What Kind of Healthcare Enterprise Can Double a $150 Billion Market Cap in Two Years?

UnitedHealth Group

Health Insurance and Health Information Technology Service Provider

In China’s internet era, medical giants have been keen on building HMO systems with the goal of “creating China’s ‘UnitedHealth’,” but across the ocean, the giant ship has long since changed course.

Since 2009, UnitedHealth Group has soared on the Nasdaq, with its stock price climbing steadily from $20 to the current $500. Even amid the ravages of the COVID-19 pandemic, the stock price never pulled back; instead, it broke out of a two-year period of stagnation in the spring of 2022 and doubled again at the onset of the third year of the pandemic.

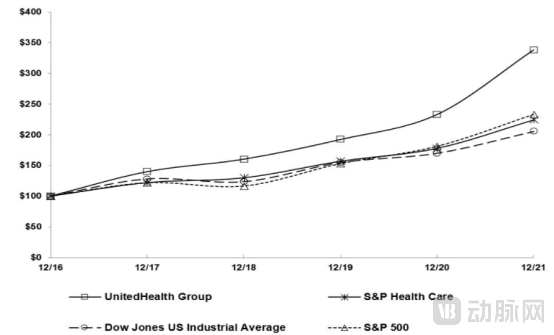

UnitedHealth Group’s stock price is buoyed by its consistently rising return on investment. Annual report data shows that its five-year investment return reached 338.16%, far exceeding the S&P 500 and standing at 1.65 times that of the Dow Jones Industrial Average.

Comparison of Cumulative Total Returns Over 5 Years: UnitedHealth Group vs. Economic Trends (Source: UnitedHealth Group Annual Report)

A Decade of Steady Growth, a Counter-Trend Rebound During the Pandemic: What Has Shaped UnitedHealth Group Today?

In 1974, a group of physicians established Charter Med Incorporated, aiming to help people access more effective and broader healthcare coverage. Four years later, Richard Burke, a former member of the organization, and Paul Ellwood, who coined the term “HMO,” carried forward the mission of Charter Med Incorporated and jointly founded UnitedHealth Group.

As the HMO model gained a firm foothold in the Upper Midwest, including Minnesota, UnitedHealth began to expand its coverage through aggressive acquisitions. By the time it acquired Sierra Health Services in 2008, it had extended its operations to all 50 U.S. states, establishing a significant market presence in each.

UnitedHealth Group’s M&A History (Data Source: Compiled by VCBeat)

This “buy, buy, buy” model sustained the insurance giant’s continuous growth for the first 20 years after its founding, but as the new millennium dawned, UnitedHealth gradually discovered that its insurance business had stalled.

Historically, UnitedHealth has consistently expanded its membership base by entering new states.At its core, it leverages mergers and acquisitions to directly acquire users who already have an intent to purchase insurance.. However, once the U.S. market was fully penetrated, UnitedHealth Group had to seek new customers within the existing market to continue expanding its domestic insurance business, leading to a sharp rise in customer acquisition costs.

In 2010, UnitedHealth Group’s M&A logic began to undergo a dramatic shift.

As strategies to boost membership numbers have hit a bottleneck and can no longer fully sustain the company’s rapid growth, management has begun to reevaluate its internal resources, seeking new growth drivers from its existing base, with the focus beingModel ValuewithData Value。

Under the HMO model, the closed-loop advantage of integrating “medical care, pharmaceuticals, and insurance” lies in its ability to standardize and project medical services and pharmaceutical expenditures, thereby ensuring controllable risks for health insurance operations. As a company with dominant strengths in the insurance sector, UnitedHealth Group has pivoted to expand into healthcare delivery and pharmaceuticals, rapidly completing this closed loop and reducing medical insurance expenditures.

The fundamental transformation of the business system can be traced back to 2004. In that year, UnitedHealth restructured its business logic by using “insurance” as the dividing line, splitting the company into two parts: UnitedHealthcare and Optum. The former is responsible forBaoInsurance Business, while the latter encompasses healthcare, pharmaceuticals, consulting and education, personal finance, and other sectors.Non-Insurance Business。

UnitedHealth Business System (Source: Compiled by VCBeat)

UnitedHealth Business System (Source: Compiled by VCBeat)

However, in its initial years, Optum’s business grew slowly, with profits accounting for less than 20% and revenue growth fluctuating between positive and negative figures, indicating significant instability. It was not until 2010 that UnitedHealth Group invested tens of billions of dollars to acquire leading companies such as the PBM provider Catamaran and healthcare IT firm Change Healthcare, while also securing surgical care operator Surgical Care Affiliates and rapid diagnostics company Alere Health. By making substantial bets on healthcare services, PBMs, and healthcare informatics, UnitedHealth leveraged Optum to capitalize on the technological dividends of the era of healthcare digitalization.

From the results, UnitedHealth’s aggressive strategy has proven highly successful. Leveraging health insurance technology has enabled it to continuously optimize its product portfolio, reduce premium expenditures, and effectively control claims risk. Meanwhile, increased investments in medical services, health management, and pharmacy benefit management (PBM) have helped both patients and providers lower healthcare costs, thereby attracting more users while reducing insurance spending.

Meanwhile, leveraging its vast data assets, Optum’s consulting and education services, as well as its financial services, have continued to grow. UnitedHealth Group has previously highlighted its impressive reach on its official website: Optum serves 80% of U.S. hospitals, 90% of Fortune 100 companies, 90 life sciences companies, and 127 million individuals.

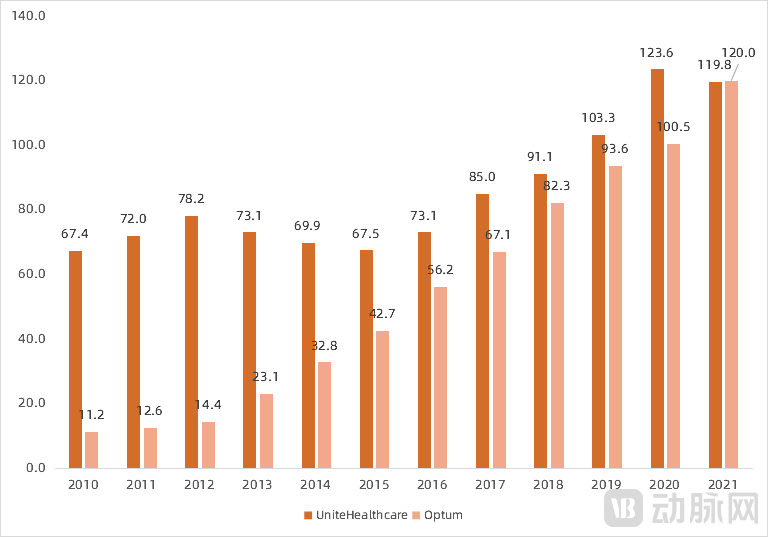

Over the past decade, Optum’s profit scale has accelerated its catch-up with the insurance business, growing at double-digit rates and driving UnitedHealth Group’s stock price steadily higher. In the 2022 annual report released recently, Optum’s segment profits even surpassed those of the insurance business for the first time, albeit by a narrow margin ($119.95 billion vs. $119.75 billion).

Comparison of Profits from UnitedHealth Group’s Two Major Business Segments (Unit: USD 100 million; Source: UnitedHealth Group Annual Report)

Today, the rise of Optum has broken through the growth constraints inherent in UnitedHealth Group’s single profit model. Its foray into “high-tech” markets such as big data, chronic disease management, and digital pharmaceuticals is continuously raising the ceiling for UnitedHealth Group’s potential—sustained profit growth and an expanding valuation range together underpin investors’ optimistic expectations.

Business innovation has continuously injected new vitality into the development of UnitedHealth Group, which helps explain its rising valuation. However, the company’s steady growth over the past two decades has relied on its sophisticated risk control system. This aspect can be analyzed from both macro and micro perspectives.

At the macro level, UnitedHealth Group’s strength lies in the deep synergies between its two business segments: UnitedHealthcare and Optum.

Initially centered on healthcare services and health insurance technology, Optum helped UnitedHealthcare generate profits by controlling costs through reduced premium payments, maintaining a unidirectional relationship in which “Optum serves UnitedHealthcare.” However, as UnitedHealthcare’s HMO system grew increasingly robust and Optum’s independent operations matured, UnitedHealthcare began to support Optum in return, directing patient flows to it and providing relevant data.

With the support of UnitedHealthcare, Optum Health’s medical services and personal finance businesses have expanded rapidly, while Optum Sight, backed by massive user data, has also made significant strides—possessing valuable resources that are difficult for other consulting firms to access.

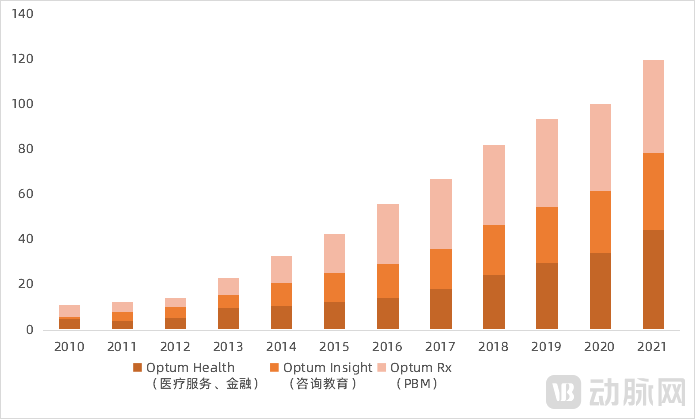

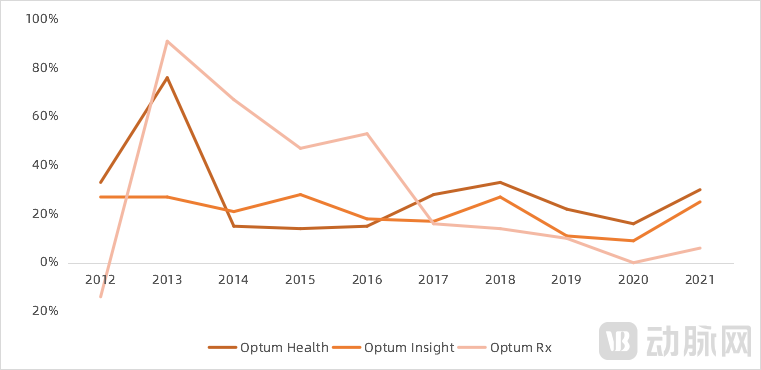

Profits from Optum’s three business segments have continued to rise, driven by acquisitions and synergies (unit: USD 100 million; source: UnitedHealth Group annual report)

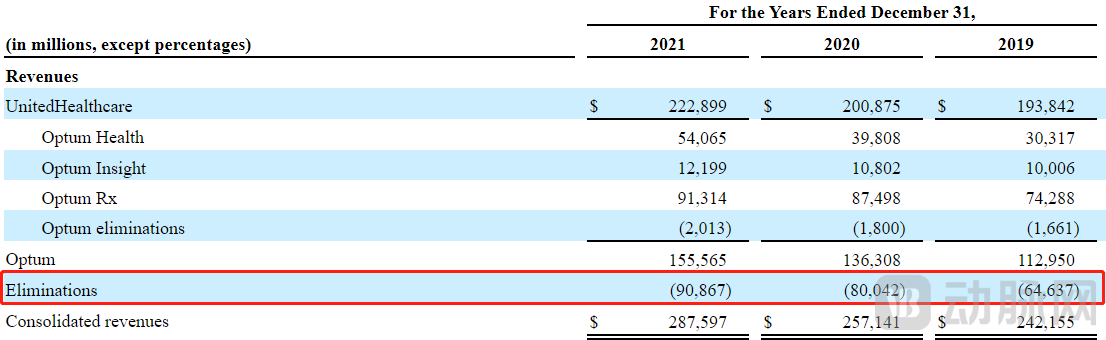

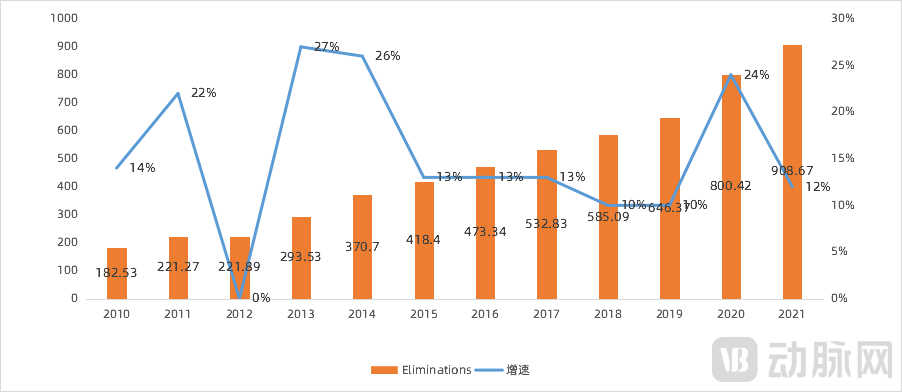

This synergy can be partially quantified using data. In UnitedHealth Group’s financial disclosures, there is a line item labeled “Elimination,” which measures premium expenditures that have been double-counted.

Excerpt of Financial Data from UnitedHealth Group’s 2021 Annual Report (Source: UnitedHealth Group Annual Report)

The gross profit of UnitedHealth’s insurance business can be roughly calculated as premium income plus out-of-pocket medical service revenue minus insurance reimbursement expenses. However, in its annual report data, UnitedHealth’s gross profit equals premium income plus medical service revenue minus insurance reimbursement expenses. The difference between medical service revenue and out-of-pocket medical service revenue constitutes “Elimination,” which is determined by the volume of medical services and the amount of insurance reimbursements. This metric can therefore be used to measure the synergies between UnitedHealth’s two business segments—a figure that has maintained double-digit growth over the past decade.

Changes in UnitedHealth Group’s Revenue Offsets (Unit: USD 100 million; Source: UnitedHealth Group Annual Report)

Annual report data show that UnitedHealth Group’s profits declined in 2013, 2014, 2015, and 2021. However, overall profits continued to grow, driven by strong performance from Optum and elimination adjustments. The elimination entries suggest that the deep synergy between UnitedHealth Group and Optum has diversified the company’s risk profile and provided substantial support for its growth.

Revisiting the Micro Level. In the first year of the COVID-19 pandemic, when the U.S. insurance industry teetered on the brink of collective bankruptcy and had to seek substantial government bailouts, UnitedHealth Group reported a remarkable 20% growth in profits.

Under U.S. policy, insurers such as UnitedHealth Group are required to cover pneumonia treatment costs for patients infected with COVID-19, but they do not provide additional premium subsidies. For a patient hospitalized for one month due to COVID-19, the insurer’s payout would exceed $300,000 (with total costs amounting to $400,000 and the patient responsible for $100,000 in out-of-pocket expenses).

In response, John Rex, CFO of UnitedHealth Group, cited two reasons for revenue growth: first, the growth of the Optum business drove overall business expansion; second, the emergence of the COVID-19 pandemic suppressed patients’ treatment for other conditions, resulting in lower healthcare utilization rates compared to pre-pandemic levels. These two factors may have partially offset the increase in COVID-19-related premiums.

On the other hand, insurance companies are also controlling premiums through other means. For example, UnitedHealth Group pays extra attention to the health conditions of vulnerable populations such as children and pregnant women, because deterioration in their health may lead to higher subsequent costs.

In terms of technology, UnitedHealth Group leveraged the pandemic to aggressively promote lower-cost virtual visits and telemedicine. Data shows that UnitedHealthcare completed approximately 33 million virtual visits in 2020, up from 1.2 million in 2019, representing a year-over-year increase of 2,500%. Optum Care clinics recorded fewer than 1,000 telemedicine visits in 2019, which surged to 1.5 million in the last nine months of 2020, resulting in substantial cost savings for UnitedHealth Group.

Investors in the secondary market are always keen to predict the inflection points faced by listed companies, especially for a company like UnitedHealth Group that has seen ten consecutive years of growth. After all, the turning point between gains and losses will inevitably arrive at some moment, particularly when latent issues begin to stir.

As previously mentioned, UniteHealthcare, which is responsible for insurance operations, has encountered a bottleneck. While its total revenue continues to grow, the slowdown in profit growth is an undeniable fact.

UnitedHealth Group has repeatedly sought to expand into overseas markets to revitalize its insurance business, but the HMO model’s heavy reliance on policy frameworks, medical services, and government spending has made it difficult to replicate. In late 2017, UnitedHealth Group planned to acquire Empresas Banmédica, a company providing healthcare services in Chile, Peru, and Colombia, but the deal was ultimately halted by local governments.

Optum, another key pillar of the enterprise, is also facing challenges. Optum Rx, responsible for the PBM business, has seen its profit growth move past the bonus period brought by mergers and acquisitions, with growth rates approaching “zero”; meanwhile, Optum Health, which includes medical services, continues to grow but consistently faces contradictions inherent in its own system.

A Detailed Discussion on the Contradictions Faced by Optum HealthWithin the HMO system, the prerequisite for lowering the medical loss ratio is to suppress medical costs, thereby saving expenses for both insurers and patients. However, indiscriminately suppressing medical reimbursement rates inevitably triggers dissatisfaction among physicians. This tension has been particularly pronounced since January 2021, when U.S. regulations required insurers to disclose negotiated healthcare prices. The disparity in reimbursement rates between UnitedHealth and regional hospitals sparked significant outrage among healthcare providers, leading multiple medical institutions to terminate their partnerships with UnitedHealth and withdraw from its network.

The only business maintaining growth with minimal risk is Optum Sight, the consulting and education arm under Optum. This segment primarily serves hospital physicians, with only approximately 100 life sciences companies having purchased its services. Despite accounting for just 4.2% of revenue in 2021, it contributed 14.2% of profits and continued to grow at a rate of 20%.

Changes in Profit Margin Growth Across Optum’s Business Segments

In the vast B2B market, Optum Sight boasts a bright future, with data serving as its core support. After all, in the era of healthcare big data, those who master business operations seize the first-mover advantage in creating disruptive innovations.

In this hundred-billion-dollar market, UnitedHealth Group is poised to build another UnitedHealth Group.

Looking back at the healthcare giant UnitedHealth Group has built over more than 40 years, we can broadly attribute its success to two key factors.

First, UnitedHealth Group created an HMO system that aligns with the government insurance framework and meets the demands of a large consumer base; second, it expanded both horizontally and vertically based on this model, building competitive barriers while leveraging data to identify new, high-quality growth opportunities.

Back in China, with UnitedHealth Group serving as a guiding beacon, a large number of insurance and internet healthcare companies have joined the effort to build China’s HMO system. Enterprises such as Ping An Insurance and WeDoctor have already achieved notable success.

Both types of enterprises hold promise to become pioneers of China’s HMO sector, but the models they build will inevitably differ from a direct replication of the U.S. model. After all, they must selectively address the following issues.

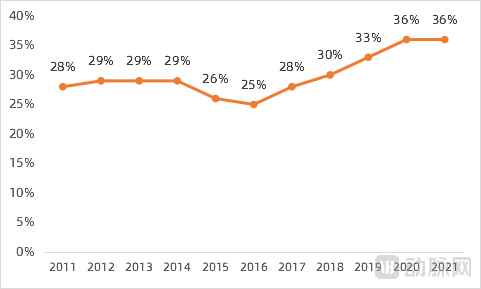

First, market characteristics. The foundation of UnitedHealth’s HMO model lies in the fragmented healthcare resources and high medical costs in the United States, along with CMS assistance that helps users cover part of their insurance premiums. In contrast, China’s domestic market is non-profit and highly fragmented, lacking a stable payer to provide premium support. As a result, even if domestic HMO systems can establish profitable business models, it remains difficult to scale them up.

Percentage of UnitedHealth’s Total Premium Revenue from CMS (Centers for Medicare & Medicaid Services)

Next is the completeness of the HMO system. UnitedHealth Group has built its HMO on a foundation of “medical care,” possessing substantial proprietary medical infrastructure while leveraging its dominant position in health insurance to attract high-quality medical institutions into its system through partnerships. In contrast, although domestic insurance companies and internet healthcare firms are also developing medical infrastructure, they do not yet have the strength to compete with public hospitals and therefore lack significant appeal to premium medical resources.

Finally, while various enterprises in China intend to establish an integrated model encompassing healthcare, pharmaceuticals, and insurance, it is difficult for them to achieve a win-win outcome among these three sectors without operating under a unified system. As demonstrated by UnitedHealth Group’s HMO model, insurance, pharmaceuticals, and medical services often exhibit a zero-sum relationship. This implies that, in the absence of a single entity to provide centralized coordination, systems constructed by insurance companies and pharmaceutical firms in China tend to have multiple, divergent objectives. Lacking shared goals and corresponding incentives, such arrangements can only be sustained through loose affiliations.

Nevertheless, the myriad challenges facing the domestic market also present opportunities for pioneers.

In 2002, Stephen J. Hemsley, then CEO of UnitedHealth Group, believed that the federal government would eventually increase funding for Medicaid. Defying prevailing skepticism, he acquired AmeriChoice, a company with an established Medicaid business, at a time when nearly all other healthcare companies were reluctant to engage in the Medicaid market. This strategic foresight secured UnitedHealth Group a significant share of the Medicaid market.

Today, domestic HMOs are also facing the same dilemma of choice.

Amid intense pressure from China’s national medical insurance system, the RMB 2 trillion premium target for health insurance in 2025 has illuminated the industry’s prospects. At this juncture, those who can accurately grasp policy trends and identify business models best aligned with regulatory directives will be well-positioned to lead the future health insurance market and reshape its competitive landscape.