When Will the Davis Double Play Arrive? A Review, Comparison, and Outlook on China's Heart Valve Industry

From investors’ frenzied scramble for equity stakes in heart valve companies to the profound impact of the capital market’s sharp downturn; from the explosive global rise of the TAVR industry to widespread concerns within the sector about the true scale of demand in China. Between 2020 and early 2022, China’s heart valve sector experienced a classic “Davis double kill.” Several leading heart valve companies listed on the Hong Kong Stock Exchange failed to meet commercialization expectations, with their market capitalizations not only falling below their IPO prices but at one point even dropping below the total amount of historical financing raised. The entire sector appeared to have hit the pause button.

Regardless, the fundamental drivers supporting the growth of the heart valve industry remain intact: China is progressively entering a phase of deep aging, and behind valvular heart disease—a typical age-related condition—lie tens of millions of patients who are not amenable to pharmacological treatment.

Past experience in Europe and the United States has shown that heart valves represent a massive market segment capable of spawning more than one decabillion-dollar medical device company. Since its listing on the NYSE in 2000, the stock price of Edwards Lifesciences, the leading player in the valve sector, has surged by more than 150-fold, far outpacing the gains of both the S&P 500 Index and the S&P 500 Health Care Index.

Setting aside the ups and downs of the capital market, if commercialization is indeed the litmus test for the medical device industry/enterprises,What stage has China’s heart valve sector currently reached, and when can we expect a Davis double play in the heart valve industry?

Given the significant differences in application scenarios between valve repair and replacement, this discussion primarily focuses on the pathway of bioprosthetic valve replacement.The author’s main argument is that:

1. The most mature segment of surgical bioprosthetic valves has entered a phase of rapid domestic substitution in China. However, even in cardiac surgery, the adoption of minimally invasive technologies—such as transcatheter bioprosthetic valves, expandable bioprosthetic valves, and sutureless bioprosthetic valves—is an unstoppable trend.

2. The interventional heart valve industry is just getting started; a flourishing diversity of innovations will be the main theme in the aortic valve segment over the next five years. The market for mere replicas of older-generation Western products is limited, as Chinese patients require original, more disease-specific solutions.

3. Mitral and tricuspid valve replacement remains in its early stages of development globally. Drawing on the commercialization trajectory of aortic valves in China, it may take considerable time before the mitral and tricuspid valve replacement market experiences explosive growth.

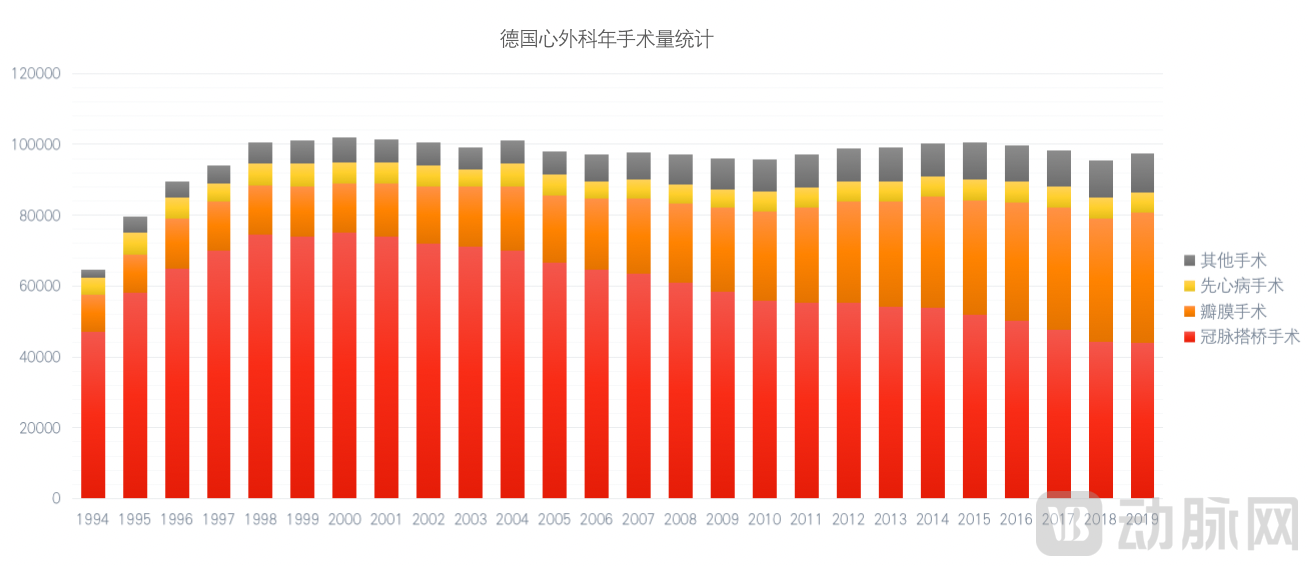

Surgical bioprosthetic valves were first introduced into clinical practice in Europe in 1965 (currently, all mainstream technologies for transcatheter heart valves worldwide also originate from Europe). However, it was not until after the year 2000, supported by a substantial body of evidence-based medical data, that the proportion of bioprosthetic valve implants surpassed that of mechanical valves, becoming the predominant choice in developed countries. As illustrated in the figure below, taking Germany—which has the most mature development of cardiac valve therapies worldwide—as an example: Since the turn of the millennium, Germany has witnessed a significant surge in surgical valve procedures, while coronary artery bypass grafting (CABG), once the absolute dominant procedure, has declined year by year. This trend reflects the inexorable impact of population aging. Considering that China’s post-war baby boom occurred approximately 15–20 years later than that of Germany, the author believes thatSince 2020, China's bioprosthetic heart valve market has benefited from the dual tailwinds of expanding market opportunities and policies promoting the substitution of imported products with domestically produced alternatives.

From 1994 to 2019, the total volume of cardiac surgeries in Germany remained virtually unchanged, while the proportional distribution underwent continuous adjustment.

As for the concern among some investors about whether surgical bioprosthetic valves will be completely replaced by transcatheter bioprosthetic valves, the author believes such worries are somewhat excessive.

Based on 20 years of data from Europe and the United States regarding the development of transcatheter aortic valve replacement (TAVR), the volume of surgical aortic valve replacement (SAVR) procedures has not decreased but has continued to increase. Edwards Lifesciences alone generates nearly $1 billion in revenue from its surgical structural heart business. Even in the longer term, the author believes that two key advantage areas of SAVR are unlikely to be replaced:

1. Younger patients around 60 years of age: Extensive research indicates that TAVR does not offer a mortality benefit over SAVR in younger patients; instead, it is associated with higher risks of permanent pacemaker implantation, paravalvular leak, and thrombosis. Consequently, the 2020 ACC/AHA Guideline for the Management of Patients With Valvular Heart Disease continues to recommend SAVR as the preferred treatment for patients under 65 years of age with low-to-intermediate surgical risk aortic stenosis; TAVR is preferred for patients older than 80 years; and for patients aged 65–70 years, the choice of procedure should be based on life expectancy and valve durability.

2. Patients with multi-valvular disease: In a nationwide study led by Fuwai Hospital, among 8,929 elderly patients with valvular heart disease, more than one-third had complex multi-valvular disease. Furthermore, a substantial number of valvular lesions secondary to coronary artery disease were not included in this study. The author believes that the advantage of interventional therapy in minimally invasive treatment of only one of multiple native valve lesions is insufficient to meet the needs of this patient population.

FinallyFrom a product perspective, the domestic market for biological heart valves remains largely monopolized by imported manufacturers, with Chinese-made valves accounting for less than 20% of the market share.As multinational giants such as Edwards Lifesciences introduce their next-generation products to China—particularly the Resilia expandable valve and the sutureless Perceval valve, which are of significant importance for advancing minimally invasive surgery—the market is poised for simultaneous long-term volume growth and gradual substitution with domestically produced alternatives. Notably, the author has learned that domestic startups have products under testing that meet or even exceed international standards.

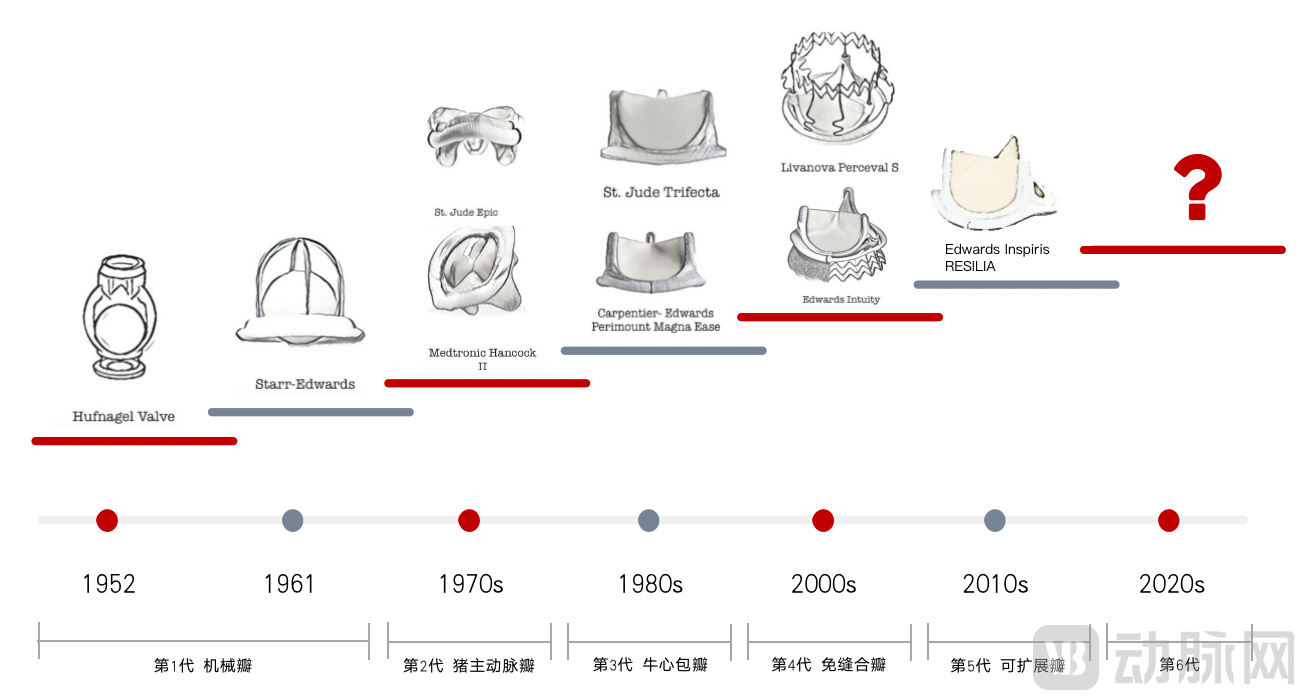

Surgical Bioprosthetic Valve Iteration Roadmap

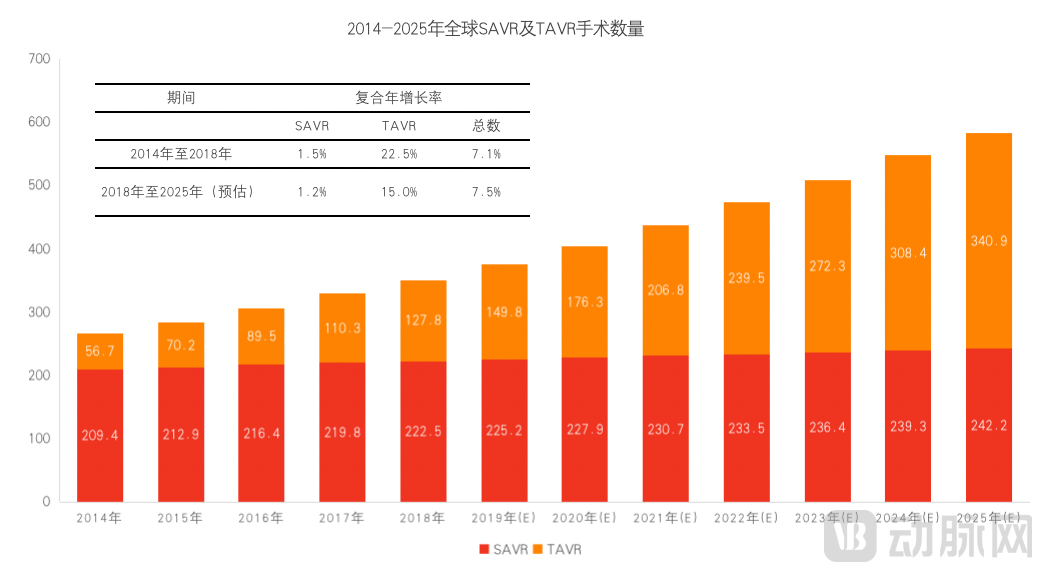

In 2002, the world’s first balloon-expandable TAVR was successfully performed. By 2019, the volume of TAVR procedures in the United States had surpassed that of surgical aortic valve replacement (SAVR). According to Frost & Sullivan, the global number of TAVR procedures increased from 57,000 in 2014 to 128,000 in 2018, representing a compound annual growth rate (CAGR) of 22.5%, with the cumulative global TAVR procedure volume exceeding 600,000. Furthermore, as the 2020 ACC/AHA guidelines listed both TAVR and SAVR as Class I indications, the number of procedures is projected to rise further to 341,000 by 2025, maintaining a robust CAGR of 15%.

Global Forecast of SAVR and TAVR Procedure Volumes

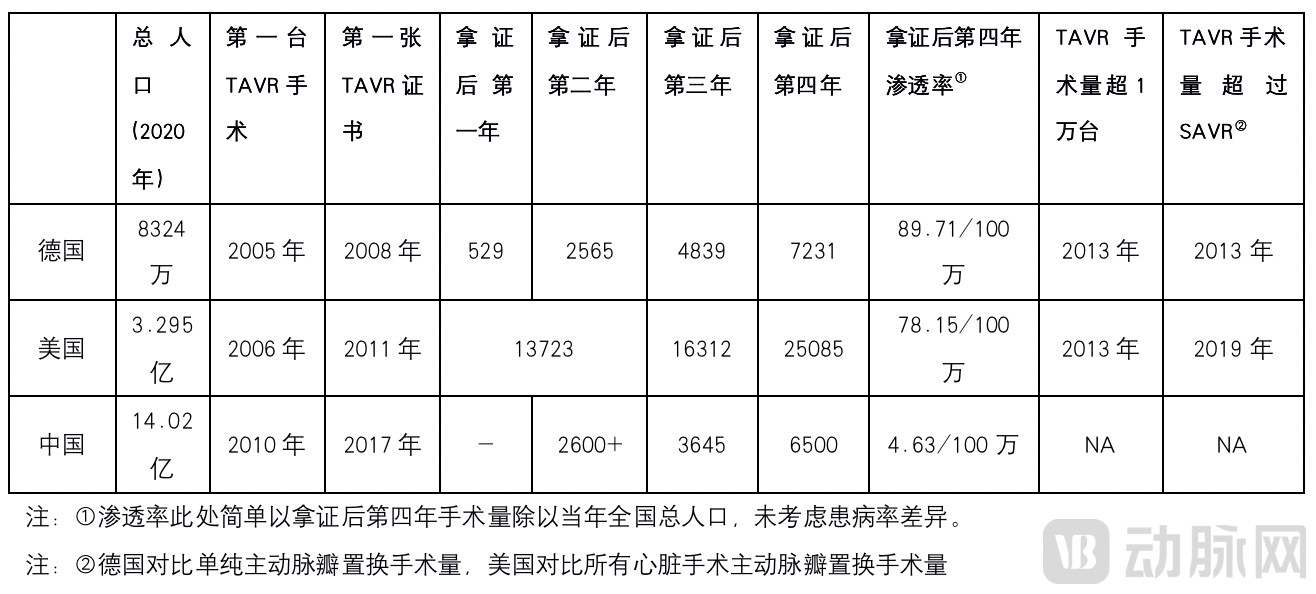

China’s valve industry has lagged behind that of developed countries in Europe and the United States for a considerable period. The first TAVR procedure in China was performed by Academician Ge Junbo in 2010, and it was not until 2017 that the two products VenusA and J Valve were successively approved domestically. To date, the commercialization of TAVR in China has entered its fifth year.

According to data from authoritative medical centers, a total of 3,645 TAVR procedures were performed across all hospitals in China in 2020, with the number projected to exceed 6,500 in 2021. Overall, based on procedure volume—a core commercialization metric—China still lags significantly behind Europe and the United States in terms of absolute case numbers, growth rate, and market penetration.

Development of TAVR Procedures in China, Germany, and the United States

In light of the relatively slow development of TAVR in China, the author believes that there are many reasons, mainly including:

1. The recurring outbreaks since 2020, coupled with the absence of early physician education and on-site proctoring by major foreign manufacturers for TAVR, have hindered the initial promotion of the procedure.

According to industry estimates, the number of physician teams in China that have independently mastered the TAVR procedure does not exceed 30, and a large number of hospitals perform very few such surgeries. According to research published in the Chinese Journal of Thoracic and Cardiovascular Surgery, in 2019, the majority (62.75%) of hospitals in China performed fewer than 20 cases; seven hospitals (13.73%) performed 20 to <50 cases; six hospitals (11.76%) performed 50–100 cases; and only six hospitals (11.76%) performed more than 100 cases. In contrast, by 2019, the United States had 669 hospitals performing TAVR procedures across all 50 states, completing a total of 73,411 TAVR surgeries. The highest-volume center completed 668 cases, with an average of 109 cases per center, and 75% of centers performed more than 50 cases.

Given that the early widespread adoption of percutaneous coronary intervention (PCI) relied heavily on extensive physician education and on-site proctoring by major foreign manufacturers, TAVR in China has directly bypassed this phase, with domestic enterprises assuming these responsibilities. This has indeed placed considerable pressure on these companies, as each TAVR firm is growing alongside physicians.

2. The spectrum of aortic diseases among Chinese patients is more diverse. Existing products are subject to intense involution within single technological pathways, while vast untapped market segments lack products developed through proactive R&D.

Similar to the well-known lung cancer, it not only has different histological classification changes but also a very strict TNM staging. All staging and grading are summaries of many years of clinical experience rather than results achieved overnight. Moreover, they have a direct impact on the treatment and prognosis of each patient.

It is a serious misconception for some domestic enterprises or media outlets to conflate pure aortic stenosis, aortic stenosis with regurgitation, and pure aortic regurgitation under the umbrella term “aortic valve disease,” or to consider that there is “little difference” between trileaflet aortic valves and bicuspid/quadricuspid aortic valve anomalies. In fact, among the tens of millions of patients with aortic valve disease, variations in age, symptoms, access vessels, annular opening, leaflet morphology, coronary artery height, as well as root and vascular calcification are so significant that clinical guidelines provide recommendations based on entirely distinct disease entities.

Given the plethora of classification criteria, the author offers some preliminary insights by adopting a less rigid approach to segmenting the aortic valve market and its current players. It is evident that existing products are subject to intense homogeneous competition. The author believes that further R&D and clinical efforts focused on me-too products yield limited value; instead, the industry should continue to develop innovative products that are more physician-friendly and more effective for patients.

Competitive Landscape of Transcatheter Aortic Valve Products in China

3. TAVR itself has a long learning curve, lacking formal offline mentorship and high-quality surgical assistance for analyzing structural heart disease methods.

Mentally “reconstructing” a patient’s cardiac anatomy based on preoperative CT, ultrasound, or angiographic images, and developing comprehensive contingency plans for a series of issues—including the difficulty of arch navigation, the challenge of crossing the valve, potential coronary artery obstruction, valve migration, paravalvular leak, and conduction block—places extremely high demands on the clinical team. However, the current mainstream preoperative planning software packages, with annual licensing fees approaching nearly one million RMB, are prohibitively expensive for many physicians. Moreover, the 30–40 minutes required for analysis per case further exacerbates the already heavy clinical and research workload borne by Chinese physicians.

The author believes that artificial intelligence technology also holds broad prospects and significant opportunities over the next five years in the highly specialized niche of valvular heart surgery—a market with substantial potential but characterized by a relatively late start, extreme technical complexity, and critical importance of preoperative planning.

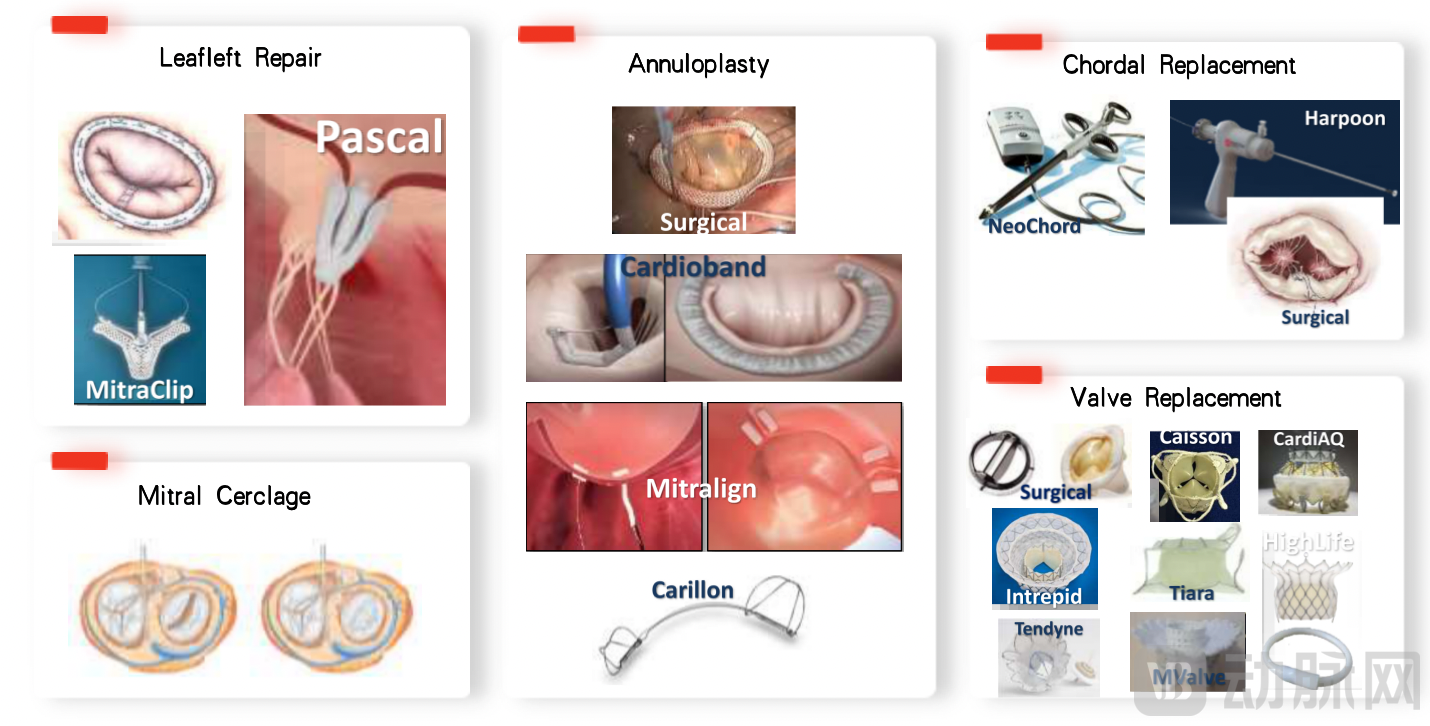

Although this article primarily focuses on advances in the field of valve replacement, any discussion of transcatheter interventions for the mitral and tricuspid valves inevitably involves the MitraClip device.

Following its approval in China in 2020, the MitraClip system officially entered the Chinese market, leveraging global experience from over 100,000 procedures for mitral regurgitation and rapid momentum in treating tricuspid regurgitation. By the end of 2021, it reached a milestone of more than 100 commercial cases in China.

It is worth noting that the NMPA’s approval document for MitraClip states that “the product is indicated for cases of significant symptomatic mitral regurgitation (MR ≥ 3+) caused by primary degenerative mitral regurgitation, treated via a percutaneous approach, in patients diagnosed by a heart team as being at high risk for mitral valve surgery.” We believe that the NMPA’s clear distinction between degenerative mitral regurgitation and functional mitral regurgitation (each roughly accounting for half of cases), along with its emphasis on “significant symptoms” and “MR ≥ 3+,” serves to clearly subcategorize the broad disease class of mitral regurgitation. This also corroborates the author’s previous assertion that the diagnosis of “valvular heart disease” requires rigorous subclassification. Furthermore, the two recent and highly controversial MitraClip studies, COAPT and MITRA-FR, may help us gain a deeper understanding of the importance of diversity within the disease spectrum.

In the fields of transcatheter mitral valve replacement (TMVR) and transcatheter tricuspid valve replacement (TTVR), relevant research worldwide is still ongoing. The technical approaches I have focused on include:

Representative Global Mitral Valve Repair/Replacement Products

The author still recalls the 40 TMVR procedures live-streamed during the 2018 TCT conference, most of which were complicated by immediate post-implantation cardiac arrest requiring on-table cardiopulmonary resuscitation (CPR). Although CPR duration varied from 2 to 20 minutes and most patients achieved return of spontaneous circulation promptly, it became evident that TMVR is by no means simply “TAVR in the mitral position.”

If TAVR improves patient prognosis by replacing the diseased aortic valve, mitral valve disease presents an extremely high level of therapeutic challenge due to its multidimensional pathology involving the left atrium, annulus, leaflets, chordae tendineae, papillary muscles, and ventricle. Successful replacement of the leaflets may have completely uncertain effects on other structures, with numerous cases even showing deterioration. These issues have kept TMVR technology struggling for progress more than a decade after its emergence.

Finally, transcatheter tricuspid valve replacement (TTVR), building upon transcatheter mitral valve replacement (TMVR), further involves implications for multiple systemic organs post-implantation. The author believes that TTVR presents more dimensions and greater complexity than TMVR, and its future resolution will require concerted efforts from physicians and engineers worldwide.

Schematic Diagram of Unicuspid/Bicuspid/Tricuspid Valve Structures

Image source: TCTMD.com

Edwards Lifesciences, the U.S.-born leader in late-stage structural heart disease, has a market capitalization exceeding $70 billion, whereas Chinese capital markets currently assign an unduly low valuation to valve companies. The author believes this is merely a short-term phenomenon, primarily driven by product homogenization and commercialization performance that fell significantly short of expectations, resulting in a temporary Davis double play.

The future Chinese market belongs to products that find the greatest common divisor among medical insurance, physicians, and patients. Such products will undoubtedly come from companies truly rooted in China, with independent R&D capabilities, strong resource integration abilities, and execution power. We look forward to seeing more globally original products emerge in China, benefiting elderly valvular heart disease patients not only in China but worldwide.

References:

1.Carroll JD, Mack MJ, Vemulapalli S, Herrmann HC, Gleason TG, Hanzel G, Deeb GM, Thourani VH, Cohen DJ, Desai N, Kirtane AJ, Fitzgerald S, Michaels J, Krohn C, Masoudi FA, Brindis RG, Bavaria JE. STS-ACC TVT Registry of Transcatheter Aortic Valve Replacement. J Am Coll Cardiol. 2020 Nov 24;76(21):2492-2516.

2. Wei Lai, Chen Nan, Yang Ye, Zheng Zhe, Dong Nianguo, Guo Huiming, Mei Ju, Xue Song, Liu Liming, Guo Yingqiang, Xu Xuezeng, Wang Chunsheng. Statistics on Minimally Invasive Cardiovascular Surgery in China in 2019. Chinese Journal of Clinical Thoracic and Cardiovascular Surgery, 2021, 28. doi: 10.7507/1007-4848.202011075

3. White Paper on Cardiac Surgery and Cardiopulmonary Bypass Data in China (2013–2020)

4.2014-2020 German Heart Surgery Report: The Annual Updated Registry of the German Society for Thoracic and Cardiovascular Surgery.

5. Wu Yunlong, Wang Yin, Dong Nianguo. Reflections in the Era of Valve Intervention—A Surgeon’s Perspective. Chinese Journal of Clinical Thoracic and Cardiovascular Surgery, 2021, 28. doi: 10.7507/1007-4848.202107094.

6. Chinese Society of Cardiology, Chinese Medical Association; Professional Committee on Structural Heart Disease. Chinese Expert Consensus on Transcatheter Aortic Valve Replacement (2020 Updated Edition). Chinese Journal of Interventional Cardiology. 2020;28(6):301-309.