WeDoctor's HMO Ecosystem Takes Shape with City, Community, Enterprise, and Specialty Models: China's Answer to UnitedHealth Goes Public

In recent years, digital Health Maintenance Organizations (HMOs) have become a focal point of discussion within China’s insurance and healthcare industries. Behind this industry fervor lies the meteoric rise of UnitedHealth Group, the “pioneer benchmark” across the Pacific, in the capital markets. Meanwhile, in China, practical efforts to implement HMO models are blossoming everywhere.

Currently, digitalization-supported HMOs can more efficiently integrate and allocate various elements across the medical industry chain, leveraging limited medical resources to cover a larger user base. This approach helps reduce healthcare costs and minimize the waste of medical resources, while also connecting all stages of healthcare delivery to truly establish a closed-loop system for the entire healthcare service process.

So, what series of impacts will digital HMOs bring to the industry? In fact, some regions and industry players have already been actively exploring the construction of a “Chinese-style HMO” and have achieved remarkable results. By comparing the practices of typical enterprises both domestically and internationally, it is evident that the development path of Chinese-style HMOs has gradually become clear, harboring significant commercial potential along the way.

An analysis of UnitedHealth Group’s profit model reveals that its health services revenue is rapidly catching up with the revenue from its traditional health insurance business.

Based on UnitedHealth Group’s financial reports in recent years, the growth of its health insurance business has slowed significantly. Leveraging technology to enable more effective health management and control health insurance premiums will remain the consistent strategic direction for the health insurance segment.

In contrast, the health services segment has demonstrated a significantly higher overall growth rate than the health insurance business. In 2020, the revenue ratio between its medical services and health insurance businesses approached 4:6, indicating a further narrowing of the gap. This trend suggests that its medical services business has gained market recognition and is generating substantial revenue. Notably, its OptumHealth and OptumRx businesses are poised to become the primary engines driving UnitedHealth Group’s future growth.

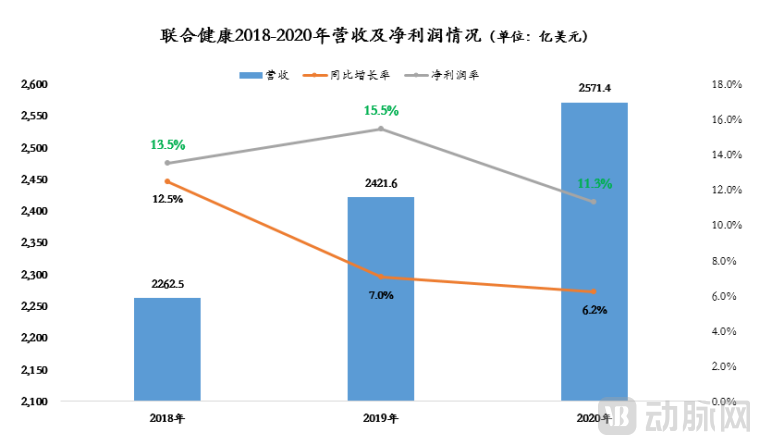

It is evident that the digitalization of healthcare services represents the future direction for the development of the entire healthcare industry. Data shows that from 2018 to 2020, UnitedHealth Group’s revenue and net profit continued to grow, with a compound annual growth rate (CAGR) of 6.6% for revenue and an average net profit margin of 13.4%. In the latest fiscal year 2021, the company’s total revenue reached $287.597 billion, a year-on-year increase of 11.8%; net profit attributable to common shareholders was $17.285 billion, up 12.2% year on year. This demonstrates that integrating “medical care + pharmaceuticals + insurance + digitalization” can significantly enhance a company’s revenue growth potential.

In contrast, within the domestic market, the dual-circulation strategy has created opportunities for the rise of a Chinese “UnitedHealth” amid the booming domestic healthcare market.Nicolas Aguzin, Executive Director and Group Chief Executive Officer of the Hong Kong Stock Exchange, has stated that China’s healthcare market presents substantial business opportunities. Currently, China’s total healthcare expenditure stands at approximately $1 trillion, accounting for 10% of the global market, and continues to experience rapid growth. He projects that China’s healthcare spending will reach $3 trillion over the next decade.

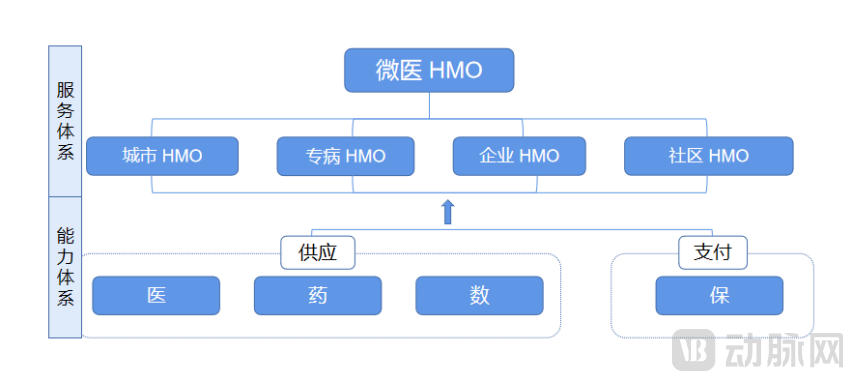

During this critical period of significant opportunity for industry development, WeDoctor, China’s largest digital health platform, has also undertaken strategic and organizational upgrades across its business segments. By integrating its various business units, capability modules, and regional operations, the company has established four core business hubs centered on “healthcare, pharmaceuticals, insurance, and data.” This restructuring enables greater business focus, more refined organizational management, and enhanced synergistic efficiency among its divisions.

Source: Caijing Health

Leveraging these four core capabilities, WeDoctor has implemented “Urban HMOs” across China, organized as tightly integrated medical consortia and primarily funded through bundled payments from basic medical insurance; it has also explored “Specialty Disease HMOs” with a focus on chronic disease management, adopting condition-based or capitation-based bundled payment models; furthermore, it has established “Community HMOs” and “Enterprise HMOs” that provide online-offline integrated digital healthcare and health maintenance services to community residents and corporate employees. These diverse forms of Health Maintenance Organizations effectively improve users’ health indicators and curb the growth rate of medical expenditures.

Image source: Compiled from publicly available online information

According to media reports, WeDoctor recently launched the “Regional Digital Health Community Partner Recruitment Plan” to seek partners across China. This signifies that WeDoctor is opening up its core standardized capabilities in the expansion, construction, and basic operations of its health communities, shifting from a previous “direct-operation” model to a “joint-operation” model. It is evident that the standardized capabilities established on the payer and supply sides enable it to select third-party partners for joint operations tailored to local conditions when implementing HMOs in various medical insurance pooling regions. Through expansion and operation via a “partnership” model leveraging capital, resources, and talent, this relatively asset-light approach will accelerate the replication and implementation of different types of HMOs, including “City HMOs,” “Disease-Specific HMOs,” “Community HMOs,” and “Enterprise HMOs.”

Public data shows that WeDoctor’s revenues from 2018 to 2020 were RMB 255 million, RMB 506 million, and RMB 1.832 billion, respectively, representing a compound annual growth rate (CAGR) of 168%. In 2020, revenue from medical services amounted to RMB 706 million, accounting for 38.6%, while revenue from health management services reached RMB 1.125 billion, accounting for 61.4%. This growth trajectory reflects the typical development pattern of digital companies undergoing industrial transformation: substantial upfront infrastructure investments and long payback periods in the early stages, followed by high growth potential in later stages.

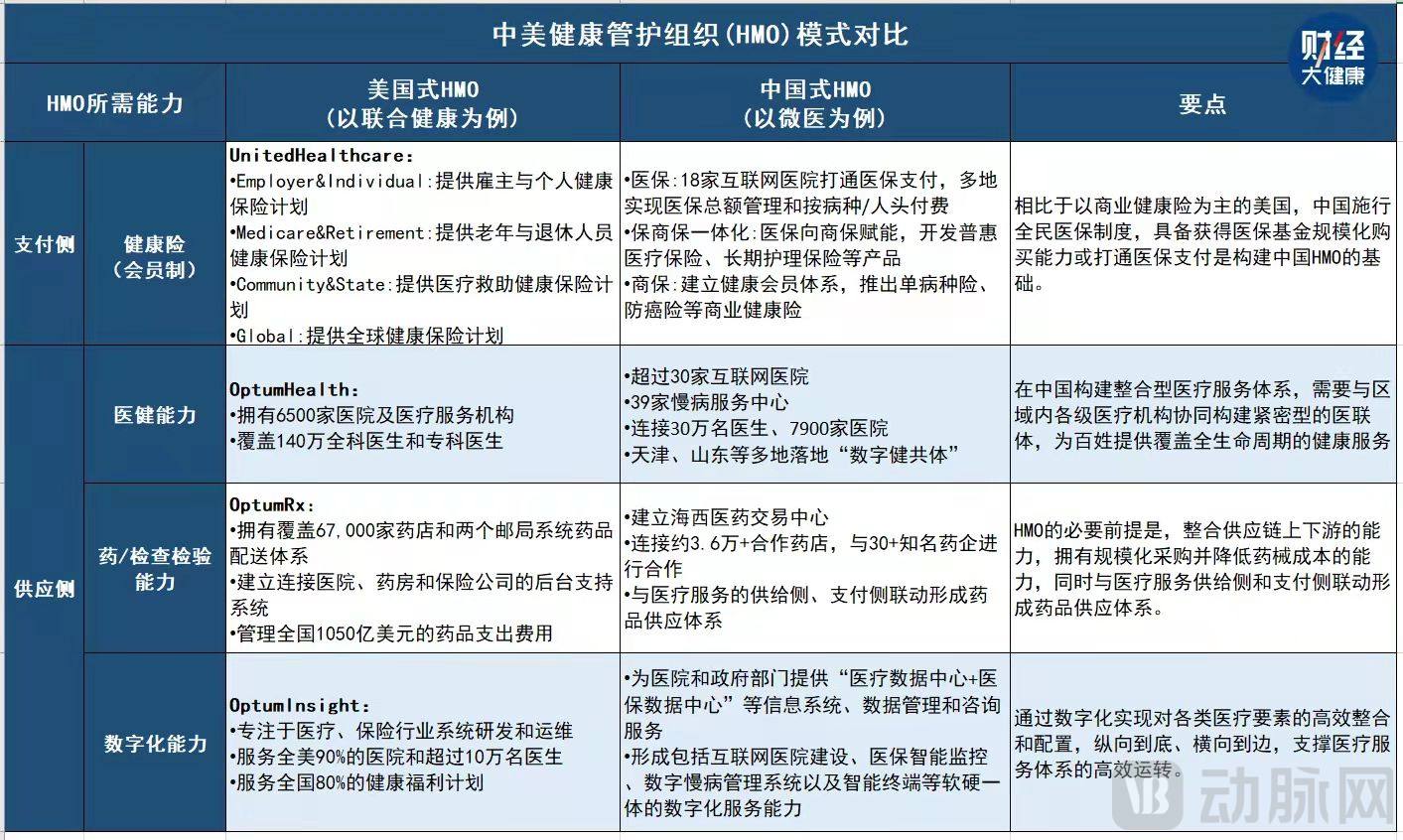

It is worth noting that within the “healthcare + pharmaceuticals + insurance + digitalization” capability model, “healthcare” possesses the strongest barrier to entry.An examination of UnitedHealth Group’s development trajectory reveals that, at its inception, the company actively acquired Health Maintenance Organizations (HMOs) and health plans to rapidly expand its service network and accumulate medical resources with high entry barriers. This strategy naturally attracted a large customer base to join its service ecosystem as “members,” enabling rapid market expansion. Subsequently, the company intensified its acquisition of health insurance firms and vigorously developed its group insurance business, thereby perfecting its payer-side business layout. Similarly, WeDoctor focuses primarily on serious medical care, providing medical services and health maintenance solutions rather than operating as a “pharmaceutical e-commerce” platform. By the end of 2021, WeDoctor had connected with more than 7,900 hospitals, covering over 80% of tertiary hospitals and more than 95% of Grade A tertiary hospitals across China. Among the 300,000 connected physicians, 57% held the title of associate chief physician or higher, and 86% held the title of attending physician or higher.

Observations of cutting-edge exploratory practices both domestically and internationally reveal that digital HMOs not only comprehensively enhance the accessibility, effectiveness, and affordability of healthcare services, but also chart a course for the high-quality development of the entire healthcare industry. Against the backdrop of an accelerating reform in the “payment + supply” system of healthcare services, the development of Chinese-style HMOs in 2022 is creating greater growth opportunities for the industry.