Dual Listings of He’s Vision and Rayne Group Signal a New Era for China's 'Golden Eyes & Silver Teeth' Healthcare Market

“Golden Eyes, Silver Teeth”: A Double Celebration!

Yesterday, He Eye Hospital and Arrail Group listed on the ChiNext board of the Shenzhen Stock Exchange and the Hong Kong Stock Exchange, respectively. On its first day of trading, He Eye Hospital’s stock price surged by as much as 38.5%, while Arrail Group’s market capitalization exceeded HK$8 billion.

As the two most market-oriented segments of healthcare services, the “Golden Eyes” and “Silver Teeth” companies went public on the same year, month, and day. While this was a coincidence, it fully reflects the encouraging growth momentum in these two sectors.

In the past two years, ophthalmology chains have entered an intensive period of initial public offerings. In 2021, Chaoju Eye Care went public on the Hong Kong Stock Exchange. In the A-share market, in addition to He’s Eye Hospital already being listed, Huaxia Eye Hospital and Purui Eye Hospital have both submitted their registration for listing on the ChiNext board.

In the dental sector, Arrail Group has broken the long-standing stalemate of no new listed dental chains since Topchoice Medical, becoming China’s first nationally branded dental chain to go public. Additionally, Yaboshi and China Dental Care Group have also submitted their IPO applications.

A company’s initial public offering (IPO) marks its entry into a new stage of development. Post-listing, the infusion of more substantial capital for business expansion and optimization of operational models will also reshape the industry landscape. Therefore, we have analyzed the use of proceeds and strategic plans of 11 listed and IPO-applicant companies in the “golden eyes and silver teeth” sector to examine potential market shifts driven by their growth.

Expanding existing stores or opening new ones is a necessary step for chain institutions to achieve business expansion and scaled operations. Public listing and financing provide more substantial financial support for newly expanded stores, while companies also need to pursue expansion to deliver better performance results.

Ophthalmology Chain Accelerates National Expansion

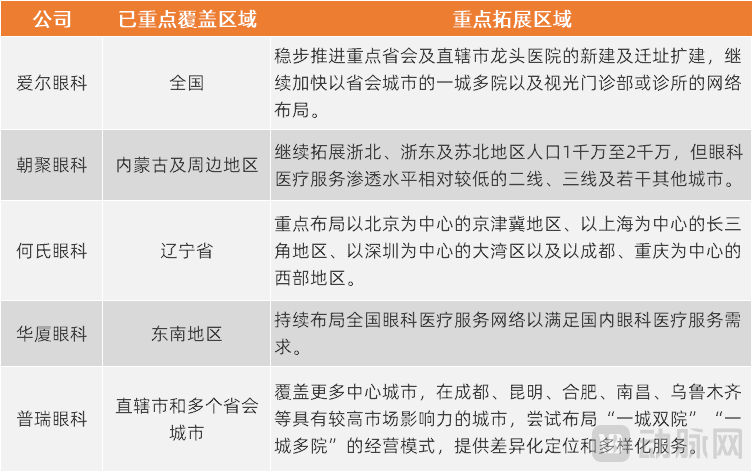

While Aier Eye Hospital has already achieved nationwide coverage, Chaoju Eye Care, He’s Eye Hospital, and Huaxia Eye Hospital and Purui Eye Hospital—both on the verge of going public—exhibit distinct regional characteristics. Nevertheless, cross-regional expansion and entering the national market have become key objectives for these companies, and they are accelerating their efforts in this direction.

Key Regions for the Expansion of Several Ophthalmology Chain Groups, Source: Company Prospectuses or Financial Reports, Compiled and Charted by VCBeat

He Eye Hospital, which went public yesterday, will next focus its strategic expansion on the Beijing-Tianjin-Hebei region centered on Beijing, the Yangtze River Delta region centered on Shanghai, the Greater Bay Area centered on Shenzhen, and the western region centered on Chengdu and Chongqing.

According to the prospectus of He Eye Specialist, the investment of funds raised from the listing includes two projects outside Liaoning Province: the newly built Beijing He Eye Specialist Hospital, which serves as a key branch for establishing regional chain operations in the Beijing-Tianjin-Hebei region; and the newly built Chongqing He Eye Specialist Hospital, which serves as a key branch for establishing regional chain operations in the western region.

In addition, Chaoju Eye Care will focus its expansion in northern Zhejiang, eastern Zhejiang, and northern Jiangsu. Purui Eye Hospital will further expand its domestic market presence to cover more central cities, and will pilot “two hospitals per city” or “multiple hospitals per city” models in cities with significant market influence, such as Chengdu, Kunming, Hefei, Nanchang, and Urumqi. Aier Eye Hospital will also accelerate its network layout of multiple hospitals per provincial capital city, along with optometry outpatient departments or clinics.

Meanwhile, C-MER Eye Care, which has expanded from Hong Kong to the Chinese mainland, will focus its strategic presence in East China, Southwest China, Central China, and cities within the Guangdong-Hong Kong-Macao Greater Bay Area, by establishing or acquiring eye hospitals, eye centers, and clinics.

EuroEyes, a multinational brand, will continue to implement its expansion plan by opening multiple clinics in China's core metropolitan areas and one to two clinics in second-tier cities.

Although companies vary in their regional expansion strategies, they share many commonalities. It is evident that key hotspots for expansion include the Beijing-Tianjin-Hebei region, the Yangtze River Delta, the Chengdu-Chongqing region, and the Guangdong-Hong Kong-Macao Greater Bay Area, with provincial capital cities serving as the primary focus for market deployment.

Dental Chains Crack the Code on Cross-Regional Expansion

Compared with ophthalmology, the overall expansion pace of dental chains has been relatively conservative, with most adopting a strategy of consolidating regional advantages.

Key Regions for the Expansion of Several Dental Chain Groups; Source: Prospectuses or Financial Reports, Compiled and Charted by VCBeat

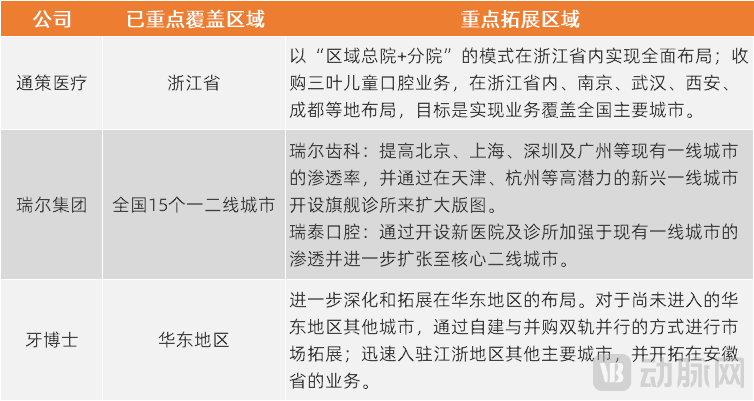

Ya Bo Shi, which was born and raised in Suzhou, has submitted its IPO application. The prospectus indicates that Ya Bo Shi will further deepen and expand its presence in East China. China Dental Care Group, which has filed its prospectus with the Hong Kong Stock Exchange four times, primarily targets the market in Wenzhou, Zhejiang Province.

Even Topchoice Medical, which has been publicly listed for many years and delivered strong financial performance, still derives the majority of its revenue from the Zhejiang provincial market. According to Topchoice Medical’s 2021 semi-annual report, medical service revenue within Zhejiang Province amounted to RMB 1.128 billion, accounting for 90.25% of hospital revenue; revenue from outside Zhejiang Province was RMB 122 million, representing only 9.75% of hospital revenue.

Currently, Topchoice Medical is achieving rapid expansion within Zhejiang Province by concurrently advancing its “Dandelion Plan” and the development of central hospitals. The “Dandelion Plan,” which entails increasing the number of branch clinics and expanding their coverage, is a key initiative for the company to establish a comprehensive presence across Zhejiang Province.

Like ophthalmology, dentistry requires heavy asset investment and has a long break-even period. However, it also faces a major hurdle: the high difficulty of standardized operations, which hinders the cross-regional expansion of dental chains.

However, Arrail Group, which went public yesterday, is an exception, having achieved a balanced chain-operation layout across multiple cities nationwide.

Aier Group pursues a differentiated business strategy through its two major brands: Aier Dental, positioned in the high-end dental care market, and Ruitai Dental, positioned in the mid-range segment. Currently, Aier Group operates 7 dental hospitals and 104 clinics across 15 first- and second-tier cities in China. Moving forward, Aier Group will continue to increase the penetration of Aier Dental in existing first-tier cities such as Beijing, Shanghai, Shenzhen, and Guangzhou, while expanding its footprint by opening flagship clinics in emerging first-tier cities with high growth potential, including Tianjin and Hangzhou. Meanwhile, Ruitai Dental will strengthen its presence in existing first-tier cities by opening new hospitals and clinics, and further expand into core second-tier cities.

The reason for the successful nationwide business expansion lies in the series of effective measures adopted by Arrail Group. In addition to the differentiated positioning of its dual brands, these measures include establishing a talent development and incentive system, implementing standardized operational procedures and systems, and building digital infrastructure, all of which ensure service quality and operational efficiency across Arrail Group’s locations throughout China.

Yesterday, VCBeat had already published in “China’s First Listed Mid-to-High-End Dental Chain Is Officially Born: An Exclusive Interview with Dr. Zou Qifang, Founder of Arrail GroupIn the article, the business model of Arrail Group was analyzed. In the future, Arrail Group’s path to breakthrough and its standardization experience may serve as a reference for the industry.

Business expansion encompasses not only quantitative growth but also the diversification and optimization of service offerings. In both ophthalmology and dentistry, new growth drivers are being identified based on existing operations, while enhanced competitiveness is achieved through business synergies.

Ophthalmology: Broadening the Base of Optometric Services and Strengthening the Apex of High-End Technology

Refractive surgery, cataract surgery, and optometric services constitute the core revenue drivers for ophthalmology chains. In optimizing their business structures, these chains primarily follow two strategic paths: expanding their optometric service networks and extending into the diagnosis and treatment of complex ophthalmic conditions and high-technical-complexity procedures.

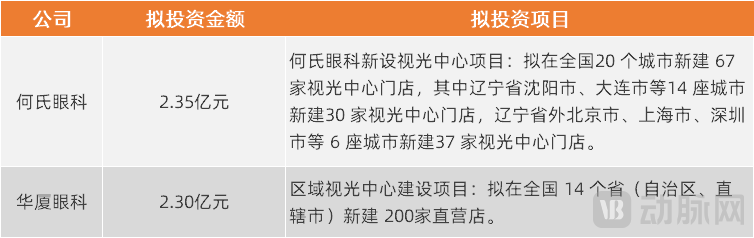

He Eye Care and Huaxia Eye Care’s Proposed Investments in Optometry Services; Source: Company Prospectuses, Chart Compiled by VCBeat

The prospectus reveals that both He Eye Specialist and Huaxia Eye Care will prioritize investments in optometry services to expand their coverage areas. In Aier Eye Hospital’s tiered chain model, optometry clinics focusing on optometry services and Aiyan e-Stations are also key components.

For ophthalmology chain enterprises, adding optometry service outlets offers numerous advantages: First, the initial investment per outlet is relatively low, the level of service standardization is high, and gross profit margins are substantial. Second, a multi-outlet layout can expand service coverage, facilitate more extensive disease screening, and generate patient referrals for ophthalmic diagnosis and treatment, refractive surgery, and other services, thereby reducing customer acquisition costs for hospitals. Meanwhile, compared with ordinary optical dispensing stores, optometry services with medical attributes possess stronger competitiveness.

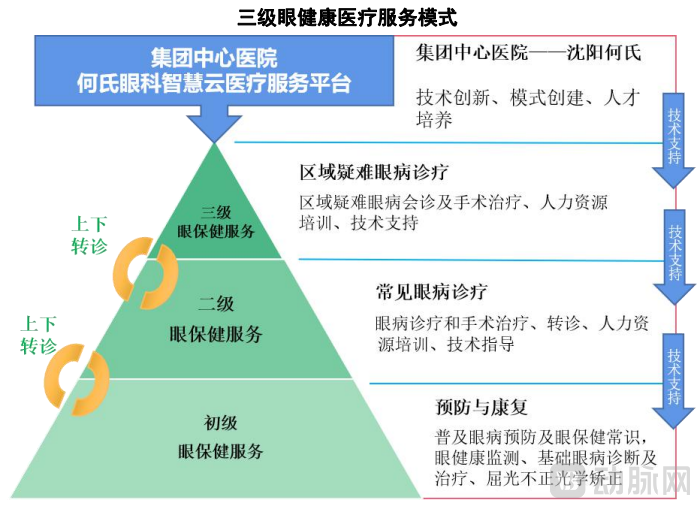

Taking He Eye Hospital as an example, it has established a three-tier eye health medical service model: primary eye care services are positioned for prevention and rehabilitation; secondary eye care services are positioned for the diagnosis and treatment of common eye diseases; and tertiary eye care services are positioned for the diagnosis and treatment of complex and refractory eye diseases within the region. A two-way referral system and vertical coordination have been formed among institutions at all levels. Specifically, primary eye care services deliver basic ophthalmic medical services to the public through optometry stores and clinics, including popularizing eye health knowledge, providing eye health monitoring, diagnosing and treating basic eye conditions, and offering optical correction for refractive errors.

It is evident that in He Eye Specialist’s service model, primary eye care services, focusing on prevention and rehabilitation, play a foundational role.

He Eye Hospital’s Three-Tier Eye Health Medical Service Model, Source: He Eye Hospital Prospectus

Amid the strong momentum in consumer healthcare, ophthalmology chains are also striving to enhance their diagnostic and therapeutic capabilities by expanding into high-technology clinical services. For instance, Purui Eye Hospital has prioritized ophthalmic medical services with advanced technical expertise—such as premium medical optometry, SMILE (Small Incision Lenticule Extraction) refractive surgery, pediatric strabismus and amblyopia management, nystagmus diagnosis and treatment, and premium cataract visual rehabilitation—while optimizing its service offerings and departmental structure. The hospital is further strengthening its diagnostic, therapeutic, and surgical services for fundus diseases, continuing to focus on managing complex and challenging ocular conditions.

Oral Care: Expansion Across All Age Groups, Focusing on Family Customer Value

Oral health challenges vary across different age groups. As public awareness of oral healthcare and consumer spending power increase, dental chains are expanding their service offerings to cater to all age demographics. Specifically, in recent years, parents have placed greater emphasis on children’s oral health, paying earlier attention to the prevention of various oral diseases and dental care. The prevalence of high-sugar foods and beverages has elevated the risk of oral diseases. Meanwhile, the accelerating trend of population aging has driven up demand among middle-aged and elderly individuals for diagnosis and treatment of oral conditions, as well as for dental restoration and implants. These factors have collectively motivated dental chains to diversify their service portfolios.

Topchoice Medical completed the acquisition of Sanye Children's Dental in 2020, initiated the construction of three secondary hospitals specializing in pediatric and family dentistry in 2021, and launched eight new Sanye-branded clinics in Zhejiang Province as well as in Nanjing, Wuhan, Xi'an, and Chengdu, with the aim of achieving nationwide coverage of its pediatric dental services across major cities in China.

Yaboshi continues to explore the expansion of its oral care service offerings and coverage across all age groups, including pediatric orthodontics and prevention and treatment of dental diseases, correction of malocclusion in adolescents, adult orthodontics and teeth whitening, and dental implants for middle-aged and elderly patients.

Currently, dental chain providers vary in their service focus, with differing gross profit margins and demand frequencies across various procedures. Once comprehensive oral health services for all age groups are established, these chains can better integrate and synergize their offerings, expand their customer base to include family units, and boost repurchase rates. Many dental chain institutions have introduced family-oriented membership programs or allow individual membership benefits to be shared among family members.

Arrail Group’s Ruitai Dental prioritizes core locations with easy customer access and proximity to residential communities when selecting sites. Yaboshi Dental enhances customer stickiness among children and their families by offering annual children’s membership cards and family treatment packages. Within family clientele, a positive experience by any one member can drive repeat consumption by other family members.

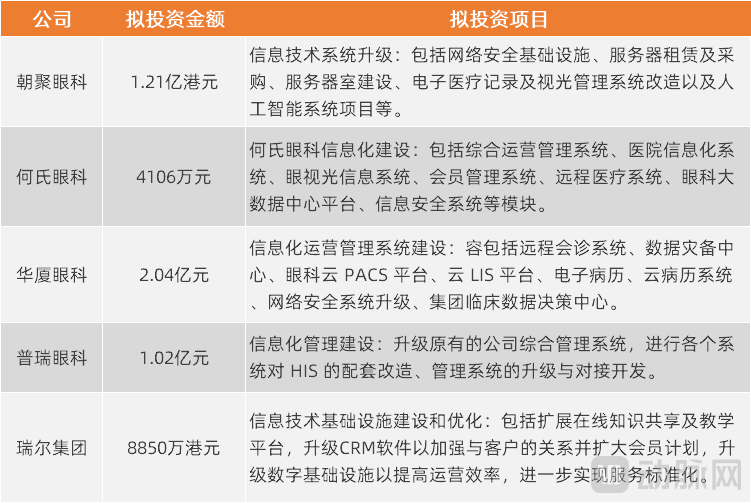

Digitalization is becoming an essential capability for healthcare service providers. Companies across various specialties, including ophthalmology and dentistry, have disclosed their digitalization initiatives in prospectuses or financial reports.

“Golden Eyes, Silver Teeth”: Investments in Digitalization Projects by Multiple Companies in the Sector. Source: Company prospectuses; chart compiled by VCBeat.

Overall, these companies will invest tens of millions to hundreds of millions of yuan in building and optimizing their digital capabilities. Digital technologies will drive multifaceted improvements in their service capabilities, service efficiency, and management effectiveness.

Currently, He Eye Specialist has established a smart cloud medical platform, leveraging intelligent ophthalmic diagnostic software and telemedicine systems to facilitate the decentralization of high-quality medical resources, thereby enabling large-scale, low-cost eye health monitoring. Shenyang He Eye Specialist has also launched an internet hospital, integrating pre-consultation, in-consultation, and post-consultation services to create a closed-loop data management system. This platform supports functionalities such as health management, telemedicine, mobile payments, interactive marketing, and intelligent analytics. With this IPO fundraising, He Eye Specialist plans to invest an additional RMB 41.06 million in the construction and enhancement of its user digitalization projects.

For Aier Eye Hospital, which has accumulated a vast amount of clinical diagnosis and treatment data, the value that digital technology can deliver is particularly significant. According to Aier Eye Hospital’s latest annual report, the company will strengthen the development of its ophthalmology big data center; fully leverage big data resources to unlock their value, enhance the level of ophthalmic research, explore AI-assisted diagnosis, and provide patients with precise diagnosis and treatment.

Topchoice Medical is building a “Future Hospital” in Hangzhou. The front end of the “Future Hospital” will feature intelligent clinical spaces, with digitalization and informatization implemented across all aspects of the patient journey, including appointment scheduling, follow-up visits, and navigation within the facility. On the back end, the hospital has established a digital dental collaboration platform and a Digital Hospital Command Center, whereby all clinical pathways are transformed into digital workflows. The “Future Hospital” also plans to develop big data and artificial intelligence platforms to organize and analyze hospital operational data and patient health information, leveraging intelligent analytics to deliver high-quality insights for clinical care and operational management.

It is worth noting that digitalization also provides significant support for the standardized operations of chain institutions. In Arrail Group’s digitalization initiatives, a SaaS platform was established for operational and medical quality management. This system supports business operations, customer relationship management (CRM), and business intelligence (BI) data analytics across different brands, regions, organizational structures, and service offerings. It also ensures compatibility for data exchange with other healthcare IT systems, thereby enhancing the capability to rapidly open and expand new clinics and hospitals. Furthermore, it enables the seamless integration of acquired clinics into Arrail Group’s centralized management framework, ensuring a consistent experience for customers across all locations.

Following its public listing, Arrail Group will utilize the funds raised to refine and upgrade these systems, and leverage a digital technology-enabled standardized framework to expand its DSO business model.

In summary, while public hospitals are vigorously advancing the development of smart hospitals, private medical institutions have also fully recognized the importance and necessity of digital technologies and are making targeted investments in this area.

A wave of IPOs among ophthalmology chains has culminated in the first nationally branded dental chain going public. In the future, the “golden eyes and silver teeth” market may undergo a series of significant changes.

Following their initial public offerings, companies will enjoy more abundant capital and stronger business expansion capabilities, leading to the emergence of more medium- and large-sized institutions. Correspondingly, as acquisitions are one of the primary means for listed companies to expand their operational scale, the market’s fragmented landscape of small and scattered players is likely to improve as more standalone or small-chain institutions are acquired by larger entities.

In this process, changes brought about by the external environment will also be superimposed.

First, changes in the upstream pharmaceutical and medical device market landscape will be transmitted to the downstream sector. In ophthalmology, domestically produced orthokeratology lenses are accelerating their development; in dentistry, the number of companies participating in the domestic clear aligner market is increasing. These developments are closely related to downstream consumer services, not only providing a wider selection of suppliers in the service sector but also enabling service providers to expand their customer base coverage through the price advantages of domestic products, thereby further enhancing market penetration.

Secondly, new technologies and business models are creating fresh opportunities for innovation. Currently, the rapidly growing field of digital therapeutics has expanded into ophthalmology, with a variety of ophthalmic digital therapeutic products being successively launched. Eye hospitals and optometry centers serve as the primary implementation settings for these products, enabling incremental service offerings. In dentistry, the Dental Service Organization (DSO) model is expanding its coverage and influence in China, facilitating the industry’s digital transformation and standardized operations.

In short, driven by both internal and external market factors, the multi-hundred-billion-yuan “golden eyes, silver teeth” market is poised for an even more optimistic outlook.