Life Science Tools: An Investment Theme Conferred by the Era

Almost overnight, attention has been drawn to previously obscure life science tools such as single-use bioreactor bags for drug manufacturing, petri dishes, and chromatography membranes. Stakeholders have identified a vast new market emerging from the widening gap between supply and demand.

In fact, as a large number of innovative macromolecular drugs and novel therapeutic modalities—such as antibody-based therapeutics, cell therapies, and vaccines—transition from laboratory research to industrial-scale production, there has been a fragmented surge in demand for biopharmaceutical manufacturing processes and associated R&D services. The physical isolation imposed by the COVID-19 pandemic further widened these market gaps, bringing them into sharper focus. Consequently, capital has flowed into the sector, empowering domestic innovators to develop their own efficient and stable solutions for downstream commercial manufacturing, spanning key stages such as cell culture media, bioreactors, and centrifugal filtration.

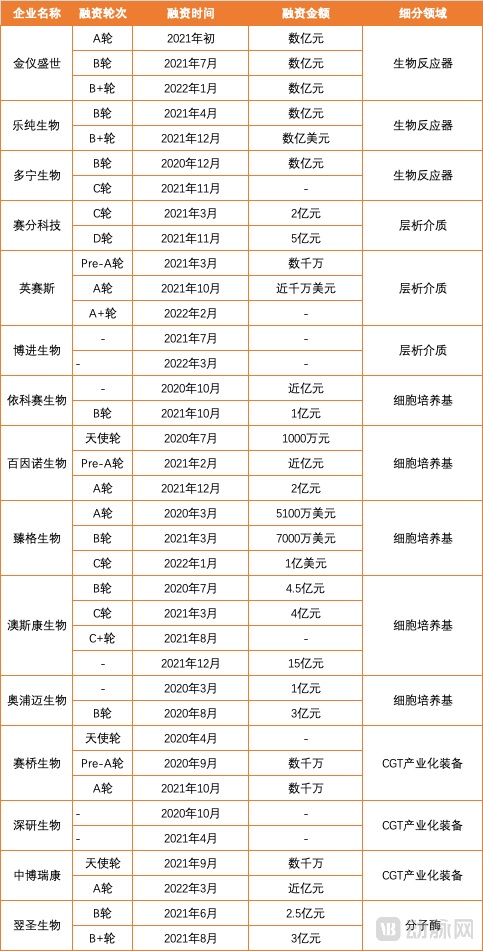

Industry enthusiasm has rapidly translated into investment momentum. Since the second half of 2020, a large number of domestic brands that have established prominence in fields such as bioreactors and cell culture media have accelerated onto the fast track of business expansion and external financing. According to incomplete statistics from the VCBeat Orange Database, from March 2020 to the time of publication, at least 15 life sciences tools companies completed two or more rounds of financing, with transaction amounts continuously reaching new highs. For instance, Auscan Biologics, a leading domestic player in cell culture media, completed four rounds of financing within two years, raising over RMB 2.5 billion. Jinshi Shengshi, which provides single-use bioprocess total solutions to companies such as CanSino Biologics, completed three rounds of financing totaling hundreds of millions of yuan within just one year, setting a new record for the speed of fundraising among life sciences tools enterprises.

Life Sciences Tools Companies That Completed Two Rounds of Financing Within a Partial Year (Data Source: VCBeat Orange Database)

In a sense, the life sciences tools industry represents a relatively certain presence amid today’s turbulent market, characterized by clear demand and stable cash flows. However, taking a longer-term perspective, what is the growth potential of this highly fragmented sector—spanning products, technologies, and markets? With generally low ceilings, how can companies expand their operational boundaries? Recently, VCBeat conducted an exclusive interview with Sun Linghao, Managing Director at Matrix Partners China, who outlined a distinctive vision for the growth of the life sciences tools industry.

Sun Linghao, Managing Director at Matrix Partners China

To date, Matrix Partners China has cumulatively invested in nearly 10 life sciences tools companies, establishing itself as one of the most active investors in this sector. Notably, Matrix Partners China served as the exclusive lead investor in the Series A financing round of Kingray Shengshi (mentioned earlier) and participated in three subsequent follow-on rounds. Other portfolio companies include Gator Bio (Xingtong Medical), a globally leading brand in next-generation label-free bioanalysis; Saiqiao Bio, a provider of digitally enabled process equipment for cell and gene therapy with independently controlled domestic technology; Inscinstech, which specializes in bioseparation technologies; and ECHO Biotech, which is developing “Chinese core” products for cell culture. Over the past two years, these companies have successively completed multiple rounds of financing, with Matrix Partners China playing a key role as a major financial investor in each case. According to Sun Linghao, after more than a decade of deep cultivation and rapid expansion over the last two years, China’s life sciences tools industry is on the verge of explosive growth, a process that is being accelerated by extensive industry collaboration. He emphasizes that investment decisions should be made with a sufficiently long-term perspective. “We believe that great companies will inevitably emerge from China’s life sciences tools industry,” he stated.

VCBeat:VBInsight appears to place significant emphasis on the life sciences tools sector. Why?

Sun Linghao:We believe that every wave of industrial development gives rise to significant opportunities for supply chain upgrading. The booming growth of the biopharmaceutical sector has brought life science tools to the brink of an explosion, prompting us to make decisive and systematic strategic investments.

VCBeat:The Eve of Industry Explosion: When Is It?

Sun Linghao:Early 2020. While systematically studying this field, Matrix Partners China began investing in source innovations for bottleneck equipment, consumables, and raw materials in the upstream segment of biopharmaceuticals. In a sense, this is the investment theme endowed to us by this era.

VCBeat:What are the criteria for judgment?

Sun Linghao:As our research into the biopharmaceutical industry deepens, we have begun to extend our analysis along the upstream and downstream segments of the industrial chain to identify systematic investment opportunities for industrial upgrading. In the post-pandemic era, we have observed three core driving factors.

First, the importance of the upstream supply chain in the life sciences sector has been highlighted under the COVID-19 pandemic. How to break through "chokepoint technologies" and achieve localization of core equipment, consumables, and raw materials have become central issues for China's life sciences industry. Regulatory authorities have also implemented multiple substantive support policies to encourage independent innovation within the domestic industrial chain.

Second, we observe that most domestic companies were established between 2008 and 2015. After a decade of accumulation, their product quality has gradually approached or even surpassed that of overseas counterparts, laying the foundation for competing on equal footing with top-tier European and American enterprises.

Third, the accumulation of talent and technology. This field involves multiple disciplines, including biology, chemistry, materials science, and mechanical engineering, and China’s years of industrial accumulation are beginning to yield results.

Based on these three major catalyst effects, we believe that the inflection point for industrial upgrading across the entire sector has emerged, and we have begun to systematically position ourselves.

VCBeat:So is the main opportunity seen in domestic substitution?

Sun Linghao:Indeed, this is the case at this stage. Regrettably, in many niche sectors we focus on, the localization rate remains below 10%. For instance, in the single-use bioreactor industry where we have invested, the localization rate for large-scale antibody production using single-use bioreactors was zero just one year ago. As core equipment for antibody and vaccine manufacturing, these systems present extremely high customer entry barriers and significant switching costs, thereby establishing substantial competitive moats.

VCBeat:Has this situation changed significantly over the past two years?

Sun Linghao:Yes, we have observed that domestic enterprises are increasingly adept at leveraging a variety of emerging technologies. They fully utilize automation tools in their production processes and integrate advanced technologies such as biosensing, microfluidics, and flexible manufacturing into their products, while effectively controlling costs and ensuring quality. From this perspective, amid the wave of digitalization, automation, and intelligence sweeping through the life sciences industry, we remain optimistic about the continued growth of domestic companies and their ability to secure a foothold in overseas markets.

VCBeat:What is the total market size?

Sun Linghao:Narrowly defined within the biopharmaceutical sector, the current global market size for life science tools is estimated at $30 billion, with the Chinese market exceeding RMB 20 billion. If the upstream consumables and reagents segment associated with the IVD industry, which was catalyzed by the COVID-19 pandemic, is taken into account, the market size would be even larger. Over the past two years, we have primarily focused on market opportunities in the upstream supply chain of the biopharmaceutical industry.

VCBeat:Is a RMB 20 billion market ceiling not particularly high?

Sun Linghao:In fact, it is essential to adopt a dynamic, phased perspective; the market is currently in its early stages and experiencing rapid growth. At Matrix Partners China, we have summarized the development of China’s life science tools into three phases.

Phase I, from 2010 to the onset of the COVID-19 pandemic, saw a cohort of companies quietly cultivating their niches with meticulous dedication. After a decade of honing their craft, they gradually emerged as hidden champions in their respective segments, although their absolute scale remained limited. In conversations with numerous founders, we learned that this sector attracted little attention at the time, making fundraising and talent acquisition exceedingly difficult. It was akin to standing alone at the bottom of a pond, gazing upward through a misty haze, where one moon’s reflection blurred into another.

Phase II, spanning the two years from early 2020 to the present, has seen the domestic market size for life science tools exceed RMB 10 billion. Individual subcategories, such as single-use bioreactors and consumables, cell culture media, and purification chromatography, have each surpassed RMB 2 billion. Driven by the dual forces of global supply chain shortages catalyzed by the COVID-19 pandemic and robust demand for import substitution, the industry has entered a period of rapid growth. We have observed that some Chinese companies have accomplished in two years what took foreign giants ten years to achieve. For entrepreneurs, this phase has often required striking a delicate balance: pursuing aggressive expansion while maintaining meticulous quality control. This is no easy feat and demands patience from all stakeholders in the industry.

Phase III is preliminarily projected to commence in 2023. As the catalytic effect of the COVID-19 pandemic gradually wanes, the industry will enter its third development cycle. Leading companies in niche segments will complete key customer validations and accumulate industrialization experience, securing entry into the sphere of industry giants around 2024–2025. Through continuous growth via mergers and acquisitions and strategic collaborations, these companies will progressively align with international standards in customer validation, product quality control systems, and marketing team development. This evolution will give rise to five or six first-class life science tools companies based in China with a global footprint.

VCBeat:From this perspective, 2023 was a critical year for the life sciences tools industry.

Sun Linghao:Yes, in fact, the end of the impact of the COVID-19 pandemic marks the true beginning of healthy development for this industry.

VCBeat:This judgment is unique.

Sun Linghao:This represents a phased conclusion derived from our evolving understanding and reflection on the life sciences tools industry. Most of the companies we monitor have experienced varying degrees of positive or negative impact on their operations due to the pandemic, yet, as everyone hopes, COVID-19 will eventually come to an end. We believe the most critical issue lies in the post-pandemic era, particularly in discussions with founders regarding business uncertainty. For instance, we examine what the pandemic-related business has truly brought to the company—whether it be team development, product market access, or other benefits. These discussions about uncertainty delve into the fundamental business considerations across short-, medium-, and long-term horizons. It is often exhilarating to witness founders’ sudden insights into the essence of these matters.

VCBeat:Is the Future Still Highly Uncertain?

Sun Linghao:Correct. More importantly, the market size of this niche segment is expanding rapidly. At this juncture, participants in the field, whether entrepreneurs or investors, should embrace a sense of mission, viewing competition and collaboration from a higher-dimensional perspective, and strengthening their core competencies to deliver value to downstream customers. As the industry matures, various forms of strategic alliances, partnerships, and mergers and acquisitions will emerge. Stakeholders will continue to collaborate across multiple dimensions, jointly driving the wave of localization within the life science industry chain. Summarized through economic theory, the life sciences tools sector possesses multiple markets and production factors capable of achieving “Pareto optimality,” gradually approaching an ideal state of resource allocation.

VCBeat:But such convergent strategies have precisely led to intense involution within the industry?

Sun Linghao:I do not believe the life sciences tools industry is characterized by involution, a view that aligns with the sentiments of most practitioners. At an industry event, I recall the founder of a leading company in this field stating, “Companies in this sector are striving to deliver high-quality products to customers, and the overall market is experiencing rapid growth. Essentially, there is no cutthroat competition within the industry; rather, we are working together to advance the development of China’s life sciences industrial chain.” This remark left a deep impression on me.

VCBeat:With So Many High-Quality Projects in Hand, Has Matrix Partners China Slowed Its Pace in the Life Sciences Tools Sector?

Sun Linghao:Not really. Two years ago, our team developed a “battle map” for the life sciences tools sector based on interviews and research, outlining key subsectors we would prioritize for coverage. To date, all of our investment activities have remained within the scope of that map. However, the industry has evolved more rapidly than we anticipated, and many founders in this space have demonstrated growth that exceeded our expectations. We believe this represents a long-term opportunity with strong certainty. As an investment firm focused on China, we continue to invest in high-quality companies in this field.

VCBeat:Do you have any insights on selecting specific investment targets?

Sun Linghao:Our research into this industry has revealed two critical overarching trends.

First, accurately assess the addressable market for the core products of the companies in question. This includes both the static size of the addressable market and the growth trajectory of specific product segments.

In the second half of 2020, we conducted a systematic study of this industry. We found that there are actually few individual categories capable of achieving substantial scale. By calculating the addressable market over the next five years, we projected the market share and profit margins of leading companies, thereby determining which categories warrant strategic investment.

Second, select an appropriate valuation framework. Based on our analysis of the development trajectories and public market valuations of international companies, we have established a dynamic valuation model for life science tools. We observe that many niche sectors experience irrational bubbles or temporary undervaluation due to periodic misjudgments in investors’ valuation frameworks.

VCBeat:How to Understand the Differences in Valuation Systems Across Various Sub-sectors?

Sun Linghao:For instance, by providing automated equipment and consumables to cell therapy clients, if the products are of high quality, customers will utilize them from the pre-IND stage through Clinical Phases I, II, and III, all the way to large-scale commercial production. While contract values in the pre-IND stage may be in the range of millions of RMB, they will certainly reach tens or even hundreds of millions of RMB at the commercialization stage. In a sense, this represents a subscription-based business model combining products and services. For such a model, if the company continues to grow and expand its customer base, we believe it deserves a significant valuation premium. This is merely an example of qualitative judgment on a business model. As a professional investment institution, we need to quantify these insights into mathematical models and establish a reasonable valuation system through rigorous research of both primary and secondary markets.

VCBeat:Are there any key factors in specific investment decisions?

Sun Linghao:Ultimately, it comes down to the judgment of the founders.

Outstanding founders across various industries share many common traits. In this field, we believe two aspects of a founder’s competency model are particularly critical: first, organizational capability. Building a core team composed of individuals from diverse backgrounds who can collaborate efficiently is of paramount importance. The upstream industrial chain involves the intersection of multiple specialized fields, including biology, chemistry, materials science, electronics, and mechanics. Meanwhile, the company’s organizational structure encompasses product R&D, process systems, quality control, marketing and sales, technical support, and more. This places significant demands on a founder’s comprehensive capabilities. Second, integration capability. As evidenced by the history of leading international peers, mergers and acquisitions (M&A) are an inevitable path to becoming an industry giant. However, in a rapidly growing market, executing M&A transactions with genuine strategic value requires exceptional judgment from founders. We look forward to seeing a cohort of founders with strong strategic thinking gradually consolidate their respective niche sectors, thereby scaling up and strengthening their enterprises.

VCBeat:High-quality projects are probably not easy to invest in, right?

Sun Linghao:When we first began conducting systematic research into this industry, few investment institutions were paying attention. This afforded us ample time to engage with teams and conduct due diligence across various sectors and projects, thereby accumulating unique insights into the industry. Over the past year, as the industry has experienced rapid growth and garnered broader attention and recognition, I believe the most critical aspect of early-stage investing remains the mutual trust between investors and high-quality founders, grounded in deep industry understanding. This forms the foundation for our long-term partnership with companies and achieves sustainable, win-win outcomes.

VCBeat:Do High-Quality Projects with Ample Cash Flow Still Need External Capital?

Sun Linghao:During its development, the company requires external support in three key areas: talent, customers, and capital. Regarding talent, through in-depth industry research and systematic investment deployment, we have established a relatively comprehensive talent mobility ecosystem. Our post-investment recruitment system helps our portfolio companies identify and secure suitable candidates. In terms of customer acquisition, Matrix Partners China has made substantial investments in the innovative drug and biotechnology sectors. We facilitate targeted introductions, and there are already numerous cases where two of our portfolio companies have established strategic partnerships for mutual benefit. As for capital, as a long-term investment institution, we frequently engage in early-stage investing and provide continuous support. Furthermore, we leverage our robust post-investment service system to assist high-quality companies and founders in achieving comprehensive growth.

VCBeat:Does this mean that post-investment management is critically important for the life sciences tools industry?

Sun Linghao:Correct. In fact, within Matrix Partners China, we have been consistently advancing our “Three-Pronged Strategy,” namely ecosystem-oriented investment, scenario-based post-investment support, and strategic brand building. In the post-investment phase, the support we provide to portfolio companies encompasses six major modules: proactive diagnostics, industrial chain synergy, emergency medical assistance, front-end empowerment by due diligence teams, and operation of an entrepreneurial ecosystem community.

In December 2021, Matrix Partners China announced the launch of “Matrix Sci-Tech Innovation Hub,” aiming to make its empowerment initiatives more practical and substantive. The initiative provides scenario-based guidance to founders with scientific or technical backgrounds in the healthcare sector, addressing common entrepreneurial challenges such as equity and stock options, fundraising, business models, talent development, organizational structure, and macroeconomic trends.

VCBeat:Can you provide a specific example of industrial synergy?

Sun Linghao:Take, for example, the nucleic acid drug bioprocessing sector, in which Matrix Partners China has made deep strategic investments.

For a long time, only foreign companies could supply industrial-grade solid-phase nucleic acid synthesizers. However, under the impact of the COVID-19 pandemic, lead times extended to over 12 months. An early-stage company in which we invested last year has become one of the few domestic suppliers capable of providing industrial-grade nucleic acid synthesizers. With independent R&D capabilities for core components, it has gained recognition from multiple small nucleic acid drug developers and nucleic acid CDMOs, addressing the urgent needs of innovative small nucleic acid drug companies. Meanwhile, the chemical synthesis of small nucleic acid drugs is a complex process that demands high-level CMC (Chemistry, Manufacturing, and Controls) capabilities. Based on this, we also invested in a team with over ten years of experience in nucleic acid synthesis CMC to serve small nucleic acid drug enterprises. Combined with our strategic layout in the field of nucleic acid drug R&D, these companies are engaging in bilateral business collaborations. As financial investors, we have initially established a win-win ecosystem in the niche sector of nucleic acid therapeutics.

VCBeat:This field is evolving rapidly. What advice or reminders do you have for entrepreneurs?

Sun Linghao:Amid the COVID-19 pandemic, domestic companies have built up substantial strength and achieved rapid growth over the past two years. However, as the pandemic gradually recedes, we believe that there are two core challenges facing these companies today that warrant sober reflection amidst the industry’s fervent development.

First, the absolute ceiling for single-product companies is not particularly high; the divergence between the valuation ranges of companies focused on niche segments and objective realities makes future integration more difficult. Second, horizontal product expansion involves inherent complexity and follows objective laws. Many rapidly growing companies oscillate strategically between providing holistic solutions and offering high-quality standalone products. Underlying this dynamic, the clarity with which a company defines its core business logic will determine its strategic direction and tactical execution.

“Sowing and harvesting do not occur in the same season; therefore, one must endure loneliness, resist temptations, and withstand setbacks.” We believe in the long-term, certain opportunities within the life sciences tools sector and are committed to standing alongside high-quality companies as they continuously meet challenges. With the courage to engage deeply, we persist in investing in founders who possess both an industry-wide vision and a strong sense of mission. Together, we will forge ahead through the wave of transformation in the life sciences industry, fulfilling the historical mandate bestowed upon us by this era!