Third-Party Medical Testing Industry at a Crossroads: Internet Giants Enter as Local Players Exit

Third-Party Medical Testing Labs Are Experiencing a Tale of Two Extremes.

On one hand, transfer announcements have been proliferating. After inquiring with familiar listed companies, enthusiastic investors received feedback indicating no current intention to acquire. However, more people expressed resignation and regret, noting, “If the equity had been listed for transfer in early 2021, it might have been quite sought-after.” Of course, there are successful examples of third-party medical laboratories being transferred. For instance, in January 2022, FanZhi Medicine, a rapid genetic testing brand, completed the full acquisition of Kangbien Medical Laboratory, a star third-party medical testing enterprise in Henan Province.

“Most third-party clinical laboratories are probably having a tough time,” an investor told VCBeat.

On the other side, internet giants are deploying their forces in full strength. In December 2021, Shanghai Weihe Medical Laboratory was established, with a business scope covering inspection and testing services, medical services, and medical research and experimental development. Weihe Medical is wholly owned by Xiaohe Health Technology Company, which itself is a wholly-owned subsidiary of ByteDance. In October 2021, Dian Diagnostics and Baidu Health signed a strategic cooperation agreement in Beijing, stating that they would integrate their respective advantageous resources to provide services such as health management, disease diagnosis and management, popular science education on laboratory testing, and appointment-based testing. Earlier, in March of the previous year, Medlinker signed an agreement with KingMed Diagnostics, under which the two parties agreed to carry out comprehensive cooperation in areas such as “Internet + Disease Testing” and “Internet + Disease Management.”

Regional third-party medical testing laboratories are retreating, while internet giants are accelerating their expansion, creating a new watershed moment for the industry. Beneath these divergent strategic moves lie distinct underlying logics, revealing a new competitive landscape within the sector.

Rather than saying that internet giants are accelerating their strategic deployments, it is more accurate to state that third-party clinical laboratories are leveraging the internet to expand their boundaries and achieve a transition from medical diagnostics to healthcare services. Amid the sweeping wave of digitalization, third-party clinical laboratories have long been poised for action.

As early as 2015, KingMed Diagnostics, the largest third-party medical laboratory in China, acquired an internet platform named “Jinzhun.” The aim was to bridge offline and online services through home-based blood collection and testing. At that time, it also launched alcohol gene testing projects on Tmall’s online pharmacy and the GO Health Mall. However, the obvious drawbacks of third-party medical laboratories’ entry into internet healthcare remained unresolved at that time. Specifically, the highly fragmented, passive, and low-frequency nature of medical testing demand made it impossible for a vertical platform to acquire and retain a sufficient number of active users. Consequently, “Jinzhun,” despite its privileged origins, failed to truly lead third-party medical laboratories into the realm of internet healthcare.

Third-party clinical laboratories still needed to wait for the right moment to tap into online traffic, and the COVID-19 pandemic provided precisely that opportunity.

During this period, two critical market pain points emerged that urgently needed to be addressed. First, COVID-19 testing directly designated third-party medical laboratories as authorized facilities, bringing these healthcare service providers from behind the scenes to the forefront and marking their first step in transitioning from pure medical science to broader healthcare services. Second, under physical isolation measures, the demand for frequent medical testing among certain patient groups was forced to shift from within hospitals to outside settings, including patients with chronic diseases, pregnant and postpartum women, and ordinary individuals with travel needs.

Over the past two years, third-party medical laboratories have been the mainstay of COVID-19 nucleic acid screening. For instance, in 2020, nearly 80% of nucleic acid tests in Wuhan were conducted by third-party medical laboratories. In mid-February, when the National Health Commission released the first list of qualified third-party institutions for novel coronavirus nucleic acid testing, it explicitly pointed out that third-party testing agencies are an important component of China’s provision of novel coronavirus nucleic acid testing services, and their role in mitigating the disruption of nucleic acid testing to the normal operations of medical institutions was once again recognized. As a result, these third-party medical laboratories have capitalized on the surge in COVID-19 testing demand, successfully tapping into the traffic flows of internet healthcare.

Following this, several leading third-party medical testing laboratories began to expand their engagement with internet healthcare.

For instance, in May 2020, Dian Diagnostics launched “Xiao Fei Jian,” a third-party online internet-based testing platform directly targeting consumer-end (C-end) users. Positioned as the company’s future third growth engine, it has received substantial resource allocation. Within less than two years, the platform established nearly 500 offline blood collection sites, migrated all of Dian Diagnostics’ laboratory offerings—comprising more than 2,700 test items—to the online environment, and acquired traffic through partnerships with major internet platforms such as Baidu, Tencent, Alibaba, and JD.com.

Currently, there are two main types of online engagement by third-party medical laboratories: medical science popularization and specialized disease management. From the perspective of internet healthcare, these approaches may appear somewhat nascent, yet they remain relatively feasible.

Let us first examine medical science popularization. For instance, the collaboration between Youlai Doctor and KingMed Diagnostics is primarily content-driven. This is easy to understand: on one hand, public awareness of clinical laboratory tests in the consumer market remains very low. Regarding these complex testing items, most people’s knowledge extends only to practical matters such as which type of sample needs to be collected and whether fasting is required. However, the correlations between various test indicators and specific diseases remain a significant knowledge gap. In reality, as public awareness of health management grows, it becomes essential to bridge this cognitive divide. The internet serves as a highly convenient channel for doing so, and experienced third-party clinical laboratories are undoubtedly high-quality producers of professional content. Therefore, it is not surprising that their focus lies on medical science popularization.

On the other hand, although internet healthcare platforms can already provide closed-loop medical services spanning from consultation to medication, the diagnostic component has always been missing. The integration of third-party medical laboratory testing content and services undoubtedly completes the business chain. According to reports, Youlai Doctor will collaborate with KingMed Diagnostics to co-establish China’s first authoritative popular science knowledge base in the field of medical laboratory testing. This initiative aims to deliver professional educational content on medical laboratory testing through short videos, covering areas such as hematological diseases, solid tumors, gynecological conditions, and perinatal and pediatric medicine.

Next is specialized disease management. As mentioned earlier, Dian Diagnostics has moved more than 2,700 medical laboratory tests online through its Xiao Fei Jian platform. On this platform, these test items are no longer organized by traditional laboratory categories; instead, they are grouped into dedicated sections such as Women’s Health, Parental Care, and Pediatric Care, with each section offering a variety of specialized tests or bundled packages.

From laboratory classification to specialized disease management is, in fact, the inevitable path for third-party medical laboratories to expand from business-to-business (B2B) services to direct-to-consumer (C2C) offerings. However, bridging this transition requires overcoming a significant gap in clinical knowledge and experience. This challenge may explain why most third-party medical laboratories choose to partner with internet healthcare platforms to deepen their expertise in specific specialties. For instance, in March 2021, Medlinker signed an agreement with KingMed Diagnostics to jointly develop a cloud-based integrated testing service solution for chronic disease management. This collaboration covers more than 70 conditions across areas such as the detection and treatment of infectious diseases, fertility and reproductive health, and cancer screening and prevention, reflecting the complementary strengths of both parties.

Leveraging the substantial traffic from internet healthcare platforms, the market penetration rate of third-party medical testing in China is expected to surpass single digits. However, for both third-party medical laboratories and internet healthcare platforms, the impact of medical science popularization and specialized disease management remains relatively limited at this stage. For third-party medical laboratories, the more pressing priority continues to be strengthening endogenous drivers of business growth.

Having discussed the aggressive expansion of internet giants, let us now briefly analyze the reasons behind the widespread closures and business transformations of regional medical testing laboratories.

As previously mentioned, third-party medical laboratories played a significant role in COVID-19 testing. This business sector has relatively low technical barriers, attracting many individuals with prior experience in third-party medical testing or IVD reagent distribution. Meanwhile, some larger third-party medical laboratory brands in the market have accelerated their chain expansion. For instance, Hybribio and Qianmai Medical have significantly increased the number of their affiliated third-party medical laboratories.

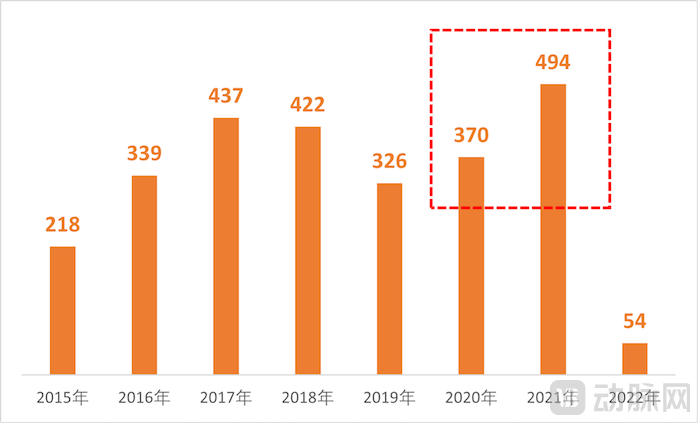

Data from Qichacha shows that the number of enterprises registered to provide independent medical laboratory services has seen a significant increase since 2020. Prior to this, the existing stock of third-party clinical laboratories had already begun to decline. As the timeframe for mass screening continued to compress, it was precisely this testing network—comprising large tertiary hospitals, provincial and municipal centers for disease control and prevention, third-party clinical laboratories, and mobile facilities—that demonstrated remarkable resilience. However, it also fostered a certain degree of market bubble, laying the groundwork for the current wave of transfers and acquisitions.

Number of Third-Party Medical Laboratories from 2015 to Present (Data Source: Qichacha)

Yet, third-party medical testing laboratories rose and fell with COVID-19 testing. On one hand, as timelines for mass screening grew increasingly tight, these labs were often forced to mobilize personnel, funding, and resources exclusively for COVID-19 testing upon receiving requests. This strained their routine testing capacity and disrupted internal operational rhythms. On the other hand, the unit price of COVID-19 nucleic acid testing was repeatedly slashed from over 100 yuan to below 10 yuan. From a profitability perspective, this once-booming business has shifted from a profit center to a cost center. Furthermore, cash flow from COVID-19-related services typically turned over more slowly than that from purely commercial testing services. Consequently, some third-party medical testing laboratories established specifically for COVID-19 testing have been compelled to cease operations to cut losses.

In a sense, the third-party clinical laboratory testing market is one where the strong grow stronger.

Third-party medical laboratories are, in essence, outsourced service providers for hospitals’ clinical testing needs. Beginning in the 1990s, pressure to control healthcare costs led hospitals to outsource medical testing services and manage them through centralized operations, giving rise to third-party medical laboratories. Initially, these entities were no different from other external service providers, engaging in asset-heavy, low-margin service businesses. Typically, third-party medical laboratories receive samples from hospitals, with volumes dependent on the test orders prescribed by physicians for patients. On the payment side, patients pay the hospital directly; approximately 40–60% of the testing fees constitute revenue for the hospital’s clinical laboratory department, while the remainder is used to compensate the third-party medical laboratory. Through this arrangement, hospitals can meet their medical testing needs at a lower cost than if they performed the tests in-house, thereby enabling the third-party medical testing market to achieve scale. Once a head-effect (market concentration among leading players) takes hold, it becomes significantly difficult for new entrants to break into the market.

On one hand, the market size is limited and competition is intense. The reason third-party medical laboratories are more cost-effective than in-house hospital testing lies in economies of scale. In other words, hospitals’ willingness to outsource medical testing services decreases as the volume of samples collected from their outpatient and inpatient populations grows. Previous data show that among users of third-party medical laboratories, primary public hospitals have the highest market penetration rate at around 10%, followed by secondary public hospitals, which account for approximately 8% of patient samples, while tertiary public hospitals have the lowest penetration rate at only about 3%. However, domestic patients are most concentrated in tertiary public hospitals, which serve over 40% of all patients. From this perspective, the ceiling for the routine testing market of third-party medical laboratories is indeed not high.

The general testing market in primary and secondary public hospitals has long become a red ocean. Within the aforementioned business and capital flows, clinicians and hospitals wield absolute bargaining power in the industry chain, leaving third-party medical laboratories in a relatively passive position. Even so, this relatively stable business continues to attract a large number of competitors. For most test items, third-party medical laboratories exhibit high homogeneity in technical pathways, pricing strategies, and service quality; as a result, intense market competition is increasingly converging on product portfolio breadth and channel resources.

Currently, this situation may be beginning to ease. In a recently leaked interview transcript, KingMed Diagnostics stated that as tertiary hospitals face increasing pressure from Diagnosis-Related Groups (DRG) payment reforms, they have started to consider the comprehensive outsourcing of laboratory services. The company further indicated that it would promptly issue an announcement once substantive progress is made in this area. If this assessment proves accurate, it would mean that third-party medical laboratories are poised to accelerate their penetration into the tertiary public hospital market—a segment where they have historically been least competitive—though this will clearly require sustained, long-term effort.

On the other hand, it is difficult for new entrants to find a foothold. Although many highly innovative specialized testing companies have attempted to establish a presence over the years, only a handful have managed to survive.

First, the logic of specialized testing contradicts the economies of scale characteristic of third-party medical laboratories. Compared with in-house hospital laboratories, third-party medical labs possess inherent advantages in specialized testing. Typically, when researchers or pharmaceutical companies identify that a certain biomarker is strongly associated with disease diagnosis or response to a specific class of drugs, but the "Catalogue of Clinical Laboratory Tests for Medical Institutions" has not yet included it, the corresponding test cannot be performed within hospitals. Consequently, early implementation of such testing must rely on third-party medical laboratories.

In third-party clinical laboratories, large volumes of samples are repeatedly used to validate new discoveries. As a result, diagnostic reagents, instruments, and consumables become standardized, evolving into clinically approved medical devices, and the corresponding assays emerge as new categories of routine testing. With low barriers to entry in the third-party clinical laboratory sector, once specialized testing products are finalized, new entrants quickly emerge to erode excess profits. The fierce competition observed in markets ranging from non-invasive prenatal testing (NIPT) to tumor genetic testing serves as a typical example. Ultimately, the market cannot sustain so many large companies; therefore, the most likely outcome is that existing giants will remain dominant as before, while a large number of new entrants will remain stuck in a state of stagnant growth over the long term.

Secondly, specialized testing enterprises often lack the conditions and willingness to scale up.

On the one hand, objectively speaking, companies developing specialized diagnostic tests are typically biotechnology firms, such as the genetic testing companies that first commercialized NIPT and tumor NGS. For them, establishing and operating a medical laboratory is a relatively uneconomical option among many choices. In terms of personnel, heads of medical laboratories are required to hold a deputy senior professional title, and laboratory staff must possess PCR certification; in contrast, management and operational staff at biotechnology companies face no such requirements, needing only a background in biological sciences. Regarding instruments, the clinical-grade versions of the same equipment mandated for medical laboratories cost 30% more than their research-grade counterparts. The same applies to reagents and consumables. Furthermore, maintaining quality control systems and managing medical waste disposal also require substantial investments of time and financial resources.

On the other hand, in terms of subjective intent, for most biotechnology companies, the purpose of establishing third-party medical laboratories is to help complete clinical validation of their specialized testing products, thereby obtaining qualifications for in vitro diagnostic (IVD) products. Their business model naturally centers on the IVD model, with subsequent operational focus placed on the construction and expansion of GMP-compliant manufacturing facilities, building clinical medical teams, and securing hospital access channels, rather than scaling up third-party medical laboratory services, which serve merely as supporting infrastructure. For instance, the third-party medical laboratory under ByteDance is highly likely intended to provide clinical trial support for new drug development, rather than directly competing with leading general testing providers for a limited market share.

Against this backdrop, how leading third-party medical testing companies, which have primarily focused on routine testing, take up the baton for specialized testing will likely be a key consideration in breaking through their future growth ceilings. In short, while some bubbles are bursting among third-party medical laboratories currently in the spotlight, those that embrace medical testing innovations upstream and integrate with internet traffic downstream will naturally see their growth ceilings rise to new heights.