Lepu Biopharma Debuts on HKEX as Pharma Stocks Emerge from the 'Winter'

LEPU BIOPHARMA

Innovative Oncology Treatment Product Developer

Last year, pharmaceutical stocks generally fell below their IPO prices, and retail investors’ sentiment toward subscribing to new listings remained subdued.

However, it is precisely after the past year’s correction of the overall high valuations in the pharmaceutical sector that the sector has now pulled back to a mid-range level. According to data from a research report by Industrial Securities, the current valuation of the pharmaceutical sector stands at approximately 32 times earnings, with its investment value becoming evident; consequently, many public mutual funds have begun to gradually allocate assets to the pharmaceutical sector.

Today, LEPU BIOPHARMA (abbreviated as LEPU BIOPHARMA-B, SEHK: 02157), a domestic pioneer in ADCs, officially listed on the Hong Kong Stock Exchange. After the opening, its share price held firm at the issue price, experiencing only a slight decline.

Perhaps the “winter” for pharmaceutical stocks has passed, and “spring” is on the horizon.

LEPU BIOPHARMA, which went public today, was formerly a subsidiary of Lepu Medical. The founder of both companies is Pu Zhongjie. In early 2017, Pu Zhongjie, the founder and controlling shareholder of Lepu Medical, together with Su Rongyu, decided to establish a biopharmaceutical company focused on cancer treatment. Consequently, LEPU BIOPHARMA was registered and established in 2018. Since its inception, LEPU BIOPHARMA has completed six rounds of financing, with investors including Vivo Capital, Yipu Capital, Ronghui Capital, Ping An Capital, Sunshine Insurance Group, SDIC Chuanghe, Haitong Innovation Capital, CDB Kaiyuan, Shiyu Capital, and Sumec Investment, among others.

In 1990, Pu Zhongjie embarked on the research and development of coronary stents as a visiting scholar at the University of Florida in the United States. In 1998, he established WP Medical Technologies, Inc., a medical technology company registered in the U.S., with his wife, Zhang Yue’e, as the sole shareholder. Notably, Zhang Yue’e and Pu Zhongjie both completed their undergraduate studies at Xi’an Jiaotong University, making them a true power couple of academic excellence and ideal entrepreneurial partners.

At a time when both scientific research and its commercialization were progressing smoothly, the couple Pu Zhongjie and Zhang Yue’er resolutely returned to China with their technology to embark on an entrepreneurial venture, founding Lepu Medical in 1999. Lepu Medical developed China’s first batch of cardiac stents, pacemakers, and other products, filling the then-empty domestic market for coronary artery stents.

Leveraging its first-mover advantage and cutting-edge technology, Lepu Medical successfully listed on the ChiNext board in 2009. At that time, the couple Pu Zhongjie and Zhang Yue’er jointly held approximately 91.43 million shares, with a market value of nearly RMB 5.8 billion, propelling them to become the wealthiest individuals on the ChiNext board.

After achieving financial independence, Pu Zhongjie became increasingly low-profile, even becoming the lowest-paid CEO among global medical device companies at one point: his annual salary was RMB 88,400 in 2014, RMB 98,400 in 2015, and RMB 106,800 in 2016; in 2019, Pu Zhongjie’s annual salary was even zero.

LEPU BIOPHARMA is the third pillar of Pu Zhongjie’s business empire, following the public listings of Lepu Medical and Lepu Diagnostics, embodying his vision for the development of China’s biopharmaceutical industry.

LEPU BIOPHARMA’s IPO offer price was HK$7.13 per share, with a total of 127 million shares issued. After deducting underwriting fees and other estimated expenses related to the global offering, LEPU BIOPHARMA will receive net proceeds of approximately HK$804.2 million from the global offering.

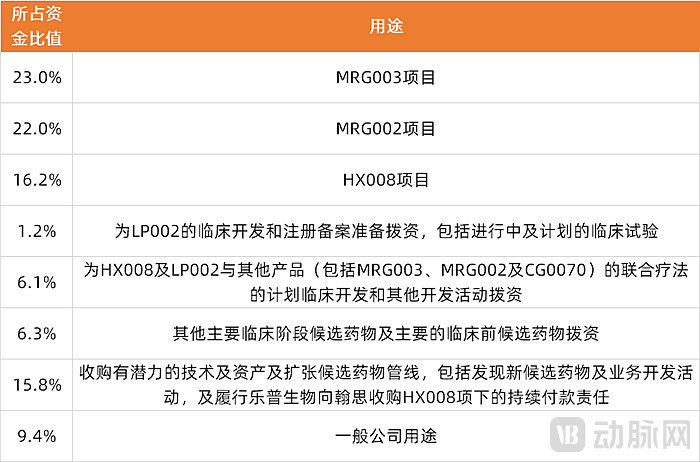

According to the prospectus, 68.5% of the proceeds from this IPO will be used for the research and development and production of core products (including MRG003, MRG002, HX008, and LP002), 15.8% will be used to acquire promising technologies and assets and expand LEPU BIOPHARMA’s drug candidate pipeline, and the remaining funds will be allocated to other clinical-stage products, research and development of preclinical-stage products, and general corporate purposes.

Use of Proceeds, Compiled from Prospectus Information

Although this listing will bring certain cash flow to LEPU BIOPHARMA, which is conducive to the company's operational development. However, according to the prospectus, LEPU BIOPHARMA's current cash balance (including cash and cash equivalents as well as time deposits with an initial term of three months) will only be able to maintain the company's financial viability for 4.9 months; if the funds raised from this listing are added (based on the lower end of the indicative offering price), it would be 14.7 months.

It is reported that LEPU BIOPHARMA has not yet generated any sales revenue from its products and has incurred continuous losses since its establishment. For the years 2019 and 2020, as well as for the eight months ended August 31, 2021, LEPU BIOPHARMA’s operating losses amounted to RMB 454.7 million, RMB 520.4 million, and RMB 662.2 million, respectively, with cumulative losses totaling RMB 1.6373 billion in less than three years.

Consequently, some negative sentiments have emerged. LEPU BIOPHARMA’s fastest-growing PD-1/PD-L1 product already operates in a highly competitive “red ocean” market in China, casting significant uncertainty on the future cash flows it will generate for the company. Although LEPU BIOPHARMA has established a comprehensive pipeline of antibody-drug conjugates (ADCs), all candidates are currently in Phase II clinical trials, meaning their path to commercialization remains considerably distant.

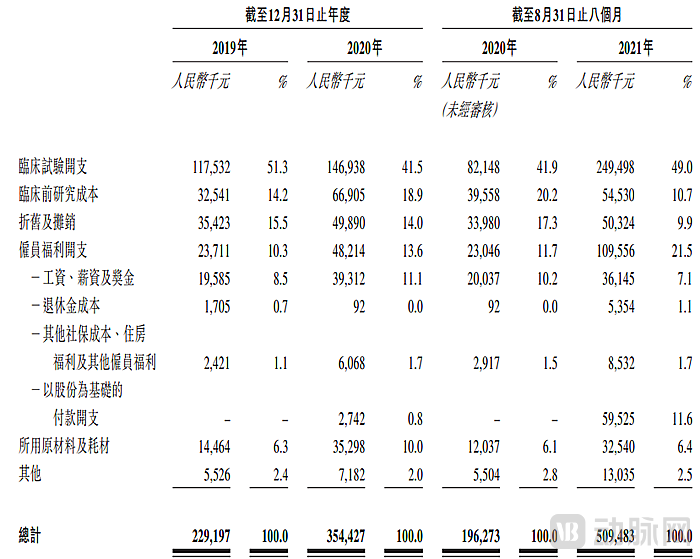

LEPU BIOPHARMA’s expenditures are heavily concentrated in research and development (R&D). In the first eight months of 2021 alone, the company’s R&D spending exceeded RMB 500 million. Among this amount, share-based payment expenses accounted for a small proportion, totaling less than RMB 60 million. The bulk of the funds was allocated to clinical trials, preclinical studies, and employee salaries. Currently, LEPU BIOPHARMA is in a critical pre-launch phase for its products, making it impossible to reduce the scale of its hard R&D expenditures. Therefore, even though the company’s cash flow has reached a critically precarious state, it cannot achieve cost savings internally (“cutting costs”) and must instead seek external revenue sources (“opening up new funding channels”).

Breakdown of LEPU BIOPHARMA’s R&D Expenditures

Therefore, LEPU BIOPHARMA’s listing has secured the company a one-year buffer period. How will LEPU BIOPHARMA address its cash crunch after going public? Based on the company’s prospectus, VCBeat New Medicine has identified three strategies for LEPU BIOPHARMA to resolve its financial predicament in the future.

LEPU BIOPHARMA is rapidly expanding its new product pipeline through a strategy of acquisitions and partnerships.

In its year of establishment, LEPU BIOPHARMA acquired controlling interests in Taizhou Hanzhong and Taizhou Aoke, thereby obtaining the anti-PD-1 antibody candidate HX008 and the anti-PD-L1 antibody candidate LP002. In the same year, LEPU BIOPHARMA acquired a controlling interest in Shanghai Meiyake, which possesses an ADC platform, securing global rights to its current ADC candidates MRG003, MRG002, and MRG001, and independently developed the ADC candidate MRG004A using this platform.

Building on the acquisition of Shanghai Meiyake, LEPU BIOPHARMA has also established collaborations with Fudan University and the Shanghai Institute of Materia Medica, Chinese Academy of Sciences: In June 2018, Shanghai Meiyake entered into a technology development agreement with Fudan University and the Shanghai Institute of Materia Medica, Chinese Academy of Sciences, for the development of a new antibody-drug conjugate (TF-ADC).

According to the agreement between Fudan University and the Shanghai Institute of Materia Medica, Chinese Academy of Sciences (SIMM, CAS), Fudan University and SIMM, CAS have granted Shanghai Meiyake an exclusive right to use the technologies, patents, and know-how related to TF-ADC developed by Fudan University and SIMM, CAS (“TF-ADC Technology”) for the development, manufacturing, and commercialization of TF-ADC in China. The exclusive license term shall last for the entire duration of the contract. MRG004A is a related candidate drug developed based on this technology.

In addition to acquiring antibody drugs and conjugated drugs, LEPU BIOPHARMA has also introduced oncolytic virus products through collaborations.In March 2019, LEPU BIOPHARMA licensed in the oncolytic virus product CG0070 from CG Oncology, Inc., along with the rights to develop, manufacture, and commercialize CG0070 in China. Furthermore, LEPU BIOPHARMA holds global development and commercialization rights for CG0070 clinical and preclinical stage candidates, as well as for candidate drugs jointly developed through joint ventures.

During the early phase of expanding its commercial footprint, LEPU BIOPHARMA undoubtedly invested heavily in acquiring in-licensed pipelines. However, the biopharmaceutical industry is often characterized by the “Double Ten” rule—development cycles exceeding ten years and R&D costs surpassing US$1 billion. In the absence of successfully commercialized products, biopharma companies frequently operate at a continuous loss. Amid current funding constraints, can these in-licensed projects of LEPU BIOPHARMA be out-licensed to generate the revenue needed to sustain further R&D? There is no shortage of individual cases demonstrating this possibility.

In August last year, RemeGen Co., Ltd. entered into a collaboration deal worth up to $2.6 billion with Seattle Genetics, granting the latter development and commercialization rights for RemeGen’s ADC novel drug, disitamab vedotin, in most overseas markets. Under the agreement, RemeGen will also receive tiered sales royalties ranging from high single digits to the low teens percent of net sales of disitamab vedotin in Seattle Genetics’ territories.

In January last year, BeiGene and Novartis entered into a collaboration and license agreement for the development, manufacturing, and commercialization of tislelizumab in multiple countries, with a total transaction value exceeding $2.2 billion. In addition, Junshi Biosciences, Innovent Biologics, I-Mab, CStone Pharmaceuticals, Nocturne Bio (InnoCare Pharma), Yuheng Pharmaceutical, and Allist have all completed high-value license-out deals in recent years.

LEPU BIOPHARMA holds global commercialization rights for MRG003, an EGFR-targeting ADC; MRG002, a HER2-targeting ADC; and HX008, a PD-1 monoclonal antibody, all of which are currently under active development. Amid the prevailing trend of Chinese innovative drugs going global, licensing out overseas rights to select pipeline assets represents a viable strategy for LEPU BIOPHARMA to rapidly bolster its capital reserves.

In addition to license-out deals, LEPU BIOPHARMA’s existing anti-PD-1/PD-L1 drugs can directly generate cash flow for the company. Let us examine just how substantial this “cash flow” could be.

Currently, LEPU BIOPHARMA’s product pipeline comprises eight clinical-stage candidate drugs, three preclinical candidate drugs, and combination therapies involving three clinical-stage candidate drugs. Of the eight clinical-stage candidates, five are targeted therapies and three are immunotherapies; among the latter, two are immune checkpoint inhibitors and one is an oncolytic virus. According to the prospectus, LEPU BIOPHARMA has initiated 28 clinical trials, three of which have entered registrational trial stages, with two being conducted in the United States.

In June 2021, LEPU BIOPHARMA submitted a New Drug Application (NDA) to the National Medical Products Administration (NMPA) for HX008 in the treatment of melanoma. In October 2021, the company submitted another NDA for HX008 for the treatment of MSI-H/dMMR (microsatellite instability-high/mismatch repair deficient) solid tumors, which was granted priority review status. With two indications having reached the NDA stage, the commercialization of HX008 is imminent.

Compared with all competing anti-PD-1 antibodies that have been marketed or entered Phase III clinical trials, the Fc region of HX008 can significantly extend the protein half-life to 17.15–23.51 days (single dose) and 18.41–38.16 days (steady-state dose), thereby reducing treatment frequency, improving patient compliance, and enhancing patient convenience and accessibility. The favorable efficacy demonstrated by HX008 in treating MSI-H/dMMR solid tumors across multiple indications facilitates the establishment of sales and marketing channels in key hospital departments, including gastroenterology, gynecology, urology, respiratory medicine, and dermatology.

To further expand the indications for HX008, LEPU BIOPHARMA has completed patient enrollment as of now. The company is currently in the follow-up phase of the Phase Ib clinical trial of HX008 for advanced solid tumors, as well as the Phase II clinical trials for non-small cell lung cancer (NSCLC), first- and second-line gastric cancer, triple-negative breast cancer (TNBC), and hepatocellular carcinoma (HCC). Additionally, the Phase II clinical trial for non-muscle-invasive bladder cancer (NMIBC) has been initiated, and the Phase III clinical trial for second-line gastric cancer is underway.

However, HX008 must contend with intense competition from other anti-PD-1 drugs on the market.

In China, the market size for anti-PD-1/anti-PD-L1 antibody therapies continues to grow. According to Frost & Sullivan, the market size for anti-PD-1/anti-PD-L1 antibody therapies in China was RMB 13.7 billion in 2020 and is projected to reach RMB 51.9 billion in 2025 and RMB 58.2 billion in 2030, representing a compound annual growth rate (CAGR) of 30.5% from 2020 to 2025 and 2.3% from 2025 to 2030. Anti-PD-1/anti-PD-L1 antibody therapies target multiple indications, including melanoma, MSI-H/dMMR solid tumors, gastric cancer, and non-small cell lung cancer (NSCLC).

It is evident that HX008 holds immense potential to meet the vast and growing market demand, making it the most promising candidate in LEPU BIOPHARMA’s current pipeline to serve as a cornerstone of cash flow.

In addition to its anti-PD-1 drug, a key cash-flow generator, LEPU BIOPHARMA is making simultaneous strides with innovative products such as antibody-drug conjugates (ADCs) and oncolytic viruses, which are poised to yield significant results in the future.

As a clinically advanced EGFR-targeted antibody-drug conjugate (ADC) in China, MRG003 is well-positioned to capture first-mover advantage, given that no EGFR-targeted ADC has yet been approved in the Chinese market. In 2019, MRG003 was recognized under China’s National Science and Technology Major Project for “Major New Drug Development.”

EGFR is a relatively broad-spectrum tumor antigen that is overexpressed in a variety of human tumors. The NSCLC market size in China alone was RMB 42.3 billion in 2020, and is projected to reach RMB 111.7 billion by 2025 and RMB 177.5 billion by 2030. MRG003 has the potential to overcome various types of acquired resistance, such as resistance to EGFR-TKIs caused by mechanisms including EGFR mutations or other mutations in key proteins downstream of the EGFR signaling cascade, thereby providing a new treatment option for the large population of EGFR-positive patients.

Another core ADC product is MRG002, an innovative HER2-targeted ADC.HER2 is a molecular target that is abnormally overexpressed in many cancer types, including breast cancer, gastroesophageal junction cancer, and gastric cancer.

As of September 2021, preclinical studies and preliminary clinical evidence have demonstrated the advantages of MRG002 over competitive HER2-targeted antibody-drug conjugates (ADCs) in terms of safety, efficacy, and pharmacokinetics. As one of the first HER2-targeted ADCs to enter clinical development in China, MRG002 features a unique design and innovative modifications to trastuzumab, enhancing patient safety and tolerability while maintaining robust antitumor efficacy.

LEPU BIOPHARMA has currently initiated a Phase II trial of MRG002 for HER2-overexpressing and HER2-low-expressing breast cancer. For the use of MRG002 in HER2-overexpressing breast cancer, LEPU BIOPHARMA has completed patient enrollment and is currently in the follow-up period. The company has obtained approval from the National Medical Products Administration (NMPA) for a registrational trial in HER2-overexpressing breast cancer. In addition, LEPU BIOPHARMA launched Phase II exploratory clinical trials in China for advanced urothelial carcinoma and biliary tract cancer with HER2 expression in April and June 2021, respectively.

In addition, in November last year, LEPU BIOPHARMA also obtained IND approval for CG0070 from the National Medical Products Administration.CG0070 is an oncolytic adenovirus in clinical development for the treatment of bladder cancer, currently leading in terms of progress., plans to conduct Phase I bridging clinical studies in patients with NMIBC and solid tumors this year. CG Oncology has completed its Phase II clinical trial of BCG-unresponsive NMIBC in the United States, and LEPU BIOPHARMA will accelerate clinical development and commercialization in China on this basis. In addition, LEPU BIOPHARMA is also exploring the combination therapy potential of OH2 with HX008 or LP002, as well as the combination of ADCs with HX008.

In addition to the aforementioned methods, a private placement may serve as another fundraising avenue for LEPU BIOPHARMA as a publicly listed company.

Private Placement: Simply put, it refers to discounted shares issued non-publicly by listed companies. The number of subscribers shall not exceed 35, the issue price shall not be lower than 80% of the market price, and the subscribed shares shall not be transferred within six months (or 18 months for subscriptions by major shareholders). The use of proceeds must comply with national industrial policies, and the listed company and its senior management must have no record of regulatory violations.

Private placements are increasingly valued by listed companies due to their low entry barriers, flexible mechanisms, large fundraising capacity, and ability to introduce strategic institutional investors. However, given that LEPU BIOPHARMA’s current issue price is already relatively low, and considering the cooling effect of the biopharmaceutical sector’s “winter,” further discounts are likely unfeasible. Therefore, in the short term, private placement plans may not be timely for either LEPU BIOPHARMA, which still faces tight liquidity post-listing, or other listed biopharmaceutical companies generally positioned in the mid-tier.

Amid a sluggish market environment, LEPU BIOPHARMA’s initial public offering (IPO) has faced widespread skepticism. This impact is not limited to LEPU BIOPHARMA alone; the entire Chinese biopharmaceutical industry is confronting challenges associated with its decline from peak performance. Despite these harsh conditions, LEPU BIOPHARMA has successfully completed its listing journey and remained resilient under intense scrutiny. Only companies with substantial strength can endure the trials of winter and welcome the arrival of spring. We believe that with the fresh capital injected through this IPO, LEPU BIOPHARMA will accelerate its pace in overcoming the current downturn.