Domestic CGM Breakthrough: How Chinese Innovators Are Challenging Global Giants in the Continuous Glucose Monitoring Market

Sibionics

Medical Device R&D and Manufacturing Company

For Ms. Yu (a pseudonym), who has been living with diabetes for five years, the need to prick her fingers multiple times a day to monitor blood glucose levels has triggered a strong aversion to needle sticks; at one point, she even felt discomfort merely at the sight of needles. For diabetic patients like Ms. Yu, the ultimate goal is to control blood glucose and prevent various complications, while their greatest hope is to avoid needle pricks altogether. Continuous glucose monitors (CGMs) can fulfill this most basic desire.

In the field of Continuous Glucose Monitoring (CGM), the domestic market was previously almost monopolized by imported brands, with domestically produced products arriving late to the scene. In recent months, CGM products from Infinovo Medical, Shenzhen Sibionics, and MicroTech Medical have successively received approval from the National Medical Products Administration (NMPA).

Over the past five years, the global CGM industry has experienced rapid growth, with the market size exceeding $5 billion. However, due to high technological barriers and a concentrated competitive landscape, the Chinese market developed slowly in its early stages. With the emergence of new domestic brands and products, all must face competition from international giants such as Abbott. How can Chinese companies capture market share from these supergiants?

For both type 1 and type 2 diabetes, the mainstream treatment approach involves a combination of lifestyle interventions and pharmacotherapy to control blood glucose levels. Medication dosages must also be adjusted to maintain blood glucose within a reasonable range. Therefore, blood glucose monitoring is a critical component of diabetes management and care.

Blood glucose monitoring methods are diverse, covering changes in blood glucose levels from the dimensions of "point," "line," and "plane." The "point" refers to self-monitoring of blood glucose (SMBG), typically using a blood glucose monitor (BGM) with capillary blood from the fingertip, which measures blood glucose levels at the specific moment of sampling. The "line" refers to continuous glucose monitoring (CGM), which uses subcutaneous micro-electrochemical sensors to measure glucose concentrations at regular intervals, generating hundreds of readings per day to capture the patient’s full-day blood glucose fluctuations. The "plane" refers to glycated hemoglobin (HbA1c), which reflects the average blood glucose levels over the past three months.

Currently, blood glucose monitoring (BGM) via fingerstick blood sampling remains the mainstream approach. However, BGM has several pain points: first, the frequent need for blood collection often causes patient discomfort; second, the inconvenience of carrying testing supplies poses challenges for patients when traveling; and third, inferring blood glucose fluctuations from limited sampling points fails to accurately reflect the true physiological state. The last issue is particularly critical, as blood glucose levels fluctuate throughout the day in response to patients’ daily activities. Traditional BGM methods struggle to provide real-time monitoring, thereby hindering patients’ ability to take timely actions to manage their blood glucose levels and ultimately posing risks to their health.

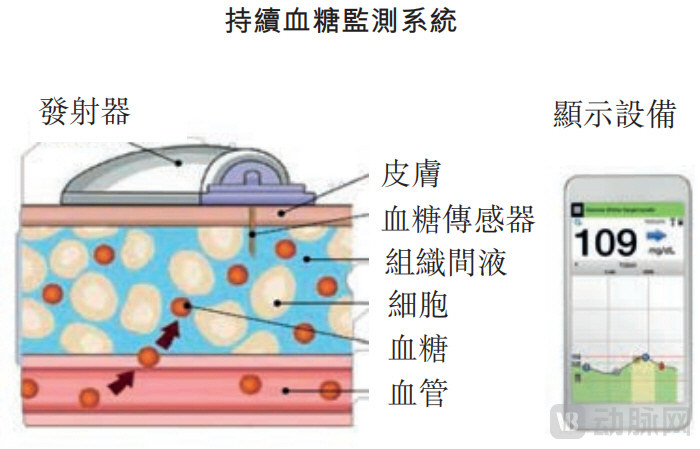

Continuous Glucose Monitoring (CGM) systems do not require fingerstick blood sampling; instead, they indirectly reflect blood glucose levels by monitoring glucose concentration in the subcutaneous interstitial fluid via a glucose sensor. These systems provide continuous, comprehensive, and reliable around-the-clock glucose data, enabling a better understanding of glucose fluctuations and overcoming the limitations of capillary blood glucose monitoring. In the future, CGM systems can be integrated with insulin pumps to guide insulin dosing based on real-time glucose information.

In an interview with VCBeat, Shenzhen Sibionics Co., Ltd. stated, “Compared with BGM, CGM can better help patients maintain blood glucose levels within the normal range and reduce HbA1c levels. Its applicable populations and scenarios are becoming increasingly extensive. Multiple diabetes guidelines, including the ‘Chinese Clinical Guidelines for Blood Glucose Monitoring’ and the American ‘Standards of Medical Care in Diabetes—2022,’ recommend its clinical use. It will play an increasingly important role in blood glucose management in the future.”

If the result of BGM is a single image, then the result of CGM is a 14-day-long movie; the amount of information they contain is not on the same order of magnitude. To realize such an extensive “movie” through a device of merely square inches, the technical difficulty is self-evident.

A CGM system consists of a sensor, transmitter, and receiver, offering relatively flexible wearing and data reception options. The CGM monitors glucose concentration in the interstitial fluid via a subcutaneously implanted sensor, which is then converted into blood glucose levels through algorithms. Glucose in the interstitial fluid interacts with the sensor, triggering redox reactions that convert chemical signals into electrical signals, which are ultimately transmitted by the transmitter to the receiver.

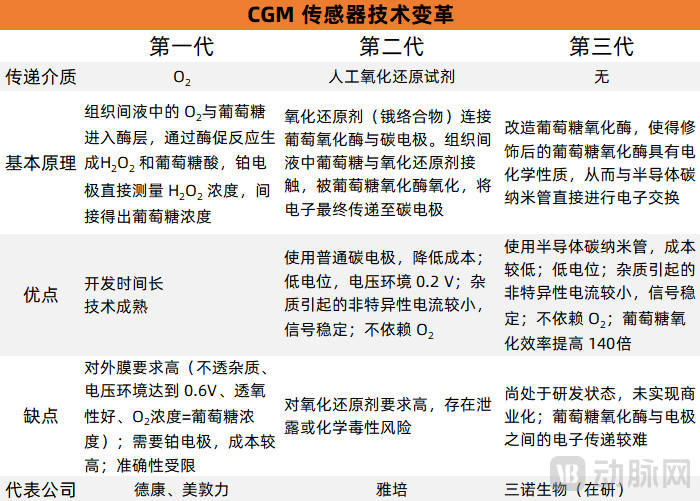

Although CGM devices are compact, they face four major technical barriers, namely:Sensor、Adventitia、AlgorithmandIntegration with Insulin Pumps. The sensor is the most critical component of CGM and also the most technically challenging part. CGM has undergone three major technological revolutions, primarily centered on capturing electrical signals generated during glucose oxidation. This not only requires the generation of stable electrical signals but also adaptation to the complex physiological environment of interstitial fluid. The representative companies for these three technological revolutions are Dexcom, Abbott, and Sinocare.

The outer membrane is the core component of the sensor. Its overall design must meet the following requirements: align with the sensor’s design strategy; allow glucose to permeate at a designed rate; minimize the passage of impurities; extend the sensor’s service life; and function effectively under physiological conditions. Consequently, there are stringent requirements for materials, physical properties, and biocompatibility. This constitutes a significant technical barrier for continuous glucose monitoring (CGM) products, with the relevant intellectual property primarily held by a few major players in the blood glucose monitoring industry.

Algorithms are a critical factor in monitoring accuracy. The input for continuous glucose monitoring (CGM) systems is the glucose concentration in interstitial fluid, while the output is the blood glucose concentration. The objective of algorithm research is to convert input data into output data as accurately as possible. However, the conversion ratio is not constant across individuals or under different physiological conditions. Companies need to continuously optimize their algorithms through data accumulation to further reduce the Mean Absolute Relative Difference (MARD). Industry leaders enjoy a first-mover advantage by leveraging their historical data and experience.

Integrating with insulin pumps to create an "artificial pancreas" represents the developmental direction of continuous glucose monitoring (CGM) systems. The advantage of insulin pump delivery lies in its ability to mimic physiological insulin secretion, thereby ensuring stable blood glucose control. Its technical barriers reside primarily in micro-motor technology (sourced mainly from Switzerland's MAXCON), while intelligent control algorithms, alarm systems, and consumables also impact product quality. No mature domestic products are currently available in China. In the global market, Medtronic is the only company with fully independent research and development capabilities, whereas Abbott and Dexcom collaborate with insulin pump manufacturers for production.

In 2019, Abbott, Dexcom, and Medtronic held 44.5%, 35.7%, and 19.3% of the global CGM market share, respectively, effectively dominating the worldwide market. In the U.S. CGM market, Dexcom accounted for nearly 60% of the market share. In China’s CGM market, Abbott captured nearly 80% of the market share, while Medtronic held approximately 11%.

A comparison of products from three multinational corporations reveals that Abbott’s advantages are primarily evident in two aspects: first, its sensors have a longer service life and offer greater convenience; second, the annual cost for patients is lower. The annual cost of using Abbott’s CGM product is approximately USD 3,400 or RMB 11,000, which is significantly lower than that of Dexcom and Medtronic products, thereby imposing a lighter financial burden on patients.

Abbott’s CGM products utilize second-generation sensor technology, derived from the “wired enzyme” technology acquired through the $1.2 billion purchase of TheraSense in 2003. This technology transmits signals from glucose oxidation to carbon electrodes via osmium-complex wired enzymes, thereby overcoming limitations posed by high impurity levels and low oxygen content in interstitial fluid. Consequently, it imposes less stringent requirements on the sensor’s outer membrane compared to Dexcom’s first-generation sensors.

Furthermore, Abbott’s CGM products integrate the counter electrode, reference electrode, and carbon working electrode onto a polyester substrate, ultimately forming a single electrode strip. Compared with Dexcom’s multi-layer structure, Abbott’s sensor design employs carbon electrodes and is amenable to mass production, thereby reducing costs and facilitating a price advantage. With its lower-priced CGM products sold in the United States, Europe, and China, Abbott is the company with the highest market share in the global CGM market.

Since the launch of the first CGM product in 2008, Abbott has introduced four CGM products: FreeStyle Navigator, FreeStyle Libre Pro (for healthcare professionals), FreeStyle Libre, and FreeStyle Libre 2. Among these, the FreeStyle Libre, launched in 2017, is available in multiple regions including China, the United States, and Europe. The product currently sold in China under the name “Fu Li Shan Shun Gan” is this very model.

Abbott’s latest product, the FreeStyle Libre 2, was launched in the United States in 2020, with a MARD value as low as 9.2%. Compared to previous versions, the new CGM device features real-time data reading and newly added alarm functions. It also partners with Insulet, a leading insulin pump manufacturer, and is compatible with their Omnipod Horizon automated insulin delivery system, connecting to form an “artificial pancreas.” Abbott’s FreeStyle Libre 3 is still under FDA review, and its sensor is only the size of a coin.

It is worth highlighting Abbott’s performance in the Chinese market. Since the FreeStyle Libre received regulatory approval for launch in China in 2016, the country has rapidly grown into the world’s largest out-of-pocket market for the product. Prior to its Chinese debut, professional consulting firms had recommended a price point above RMB 1,000; however, Abbott ultimately set the unit price at approximately RMB 600. The challenge posed by this low-price strategy lay in devising an effective channel strategy within constrained gross margin parameters. To address this, Abbott proactively went all-in on e-commerce channels, thereby successfully resolving the distribution challenges associated with its consumer-friendly pricing approach.

Thus, since pioneering the establishment of a Tmall flagship store for medical devices across China in 2017, Abbott’s FreeStyle Libre has consistently ranked first among imported brands in the blood glucose monitoring category during major e-commerce promotions such as the June 18 (6.18) and Singles’ Day (Double 11) shopping festivals. Furthermore, Abbott has launched initiatives including its Chief Experience Officer program and the “FreeStyle Libre Cycling Club” for individuals with diabetes, inviting figures ranging from former UK Prime Ministers to Real Madrid football stars to experience FreeStyle Libre products and share how the technology has transformed their lives, garnering extensive media coverage. Leveraging its advantages as a multinational corporation, Abbott has ensured precise and effective product promotion. Following the completion of its consumer-facing sales channel layout, Abbott introduced the hospital version of FreeStyle Libre in 2018, marking its strategic penetration into hospital-based channels.

Recognizing that going it alone was insufficient, Abbott has successively partnered with enterprises such as Ping An Insurance and ZhongAn Insurance to lower the payment threshold for FreeStyle Libre. It has also collaborated with Zhiyun Technology, Tangtangquan, Sinopharm Health, and JD Internet Hospital, while jointly calling on delegates to the Two Sessions to advocate for the inclusion of type 1 diabetes in the national rare disease catalog. Over the years, Abbott’s partners have included not only companies such as AliHealth, JD.com, First Pharmacy, and Nepstar, but also public policymakers, including the Qingdao Municipal Government. Building a vibrant ecosystem is central to Abbott’s strategy for promoting FreeStyle Libre—a philosophy that has enabled FreeStyle Libre to capture nearly 80% of the continuous glucose monitoring (CGM) market in China.

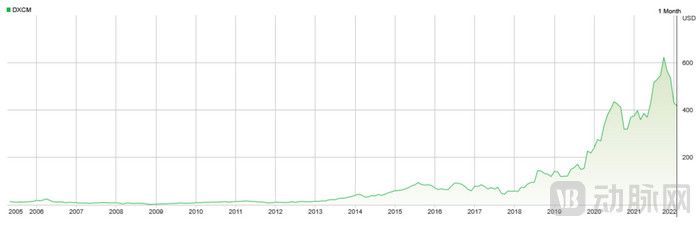

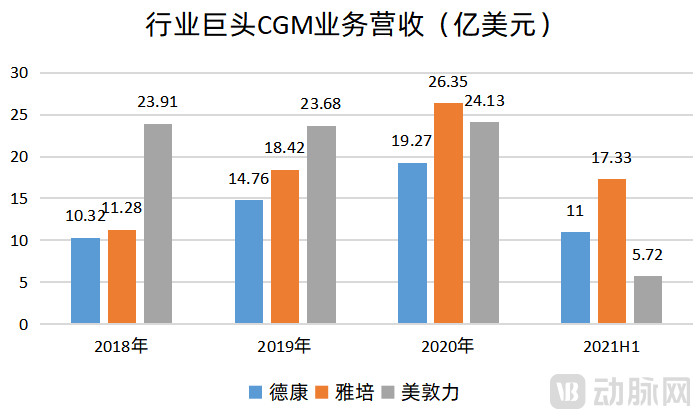

Among the three international CGM giants, Dexcom focuses exclusively on CGM glucose monitoring, while Abbott and Medtronic have multiple business segments. Therefore, we can correlate Dexcom’s performance in the secondary market with the development of the CGM industry.

Dexcom’s stock price can be broadly divided into three phases. The first phase, from 2005 to 2013, was a period of price stability. Following its listing on the NASDAQ with a valuation of approximately $5.2 billion, the company successively launched the G1–G4 product series, which received lukewarm market response. The second phase, from 2013 to 2017, saw a gradual rise in stock price. The turning point came in 2014, when Dexcom collaborated with the University of Padova to develop the 505 algorithm, which was integrated into the G4 system. This reduced the Mean Absolute Relative Difference (MARD) from 13% to 9%, establishing accuracy as an industry benchmark. The G5 model, launched in 2015, retained this algorithm and garnered positive market feedback.

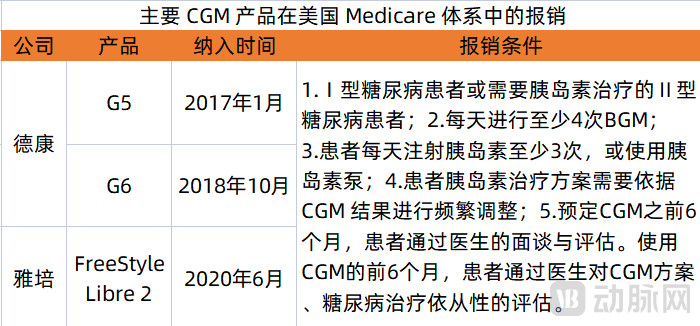

Phase III, beginning in 2018, was marked by a significant surge in stock price. During this period, Dexcom launched its flagship product, the G6, which offered substantial improvements over the G5 in terms of sensor lifespan and fingerstick blood glucose calibration, and enabled integration with automated insulin delivery systems. Another milestone event was the inclusion of Dexcom’s products in Medicare reimbursement coverage in 2017. By November 9, 2021, Dexcom’s market capitalization reached $61.7 billion. It was also during this period that CGM market penetration steadily increased, with Dexcom, Abbott, and Medtronic successively launching integrated CGM products, further heating up the market.

Most of Dexcom’s products have received dual certification from the United States and the European Union, with U.S. sales revenue accounting for 78.3% of its total revenue, making it the company’s primary income source. Considering only CGM products (excluding insulin pumps), Dexcom’s sales revenue is second only to Abbott’s, and it held a 57.5% market share in the U.S. market in 2019. Despite their higher price point, Dexcom’s CGM products capture more than half of the U.S. market; this dominance is attributable not only to product-related factors but also to Dexcom’s early entry into the Medicare system.

Cost is an unavoidable consideration for patients. For blood glucose monitoring (BGM) systems, the annual cost is approximately RMB 1,500, calculated based on one glucometer and 365 sets of test strips and lancets (four per day). In contrast, for continuous glucose monitoring (CGM) systems, taking Abbott’s FreeStyle Libre—the brand with the largest market share in China—as an example, 26 sensors are required per year, resulting in a cost exceeding RMB 10,000. If borne out-of-pocket, this imposes a significant financial burden, which indirectly affects market demand and adoption.

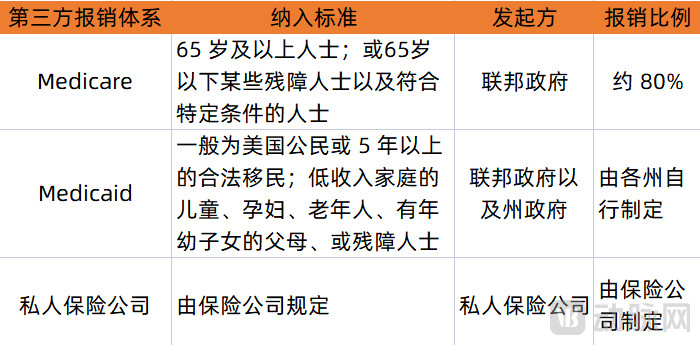

The United States has a diverse third-party reimbursement system, with continuous glucose monitoring (CGM) covered under Medicare, Medicaid, and private insurance plans. CGM devices from companies such as Dexcom and Abbott are included in Medicare coverage, requiring eligible patients to pay only 20% of the cost. Under Medicaid, reimbursement criteria are determined by individual states, and reimbursement rates for CGM depend on each state’s regulations. Reimbursement conditions and rates among private insurers vary by company. Supported by the U.S. reimbursement framework, CGM penetration has increased significantly, reaching 25.8% in the United States in 2020, compared to just 10% in other regions worldwide.

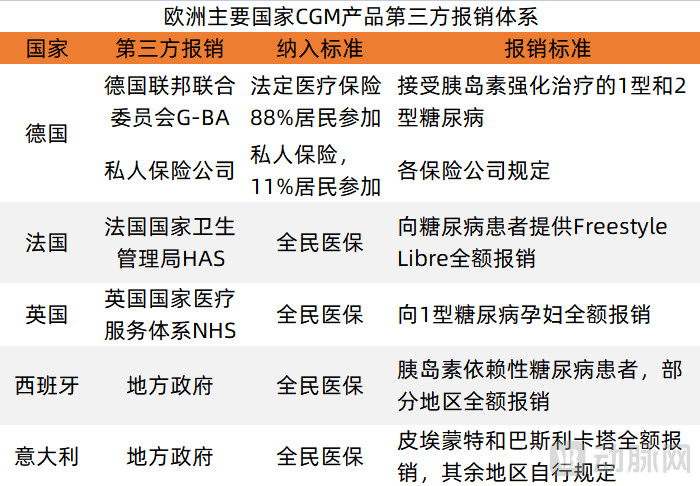

Many European countries have also incorporated continuous glucose monitoring (CGM) systems into their reimbursement frameworks. In the United Kingdom and France, eligible patients receive full reimbursement through national healthcare systems, while in Germany, private insurers provide partial or full coverage for patients meeting specific criteria. The inclusion of CGM devices in third-party reimbursement systems across Europe and the United States has alleviated individuals’ financial burdens, serving as an intrinsic driver for market expansion.

Blood glucose monitoring has been established earlier in Europe and the United States, where market education is already complete; therefore, retail channels dominate sales. In the United States, for example, retail accounted for 85% of the BGM market in 2020, compared to only 50% in China. As an innovative and relatively high-priced blood glucose monitoring device, CGM is typically first used or switched through hospital-based channels, while subsequent repurchases are mostly made through retail channels or other reimbursable channels.

In European and American markets, retail has become a key sales channel, driven by well-established market education, relatively high penetration rates, and minimal reimbursement restrictions. Furthermore, the frequent use of blood glucose monitoring devices by diabetic patients makes the retail model better aligned with their usage scenarios, serving as another major driver of market demand.

The market share of continuous glucose monitoring (CGM) systems in China is generally lower than that in the United States and Europe. Patients with type 1 diabetes and those with type 2 diabetes requiring intensive insulin therapy have a greater dependence on insulin treatment, leading to higher acceptance of glucose monitoring compared to other types of diabetic patients. In 2020, the CGM penetration rate among patients with type 1 diabetes was 25.8% in the United States, whereas it was only 6.9% in China, amounting to just one-quarter of the U.S. level. The majority of patients requiring regular monitoring still rely on blood glucose monitoring (BGM) products, which fail to adequately meet the needs for real-time monitoring and timely glycemic control.

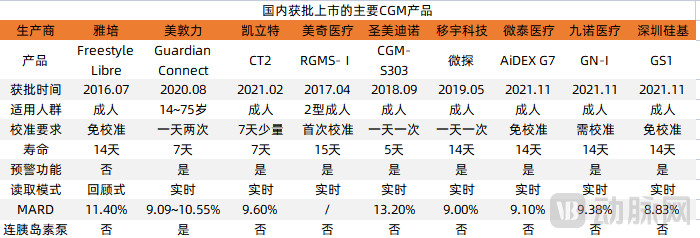

China’s CGM market is in its early stages of development. Driven by substantial market demand, domestic companies have continuously intensified their efforts to overcome CGM technical challenges and have achieved successive successes. Currently, two imported products (Abbott, Medtronic) and seven domestically produced products (Sinocare, Kailite, Yiyu Technology, Princeton, Meiqi, Sibionics, MicroTech, and Infinovo) are available on the Chinese market. In addition, domestic companies such as Sinocare Biosensor are engaged in the research and development of next-generation sensor technologies. VCBeat has compiled an overview of the major CGM products currently marketed in China.

From a product perspective, domestically produced devices have fully leveraged their late-mover advantage, matching or even surpassing imported products in performance. This is no easy feat. In an interview, a representative from Sibionics, which currently boasts the best Mean Absolute Relative Difference (MARD) value, stated: “The MARD value has consistently been regarded within the industry as a key reference indicator for product accuracy, while sensor technology is the primary factor influencing product performance. Sibionics employs second-generation sensor technology, featuring independently designed and synthesized metal redox polymers that replace oxygen as electron mediators to support in vivo redox reactions. This approach shields product performance from interference by biological environmental factors, significantly enhancing monitoring accuracy, stability, and anti-interference capabilities.”

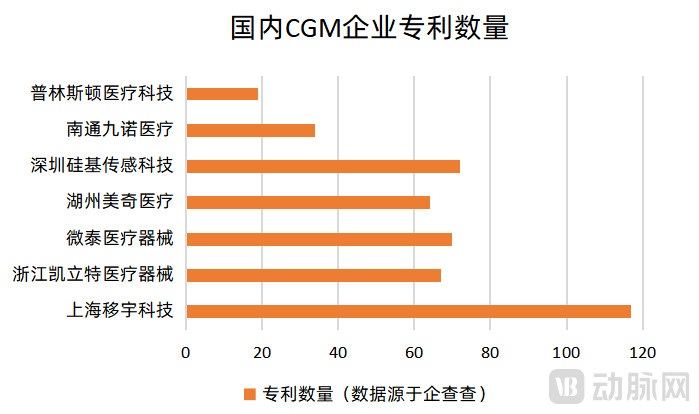

R&D investment can also be gauged by the number of related patents. It is evident that domestic companies possess a strong awareness of technological protection, with over 400 relevant patents filed for CGM technology and product improvements (this figure includes patents related to the insulin pump businesses of MicroTech Medical and Shanghai Yuyue). While expanding their domestic distribution channels, many Chinese companies are also securing patent protection in overseas markets through the Patent Cooperation Treaty (PCT) route.

Of course, there is still room for improvement in domestically produced products. For instance, in terms of calibration, currently only Sibionics and MicroTech Medical offer fully calibration-free solutions, while other domestic products still require fingerstick blood glucose calibration to varying degrees. This is not particularly user-friendly.

For companies, beyond the technical challenges in the R&D phase, ensuring the consistency and stability of CGM products after large-scale commercial production presents another significant hurdle. Therefore, the manufacturing process should not be overlooked. For instance, Shenzhen Sibionics Co., Ltd. has established a precision manufacturing system that includes a 3,600-square-meter Class 10,000 cleanroom workshop, a 150-square-meter independent chemical synthesis laboratory, high-precision laser cutting systems, precision enzyme dispensing systems, and precision alignment screen printing systems. It also features self-developed AOI (Automated Optical Inspection) visual inspection systems, ICT (In-Circuit Test) systems, and high-throughput electrochemical testing systems, along with advanced detection equipment to provide quality assurance for standardized production. These capabilities are essential to guarantee product consistency at an annual production scale of millions of units.

MicroTech Medical also stated in its prospectus that it has specifically constructed a 1,500-square-meter ISO Class 7 cleanroom and an 80-square-meter ISO Class 8 cleanroom for product manufacturing and pre-delivery inspection. This indicates that the mass production phase is not only related to cost but also a critical factor in achieving calibration-free performance.

Furthermore, domestically produced CGMs generally adopt real-time reading methods, unlike the retrospective approach used by Abbott’s FreeStyle Libre. The distinction lies in the fact that retrospective reading involves the CGM collecting and storing data at set intervals, which is then retrieved and displayed via a reader or smartphone; whereas real-time reading not only records data at regular intervals but also monitors current blood glucose levels and provides alerts for dangerous fluctuations. For patients at risk of hypoglycemia, this feature is critically important and serves as a key selling point that highlights product competitiveness.

Technological gaps can be closed by increasing R&D investment, but the market gap is the real challenge facing domestic companies. In the face of Abbott’s 78% and Medtronic’s 11% market share in China’s CGM market, domestic companies remain optimistic. According to IDF data, China had 140 million diabetes patients in 2021, making it the country with the largest number of diabetes patients globally. The growth rate from 2011 to 2021 reached 56%, and this figure is expected to continue growing at a high speed.

In terms of market penetration, data from MicroTech Medical’s prospectus shows that in 2020, the CGM penetration rates for type 1 diabetes, type 2 diabetes, and gestational diabetes were 25.8%, 9.0%, and 4.0% respectively in the U.S. market; 18.2%, 7.0%, and 2.8% in the five major EU countries; and only 6.9%, 1.1%, and 0.3% in China. It is projected that by 2030, these figures will rise to 63.7%, 50.7%, and 9.2% in the U.S., 60.6%, 49.2%, and 6.2% in the five major EU countries, and 38.0%, 13.4%, and 1.0% in China. This means that in the coming years, the domestic CGM penetration rate will be more than five times its current level, indicating broad market prospects.

From this perspective, Abbott’s current 78% market share does not constitute a particularly serious issue. This is because domestic companies are not engaged in a zero-sum competition with Abbott and Medtronic over existing market share; rather, they are each striving to expand an incremental market. In the early stages of industry development, having a leading enterprise drive the expansion of the overall market is not detrimental to other players in the sector.

As patient awareness of continuous glucose monitoring (CGM) remains limited in China, product selection largely depends on physician education. Physicians’ endorsement of CGM products requires long-term clinical observation. From product development to market education, and from marketing promotion to comprehensive digital services, robust product quality and rapid iteration capabilities are essential to secure long-term recognition from medical experts. Domestic companies are well aware of this and are tailoring product features to meet hospital-based needs.

Taking Sibionics as an example, a hospital-wide glucose management solution has been developed around its CGM products, enabling unified management of patients across multiple departments. This solution integrates the entire workflow of glucose data display, storage, and transmission, thereby creating favorable conditions for remote endocrinology consultations. Physicians can gain comprehensive insights into changes in patients’ conditions, assess the severity of metabolic disorders, and formulate rational glucose-lowering regimens. This approach enhances the work efficiency of healthcare professionals and improves the rate of glycemic target attainment among hospitalized patients.

Since continuous glucose monitoring (CGM) and blood glucose monitoring (BGM) target similar patient populations, manufacturers with established BGM sales channels can gain a first-mover advantage in the future CGM market competition. For instance, Yuwell Medical entered the CGM sector by acquiring equity in Zhejiang Kailite. If Sinocare successfully develops its products based on third-generation sensor technology, its existing 18 million BGM end-users would constitute a potential customer base.

Meanwhile, domestic companies are leveraging their localization advantages by integrating numerous features into mobile apps. In addition to basic functions such as viewing blood glucose levels and trends, and receiving alerts for hyperglycemia and hypoglycemia, users can also receive recommendations on diet, exercise, and sleep. For instance, Shenzhen Sibionics Co., Ltd. enables remote data sharing and collaborative disease management among family members through its mini-program. It also generates blood glucose reports compliant with clinical guidelines. Through its affiliated Sibionics Internet Hospital, and in conjunction with a professional service team comprising endocrinologists and physician assistants, the company provides enhanced digital medical services to patients, their families, and healthcare providers across various blood glucose management scenarios both inside and outside hospitals. For continuous glucose monitoring (CGM) products, which involve recurring consumption, patient-centered care services can effectively improve user adherence.

Furthermore, in terms of market layout, since the approval cycle for EU CE certification is shorter than that in China and the United States, many domestically produced products even enter the European market first. For example, Infinovo Medical obtained its EU CE certificate in June 2019. Currently, its CGM products are being sold simultaneously in 15 overseas countries; Shanghai Yiyu has also entered multiple European countries; Zhejiang Kailite has partnered with Ascensia Diabetes Care to promote and sell its products in the international market.

The high penetration of CGM in the U.S. market is inseparable from the support of insurance coverage. In this regard, domestic policies in China have not yet provided comprehensive coverage. Currently, policies vary by locality; for example, Shenyang has included CGM in its medical insurance reimbursement list, and Shanghai has launched partial pilot programs. However, these measures largely target inpatient reimbursement, while home use remains excluded from coverage. From an economic perspective, controlling blood glucose levels to reduce complications holds positive significance for containing medical insurance costs, suggesting that changes may occur in the future.

Regarding future development, domestic enterprises have their own strategic considerations. For instance, MicroTech Medical is developing next-generation artificial pancreas products that integrate its proprietary continuous glucose monitoring (CGM) systems with insulin pumps, thereby deepening its engagement in this field. Meanwhile, Shenzhen Sibionics Co., Ltd. believes that CGM products are not limited to patients with diabetes. Blood glucose levels directly or indirectly affect the metabolic system, organ health, and the immune system; in daily life, these effects are reflected in areas such as exercise, fitness, and fat loss. Therefore, CGM-based technology can be leveraged to develop blood glucose monitoring products better suited for these populations, thereby expanding the target audience.

As technology continues to mature, continuous glucose monitoring (CGM) systems will gradually gain wider acceptance among patients with diabetes. During the rapid growth of China’s CGM industry, companies with robust product portfolios, such as Shenzhen Sibionics Co., Ltd., MicroTech Medical, and Infinovo Medical Co., Ltd., have emerged. Meanwhile, enterprises like Sinocare Inc. are striving to achieve leapfrog development in foundational CGM technologies. In addition, listed companies including Lepu Medical, Andon Health, and Cofoe Medical have announced their independent research and development efforts in CGM. Looking ahead, companies that offer high-quality products at competitive prices, maintain comprehensive market layouts, and possess strong channel sales capabilities are more likely to succeed. We anticipate the rise of a new wave of domestic players that will continuously break through technical barriers and expand market reach.