Sipai Health Technology Files Updated Prospectus to Capture Trillion-Yuan Commercial Health Insurance Opportunity

Commercial health insurance has become a blue-ocean market that countless enterprises are eager to enter.

In recent years, against the backdrop of "Healthy China" becoming a national strategy, commercial health insurance has achieved rapid development, driven by favorable policy dividends for health insurance and heightened public awareness of health insurance.

Data offers a glimpse into the growth potential of the health insurance market.According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the compound annual growth rate of health insurance premiums reached 28% over the past five years, far exceeding that of life insurance and accident insurance. Health insurance premiums were projected to surpass the RMB 1 trillion mark in 2021. Moreover, the share of health insurance among all insurance categories rose from 18.2% in 2016 to 23% in the first five months of 2021, making it the second-largest insurance segment in the industry.

More importantly, with rising out-of-pocket healthcare expenditures, the onset of population aging, accelerated urbanization, and an expanding population of patients with chronic diseases,China’s current social security provision capacity still struggles to meet the rapidly growing health protection needs of its population, particularly the demand for supplementary and upgraded medical services among urban employees with greater financial means and their families.

The underlying reason is that the basic medical insurance scheme is designed to provide fundamental coverage and cannot bear additional medical costs; therefore, the development of commercial health insurance is needed to cover the portion not reimbursed by basic medical insurance. According to statistics from the National Healthcare Security Administration, by the end of 2020, the number of participants in China’s Employee Basic Medical Insurance had reached 340 million, representing a single-country market comparable in size to the total population of the United States, which undoubtedly constitutes a vast sector for growth.

Based on this, numerous companies have entered the market. Among them,As a representative enterprise in the industry, Medbanks Health Technology recently publicly updated its prospectus, continuing to accelerate its IPO process.

To date, Medbanks Health Technology has enjoyed the long-term favor of numerous high-quality investment institutions.Such as Tencent, Fidelity Investments’ funds, Times Capital, IDG Capital, Shuanghu Capital, Adamas Capital, CDH Investments, and many other secondary market professional investors involved in healthcare and biotechnology IPOs over the past two years, including Hudson Bay, Octagon, 3W, etc.

What is the current landscape of the health insurance market? What challenges and opportunities exist? What is the future evolution path? To address these questions, VCBeat examines the industry landscape and analyzes the updated prospectus of Medbanks Health Technology to glean insights into the answers.

The Future of Health Insurance Is Closely Linked to the Direction of Healthcare Reform.

From a macro perspective, improving the efficiency of medical insurance fund expenditures and implementing cost containment measures have been the government’s approach to healthcare reform in recent years.Thus, it can be seen that the National Healthcare Security Administration was established during the 2018 major reform of State Council institutions, with its mission being “healthcare cost containment” and “coordinated reform of healthcare, health insurance, and pharmaceuticals.”

Against this backdrop, the development of health insurance to serve as a supplementary component of medical security has been frequently highlighted in policy discussions. For instance, in March 2020, the “Opinions on Deepening the Reform of the Medical Security System” issued by the Central Committee of the Communist Party of China and the State Council explicitly defined commercial health insurance as an important supplement to basic medical insurance and a key element of China’s multi-tiered medical security system. Furthermore, the 14th Five-Year Plan not only emphasized the national strategy of “Healthy China” but also mentioned “insurance” more than ten times.

In addition to easing the pressure on the medical insurance system through policy support, health insurance can also resolve supply-side contradictions.This is because, driven by factors such as the expanding population with chronic diseases and rising economic levels, there is an increasingly strong demand for high-quality medical resources and better control of healthcare expenditures, which in turn has fueled growing market demand for health insurance.

For users,The greatest value of health insurance lies in its ability to address future uncertain medical expenses through affordable and predictable upfront costs.It is important to note that although most diseases are currently covered by national health insurance, and drug prices have shown a significant downward trend under the volume-based procurement policy, the out-of-pocket medical burden on individuals remains substantial.

According to data released by the National Healthcare Security Administration and the National Health Commission, the total expenditure of the national basic medical insurance fund (including maternity insurance) in 2020 amounted to RMB 2.1032 trillion, accounting for 41.8% of China’s total social and personal health expenditures in that year—still less than half. At the individual level, however, a single major accident can plunge an ordinary household into poverty due to illness, highlighting an urgent need to address this risk exposure.

It is precisely for this reason that hundreds of millions of urban employees and their families, who possess greater financial capacity, have seen a surge in demand for health insurance. This has driven the rapid development of the health insurance sector, turning it into a trillion-yuan blue ocean market.

However, issues have gradually emerged: in the traditional insurance market, companies often operate health insurance with a mindset of “buy insurance, get services,” which has prevented health insurance from realizing its true value.

This lies in the fact that,The essence of health insurance lies in the management capability of medical healthcare, meaning its value must be built upon a matched medical security service system.. This is also the foundation for the long-term and healthy development of commercial health insurance.

To this end, the “Report on Issues and Recommendations for the Development of Commercial Health Insurance in China,” issued by the China Banking and Insurance Regulatory Commission (CBIRC), specifically points out that greater integration between health insurance and health management should be promoted, comprehensive health insurance products and services should be provided, and collaborative operations between health insurance and health management services should be achieved.

In line with this trend, a large number of innovative health insurance companies have emerged, including Medbanks Network Technology. Unlike traditional health insurers, they adopt a patient-centric approach,By leveraging its robust and comprehensive capability to integrate medical resources, it has used the healthcare network as an entry point to establish a new logic for health insurance centered on health management services.

Since then, the health insurance industry has entered the eve of profound transformation, with the market landscape shifting toward diversification. Specifically, it is evolving from a model dominated by single insurance carriers into a diversified ecosystem encompassing internet platforms, healthcare institutions, pharmaceutical groups, health management organizations, medical big data companies, and entities from the real economy.

Following this path, leading enterprises have achieved rapid development and gradually approached the eve of their initial public offerings.

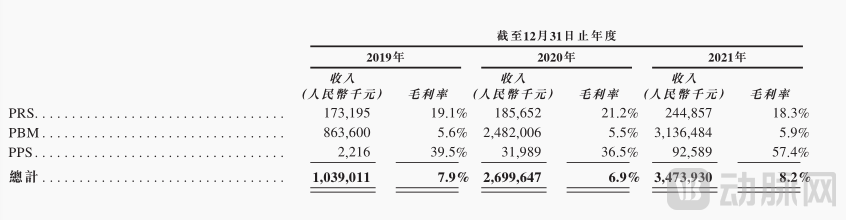

To address the supplementary and upgraded healthcare needs of hundreds of millions of people, Medbanks Health Technology, which recently updated its prospectus, has established three business lines: Physician Research Solutions (PRS), Pharmacy Benefit Management (PBM), and Provider Network and Payer Solutions (PPS). In 2021, its total combined revenue exceeded RMB 3.4 billion.

(Revenue Breakdown by Business Segment of Medbanks Health Technology; Source: Prospectus)

The logic behind the three business lines lies inBy establishing a medical network and medication management system under an integrated health-insurance payment manager, we can create a comprehensive healthcare management network connecting insured individuals, patients, general practitioners and specialists, medical institutions, and health insurance payers, thereby achieving a closed loop of “pharmaceutical, healthcare, and insurance services.”

Specifically,PRS primarily provides Site Management Organization (SMO) services for oncology clinical trials., this business primarily supports the drug development process for clinical trials conducted by pharmaceutical companies. The prospectus reveals that as of December 31, 2021, Medbanks Health Technology’s trial centers, distributed across 86 cities, had cumulatively served 272 clients, including China’s top ten listed pharmaceutical companies engaged in innovative drug research and development.

On the hospital and specialist physician side, Medbanks Health Technology covers more than 2,800 principal investigators and over 425 hospitals across China through its PRS business, including full coverage of 27 provincial-level specialized oncology hospitals and five national cancer treatment centers. Through this business, Medbanks Health Technology has built a network of specialists in major disease areas at key medical institutions across all major healthcare hub cities in China, focusing its development on the supply-side core of healthcare management.

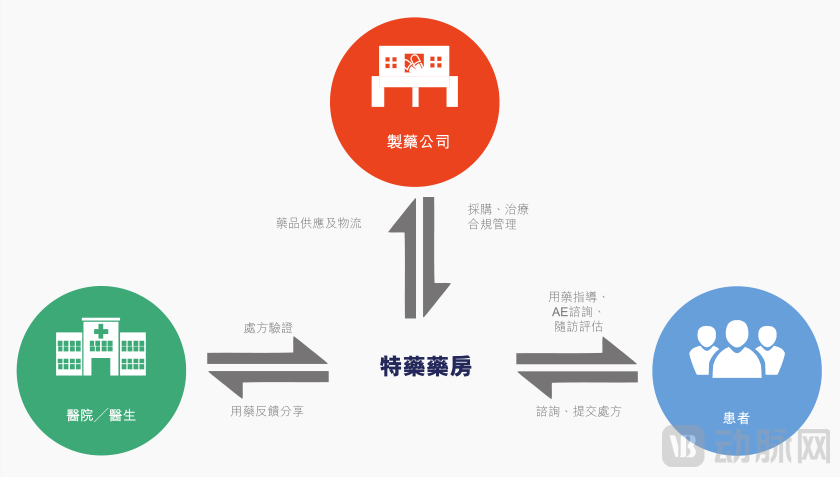

The PBM business line primarily comprises specialty pharmacies and patient-centered value-added pharmacist services., with a core focus on specialty drugs for the treatment of tumors and other critical illnesses. What does this mean? It means that patients can access the most innovative medications currently available through Medbanks Health Technology, along with pharmaceutical care services, including prescription verification, medication guidance, adverse event (AE) consultation, and follow-up assessments.

(Pharmacist-related services; image source: prospectus)

According to the prospectus, as of December 31 last year, Medbanks Health Technology operated 91 specialty drug pharmacies across all provincial-level administrative regions in mainland China, excluding Tibet and Qinghai. These pharmacies specialize in providing prescription medications for cancer and other critical illnesses, offering a wide range of specialty drugs including newly launched innovative therapies, such as the full lineup of PD-1 inhibitors currently approved for commercialization in China. Furthermore, pharmacist services help ensure better medication adherence and therapeutic outcomes for patients after they receive their prescriptions.

Currently, 73 of Medbanks Health Technology’s specialty drug pharmacies have been designated as social insurance-approved pharmacies, accounting for approximately 80% of its total specialty drug pharmacy network. In addition, 42 of these pharmacies have obtained “dual-channel medical insurance qualification” from local healthcare security administrations, enabling patients to seek reimbursement for specialty drugs that were previously reimbursable only when purchased at public hospitals. Furthermore, Medbanks’ specialty drug pharmacies have established direct billing arrangements with major insurance companies, providing patients with additional payment solutions.

Notably, Medbanks Health Technology has not adopted the industry’s prevalent strategy in recent years of rapid expansion and revenue consolidation through mergers and acquisitions. Instead, it has chosen the more challenging but higher-quality approach of building its own specialty drug pharmacies.,This enables the rapid and efficient implementation of pharmacist services and nationwide self-operated network management in accordance with unified standards, resulting in more efficient resource allocation and reduced risks associated with integrated management. This is likely attributable to the strong synergy with Medbanks’ PRS business and its strategy of co-developing around the core supply-side medical resources, namely physicians and hospital networks. Through this business line, Medbanks has further established a nationwide medication management network built upon its existing network of medical experts.

(The Operational Logic of Specialty Pharmacies. Image source: Prospectus)

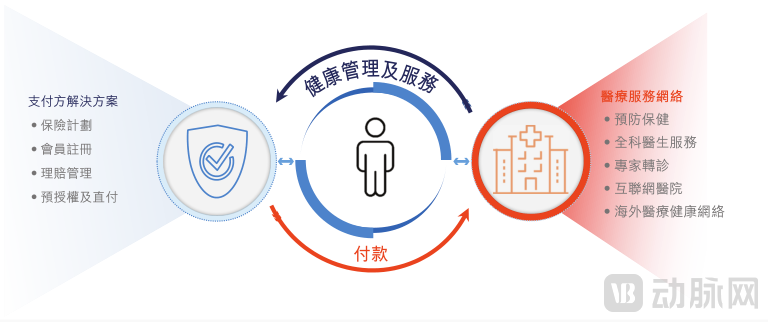

PPS Business, according to the prospectus, Medbanks Health Technology has currently aggregated more than 1,200 Grade A tertiary hospitals, 55,000 physicians, and 500 health examination institutions across over 150 major cities in China, achieving effective integration of medical resources.

(Medical Service Network and Payment Solutions; Source: Prospectus)

Having established its healthcare resource network, including physicians, medical institutions, and drug management services, Medbanks Network Technology has further integrated commercial insurance payment solutions and co-developed differentiated health insurance plans with major insurers.

For example, Medbanks Health Technology has implemented inclusive supplementary medical insurance in multiple regions and launched a new generation of corporate health and medical benefits solution—Medbanks Health Insurance. The product logic of Medbanks Health Insurance is based on a model of proactive management by corporate physicians, completing the commercial insurance closed loop of “incident occurrence–service–claims settlement” within Medbanks’ self-built healthcare system. It rapidly expands its reach across China, helping enterprises accelerate their development through high-quality and efficient medical services.

As a supplement to the national basic medical insurance, Huiminbao provides additional coverage for critical illnesses, medical services, and specialty drugs at prices affordable to the general public. Furthermore, Jiankangbao offers employers and their employees more comprehensive and advanced protection, delivering flexible, high-quality health and disease management services. These products have rapidly gained market recognition. To date, Medbanks Health Technology has served over 14.3 million individual members and 740 corporate clients.

It is evident that by deeply integrating the medical networks, drug management systems, and other frameworks of payment administrators to achieve tangible commercialization, Medbanks Health Technology has developed health insurance products with a genuine foundation in healthcare management. Furthermore, through the differentiated sales of these health insurance products, the company has secured a substantial user base for its aligned medical security system.It is through bidirectional interaction that Medbanks Health Technology has set its business flywheel in motion, enabling the practical operation of the “pharmaceuticals and healthcare” closed loop.

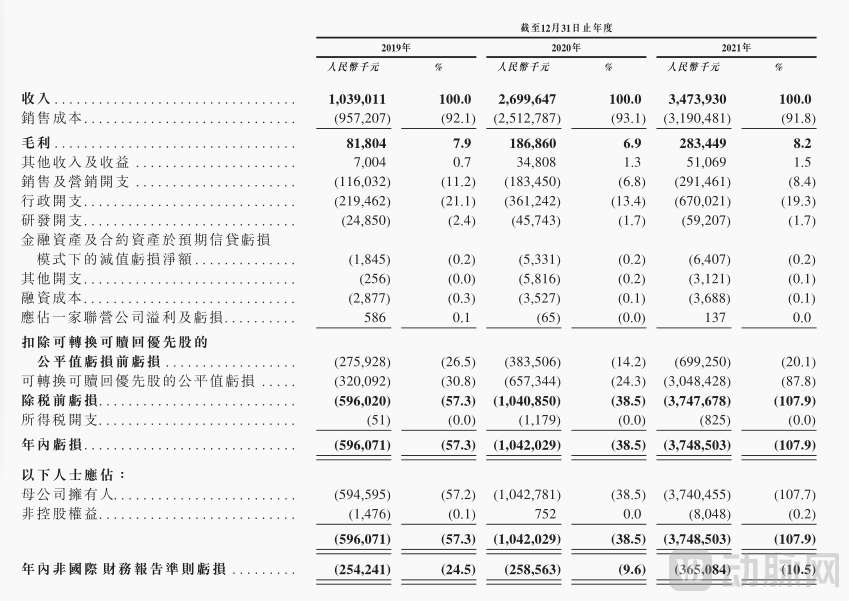

Reflected in the financial statements, over the past three years, Medbanks Health Technology has achieved sustained high-speed organic business growth and expanded into new business lines each year, while maintaining its strategy of self-built infrastructure and robust operations., continuously strengthening the comprehensive health insurance system. Meanwhile, losses incurred from investments during the infrastructure development phase remained moderate.

Taking the Non-IFRS loss—a metric closely monitored by professional Tier 1 and Tier 2 investors, which excludes non-cash gains or losses arising from changes in the valuation of historical preferred shares and share-based option grants—as an example, Medbanks Health Technology reported a loss of RMB 259 million in 2020, a year marked by rapid growth in its PBM segment, and a loss of RMB 365 million in 2021, when its PPS segment experienced rapid expansion.

Given the complexity of building an innovative medical service assurance system by Medbanks Health Technology, and its approximately RMB 1.6 billion in cash and bank wealth management products and other financial assets on its balance sheet at the end of 2021, the overall development appears to be steadily improving with "ample ammunition."

(Specialized Health Technology’s Financial Statements | Source: Prospectus)

China's health insurance industry is entering a phase of rapid development.

From a macro perspective,Since the launch of drug R&D reforms in 2014, the comprehensive elimination of drug markups in public hospitals in 2017, and the establishment of the National Healthcare Security Administration in 2018 to consolidate multi-party medical security responsibilities, China’s new healthcare reforms, centered on the “tri-medical linkage” mechanism, have gradually entered a phase of deep-water challenges.In February 2020, the State Council issued the "Opinions on Deepening the Reform of the Medical Security System," further clarifying the need to accelerate the establishment of a multi-tiered medical security system and promote reforms in payment methods and the supply side of pharmaceutical and healthcare services.

Driven by strong policy support, China’s healthcare delivery, pharmaceutical utilization, and payment systems are accelerating their optimization, moving toward a multi-tiered medical security framework. Markets such as out-of-hospital prescriptions, online diagnosis and treatment, commercial health insurance, and health management have also entered a phase of rapid growth.

In the industrial sector, this is reflected in continuous large-scale financing within the industry, with leading companies such as Medbanks Health Technology actively pursuing initial public offerings (IPOs).However, on the other hand, significant challenges remain to be overcome in establishing a closed-loop ecosystem integrating healthcare, pharmaceuticals, and insurance. These include information asymmetry, high claims ratios, low profitability, and insufficient specialization. Consequently, the industry continues to impose stringent requirements and high expectations on market entrants, placing greater emphasis on innovation and service efficiency in future development.

From an international perspective, Kaiser Permanente and UnitedHealth Group have become the benchmarks for the health insurance industry. Taking UnitedHealth Group as an example, as a constituent of the U.S. S&P 500 Index, it currently generates annual revenue exceeding $240 billion (approximately RMB 1.5 trillion) and has a market capitalization of over $450 billion, undoubtedly serving as a bellwether for health insurance companies.

Looking back on the development path of UnitedHealth, founded in 1974, its core has been prioritizing healthcare service capabilities and continuously driving innovation.For example, in 1988, UnitedHealth pioneered the pharmacy benefit management (PBM) business by linking benefit design with retail pharmacy networks and offering mail-order prescription services. In its subsequent development, UnitedHealth continuously expanded its business boundaries and deepened its medical services. For instance, in insurance product design, it added prescription drug coverage to its existing inpatient medical benefits, which helped it tap into the senior market. It is evident that the key for health insurers to seize emerging trends lies in continuously enhancing their medical service capabilities and pursuing iterative innovation. UnitedHealth emphasizes that it processes over $1 trillion in total medical bills annually and manages more than $250 billion in healthcare expenditures for clients and consumers.

From the perspective of social benefits,The Professional Exploration Path of Health Insurance in the Next 10 Years Will Continue to Focus on Insurance Protection Driven by Medical and Health Management, thereby delivering tangible healthcare management experiences to the general public。This not only aligns with the health service objectives required by “Healthy China 2030,” but also constitutes an indispensable component in achieving “common prosperity in health.”

The road ahead may be long, but time is an effective measure of value: once health insurance companies have earned users’ enduring trust and confidence, they will surely emerge as the true gold amidst the industry’s rigorous selection process.

Under this trend, the health insurance industry is poised to enter a more prosperous and diversified era.