Two Weeks After China's Antigen Testing Market Opened: A Stress Test for Domestic Brands

The First Shoe Drops for COVID-19 Antigen Testing. The release of centralized procurement results from Shandong’s special program and the Tianjin-Hebei region, among others, has pushed average winning bids into a more reasonable range, intensifying market competition overnight.

Over the past two weeks, developments in COVID-19 antigen testing have accelerated dramatically, resulting in an information explosion. On the very evening when the National Health Commission released the “Trial Implementation Plan for the Application of COVID-19 Antigen Testing” (hereinafter referred to as the “Application Plan”), significantly expanding the prospects for domestic COVID-19 antigen testing and home-based self-testing, Vazyme’s COVID-19 antigen self-test kit received approval for market launch. Meanwhile, the National Medical Products Administration expedited the review and approval of change applications submitted by four companies—Beijing Jinwofu, BGI Genomics, Wondfo Biotech, and Beijing Huaketai—that had previously obtained qualifications for professional-use tests. By the early morning of the following day, a total of five COVID-19 antigen self-test kits had been approved for market launch in China, marking the first batch in the country.

Almost simultaneously, major brands have established strategic partnerships with online and offline channel networks such as Dashenlin, Laobaixing, JD Health, Baidu Health, and Suning.com. With the starting gun for sales imminent, it is evident that these companies are well-prepared and amply resourced. A day later, five companies—Wantai Bio, Hotgen Biotech, Boao Saisi, Mingdao Jiece, and Lepu Diagnostic—also obtained registration approval from the National Medical Products Administration (NMPA) for their COVID-19 antigen self-test kits. The industry giants have surged ahead; in just one weekend, the COVID-19 antigen testing market has shifted from a battle for market access to a competition centered on products and even distribution channels.

Subsequently, active players in overseas markets such as Mindray Diagnostics, Orient Gene, ACON Biotech, Zhongyuan Huiji, Odle Bio, Kanghua Biology, AllTest Biotech, YHLO, and Yirex successively obtained approvals from the National Medical Products Administration (NMPA) for COVID-19 antigen self-test kits. With industry giants circling and 19 product registration certificates already issued, competition was poised to erupt. (Statistics as of March 23, 2022)

As provinces intensified their centralized procurement efforts, the competition among industry giants reached a fever pitch. On March 15, Guangdong, Henan, and Shandong successively issued notices on implementation plans for the centralized procurement of COVID-19 antigen testing reagents, explicitly launching bulk purchasing for these products. By the evening of March 16, Shandong had finalized its special centralized procurement round for COVID-19 antigen testing reagents, with BGI Genomics, Wantai BioPharm, Medsun Biotech, Orient Gene, and Boao Saishi among the first batch included in the government’s procurement list. On March 20, the Tianjin Medical Procurement Center also announced the initial listed prices for COVID-19 antigen testing reagents in Tianjin and Hebei, with 15 companies selected. One day later, the National Healthcare Security Administration officially issued a document requiring all provinces to temporarily include COVID-19 antigen testing in their basic medical insurance catalogs.

In the blink of an eye, China’s COVID-19 antigen testing industry has grown from scratch to prominence, with its late-mover advantages fully demonstrated across brand vitality, regulatory frameworks, and channel development.

Amid the global frenzy for the hottest medical products, domestic users’ enthusiasm has surged to unexpectedly high levels.

The implementation of COVID-19 antigen testing progressed rapidly. As early as March 13 this year, students and faculty at Jilin University, who were confined due to the pandemic, became the first batch of users of domestic self-test kits for COVID-19 antigens. This initial consignment, totaling 12 million test kits, was procured without delay by the Department of Industry and Information Technology of Jilin Province and distributed free of charge by volunteers to the first group of end-users, reflecting a tangible and urgent demand.

In community-based application scenarios, the rollout of COVID-19 antigen testing has been somewhat slow, yet consumer enthusiasm for trying out this new technology continues to surge.

Media visits have revealed that, due to restrictions on sales qualifications and procurement and delivery cycles, most offline pharmacies can only accept pre-orders for COVID-19 antigen self-test kits, with uncertain arrival times. These products, retailing at around 30 yuan each, are highly sought after by consumers. “Order volumes have been substantial since the 14th, with many people directly purchasing 50 boxes,” said a pharmacy staff member. At another pharmacy, more than 10 WeChat groups have been created for customers who reserved COVID-19 antigen test kits from brands such as Jinwoofu and Wondfo after providing their identity information.

COVID-19 Antigen Self-Test Kits Also See Surging Demand on E-commerce PlatformsSince March 14, major e-commerce platforms such as JD.com, Tmall, and Suning.com have successively launched pre-sales for the first batch of COVID-19 antigen test kits. According to media reports, within just a few days, monthly sales of COVID-19 antigen self-test kits at nearly all online pharmacies offering them exceeded 5,000 units, with most products sold in bulk packs of 20–30 tests per box. “The products have only just been launched, and many merchants are still in the pre-sale phase, resulting in extremely tight inventory,” the media outlet confirmed with customer service representatives, underscoring the high demand for COVID-19 antigen self-test kits.

Behind this consumption boom lies the vast potential market for COVID-19 antigen testing. Research suggests that, from a long-term perspective, the market size for COVID-19 antigen tests could exceed RMB 100 billion, encompassing both the static market formed by at-home self-testing and the dynamic market generated by large-scale COVID-19 screening initiatives.

In fact, the promotion of COVID-19 antigen testing in China emerged as a response to the evolving landscape of pandemic control. In the third year of the COVID-19 era, China’s epidemic prevention strategies underwent subtle adjustments. One year later, the National Health Commission released the Diagnosis and Treatment Protocol for Novel Coronavirus Pneumonia (Trial Version 9) (hereinafter referred to as the “Protocol”), which introduced significant changes ranging from viral characteristics and testing methods to diagnostic criteria and treatment approaches.

On the one hand, from the original SARS-CoV-2 strain to the Delta and Omicron variants, and even to “cocktail” strains formed by various combinations of mutations, the transmissibility of the novel coronavirus has increased several-fold. Accordingly, the Guidelines recommend that suspected cases be tested for common respiratory pathogens using methods such as rapid antigen testing and multiplex PCR nucleic acid testing, which aligns with the previous Application Guidelines. Although the eighth edition also mentioned antigen testing, its use was restricted to healthcare institutions; the new edition states that antigen tests can be used at home by individuals, further affirming the value of antigen testing.

On the other hand, with the widespread administration of COVID-19 vaccines and the successive market launch of specific anti-COVID-19 therapeutics, the likelihood of severe illness and death from COVID-19 has significantly decreased. In light of this, the Plan has lowered the criteria for centralized quarantine and discharge of patients with mild symptoms. According to the Plan, cases classified as mild are subject to centralized quarantine management rather than mandatory isolation at designated hospitals. Furthermore, isolation measures may be discontinued for mild cases if two consecutive nucleic acid tests for SARS-CoV-2 show cycle threshold (Ct) values of ≥35 for both the N gene and the ORF gene, or if two consecutive tests return negative results. Previously, a Ct value of ≥40 was required for hospital discharge.

The increased transmissibility of the novel coronavirus, coupled with the growing demand for out-of-hospital management, has made large-scale COVID-19 screening essential. Unlike diagnostic testing, screening targets individuals who are typically asymptomatic or have only suspected exposure, such as residents in medium- to high-risk areas, travelers, and individuals in closed or semi-closed settings. Consequently, greater emphasis is placed on the cost-effectiveness, timeliness, and convenience of testing methods. The primary objective is to identify cases with sufficiently high viral loads rather than to clinically diagnose COVID-19 patients. In this context, the methodological characteristic of COVID-19 antigen tests—requiring viral levels in samples to reach a certain threshold before yielding a positive result—offers superior health economic value.

It is worth noting that although the focus has been on competition for products and brands, antigen detection technology itself is already relatively mature. What cannot be ignored is that the economic logic of large-scale screening actually comes with higher requirements for the technical attributes of COVID-19 antigen detection. The opening of the COVID-19 antigen detection market is tantamount to a surprise stress test for domestic IVD brand companies.

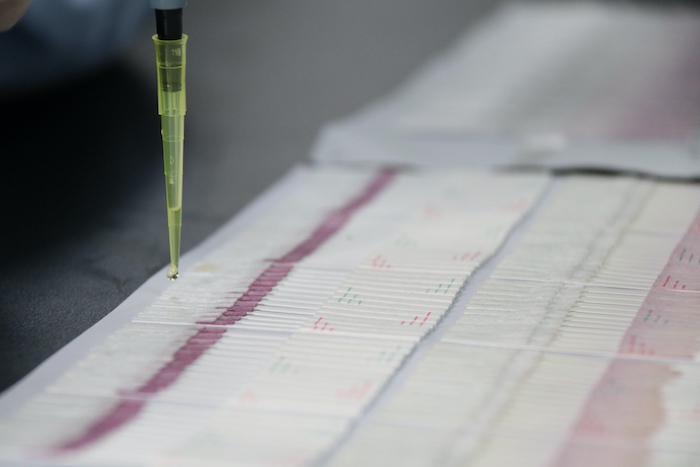

Among currently approved products, colloidal gold immunochromatography is the mainstream technology. This method employs highly specific antigen-antibody reactions combined with immunochromatographic techniques. The sample flows along the nitrocellulose (NC) membrane, reacting with antigens or antibodies pre-immobilized in the test zone and with colored conjugates (antigen or antibody labels) coated on the conjugate pad. A positive result is determined when both the test line (T) and the control line (C) show visible coloration.

Manufacturing Process of COVID-19 Antigen Test Kits (Image source: Provided by the interviewee)

This method of qualitative result interpretation based on color development imposes stringent requirements on factors such as antibody activity in the test zone and the flow rate of the sample through the test zone, thereby demanding higher quality standards for the core raw materials of the reagents.

For reagent raw material manufacturers, this is both a test of production capacity and a challenge to service capabilities. Details in the development of antigen detection reagents, such as antibody selection and sensitivity control, form the core technical barriers for raw material suppliers. They typically need to undergo extensive screening and repeated validation to determine the optimal solution. Moreover, rapidly responding to users' ever-changing needs and providing necessary technical support at the earliest opportunity require raw material manufacturers to possess rich practical experience and continuous learning abilities.

In fact, until just before the outbreak of the COVID-19 pandemic, raw materials for in vitro diagnostic (IVD) reagents were long dominated by overseas brands. Statistics show that in 2019, imported products accounted for as high as 88% of the domestic IVD raw material market. During the pandemic, shortages, supply disruptions, and price hikes for core IVD raw materials not only exposed supply chain security vulnerabilities but also strengthened the product capabilities of domestic suppliers, giving rise to a large number of experienced Chinese brands. Examples include Fibio Biologics and Vazyme, which provide core biologically active raw materials.

VCBeat has noted that as the Omicron variant accelerated the global spread of COVID-19, China emerged as a key export market for rapid antigen tests. According to data from the General Administration of Customs of the People’s Republic of China, more than RMB 70 billion worth of COVID-19 test kits were exported worldwide in 2021 alone. In January 2022, exports of antigen test kits totaled RMB 16.48 billion, rising to RMB 18.02 billion in February, bringing the cumulative export value for the first two months to RMB 34.5 billion. As a brand with years of deep involvement in the upstream IVD sector, HyTest Biotech can be regarded as the hidden champion behind the global success of COVID-19 antigen test kits. The company launched rapid R&D efforts on core raw materials for antigen testing—specifically, antibodies against SARS-CoV-2—at the outset of the pandemic, making it one of the earliest enterprises in the industry to introduce such products. It has since become a leading supplier of raw materials in this field.

The head of product at Fapon Biotech told VCBeat that the company’s emergence as a major global supplier is attributable to its robust foundational biotechnology platforms, technical services, and supply capabilities. The previously established mouse hybridoma technology platform, rabbit monoclonal antibody development platform, industry-leading antibody affinity maturation and antibody engineering platforms, and comprehensive physicochemical quality control platform have enabled the continuous iteration and performance enhancement of Fapon’s COVID-19-related products, sustaining their competitive edge in the industry. Having undergone four generations of upgrades, these products currently represent the state of the art.

Secondly, as the novel coronavirus continues to mutate, HyTest Biotech closely monitors viral strain evolution to ensure sensitivity and specificity. A professional team promptly tracks the prevalence of emerging variants, analyzes amino acid mutation frequencies, identifies the geographic distribution and spread of variant strains, and assesses the impact of these mutations. Upon early warning and identification, the company rapidly initiates the development of recombinant antigens and evaluates the risk of detection failure for antigen-based diagnostic products against variant strains. “We have successively made“More than 200 mutant combination antigens,” said the head of product at Fapon Biotech.

Furthermore, antibody production follows the paradigm of biologic macromolecule drugs to establish high-yield, stable cell lines. Scale-up manufacturing is conducted using mammalian cell fermentation technology, with process development adhering to pharmaceutical standards. The final product undergoes structural characterization by mass spectrometry and comprehensive, standardized, and robust physicochemical analysis for quality control release, laying a solid foundation for controlling batch-to-batch variability. Meanwhile, Fapon possesses large-scale production resources and equipment capable of meeting diverse capacity requirements, allowing flexible utilization based on demand. This ensures high customer stickiness and timely, ample inventory. In terms of product services, we have a professional technical support team that provides customers with comprehensive raw material usage solutions, assists in accelerating product development, and meets the diverse needs of our clients.

VCBeat has learned that Chinese IVD raw material manufacturers, having weathered the trial of the COVID-19 pandemic, have achieved faster technical response times and built sufficient production capacity resilience. More importantly, they are able to provide timely localized services to customers. “Fapon Biotech has extensive experience in antibody development. It rapidly developed antibodies suitable for COVID-19 antigen testing and dispatched its technical team to customer sites promptly to provide support, helping customers adapt to the fast-paced changes in the market,” said a product manager at Fapon Biotech. Furthermore, maintaining stable supply capabilities during sudden market surges was key to Fapon Biotech standing out among numerous IVD raw material suppliers. “This truly tests a company’s capacity management capabilities and is the supplier attribute most valued by customers once the market stabilizes.”

Following the deregulation of antigen testing in China, regulatory authorities and brand owners are sparing no effort in approval, production, and market launch. As a result, Fapon Biotech’s R&D and manufacturing headquarters in Dongguan, Guangdong Province, is busier than ever. Amid intensifying market consolidation favoring leading players in the COVID-19 antigen sector, truly superior solutions depend, above all else, on the meticulous attention to detail by domestic manufacturers of reagents and raw materials.

Indeed, whether it is the entry of industry giants, the scarcity of available test kits, or challenges in production capacity, these are all phased characteristics of the growth of China’s domestic COVID-19 antigen testing industry. We have reason to believe that Chinese manufacturers can withstand this stress test and provide more diversified solutions for domestic COVID-19 epidemic prevention and control.