/2021 fiscal year, more than 70% of Carl Zeiss Meditec’s income was derived from operations in the Americas and the Asia-Pacific region. It is fair to say that Carl Zeiss Meditec’s global reputation is attributable not only to its foundational technological expertise but also significantly to its international strategy.

Turning our attention back to domestic companies, Tupai Medical and VisionTek Imaging, both of which secured two consecutive rounds of financing last year, initially entered the ophthalmic equipment market with their self-developed optical coherence tomography (OCT) devices and have since gradually expanded their product portfolios across multiple ophthalmology subspecialties. Meanwhile, each company has established a global business division and an overseas operations and R&D center to strategically position themselves in international markets.

ChaoMu Technology, which also secured financing last year, has made the treatment of nystagmus its initial market entry point. While achieving significant breakthroughs in this area, the company is also expanding into the fields of glaucoma and myopia, continuously broadening its scope of coverage.

It is evident that although domestic and international enterprises face different market environments and have distinct strategic priorities, most have opted for multi-sector coverage and global expansion in their market strategies. This approach aims to enhance their service capabilities and scope, thereby driving scalable growth for the enterprises.

Where Are We Headed?

Currently, the ophthalmology sector continues to gain momentum in the primary market. Correspondingly, the previously “under-the-radar” field of ophthalmic equipment is receiving increasing attention from investors, with some companies embarking on initiatives to break import dependence and expand into overseas markets.

In terms of the market, lower-tier markets will become a significant source of incremental growth for the ophthalmic equipment industry. The "14th Five-Year Plan for National Eye Health in China (2021–2025)" proposes deepening paired assistance from tertiary hospitals to county-level hospitals, continuously carrying out initiatives such as the "Guangming Project" and "Guangming Xing," promoting the decentralization of cataract sight-restoration surgical techniques, and enhancing the capacity of county-level hospitals to perform cataract sight-restoration surgeries. By the end of the 14th Five-Year Plan period, more than 90% of county-level hospitals that meet the recommended standards for comprehensive service capabilities will perform cataract sight-restoration surgeries, and the national cataract surgery rate per million population will exceed 3,500.

Therefore, under the guidance of relevant policies, more ophthalmic surgeries will become widespread in lower-tier markets, and correspondingly, medical institutions’ demand for ophthalmic medical equipment will continue to grow. As a result, the future growth market for the ophthalmic equipment industry will be primarily concentrated in lower-tier markets.

Furthermore, scaling up will also become a development direction for some enterprises. For a long time, China’s ophthalmic equipment industry has been characterized by fragmentation and small-scale operations. However, some domestic companies with core technological barriers are now leveraging their technical advantages to continuously expand their market share and deploy multi-product line coverage. This strategy is gradually enabling them to achieve economies of scale and accelerating the process of import substitution with domestically produced alternatives.

Amid the trends of an expanding market and rising attention, industry players must hone their internal capabilities and establish genuine core technological barriers to seize opportunities and realize their value.