China Renaissance 2021 Annual Review of Healthcare and Life Sciences | Smart Healthcare Edition

Since the outbreak of the COVID-19 pandemic, market attention to the life sciences and healthcare sectors has remained strong. New technologies such as cloud computing, the Internet of Things (IoT), mobile internet, big data, artificial intelligence (AI), 5G networks, and blockchain have been increasingly adopted in the medical field, driving profound transformations in healthcare and accelerating the emergence of new models, business formats, technologies, and services. How to leverage technology to empower the healthcare industry remains a long-term focus and pursuit for professionals in smart healthcare. The Healthcare and Life Sciences Team at China Renaissance joins you in reviewing the market developments of 2021 and looking ahead to the future.

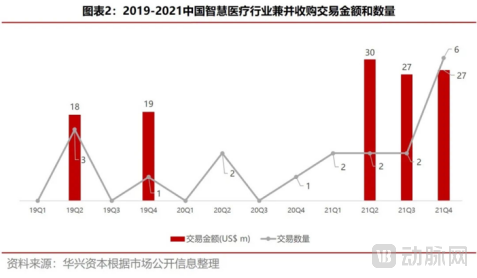

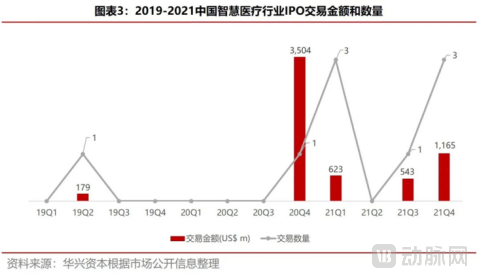

Overall, influenced by the macroeconomic environment, the healthcare industry cooled significantly in the second half of 2021 compared to the first half. However, as an emerging sector, smart healthcare maintained considerable momentum in the private equity market in 2021, with transaction volumes continuing to rise based on primary and secondary market activities. Companies with rapid business development and capital market progress have successively entered the IPO stage, while industry consolidation trends have begun to emerge amid tightening funding conditions.

2021 marked the inaugural year of China’s 14th Five-Year Plan. The state has placed significant emphasis on the smart healthcare and digital health sectors, with relevant authorities intensively issuing outline and regulatory documents pertaining to smart healthcare. These measures aim to establish a more precise and effective medical insurance payment system, enhance the diagnostic and treatment capabilities of hospitals and medical institutions at all levels, advance the development of healthcare informatization, and strengthen the regulation of internet-based healthcare services.

In March 2021, the National Healthcare Security Administration issued the Statistical Bulletin on the Development of Medical Security in 2020, which outlined the current status of DRG pilot programs in multiple cities and clarified the work plan for DIP. This marks China’s entry into an era of precision medical security, wherein the medical insurance fund will more accurately target the attributes of primary care and essential medical services.

In June 2021, the General Office of the State Council issued the “Opinions on Promoting High-Quality Development of Public Hospitals,” proposing to “strengthen the supporting role of informatization” and promote the deep integration of new technologies—such as cloud computing, big data, the Internet of Things (IoT), blockchain, and 5G—with medical services. Hospitals need to enhance their medical service capabilities, accelerate the development of smart hospitals, and implement refined management of health insurance cost containment. In the same month, the National Healthcare Security Administration released the “Healthcare Security Law (Draft for Comments),” marking China’s entry into a new era of healthcare reform governed by law. It also clarified the positioning of commercial health insurance and encouraged enterprises and capital to engage in the commercial health insurance sector.

In September 2021, the National Health Commission and the National Administration of Traditional Chinese Medicine jointly issued the supporting document “Action Plan for Promoting High-Quality Development of Public Hospitals (2021–2025),” which explicitly stated that “by 2022, the average levels of electronic medical record (EMR) application in secondary and tertiary public hospitals across China shall reach Level 3 and Level 4, respectively; the average levels of smart services shall strive to reach Level 2 and Level 3; and the average levels of smart management shall strive to reach Level 1 and Level 2,” thereby supporting a new model of integrated online and offline medical services.

In October 2021, the National Health Commission issued the “Announcement on Soliciting Public Comments on the Detailed Rules for the Supervision of Internet-based Diagnosis and Treatment (Draft for Comments),” which clearly defined the classification of internet hospitals and the scope of diagnosis and treatment. The document covers multiple aspects, including supervision of medical institutions, personnel, business operations, quality and safety, and regulatory responsibilities related to internet-based diagnosis and treatment. These measures, representing continuous improvement and refinement of regulatory frameworks, have further solidified the importance of internet-based diagnosis and treatment in healthcare services.

In 2021, certain niche segments of smart healthcare, such as surgical robots, digital therapeutics, and brain-computer interfaces in neuroscience, became favored targets of capital markets. Meanwhile, previously popular sectors like internet healthcare, AI-driven drug discovery, and AI-assisted diagnosis have entered a consolidation phase following their earlier boom.

1. Surgical Robots

With the booming interest in the broader robotics sector, medical robotics has made significant strides in recent years, with surgical robots and rehabilitation robots leading the rapid development. Surgical robots are primarily categorized into four major types: laparoscopic robots, orthopedic/neurosurgical robots, vascular interventional robots, and needle-based robotic systems.

Among these, da Vinci–representative laparoscopic robotic systems feature high technical barriers and significant clinical efficacy, with approximately 6,000 units installed worldwide, making them the most maturely applied technology in surgery. Orthopedic robots, particularly those for joint procedures, rank second in installation volume and represent the next breakthrough in precision surgery. Compared with open surgery and conventional minimally invasive surgery, surgical robots offer flexible robotic arms compatible with highly complex procedures, greater surgical precision and stability, three-dimensional high-definition visualization, and tremor filtration. They can reduce surgeons’ radiation exposure, decrease postoperative adverse events, accelerate bed turnover, thereby lowering hospitalization costs and improving hospital performance.

The 2021 volume-based procurement (VBP) of orthopedic consumables has prompted investors to shift greater attention toward the orthopedic robotics sector. In the short term, the closed-loop consumption model of “equipment + consumables” remains relatively immune to centralized procurement policies. Compared with other countries, China’s orthopedic surgical robotics industry started later and is still in its early stages of industrialization. According to Persistence Market Research, approximately 26 new orthopedic surgical robots were installed in China in 2018, accounting for less than 4% of the global total. Orthopedic robots can be primarily categorized into spine-focused and joint-focused systems. Domestic companies that have obtained medical device registration certificates for orthopedic surgical robots include Mazor Robotics, MEDTECH, MAKO Surgical, Xinjunte, Santan Medical, and Tinavi. Companies that have completed patient enrollment in clinical trials include Yuanhua Intelligence and Hangzhou Jianjia. Additionally, nearly ten other companies have products currently in the registration-related clinical trial phase. In the spine segment, Tinavi (stock code: 688277), listed on the STAR Market, serves as a representative example; however, due to subpar financial performance over the past two years, questions remain among capital market participants. The joint-focused segment is relatively hotter, with leading enterprises such as Xinjunte, Yuanhua Intelligence, and Changmugu securing substantial financing in 2021.

Furthermore, in 2021, Beijing and Shanghai separately included certain orthopedic robotic surgeries and certain laparoscopic robotic surgeries within the scope of medical insurance reimbursement, marking another investment by China in promoting precision surgery. With the rollout of local medical insurance policies across various regions, 2022 will be a pivotal year for the commercial implementation of surgical robot enterprises in China.

2. Digital Therapeutics

2021 is regarded as the inaugural year of Digital Therapeutics (DTx) in China. Following extensive market education by various institutions and media outlets in the first half of the year, investment firms actively deployed capital in the second half, resulting in numerous companies securing financing. Markets and Markets estimates that the global digital therapeutics market size was $3.4 billion in 2021 and is projected to grow to $13.1 billion within five years, maintaining an annual growth rate of over 20%. In terms of application areas, the most significant investments have been made in neurological and psychiatric disorders, as well as chronic disease management.

Following clinical validation and regulatory approval, digital therapeutics can be introduced into hospitals as “digital drugs” and prescribed by physicians to patients. Alternatively, they can serve as adjunctive interventions for disease management, offering novel approaches to enhance treatment adherence. This facilitates systematic and organized out-of-hospital management and treatment protocols, reduces the total medication costs per patient across the entire care continuum, and further curbs healthcare expenditures.

The surge in popularity of digital therapeutics (DTx) over the past two years can be attributed to two primary factors. First, regulatory authorities have clarified the submission framework for DTx as “digital drugs.” Companies such as Pear Therapeutics, Akili Interactive, and Propeller Health have conducted extensive clinical trials, resulting in FDA approval for nearly 30 DTx products. These approvals have demonstrated the efficacy of software-driven interventions across various therapeutic areas, including neuroscience, cognition, respiratory health, motor function, and endocrinology. Second, several prominent U.S. DTx companies spearheaded the establishment of the Digital Therapeutics Alliance (DTA), which defined the scope, definition, and regulatory pathways for DTx. This initiative rapidly attracted participation from numerous enterprises and provided substantial resources for market education. In 2021, multiple Chinese DTx companies joined the DTA, including Miao Health, Weimai, Shuyu Technology, MedSci, Wangli, Liangyihui, and Jianhai Technology.

Since November 2020, some domestic manufacturers have obtained Class II certification for digital therapeutics. However, the approval rules and processes for the more prestigious Class III certification remain to be clarified. In 2022, regulatory registration filings and clinical trials will become new strategic imperatives that companies in this sector must address. As a therapeutic product category that can be directly offered to patients, digital therapeutics boast relatively broad commercialization scenarios. Nevertheless, as an emerging sector, the practical implementation of commercialization remains a significant challenge.

3. Brain Science and Brain-Computer Interfaces

Brain science is at the forefront of global scientific research today and is regarded as the “final frontier” of natural sciences. Developed economies such as those in Europe, the United States, and Japan have made substantial investments in this field. According to data from CB Insights, the global market size for brain science reached $6.2 billion in 2020 and is projected to surpass $10 billion by 2024, with a compound annual growth rate (CAGR) of 17% expected between 2020 and 2024. It is widely recognized as the next industry poised to bring disruptive impact to human society.

In recent years, China has continued to invest in brain science research and industrial development. During the 13th Five-Year Plan period, the "China Brain Project" was officially launched, during which Chen Tianqiao, founder of Shanda Group, announced a $1 billion investment to establish a Brain Science Research Institute. The Outline of the 14th Five-Year Plan (2021–2025) for National Economic and Social Development and the Long-Range Objectives Through the Year 2035, released in March 2021, stated that during the 14th Five-Year Plan period, China's Brain Project would adopt a structure of "one body with two wings." This framework is based on researching the neural principles of brain cognition, aiming to develop treatments for major brain disorders and promote the development of next-generation artificial intelligence. In September 2021, the Guidelines for Project Applications in 2021 under the Major Science and Technology Innovation 2030 Program—"Brain Science and Brain-Inspired Intelligence" were released, marking the official commencement of China's Brain Project. Currently, domestic entrepreneurial teams in the field of brain science primarily originate from universities and research institutions.

The continuous cross-disciplinary expansion between brain science and other fields has spurred the emergence of new disciplines and technologies, such as neuroeducation and brain-computer interfaces (BCIs), with applications spanning bionics, artificial intelligence, healthcare, and more. Among these, BCIs have become a hot topic in brain science in recent years. They primarily facilitate information exchange between the brain and external devices, enabling direct control of such devices by the brain without relying on the peripheral nervous system. Based on methods of brain signal acquisition, BCIs are mainly categorized into invasive, non-invasive, and semi-invasive types, each with its own advantages and disadvantages.In recent years, the BCI field has frequently made headlines in major medical media outlets and has given rise to numerous standout companies. Examples include Neuralink, founded by Tesla’s Elon Musk; BrainCo, established by the first Chinese team selected for the Harvard Innovation Lab; and NeuroPace, which competes with industry giants such as Abbott, Boston Scientific, and Medtronic. Additionally, domestic Chinese manufacturers such as NeuraMatrix, UltraBrain Galaxy (Younao Yinhe), BrainLand (Naolu Technology), and BoRuikang have emerged as star players in this sector.