One Year After Coronary Stent Volume-Based Procurement: Have Companies Recovered?

Lepu Medical

Developer and Manufacturer of Cardiac Interventional Medical Devices and Pharmaceuticals

The centralized volume-based procurement of coronary stents, which began at the end of 2020, was implemented throughout the entire year of 2021. One year is a brief period for a pharmaceutical or medical device product, but it represents a significant span in terms of industry transformation. There are many data points and phenomena worth discussing.

In the first year of centralized volume-based procurement, 27 products from 12 companies were involved. Rankings were determined based on product bid prices in ascending order, with the lowest-priced winning products guaranteed no less than 10% of the total allocable volume, and ultimately 10 products were selected. These rules dictated that the procurement outcomes would reshape the market landscape. Large enterprises with substantial capital reserves and high R&D investment would leverage their economies of scale to accelerate market capture, while smaller firms with limited technical capabilities and funding shortages would face significant challenges, often resulting in their marginalization or exit from the market.

Let us first revisit the bid-opening results from one year ago that transformed the industry. Ten products from eight companies were selected in this volume-based procurement. Following this centralized procurement, the average price of coronary stents dropped from approximately RMB 13,000 to around RMB 700. Compared with 2019, the average price reduction for identical products from the same manufacturers reached 93%. The coronary stents procured in this round are made of cobalt-chromium or platinum-chromium alloys, elute sirolimus and its derivatives, and have a procurement cycle of two years.

Based on the results, mainstream products commonly used in clinical practice by medical institutions were largely selected in the centralized procurement, covering more than 70% of the intended purchase volume of these institutions. A total of 2,408 medical institutions participated in the centralized procurement, including all 851 institutions with an annual purchase volume exceeding 500 units. The intended purchase volume for the first year reached 1.07 million units, approaching the usage volume of drug-eluting cobalt-chromium stents in 2019 (1.09 million units) and accounting for 65% of the total procurement volume across all materials in 2019 (1.65 million units). Following the centralized procurement, the significant price reduction is expected to trigger a substantial increase in usage, meaning that actual purchase volumes will often exceed the contracted amounts. In other words, this is a market that enterprises cannot afford to lose.

One Year On: What Is the Current Status of Companies Participating in Centralized Procurement? VCBeat Provides an Overview.

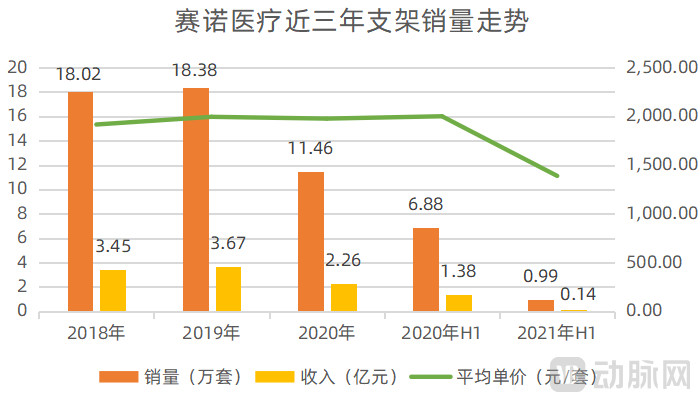

SinoMedical’s name did not appear in the aforementioned bid-winning table, as its flagship product is the BuMA drug-coated stainless steel coronary stent. The scope of this volume-based procurement (VBP) covered drug-eluting stent systems made of cobalt-chromium or platinum-chromium alloys and loaded with rapamycin or its derivatives. Consequently, its product naturally failed to win the bid. Even though SinoMedical previously held a market share exceeding 10% and ranked among the top four domestically, it has inevitably been marginalized in the market following the VBP.

Based on the sales volume of Sino Medical's coronary stents over the past year, the impact of not being included in the procurement list has been significant. The year-on-year decline in sales volume reached 85.61%, dropping from a peak of 183,800 units in 2019 to less than 10,000 units in the first half of 2021. During the same period, revenue decreased by 90%, falling from RMB 367 million in 2019 to RMB 14 million in the first half of 2021.

According to Sino Medical's 2021 annual performance forecast, the total operating revenue for the full year of 2021 is expected to be RMB 188 million to RMB 194 million, representing a year-on-year decrease of 40.75% to 42.58%. The net profit attributable to shareholders of the parent company is projected to be a loss of RMB 131 million to RMB 140 million, marking a year-on-year decline of 682.48% to 722.50%. In 2021, the revenue from the coronary business segment amounted to RMB 59 million to RMB 62 million, reflecting a year-on-year decrease of RMB 188 million to RMB 191 million.

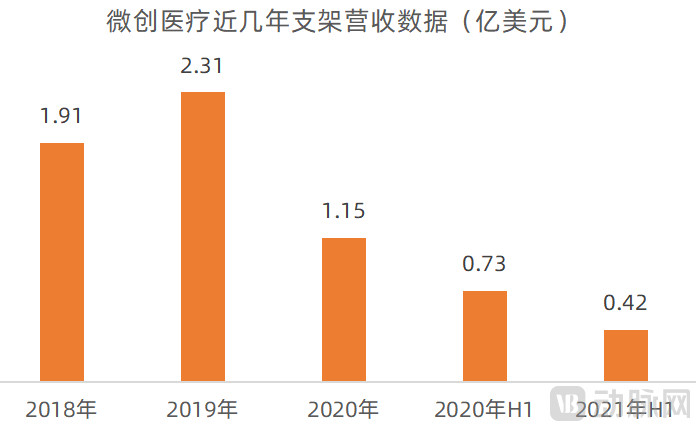

MicroPort had two products shortlisted, securing the largest share in this volume-based procurement round. The intended purchase volume was 260,000 units, while the actual procurement exceeded 1 million units. Sales volume increased by 200% year-on-year, and market share rose from 23% to 47%. Nevertheless, overall revenue from coronary stents continued to decline.

This trend was already evident in the 2021 semi-annual report. As one of its three core business pillars, the vascular intervention segment (including coronary stents, drug-coated balloons, etc.) saw a significant 24.4% year-on-year decline in revenue to USD 66.837 million in the first half of 2021, with its share dropping to 17%. By comparison, the corresponding shares were 22% in 2020 and 33% in 2019, indicating a marked contraction in revenue scale. Net profit amounted to only USD 7.849 million, representing a nearly 80% year-on-year plunge.

MicroPort Scientific Corporation recently issued a 2021 annual profit warning announcement, indicating that sales revenue during the reporting period was expected to achieve double-digit year-on-year growth. However, the Group recorded a period loss attributable to equity shareholders of the Company of approximately USD 275 million to USD 285 million, representing a year-on-year decline of 43.98% to 49.21%. Affected by this news, the company's stock price once plummeted by 10%.

Lepu Medical, previously ranked second in domestic market share for coronary stents, had only one product shortlisted in this volume-based procurement: the cobalt-chromium alloy rapamycin-eluting stent system (GuReater). The product’s gross margin was approximately 78.06% in 2019. Its price was reduced by 92.32% in the procurement process, dropping from RMB 8,400 per unit to RMB 645 per unit. Based on the contracted procurement volume of 150,000 stents, Lepu Medical’s total revenue from this product in 2021 is expected to be less than RMB 100 million.

Based on GuReater’s 2019 sales data, the product’s net profit is projected to decrease by RMB 110–130 million. According to the first-quarter report of 2021, the contracted volume for centralized procurement in 2021 was 143,900 units; however, shipments under centralized procurement reached 98,800 units in the first quarter alone, resulting in an 89% increase in net profit and essentially overcoming the short-term impact of coronary artery stent centralized procurement.

According to the 2021 semi-annual report, with the implementation of centralized procurement, although the traditional stent business declined significantly, the innovative product portfolio of "intervention without implantation" achieved remarkable growth, generating sales revenue of RMB 364 million, a nearly 20-fold increase year-on-year. During the reporting period, the second quarter saw a quarter-on-quarter growth of 75.6% compared to the first quarter, and the overall stent business segment in the second quarter basically returned to the normal level of 2019.

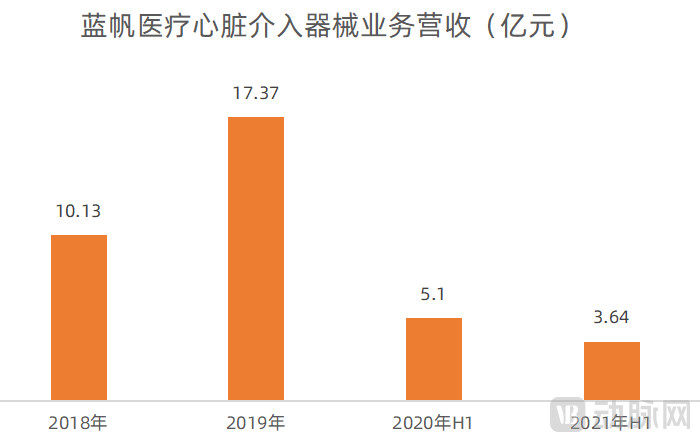

Blue Sail Medical’s coronary stent business was acquired through the purchase of Biosensors International. Its entire cardiac interventional device portfolio includes bare-metal stents, drug-eluting stents, drug-coated stents, balloon catheters, and other ancillary products for interventional cardiac procedures. The “Xinyue” series, which has been shortlisted this time, belongs to the category of drug-coated stents.

As can be seen from the chart, revenue from the relevant business segment in the first half of 2021 amounted to only RMB 364 million, representing a 28% decrease compared to the same period in 2020, which was already impacted by the pandemic. This decline occurred despite a 437% year-on-year increase in sales volume of stents under the “Xinyue” brand. Although sales volume quadrupled, the gross profit margin decreased by 25.72 percentage points. The short-term impact was highly significant.

The increase in sales volume driven by centralized procurement failed to offset the impact of price reductions, and coupled with the fact that other coronary products had not yet been launched or achieved significant sales volume, this led to a substantial decline in performance. According to Blue Sail Medical’s 2021 earnings forecast, net profit decreased by 26.07%–48.82% year-on-year.

Overall, after their products were included in the centralized volume-based procurement (VBP) program, companies experienced a significant impact on both operating revenue and gross profit margins, which even substantial procurement volumes could not fully offset. So, what adjustments have the selected companies made this year to cope with these changes?

MicroPort is the first domestic company to go public in the coronary stent industry. Over the past decade, it has launched four drug-eluting stents (DES). Its first-generation DES, Firebird, has been phased out, while its second-generation product, Firebird2, pioneered the application of cobalt-chromium alloys. Currently, sales revenue from coronary stent products accounts for approximately 30% of the company's total revenue.

With its Firebird 2 and Firekingfisher products winning bids in the centralized procurement at prices of RMB 590 and RMB 750, respectively, MicroPort became the company with the highest stent procurement volume, accounting for 36% of the total awarded quantity despite price reductions exceeding 90%. Benefiting from the centralized procurement program, MicroPort’s drug-eluting stent products have cumulatively reached more than 2,700 hospitals.

From another perspective, MicroPort Medical won bids for its two highest-market-share products in this volume-based procurement, thereby defending its existing market channels, consolidating its market share, and redirecting market resources toward high-margin products. Its orthopedic medical device business, cardiac rhythm management business, aortic and peripheral vascular interventional product business, neurointerventional product business, and heart valve business all achieved rapid growth, with year-on-year increases of 22.9%, 20%, 68.6%, 114.5%, and 121.8%, respectively.

In addition to the two products that won bids in the centralized procurement, MicroPort also has the Firehawk targeted drug-eluting stent and Firesorb, a bioresorbable rapamycin (sirolimus)-targeted eluting coronary stent still in the research and development phase.

The advent of drug-eluting stents has reduced the rate of vascular restenosis; however, coating stents with drugs increases the risk of late thrombosis. The concept of "targeted elution" aims to reduce the drug dosage to a level sufficient to prevent restenosis without inducing late thrombosis, which served as the foundational principle behind the development of Firehawk. Firehawk features the lowest drug load globally, less than one-third of that in other stents, thereby significantly enhancing safety while achieving comparable efficacy.

In the short term, hospitals will prioritize meeting the guaranteed purchase volumes for products included in the centralized procurement program, which will impact Firehawk’s sales. However, thanks to its expanding market share, Firehawk has also gained access to over 100 additional hospitals. The channel advantages derived from its increased market share are gradually being monetized.

From the perspective of the secondary market, although volume-based procurement (VBP) has had a certain impact on the vascular intervention business segment, MicroPort’s stock price showed a consistent upward trend from the announcement of VBP in late 2020 to July 2021, six months after its implementation. What happened during this period?

Volume-based procurement will inevitably impact MicroPort’s cardiovascular interventional business in China, prompting the company to accelerate its overseas stent business expansion. Its sales volume in Europe increased by 131% year-on-year, with an average of 700–800 stents implanted per month. Furthermore, the company began localized research, development, and production of stents in the United States and India last year.

However, the overseas market cannot immediately boost MicroPort’s revenue; this requires time. What truly expands the ceiling of market expectations is the growth of new businesses. In addition to its three core business segments—traditional cardiovascular intervention, orthopedic medical devices, and cardiac rhythm management—MicroPort Medical has added peripheral and aortic intervention, neurointervention, heart valves, surgical robots, and radiofrequency/cryoablation therapies.

MicroPort has adopted a strategy of spinning off subsidiaries for independent listings. To date, it has successfully listed MicroPort Endovastec, MicroPort CardioFlow, MicroPort NeuroTech, and MicroPort MedBot. The market capitalization of MicroPort MedBot has now exceeded HK$20 billion, nearly matching the total market capitalization of MicroPort Medical. Furthermore, MicroPort EP MedTech also has plans for a separate listing.

Currently, among the four companies spun off for independent listing, only MicroPort Endovastec has achieved profitability. Last year, MicroPort Endovastec reported revenue of RMB 685 million, a year-on-year increase of 45.59%, and net profit attributable to shareholders of RMB 316 million, up 47.3% year on year. The other three businesses, such as MicroPort MedBot, remain in the research and development stage.

From a policy perspective, as the current penetration rate of aortic endovascular intervention remains relatively low—with fewer than 100,000 stent grafts implanted annually—it is still considered an innovative therapy. Furthermore, the wide variety of stent models poses significant challenges for inventory management. Since no local pilot programs have been launched to date, the short-term impact of centralized procurement is expected to be limited, allowing MicroPort Endovastec to continue benefiting from the launch window of its new products.

As some medical device companies specializing in single-product categories face pressure from centralized procurement and find it increasingly difficult to invest substantial capital in developing new product categories, MicroPort Medical, as a platform-based medical device company, has promoted the coordinated development of multiple business segments through spin-off listings for financing.

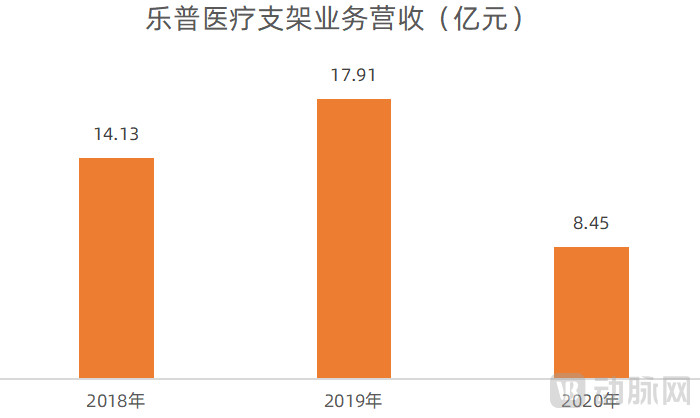

Although the volume-based procurement (VBP) pricing policy was not implemented until 2021, its negative impact had already become apparent in 2020. For instance, Lepu Medical’s revenue from metal stents amounted to RMB 845 million in 2020, representing a 38% decline compared with 2019. This decrease was primarily attributable to a certain volume of stents that had been sold but not yet implanted within the distribution channels, necessitating resolution through returns or price adjustments. Consequently, Lepu Medical recorded substantial impairment losses in the fourth quarter of 2020.

On the surface, Lepu Medical appears to incur greater losses with increased sales volume after joining the centralized procurement program. However, the core significance of centralized procurement lies in streamlining distribution channels. For enterprises, this reduces marketing and sales expenses, while ensuring timely payment settlement (healthcare institutions must settle payments with enterprises within 30 days).

The 2019 annual report showed that the gross profit margin of Lepu Medical’s stent system was approximately 78.06%, with selling expenses accounting for 37.16% of total operating costs. If this expense item were excluded, the gross profit margin of Lepu’s stents could rise to 86.2%, reducing the cost per stent to RMB 414. In other words, even with a winning bid price of RMB 645, the stent product would theoretically still have a profit margin of around RMB 230.

In the short term, price reductions under the volume-based procurement (VBP) program will undoubtedly have a significant impact on corporate revenue. However, for Lepu Medical, which has established a comprehensive layout across the entire cardiovascular industry chain, the impact of any single product is temporary. A more critical consideration is whether the company can leverage the VBP initiative as an opportunity to expand hospital access for a broader range of its products.

The rapid absorption of the impact from volume-based procurement can be attributed to Lepu Medical’s forward-looking product portfolio strategy. Six years ago, Lepu Medical began advocating the concept of “intervention without implantation” in the field of percutaneous coronary intervention (PCI). The core objective is to provide effective disease intervention and treatment for patients who do not require metal stent implantation, through the combined use of conventional accessories, cutting balloons, drug-eluting balloons, and bioresorbable scaffolds. This approach also aims to reduce complications associated with metal stent implantation and alleviate the psychological burden on patients.

Drug-coated balloons function similarly to coronary stents. The balloon serves as a drug carrier, delivering the medication to the lesion site and causing transient dilation of the affected vessel; the balloon is then withdrawn, whereas the stent remains permanently implanted within the diseased vessel.

It is precisely the forward-looking, continuous investment in R&D and the academic promotion of the “intervention without implantation” concept that have enabled Lepu Medical to rapidly recover its related businesses despite the impact of the centralized procurement of coronary stents. Through six years of academic promotion, Lepu has established a complete product portfolio for “intervention without implantation,” branded as “Drug-Cut” (drug-coated balloons, bioresorbable scaffolds, and cutting balloons). Furthermore, Lepu is actively engaged in the development of a broad pipeline of products, including intravascular measurement devices.

According to Lepu Medical’s latest third-quarter 2021 financial report, the company’s total revenue for the first three quarters reached RMB 8.635 billion, representing a year-on-year increase of 35.19%. Although revenue from its traditional stent business declined, the innovative “intervention without implantation” product portfolio generated RMB 613 million in revenue, surging by 1,073.24% compared to the same period last year and successfully offsetting the impact of the coronary stent business.

To mitigate the impact of centralized procurement, Lepu Medical has fully leveraged its cross-cycle product portfolio strategy, establishing a combination that uses winning bid products as an entry point alongside high-margin non-bid product lines, thereby driving profitability through volume.

Blue Sail Medical started with health protection gloves. As the world's largest manufacturer of PVC gloves, it achieved its best performance since going public in 2020 amid the COVID-19 pandemic, with operating revenue reaching RMB 7.9 billion and net profit attributable to shareholders after deducting non-recurring gains and losses amounting to RMB 1.7 billion. It was even dubbed the "Glove Mao" at one point. Currently, the health protection glove business accounts for over 90%, while cardiac interventional devices make up approximately 7%.

In this volume-based procurement (VBP) round, Blue Sail Medical adopted the most aggressive strategy, submitting the lowest bid of RMB 469. According to VBP rules, in addition to the intended purchase volumes reported by medical institutions, at least 10% of the unallocated volume is directly assigned to the winning bidder. Furthermore, the company remains free to compete in markets outside the VBP framework.

This strategy is closely tied to product portfolio planning. Currently, Blue Sail’s coronary stents can be categorized into four major types:

First, the BioMatrix product series consists of polymer-free drug-eluting stents, which are primarily marketed in Europe, South Korea, Southeast Asia, and other regions;

Second, the Excel stainless steel drug-eluting stent—a stainless steel, polymer-based, biodegradable device—is primarily marketed in China and is expected to be phased out with technological advancements.

Third, EXCROSSAL is a cobalt-chromium drug-eluting stent featuring a cobalt-chromium alloy platform and a biodegradable polymer. It is primarily marketed in China and can be regarded as an upgraded version of the previous-generation product (EXCEL).

Fourth, the BioFreedom product series comprises drug-coated stents utilizing Biosensors’ proprietary patented drug A9. These products are primarily marketed in Europe, Japan, and the United States, and are poised for imminent launch in the Chinese market.

Although the Xinyue stent, which won the bid in this volume-based procurement, has received positive industry reviews for its product performance, it exhibits a high degree of homogenization with existing products. Blue Sail Medical is currently focusing its R&D efforts on the BioFreedom stent, which features distinct differentiated selling points. This product is poised to capture market share outside the procurement framework and contribute relatively higher profit margins.

BioFreedom is the first stent worldwide capable of reducing the duration of post-procedural antiplatelet therapy from one year to one month, fundamentally mitigating patients’ bleeding risk. Approved in China in June 2021, it remains the only imported drug-eluting stent approved by the National Medical Products Administration (NMPA) for one-month dual antiplatelet therapy (DAPT) in patients at high bleeding risk.

Furthermore, the upgraded BioFreedom Ultra stent has obtained CE certification in Europe and entered 12 countries and regions, including France, the United Kingdom, Italy, Denmark, and Sweden, gaining market recognition. It has also been successively approved in Thailand and South Korea, while its registration process in China is currently underway.

In this centralized procurement round, Blue Sail Medical adopted a low-price strategy to expand its hospital coverage, rapidly extending its sales network to more than 2,300 hospitals. As of June 2021, sales volume of the Xinyue stent exceeded 220,000 units, representing a year-on-year increase of over 430%, thereby consolidating its market share and laying the foundation for the promotion of new products.

Furthermore, Biosensors International maintains a robust product pipeline that includes drug-coated balloons (DCB) and interventional balloons for totally calcified coronary lesions and chronic total occlusion (CTO) lesions. The company also closely monitors global R&D advancements in bioresorbable scaffolds across materials science, mechanical manufacturing, and pharmaceutics, ensuring it remains at the technological forefront of coronary intervention.

In other words, the key for Blue Sail Medical to mitigate the impact of centralized procurement lies in whether its new products can be launched and scaled up in a timely manner to keep pace with the high coverage of centralized procurement, thereby expanding the market alongside its existing product portfolio.

In addition to these representative companies, other domestic players such as Yisheng Technology, Jinrui Kaili, and Wanrui Feihong are not discussed here, as they are not yet publicly listed and thus lack available financial reports, and their overall market share is relatively small. Among foreign brands, Medtronic and Boston Scientific were also included in the centralized procurement program. Medtronic’s coronary and renal denervation businesses, including drug-eluting stents (DES), saw growth of approximately 15%. Compared with the high triple-digit growth achieved by some of its other business segments, the stent business exhibited slow growth, and the company’s financial report explicitly noted that this performance continued to be affected by China’s centralized procurement. Boston Scientific, on the other hand, did not directly disclose details of its China operations in its financial report.

Overall, the products of several companies have been impacted in terms of both revenue and gross margin after entering the centralized procurement system, a effect that even substantial purchase volumes cannot fully offset. From a product perspective, companies should prioritize bidding with mature products that hold significant market share, while simultaneously laying out their pipeline for products in the introduction and growth stages, such as bioresorbable stents. Although centralized procurement of consumables has compressed profits for some enterprises, it has also driven the industry back onto a track of healthy market competition centered on quality, technology, and clinical efficacy.

For enterprises facing large-scale volume-based procurement, winning the bid is fundamental, while post-award product portfolio management strategies are key to turning the tide. A cross-cycle R&D layout for product portfolios serves as a crucial safeguard against external risks and enables companies to maximize and rapidly monetize the channel traffic advantages derived from winning volume-based procurement bids.