Olympus and Boston Scientific Make Strategic Moves in the $30 Billion Urology Device Market: How Are Chinese Innovators Breaking Through?

By reviewing news from the urology field in recent years, we have observed that global medical device companies are highly active in urology, with frequent mergers and collaborations, approvals of innovative devices, financing, and IPOs.

Taking the recent year 2021 as an example, in May, Olympus completed its acquisition of the Israeli medical device company Medi-Tate,Through this acquisition, Olympus will expand its business line for the treatment of benign prostatic hyperplasia (BPH)., solidifying its leadership position in the field of urological equipment.

In September of the same year, Boston Scientific announced the completion of its $1.07 billion acquisition of Lumenis’ global surgical business, this acquisitionIntegrate its kidney stone management and benign prostatic hyperplasia products with Lumenis’ laser product portfolio, expanding its global footprint and accelerating growth in Europe and Asia.

Almost simultaneously, GE Healthcare announced that it had reached an agreement to acquire BK Medical for $1.45 billion. It is reported that BK Medical has long focused on the research and development of visualization guidance technologies for minimally invasive and robotic surgeries.Especially in achieving visualization of deep tissues during neurosurgery, abdominal surgery, and ultrasound-guided urological procedures. This complementary acquisition will propel GE HealthCare’s ultrasound business from diagnostics into surgery and therapy.

The high level of interest in urological instruments is evident, fundamentally driven by the high prevalence of urological diseases. Propelled by extensive clinical demand, urology, as a equipment-intensive specialty, is witnessing continuous innovation and development in its diagnostic and therapeutic devices. So, what are the recent trends in the development of urological diagnostic and therapeutic devices? How have Chinese companies performed in terms of innovation? VCBeat has conducted a preliminary review of this field.

According to the "2020 In-Depth Research Report on the Global and Chinese Urology Equipment Industry" by New Thinking Industry Research Center, the global urology equipment market is projected to grow from USD 38 billion in 2021 to USD 46.4 billion in 2026, with a compound annual growth rate (CAGR) of 4.1%.

From the perspective of disease categories, common conditions in urology include urinary tract tumors, urinary calculi, urinary tract trauma, genitourinary infections, genitourinary malformations, adrenal disorders, and prostatic diseases. This article primarily focuses on urinary tract tumors, calculi, and prostatic diseases.

1. Urinary System Tumors: The Main Tumor Burden of the Urinary System in China Is on the Rise

Urinary system tumors mainly include renal tumors (such as renal cell carcinoma and Wilms tumor), urothelial carcinoma of the renal pelvis and ureter, bladder cancer, prostate cancer, and urethral cancer.Among these, renal cell carcinoma, bladder cancer, and prostate cancer are the three most common urological malignancies in China, with their incidence rates all showing an upward trend.

According to the latest 2020 global cancer burden data released by the International Agency for Research on Cancer (IARC) of the World Health Organization, among the top ten cancers by incidence worldwide, prostate cancer ranked fourth with 1.41 million cases, and bladder cancer ranked tenth with 570,000 cases.

For Bladder Cancer, according to relevant data, the incidence rate of bladder cancer in China was 5.80 per 100,000 in 2015, ranking 13th among all malignant tumors. Among them, the incidence rate in males was 8.83 per 100,000, ranking 7th; while in females it was 2.61 per 100,000, ranking 17th.For Prostate Cancer, According to IARC statistics and projections, the incidence rate of prostate cancer in China was approximately 15.6 per 100,000 people in 2020, with over 110,000 new cases.For Renal Cell Carcinoma, in 2015, data showed that the incidence of renal cell carcinoma in China was rising at an annual rate of approximately 3%.

Professor Wei Wenqiang, Director of the Cancer Registration Office at the National Cancer Center and the Cancer Hospital of the Chinese Academy of Medical Sciences, stated at the “2022 Beijing Young Urologic Oncology Forum”: “Based on preliminary estimates of cancer patient conditions, there were 710,000 kidney cancer patients, over 650,000 prostate cancer patients, and over 560,000 bladder cancer patients in China in 2020.”

Although the incidence of urologic tumors in China continues to rise, data show that the five-year survival rates for major urologic malignancies have been steadily increasing over the past six years. This progress is attributable, in part, to advances in early diagnosis and screening, as well as improvements in surgical treatment modalities,Particularly innovations in early detection products for urological tumors and laser devices.。

Among these, for early detection products targeting urological tumors, domestic companies such as RenDong Medicine, Hongyuan Biology, Jinxiang Medicine, and Autobio Diagnostics are either developing or have already launched screening products. Research institutions such as Shanghai Jiao Tong University and the Beijing Institute of Genomics, Chinese Academy of Sciences, have also made breakthroughs in this field.

2. Urinary System Stones: Incidence Rate Increasing Year by Year

Urinary calculi are common and frequently occurring conditions in urology, encompassing renal calculi, ureteral calculi, bladder calculi, and urethral calculi. Urinary calculi generally cause obstruction of the kidneys, ureters, bladder, and urethra, and in more severe cases, can lead to renal impairment and failure.

According to relevant data, the incidence of urolithiasis in China is approximately 6%–7%. Among men, the peak age for stone formation is 30–50 years, whereas in women, it occurs during two age ranges: 20–30 years and 40–50 years. Furthermore, the recurrence rate of urolithiasis is as high as 60%–80%. Therefore, the treatment of urinary calculi has two primary objectives: first, to eliminate stones and preserve renal function; second, to address underlying causes and fundamentally prevent stone recurrence.

For treatment, the stone-free rate is one of the important indicators for evaluating the efficacy of urinary tract stone management.The main approaches for stone removal include conservative expulsion, extracorporeal shock wave lithotripsy (ESWL), and stone extraction via percutaneous nephrolithotomy or ureteroscopy.. To reduce the recurrence rate of kidney stones, active patient cooperation is essential, including adopting healthy lifestyle habits, ensuring adequate fluid intake, engaging in regular physical activity, and adhering to a reasonable and scientifically balanced diet.

3. Prostate Diseases: Accounting for Over 60% of Urology Outpatient Visits

Prostatic diseases are common conditions in adult males, primarily including prostatitis, benign prostatic hyperplasia, and prostate cancer.

For Prostatitis, reportedly accounting for approximately 33% of urology outpatients in China,Approximately half of all men will be affected by this condition at some point in their lives.It has a high incidence rate, with male patients under the age of 50 being the most affected. Common symptoms include urinary frequency, urinary urgency, pelvic and sacral pain, and sexual dysfunction.

The primary treatment modalities for prostatitis include pharmacological therapy, physical therapy, and surgical intervention.Surgical treatment is primarily indicated for recurrent chronic bacterial prostatitis. Although transurethral resection of the prostate (TURP) can achieve a cure by removing the prostate gland, it may lead to other adverse effects; therefore, surgical intervention is not the first-line treatment for prostatitis.

For Benign Prostatic Hyperplasia (BPH), which is a common disease among middle-aged and elderly men. According to incomplete statistics, approximately half of men aged 51–60 have benign prostatic hyperplasia (BPH), while 90% of those over the age of 80 are affected by BPH. Based on these figures, it is estimated that there are tens of millions of BPH patients in China. With the accelerating trend of population aging, both the incidence rate and the number of BPH patients continue to rise.

Currently, pharmacological, surgical, and minimally invasive treatments for BPH are all well-established.Among these, surgical treatments mainly include transurethral resection of the prostate (TURP), transurethral incision of the prostate (TUIP), and open prostatectomy.

Transurethral resection of the prostate (TURP) is currently the “gold standard” for the treatment of benign prostatic hyperplasia (BPH). However, with the widespread adoption of enucleation and laser resection techniques in China, the gold-standard status of TURP is being challenged. Internationally, new advancements have also emerged, including urethral dilation using surgical dilators, water ablation, and Rezūm water vapor thermal therapy.Overall, surgical treatment for benign prostatic hyperplasia (BPH) has become more diversified and is trending toward minimally invasive and convenient approaches.

The substantial demand in urology has given rise to a market for related medical devices, driving vigorous industry growth. Concurrently, there is an upgrade in the quality of demand, which translates into higher requirements for equipment. In recent years, urology has been continuously evolving towards minimally invasive and precise approaches, making the development direction of medical devices self-evident:Represented by endoscopes, surgical robots, lasers, and lithotripsy devices,It assists physicians in diagnosis and treatment by enabling clearer identification of lesions and more precise therapeutic interventions.

According to relevant reports, the urology equipment market is segmented into instruments, consumables, and accessories. Among these, the instrument sub-segments—including endoscopes, laser and lithotripsy devices, robotic systems, and urodynamic systems—account for the largest share.

1. Endoscopes & Surgical Robots: A multi-billion-dollar market attracting significant capital interest, with multiple companies entering the field and products sequentially obtaining regulatory approvals

Globally, the proportion of minimally invasive surgery (MIS) dominated by endoscopic diagnosis and treatment is gradually increasing, and the endoscopy market is heating up accordingly.According to data from Evaluate MedTech, the global endoscopy market was valued at USD 20.6 billion in 2017 and is projected to reach USD 26.0 billion by 2021, representing a CAGR of 6.0%. According to data from the China Association of Medical Device Industry, China’s endoscopy market grew from RMB 10.2 billion in 2013 to RMB 22.1 billion in 2018, achieving a CAGR of 16.7%, which exceeds the global growth rate.

Urology is a key department for minimally invasive surgical treatment. Minimally invasive therapies cover nearly all urological conditions, and endoscopes are undoubtedly the cornerstone instruments in minimally invasive urologic surgery.Minimally invasive treatments in urology can be divided into two major categories: one is endoscopic surgery, including cystourethroscopy, ureteroscopy, percutaneous nephroscopy, and seminal vesiculoscopy; the other is laparoscopic surgery, which involves performing procedures through the peritoneal or retroperitoneal cavity using minimally invasive instruments.

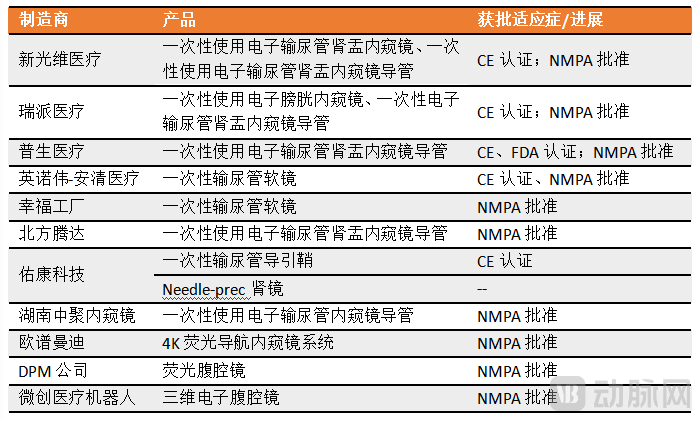

Statistics on Selected Innovative Endoscopic Products Source: VCBeat, Official Website of the National Medical Products Administration, and Publicly Available Online Information

Through a review of endoscopes used in urological procedures, we have found that single-use endoscopes, which can address clinical cross-infection, have become a major highlight in the endoscopy field over the past two years. In terms of service life, turnover frequency, and disinfection difficulty, single-use endoscopes offer significant application advantages in urology. Regarding regulatory approvals, single-use endoscopes in China are currently concentrated in the urological sector.

Secondly, endoscopes, including fluorescence endoscopes and 3D endoscopes, have also seen new developments. These endoscopes are primarily laparoscopes and can be used in urological scenarios; functionally, they are mainly developing towards clearer imaging and more accurate identification of lesions. Currently, domestic companies have layouts in these innovative endoscope fields. And the innovative endoscopes combined with new technologies are precisely the overtaking curve for domestic brands against imported brands.

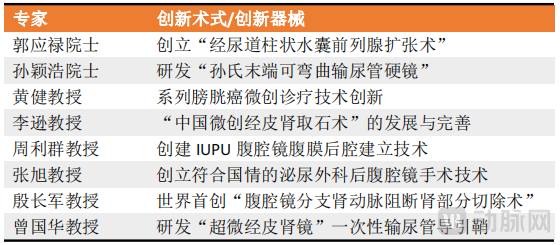

In addition, urology experts in China have innovated numerous endoscopic surgical techniques and instruments in clinical practice, representing Chinese urology on the international stage.

# Incomplete Statistics on Innovations by Chinese Urology ExpertsSource: Compiled from publicly available online information

On the other hand, the most significant trend and hallmark in the evolution of laparoscopic surgery to date is robot-assisted laparoscopic technology, namely, surgical robots.

Surgical robots, with their flexible robotic arms, can avoid issues such as operational blind spots associated with traditional laparoscopic instruments; meanwhile, their precision can reach ten times that of open surgery. Overall, robotic surgery can shorten both operative time and the surgeon’s learning curve.

It is reported that prior to the advent of robotic-assisted laparoscopic surgery, laparoscopic radical prostatectomy required 4–5 hours of operative time, resulted in approximately 400 mL of blood loss, and necessitated a hospital stay of about seven days, with patients being prone to postoperative complications such as urinary incontinence and sexual dysfunction.

Following the adoption of laparoscopic robotic surgery for radical prostatectomy, studies have shown that the mean operative time is only 154 minutes, approximately 96% of patients are discharged within 24 hours postoperatively, and complication rates are significantly reduced.

Endoscopic surgical robots are considered to have the greatest market potential among surgical robots.According to Frost & Sullivan statistics, the global surgical robot market size was approximately USD 8.3 billion in 2020, with the laparoscopic robot market accounting for USD 5.25 billion, representing a 63% share. In China, the national surgical robot market size reached approximately USD 425 million in 2020, of which laparoscopic robots accounted for 75%.

Urological surgery is a classic application of laparoscopic robotic systems, including radical prostatectomy and partial nephrectomy.Judging from the development trajectory of the da Vinci Surgical System, the evolution of laparoscopic robotic surgery has progressed from urology to gynecology and then to general surgery. The successful application in urologic oncology procedures was the critical first step for laparoscopic robots to gain clinical acceptance among physicians and thereby penetrate the market.

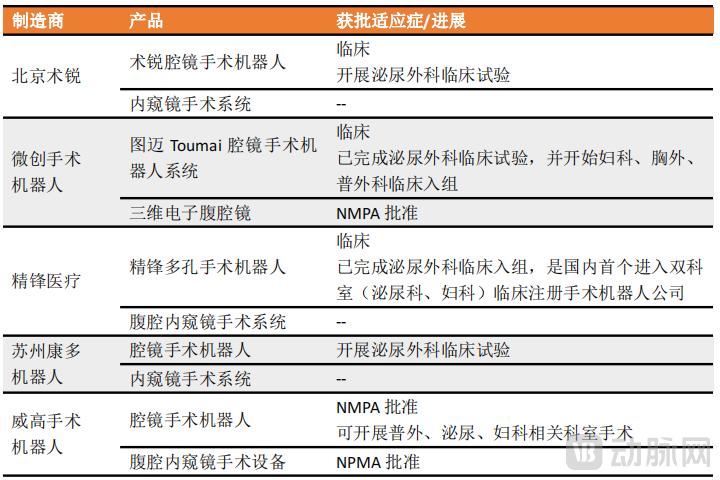

It is reported that multiple laparoscopic surgical robots are currently at various stages in the Chinese market, including regulatory approval and clinical trials.Among them, the approved Weigao surgical robot can be used for surgeries in general surgery, urology, and gynecology departments; multiple robots from MicroPort MedBot, Jingfeng Medical, ShuRui, and Kangduo have also successively initiated clinical trials in urology.

Source: VCBeat, official website of the National Medical Products Administration, and publicly available online information

2. Laser equipment: Applied in multiple fields such as lithotripsy and tissue ablation, with blue laser technology leading globally.

The therapeutic principle of laser treatment is to eliminate lesions by coagulating, vaporizing, or cutting biological tissues through the photothermal and photomechanical effects of laser. According to data from China Industry Information Network in 2017, the market size of China's laser medical device industry was approximately RMB 9.82 billion in 2017, with a compound annual growth rate exceeding 18%. However, compared with countries in Europe and the United States, there is still a certain gap in China's laser medical industry.

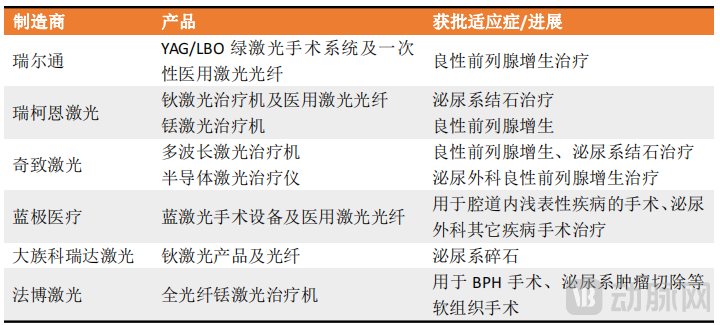

In the field of urology, relevant domestically produced equipment has already been applied, but the enterprises are small in scale.Lasers, as an essential energy platform in endourology, are widely used in the surgical treatment of conditions such as endoscopic lithotripsy, benign prostatic hyperplasia, superficial bladder tumors, and renal cysts.Currently, the lasers commonly used in clinical practice mainly include holmium laser, green laser, and thulium laser.

Source: VCBeat, official website of the National Medical Products Administration, and publicly available online information

Notably, blue laser, a semiconductor laser with a wavelength of 450 nm, warrants mention. Compared with green laser, blue laser offers superior tissue vaporization capability due to its shorter wavelength; compared with holmium and thulium lasers, it demonstrates stronger hemostatic efficacy. Furthermore, blue laser is less demanding regarding the surgical operating environment, thereby expanding the application scenarios for laser surgery.

It is reported that Lanji Medical’s blue laser surgical equipment has recently received approval from the National Medical Products Administration (NMPA), marking this asThe world’s first blue laser surgical energy platform, a globally leading technology。

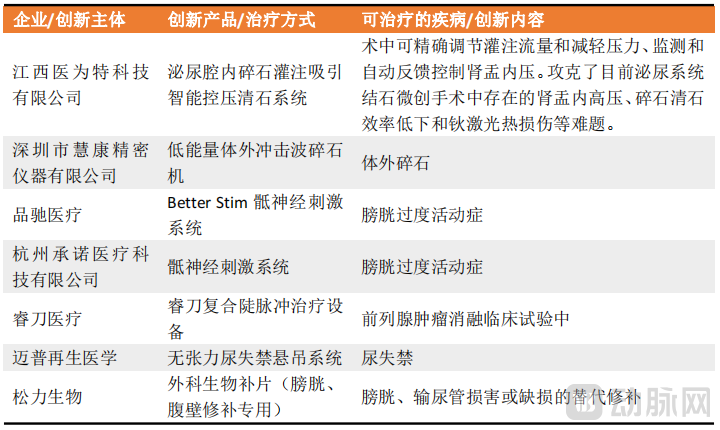

3. Other Devices: Innovation Gains Momentum, but the Product Landscape Remains Fragmented

By reviewing the medical devices that have entered the “Green Channel” for Special Approval of Innovative Medical Devices in China, we found that they include various types of devices such as lithotripsy equipment, neurostimulators, tumor ablation devices, and implants. The following list includes only a subset of these devices.

Source: VCBeat, compiled from publicly available online information

The innovative devices listed in this article represent only the “tip of the iceberg” of device innovation in China’s urology field. Although the information is not comprehensive, it already allows us to glimpse the tremendous creativity embedded in China’s urological devices.

A review of the development of modern urology reveals that revolutionary breakthroughs have been almost entirely driven by advanced innovative devices. For instance, laser technology has enhanced the efficiency of treating benign prostatic hyperplasia and urinary calculi, while the advent of surgical robots has reduced the complexity of intricate procedures while ensuring surgical precision.

From the perspective of modern medicine, urology was introduced to China from the West only in the early 19th century, and we have been striving to catch up with international advancements. As we stand at the cusp of a new wave of medical technological transformation, driven by innovations in imaging diagnostics, robotics, digital technologies, and gene therapy, what further changes await urology as a discipline at the forefront of scientific innovation? Moreover, can China’s healthcare industry gain greater autonomy under the leadership of these emerging technologies?

We will continue to monitor the development of innovative devices in urology. Welcome to exchange ideas.

References:

[1] The Fastest Knife, the Brightest Light, the Most Precise Ruler—Rapid Growth in the Medical Laser Market. Daotong Investment

[2] Dr. Tang Yuzhe. Popular Science | A Few Things About Urology. Medlive Urology

[3] The Development of Endourology: A Perfect Combination of Technology and Art. Surgical Channel, Medical World

[4] Sun Shengkun. Cool-headed Reflections on the Hype Surrounding Urological Technologies. Jingjing

[5] Domestic Substitution: Six Major Innovation Directions Aim to Overtake on the Curve—2021 Endoscopy Innovation Trends Report. VCBeat