Over 30% of Firms Withdraw IPO Filings Amid CSRC's 'Seven Soul-Searching Questions' on STAR Market

The uncertainty surrounding the commercialization of technologies by frontier tech enterprises entails pervasive risks and hard-to-estimate premiums, meaning their development is typically driven only by venture capital firms. However, under China’s previously cautious principles for secondary market access, venture capital firms willing to invest in hard-tech innovation companies struggled to find suitable exit mechanisms, forcing them to seek listings in markets such as Hong Kong and New York. In the absence of adequate domestic exit channels, many high-quality enterprises experienced dilution of their equity to foreign investors.

Under the current circumstances, the STAR Market has paved a new path for institutional investors in hard-tech enterprises, effectively mitigating the outflow of high-tech equity; however, applicant companies will face exceptionally stringent regulatory scrutiny.

Statistical data shows that among the 392 IPO bell-ringing ceremonies to date, 84 were from the life sciences sector. Meanwhile, 150 companies terminated their IPO applications, representing a termination rate of 38.46%. Among these, 32 were healthcare-related companies, with a termination rate of 38.10%.

Among the 31 healthcare companies that terminated their IPOs, a total of 26 withdrew during the inquiry stage, while five failed to pass the review by the Listing Committee. It can be reasonably inferred that the inquiry stage represents the most significant hurdle for companies seeking to list on the STAR Market.

How Do Successfully Listed Companies Achieve Breakthroughs? What Challenges Led to the Unfortunate Termination of Others? VCBeat Analyzed Inquiry Letters Sent to Nearly Half of the Companies Applying for Listing on the STAR Market, Identifying Four Categories Comprising Eight Key Questions.

The term “sci-tech innovation” encompasses two key elements: frontier advancement and innovation. Specifically, companies must hold more than 50 invention patents (including national defense patents) related to their core technologies and main business revenues, and these must constitute core technologies and main business revenues that demonstrate sci-tech innovation attributes. Prospectuses lacking sufficient “sci-tech content” will not be approved by the Shanghai Stock Exchange.

However, accurately measuring the subjective “scientific content” in practice is not easy. Except for a few technologies that can be fairly evaluated by practitioners, more often than not, applicant companies need to find corresponding evidence to prove their claims. In other words, through inquiries about core technologies, it is necessary not only to confirm that the technological positioning meets the requirements but also to analyze the industry and compare domestic and international competitors, using evidence to persuade regulators.

Question 1: Foreign brands have long dominated the market. Do domestic breakthrough players possess proprietary technologies?

With immense potential for import substitution, the pharmaceutical and medical device industry has long been the top priority in healthcare investment. A large number of companies have gone public by meeting either the second set of listing criteria, which focus on “revenue and R&D,” or the fifth set, which emphasize “national standards and clinical requirements.” The most significant commonality between these two sets of criteria is “innovation.”

Medical imaging equipment manufacturer Bestcare submitted its prospectus in March 2019. Its primary revenue source was magnetic resonance (MR) systems, accounting for over 60% of total revenue, with superconducting MR systems contributing approximately 30%. In the prospectus, Bestcare cited its “No. 1 market share in permanent magnet MR systems” as evidence of the company’s leadership and innovation.

However, from the perspective of MRI technology development, although permanent magnet MR systems have low acquisition and maintenance costs, their ultra-high field strength of no more than 0.5T means they can hardly meet the current demands for image quality in precision medicine. Leading companies such as Siemens, GE Healthcare, and Philips have successively abandoned their permanent magnet MR production lines.

Against this backdrop, the Shanghai Stock Exchange (SSE) raised questions three consecutive times regarding the technological leadership of Best Technology, requiring it to provide peer comparisons. In its response to the third round of inquiries, Best Technology acknowledged the risk of declining sales of its permanent magnet-based products and clarified the gap between its proprietary technologies and those of international peers. One month later, the company applied to terminate its listing.

Weigao Orthopaedics, the leading domestic orthopedic medical device manufacturer in China, has encountered similar issues.

Weigao Orthopaedics possesses 14 core technologies across four major segments: spinal, trauma, joint, and sports medicine. However, as companies such as Johnson & Johnson, Medtronic, Stryker, and Sanyou Medical have long maintained industry leadership, the Shanghai Stock Exchange raised questions during the first round of inquiries regarding the distinctiveness of Weigao Orthopaedics’ core technologies.

Brief Question: The Issuer possesses 14 core technologies in the fields of spine, trauma, joints, and sports medicine. Please explain whether industry competitors such as Johnson & Johnson, Medtronic, Stryker, and Sanyou Medical have identical or similar technologies. Compare the data and indicators of the Issuer’s core technologies with those of other technologies to further demonstrate the advanced nature of its core technologies.

In its response, Weigao Orthopedics focused on demonstrating that “all of Weigao Orthopedics’ core technologies are independently developed.” It provided a detailed listing for each category of technology and patent, conducted parameter comparisons between imported and domestically produced manufacturers, and explained the background and usage of each jointly owned patent, thereby presenting evidence that these patents do not involve the issuer’s core technologies.

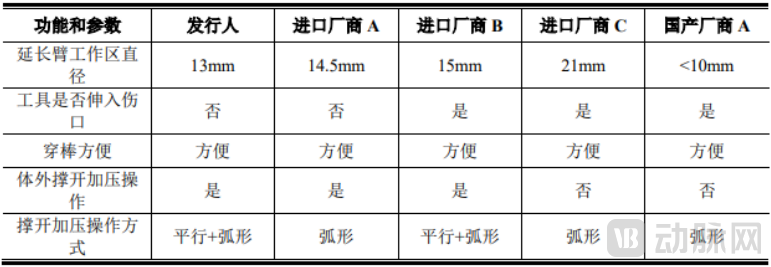

Using a semi-open elastic arm percutaneous minimally invasive technique, Weigao Medical provides the following chart to demonstrate that its related technology has achieved a relatively smaller diameter of the extended arm working zone compared to other imported manufacturers. This not only proves the uniqueness of the technology but also highlights its advanced nature. The remaining 14 technologies are similarly explained one by one using comparable methods.

Comparison of Weigao Orthopaedics’ Semi-Open Elastic Arm Percutaneous Minimally Invasive Technology with Domestic and International Enterprises (Data Source: Shanghai Stock Exchange)

After the first round of inquiries, the Shanghai Stock Exchange did not raise further questions regarding Weigao Orthopaedics’ core technologies in subsequent inquiries. In December 2021, Weigao Orthopaedics successfully went public.

Question 2: The source of core technologies is questionable. Does the company have any intellectual property disputes?

While core technologies are undoubtedly essential, from a regulatory perspective, it is also necessary to consider whether such technology remains firmly under the enterprise’s own control.

Haihao Pharmaceuticals is an innovative oncology drug developer. Ding Jian, a former director of the Institute of Materia Medica and an academician of the Chinese Academy of Sciences, serves as its actual controller. With a strong founder background and the participation of multiple academicians, it was once a rising star heavily favored by venture capital during the era when investors prioritized founders in the innovative drug sector.

With the endorsement of high-caliber R&D personnel, Haihe Pharmaceutical did not attract excessive scrutiny during the inquiry phase—the issues arose at the Listing Committee meeting.

While the impressive backgrounds of its R&D personnel certainly endorse Haihe Pharmaceuticals’ scientific and technological innovation capabilities, the fact that 18 out of its 19 projects are either licensed-in or co-developed—with its pipeline consisting almost entirely of license-in assets—raises concerns about whether the company relies too heavily on third parties, thereby lacking the independent R&D capabilities required for listing on the STAR Market.

At the Listing Committee meeting, the Shanghai Stock Exchange rejected Haihe’s IPO application on the grounds that it “failed to accurately disclose whether it had independently made substantive improvements to its core products introduced through licensing or developed in collaboration, and whether it was technologically dependent on its partners.”

Haihe Pharmaceuticals’ termination has sparked widespread discussion. The prevailing view is that, compared with the innovation-driven license-out model, the license-in “buy-and-buy” approach is unlikely to be well received by the STAR Market.

Similar intellectual property disputes also emerged during the IPO inquiry process of Anhan Technology. Although the subsequent three-year patent litigation concluded with “all of Chongqing Jinshan’s claims being dismissed,” it had a profound impact on Anhan Technology’s IPO progression.

For enterprises, there is no possibility of rectifying such issues in the short term. This means that if a company intends to list on the STAR Market, it must consider developing its core capabilities in-house at an early stage.

Against the backdrop of a shift from profit orientation to market capitalization orientation, the STAR Market does not mandate profitability for applicant companies but imposes stringent requirements on their market capitalization, with business operations being a key factor in sustaining such valuation.

In each round of inquiries, the Shanghai Stock Exchange (SSE) issues detailed requests regarding the company’s core business to verify that it meets the STAR Market’s requirements for technology enterprises and to ensure that its revenue composition is lawful and sustainable, thereby helping investors mitigate potential operational and market risks.

The vast majority of companies applying for listing on the STAR Market possess sufficient substantive merit to meet the regulatory authorities’ data disclosure requirements. The critical questions are whether the sources of corporate data are themselves lawful, and whether such lawfully obtained data can withstand regulatory scrutiny.

Question 3: With competitors being acquired one after another, can niche industries truly achieve industrialization?

Although Tinavi Medical Technologies, a domestic orthopedic surgical robot enterprise, is among the leading players in China, it faces intense competition from overseas orthopedic giants due to the late start of the surgical robot industry in the country. Amidst the monopoly held by these international behemoths, do late entrants have any opportunity to disrupt the market landscape? The Shanghai Stock Exchange has raised the following questions:

Question: According to the prospectus, among the three comparable companies in the same industry, Mazor Robotics was acquired by Medtronic in 2018, Medtech was acquired by Zimmer Biomet in July 2016, and MAKO Surgical was acquired by Stryker in 2013. Please explain: Does the fact that all three comparable companies were acquired indicate that this business segment faces inherent risks in market commercialization? Are there any potential technical defects? Furthermore, in light of the sales performance in the first half of 2019, please clarify whether there are any obstacles to the market promotion and scaled application of the Company’s products.

In its response letter, Tinavi Medical Technologies viewed the acquisition as an endorsement of startups by industry leaders. The company stated that when technologies or products with a certain level of maturity have already emerged in a new field, but international medical giants have not yet developed their own proprietary technologies or products, these giants typically choose to pursue mergers and acquisitions. This strategy allows them to rapidly enter the new sector, achieve technological leapfrogging, and generate synergistic effects by integrating with their established product portfolios, thereby securing monopoly profits. In response to the Shanghai Stock Exchange’s inquiry regarding barriers to scaling, Tinavi directly cited its 25.23% year-on-year revenue growth as evidence.

After up to five rounds of inquiries, Tinavi successfully went public, becoming the first surgical robotics company listed on the STAR Market.

In terms of institutional innovation, the STAR Market has drawn on the U.S. dual-class share structure to establish “special voting rights,” aiming to safeguard the interests of minority shareholders to the greatest extent possible. Nevertheless, many enterprises still retain remnants of VIE (Variable Interest Entity) or red-chip structures when submitting their prospectuses, or present relatively complex equity ownership due to investments by various funds. Therefore, during the inquiry process, the Shanghai Stock Exchange first guides companies to clarify their equity structures and eliminate relevant agreements, ensuring that the equity information in the prospectus is clear and understandable.

In this segment, the Shanghai Stock Exchange adopts a relatively lenient stance toward enterprises. As long as companies can clearly articulate their equity ownership structures, demonstrate the absence of related parties involved in core business operations, and propose viable solutions for any residual structural issues, they typically receive tacit approval from regulators.

Question 4: Can the company successfully go public if the valuation adjustment mechanism (VAM) agreement is urgently terminated?

Valuation Adjustment Mechanism (VAM) agreements are quite common among innovative tech companies going public, but can the STAR Market tolerate listings amid such risks?

IVD industry leader Sansure Biotech entered into a total of four valuation adjustment mechanism (VAM) agreements during its IPO application process, with counterparties including Suzhou Lirui, China Cinda, and Anhui Zhidao, among others. In response to inquiries from the Shanghai Stock Exchange, Sansure Biotech stated that no VAM clauses were triggered during the process.

“The King of Valuation Adjustment Mechanisms (VAMs)”: Besta signed eight VAM agreements over seven years, covering various types such as performance-based and IPO-related VAMs. During its development, Besta provided compensation twice due to failure to meet performance targets, and some agreements remain uncleared.

From the results, Sansure Biotech did not face multiple rounds of inquiries due to the existence of valuation adjustment mechanisms (VAMs) and successfully listed thereafter. In the case of Besta, despite multiple VAM agreements and the emergency termination of certain commitments prior to its IPO, the Shanghai Stock Exchange did not raise further related questions in the second round of inquiries after Besta fully disclosed the details and performance status of each VAM agreement. Therefore, although Besta subsequently withdrew its application, the content of the inquiry letters suggests that its withdrawal was largely unrelated to the VAM agreements.

From this perspective, the Shanghai Stock Exchange does not heavily interfere with the existence of valuation adjustment mechanisms (VAMs). As long as companies fully disclose the associated risks to investors, the presence of such agreements may be considered harmless.

Question 5: Can “Category-3 Shareholders” be recognized by the STAR Market?

“Three-tier shareholder” look-through verification is difficult, easily giving rise to issues such as nominee shareholding and benefit tunneling, which often conflict with the IPO review requirements of “clear equity ownership and stable equity structure.” This has at one point become a mandatory issue that many companies had to address prior to their initial public offerings.

The Shanghai Stock Exchange has adopted a relatively moderate stance toward “three types of shareholders,” gradually shifting from “strict prohibition” to “progressive relaxation.” Nevertheless, it has issued multiple rounds of inquiries regarding the presence of such shareholders in companies like Besta and Sansure Biotech, indicating its preference for companies to eliminate these shareholder structures to the greatest extent possible.

Question to Besta: There are contractual funds among the company’s existing shareholders, with a total of 303 shareholders. Please disclose the transitional arrangements for the “three types of shareholders” and the impact of such matters on the issuer’s ongoing operations.

In response to the aforementioned issues, Besta disclosed details regarding five “Category III shareholders,” indicating that one fund would be converted into a closed-end fund, while the four funds unable to undergo such conversion would cease further capital injections. It further committed that all five funds would exit via secondary market share reductions after the issuer’s listing. Sansure Biotech was also questioned about its Category III shareholders; however, it had already cleared these holdings during its operational period, thereby avoiding follow-up inquiries from the Shanghai Stock Exchange.

During the inquiry phase, approximately 20%-40% of the questions raised by the Shanghai Stock Exchange focused on financial information. Therefore, applying for listing on the STAR Market imposes higher requirements on capital market “gatekeepers,” such as accountants and sponsors.

Nokangda, a pharmaceutical technology enterprise, was one of the two companies subject to on-site supervision by the Shanghai Stock Exchange (SSE) in the early stages of its STAR Market sponsorship business. Due to the failure to disclose RMB 105 million in related-party transactions between Nokangda and Yijia Xinchuang (whose legal representative is the mother-in-law of the issuer’s spouse), Liu Taotao and Deng Jianyong, the sponsoring representatives from Debon Securities, received regulatory warnings for inadequate performance of their duties.

This matter likely had a significant impact on Nuokangda’s journey to list on the STAR Market. Following this round of inquiries, Nuokangda voluntarily terminated its IPO application.

The STAR Market has zero tolerance for financial fraud, fraudulent issuance, and other misconduct. In the financial information section, regulators typically raise the most detailed inquiries. Furthermore, even if a company passes the inquiry stage, its listing application may still be rejected at the Listing Committee meeting if its financial information is not truthful, accurate, and complete. Consequently, investors pay close attention to the sponsor’s strength, as well as the reporting accountant’s reputation in the capital markets, ranking by the Chinese Institute of Certified Public Accountants (CICPA), audit experience in science and technology innovation sectors such as TMT, and capabilities and qualifications in IT auditing.

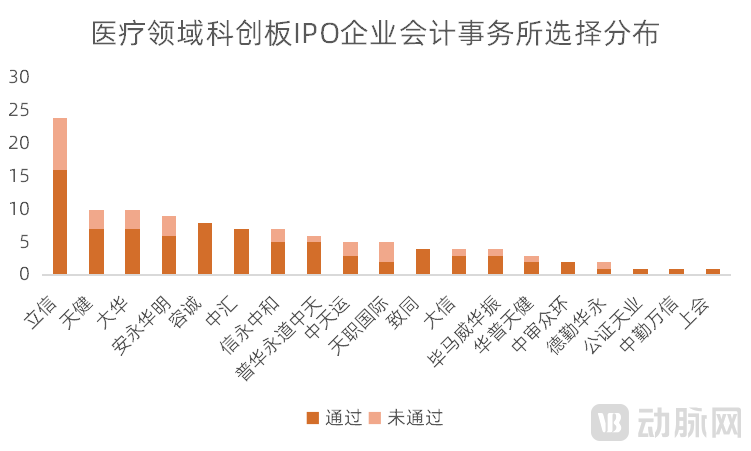

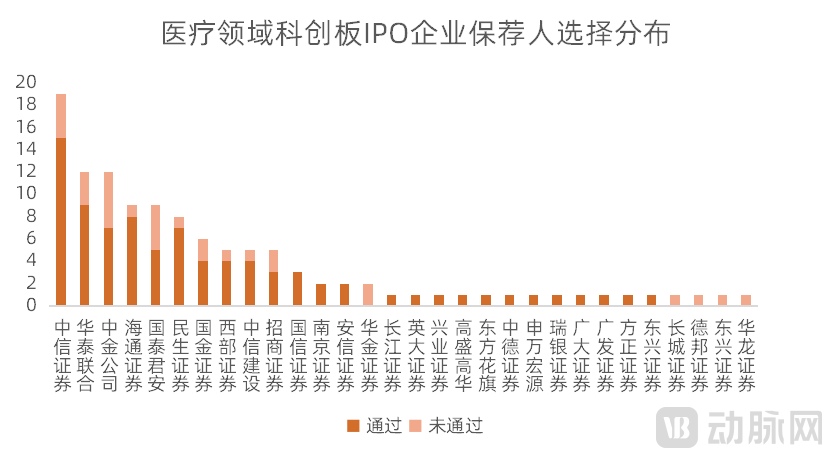

Since the launch of the STAR Market, a total of 112 healthcare companies have submitted prospectuses. The selection of sponsors and accounting firms is shown in the figure above (Data source: VCBeat; Compilation date: March 8, 2022).)

Question 6: Identical revenues but vastly different production capacities—is there a possibility of data fabrication?

Keqian Biology is a company specializing in the research and development, production, sales of veterinary biological products, and technical services for animal disease prevention and control. It was among the first batch of companies to submit its prospectus to the STAR Market. However, after the public disclosure of its prospectus, the company faced media scrutiny due to doubts regarding its production capacity data, major customer data, and gross profit margin. In response to these concerns, the Shanghai Stock Exchange raised the following questions:

Question: During the reporting period, the revenue contributions from the Issuer’s live vaccines and inactivated vaccines were roughly similar, serving as the primary sources of business income. However, a comparison of production capacity reveals that the capacity utilization rate for live vaccines was 98.93% in 2018, whereas that for inactivated vaccines was 65.84%. Please disclose the specific reasons for the significant difference in capacity utilization rates between the two types of vaccines, taking into account factors such as differences in market demand, number of production lines, production capacity, and sales volume.

Regarding this issue, Keqian Biology separates its production capacity for live and inactivated vaccines into poultry and swine categories. In terms of market share, the market sizes for live and inactivated vaccines in the swine sector are similar, whereas the scale of the inactivated vaccine market in the poultry sector is approximately twice that of the swine sector. Therefore, although Keqian Biology has achieved strong sales performance in the swine market (with a capacity utilization rate of 98.93%), it has additionally introduced production lines for poultry inactivated vaccines to further capture market share. As buyers for these newly added production lines have not yet been secured, the capacity utilization rate for inactivated vaccines remains lower than that for live vaccines.

Question 7: What accounts for the difference in gross profit margin compared to industry peers?

Discrepancies in gross profit margins compared to industry peers are a common challenge faced by many enterprises. Gross profit margins that are significantly higher or lower than those of competitors often invite scrutiny. In the previous question, it was noted that Keqian Biology, a vaccine manufacturer, has seen its gross profit margin steadily rise to as high as 80%, whereas Jiahe Meikang, a new listing on the STAR Market specializing in medical IT software, reports a gross profit margin fluctuating around only 40%. In response, the STAR Market raised the following questions.

According to Keqian Biology’s response, the technology behind its innovative veterinary vaccine products remains under patent protection, and only a few enterprises are capable of producing such vaccines. Consequently, driven by patent protection and the gradual expansion of market size, Keqian Biology’s gross profit margin has also increased.

In addressing this question, Jiahe Meikang offered no embellishments, directly citing MediTech’s gross margin data. It frankly stated that hospitals have raised their acceptance standards for electronic medical record (EMR) systems. To enhance implementation quality and meet these hospital acceptance criteria, the company outsourced technical services, resulting in higher costs and a decline in gross margin.

Furthermore, the smart healthcare initiatives newly added from January to March 2020 were also high-cost projects. For instance, the electronic medical record (EMR) project for Hainan Cancer Hospital Co., Ltd. (with a gross margin of -222.64%) and the EMR project for the Department of Psychiatry at Beijing Chaoyang Hospital, Capital Medical University (-5.06%), further dragged down the gross margin. For healthcare IT companies, investment in the implementation of new products is indeed necessary.

Gross Margin Data for Electronic Medical Records of Jiahe Meikang and Maidi Technology (Data Source: STAR Market)

It is worth noting that MediTech has long ranked among the top in gross profit margin across the entire healthcare IT industry. In comparison with its peers, Jiahe Meikang’s gross profit margin is not particularly high. Under such circumstances, the company can address the inquiry by simply providing accurate data.

For enterprises, the STAR Market is a double-edged sword. A successful listing ceremony naturally signifies victory, but a failed one means the company will incur substantial listing costs, face potential funding dilemmas, and suffer public skepticism. Therefore, before applying for an IPO, companies should carefully consider their objectives, timing, and likelihood of success.

From the current requirements of the STAR Market, issues such as scientific and technological innovation attributes and patent status strike at the core of enterprises. These issues cannot be resolved immediately and require time to address. Therefore, if enterprises wish to file an application, it is advisable to define their objectives 1–2 years in advance and begin preparing for these core issues at an early stage.

Incomplete disclosures in the prospectus typically give rise to numerous minor and cumbersome questions during the inquiry phase, which not only increases the workload of reviewers but also extends the number of inquiry rounds from 2–3 to 4–5, resulting in some companies experiencing an inquiry period exceeding one year. In other words, with adequate preparation, the vast majority of issues raised during the STAR Market’s inquiry process can be effectively avoided.

Therefore, given that the current IPO applications on the STAR Market are not yet mature, a reputable sponsor, a competent law firm, and a qualified accounting firm can help companies avoid many pitfalls.