Slowing Healthcare IPO Pace: How Investment Firms Navigate the Anxiety Period

In the spring of 2022, the capital market was fraught with chill, bringing numerous uncertainties to the healthcare industry.

On March 23, First Medicine Holdings, newly listed on the STAR Market, opened below its IPO price, with intraday losses exceeding 22% at one point, before closing at RMB 32.11 per share, down 19.52%. Yihua Pharmaceutical, known as the “first stock in urogenital oncology,” also saw its share price drop by 23.41% on its first day of trading in January.

Faced with the relentless decline in the secondary market, Hillhouse Capital has also taken action. According to Wind data, starting from the third quarter of last year, Hillhouse Capital successively reduced its stakes in several healthcare companies, including Asymchem, Aier Eye Hospital, Tigermed, Hengrui Medicine, and WuXi AppTec.

As stock prices declined, a wave of IPO withdrawals began to emerge. According to data from Choice, more than 70 companies suspended their initial public offerings (IPOs) on the STAR Market and the ChiNext Board in 2022. For many innovative enterprises, the current moment is not favorable for going public. The IPO process for startups appears to have been put on pause.

Data Source: East Money Choice, extracted based on GICS industry classification; companies not classified under GICS Healthcare are excluded.

For entrepreneurs, an initial public offering (IPO) is often the ultimate battle, symbolizing financial freedom, personal achievement, rewards for their teams, and accountability to investors. The fervor of the past seems like it was only yesterday. One investor candidly admitted that although some of the companies in his portfolio had already passed key stages such as stock exchange hearings, his advice was to “postpone and continue observing.”

What exactly is going on?

Unable to list on the STAR Market, hesitant to list on the Hong Kong Stock Exchange: This is the dilemma companies face at this stage.

The relaxation of listing requirements for pre-revenue pharmaceutical companies on the STAR Market and the Hong Kong Stock Exchange’s Chapter 18A has provided capital with opportunities for rapid inflow, value appreciation, and exit.

For a long period, subscribing to initial public offerings (IPOs) in China’s A-share market was considered a risk-free profit opportunity, with first-day trading prices falling below the IPO price (known as “break-even failure” or “price break”) being extremely rare; indeed, not a single such case occurred throughout 2020. However, the listing of many unprofitable companies, compounded by factors such as war, the pandemic, and geopolitical maneuvering, has now made price breaks a common occurrence. The market capitalization and liquidity of smaller companies are cause for concern, and their stock prices face further downward pressure after the lock-up period expires. Consequently, exiting through the secondary market has become a mere distant hope for investment institutions.

Companies Listed on the Hong Kong Stock Market That Broke Below Their IPO Price on the First Day of Trading Last Year Data Source: East Money Choice

A-Share Companies That Broke Issue Price on First Day of Listing Last Year Data Source: East Money Choice

Among the 35 healthcare companies that listed on the Hong Kong Stock Exchange last year, 14 saw their share prices fall below the IPO price on the first day of trading, resulting in a breakage rate of 40%. More than 30 companies experienced a decline in market capitalization over the full year, failing to outperform the relatively weak Hang Seng Index. The situation in China’s A-share market was relatively better, although instances of shares breaking their issue price also occurred.

The decline in stock prices of publicly traded companies in the secondary market has directly led to a 50% drop in valuations for comparable private companies in the primary market, with both investment and fundraising activities experiencing cliff-like declines. “Publicly listed companies in the secondary market that generate revenue and profits are valued at less than HK$2 billion; what justifies this project being valued at RMB 5 billion?” an investor stated that this is the “soul-searching question” he has frequently received from partners recently.

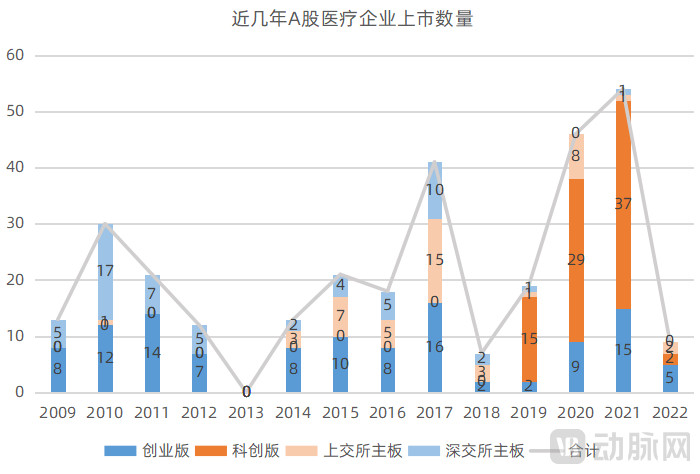

What exactly happened? To answer this question, we must start with the STAR Market. As can be seen from the chart, it was the establishment of the STAR Market in 2019 that triggered the wave of listings among healthcare companies in recent years. However, in February 2021, the China Securities Regulatory Commission (CSRC) issued the Regulatory Rules Application Guidelines—Disclosure of Shareholder Information for Companies Applying for Initial Public Offerings, which explicitly required an extension of the lock-up period for new shareholders and emphasized the completeness and accuracy of information disclosure. In April, the Guidelines for the Evaluation of STAR Market Attributes (Trial) further strengthened and quantified the requirements for technological advancement and innovation on the STAR Market.

Data Source: East Money Choice

Furthermore, among the five listing criteria for the STAR Market, the first set of standards—chosen by the largest number of companies—requires profitability metrics. Specifically, on the basis of a projected market capitalization of no less than RMB 1 billion, a company must either have recorded positive net profits in each of the last two years with cumulative net profits of no less than RMB 50 million, or have achieved a positive net profit in the most recent year along with operating revenue of no less than RMB 100 million. In contrast, the second through fifth sets of criteria focus on operating revenue, R&D investment, cash flow, or product advantages, and do not impose any profitability requirements. This approach helps attract companies with core technological strengths but temporary lack of profitability to apply for listing, thereby addressing weaknesses in the capital market.

“Although the STAR Market operates under a registration-based system, the entire inquiry process has actually tightened control over listing companies, making it not so easy for enterprises. This is particularly true regarding the scrutiny of their scientific and technological innovation attributes. Many questions are difficult for companies to answer, and the issues involved are quite detailed. As a result, many enterprises lack confidence in their ability to successfully list on the STAR Market,” an investor stated in an interview with VCBeat.

These regulations have led many startups to choose the Hong Kong stock market for their initial public offerings (IPOs), a trend further intensified by the relaxation of profitability requirements under Chapter 18A of the Hong Kong Stock Exchange Listing Rules. Taking innovative medical devices as an example, companies in high-demand sectors on the Hong Kong market—such as innovative drugs, heart valves, bioresorbable stents, nerve block therapies, and pulsed field ablation for electrophysiology—tend to prioritize listing in Hong Kong.

First, there are no revenue requirements; second, the capital exit channels are faster. Therefore, whether for company founders or investment institutions, there is a strong desire for a quicker exit path. As a result, investment institutions will generally recommend that companies list on the Hong Kong Stock Exchange whenever they meet the listing criteria.

To some extent, the low entry barriers of the Hong Kong stock market have diverted listings away from the STAR Market and the ChiNext Board, which is also one of the factors contributing to the slowdown in medical IPOs on the STAR Market.

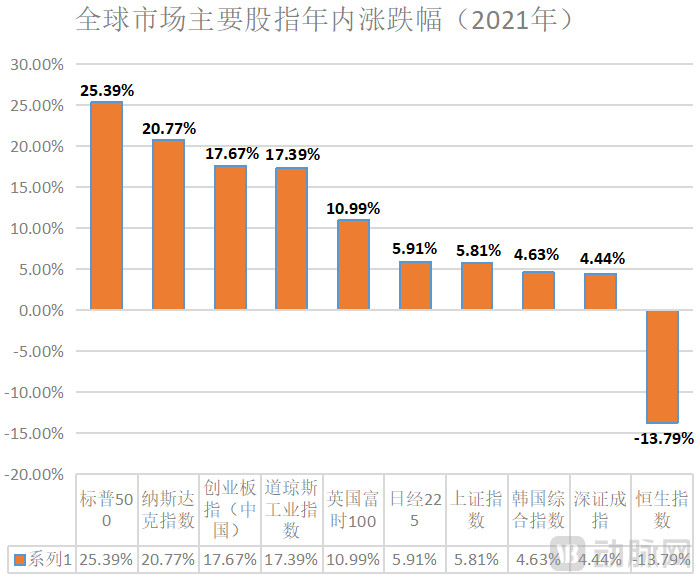

However, the Hong Kong stock market is a highly distinctive one. Throughout 2021, while major global indices posted positive gains, the Hang Seng Index stood out as the only one with a significant decline. Behind the persistent downturn in Hong Kong-listed stocks lies the continuous exodus of foreign capital. According to Choice Financial Data, net outflows from international intermediaries exceeded HK$120 billion over the 20-day period ending March 2022. Wind data shows that, as of April 2021, international and Hong Kong-based intermediaries held approximately 80% of the total market capitalization of Hong Kong-listed shares (based on shareholdings), while the Stock Connect program and mainland Chinese intermediaries accounted for roughly 20%. This implies that pricing power for stocks listed on the Hong Kong Stock Exchange is dominated by foreign investors, who hold an 80% share. The withdrawal of foreign capital has further intensified stock price volatility.

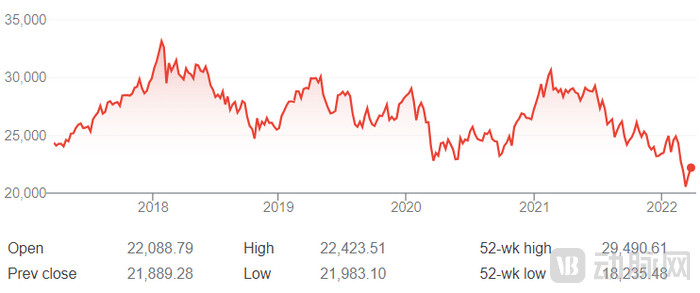

Hang Seng Index 5-Year Trend

Over the past five years, the performance of the Hang Seng Index has also confirmed its current downturn. In 2018, global capital markets experienced severe volatility, with simultaneous declines in both equities and bonds, leading to a near-universal retreat in global risk assets. From its peak during the 2018–2020 period, the Hang Seng Index drew down by 34.5%, while the 37% decline from its high on February 18, 2021, to date has followed an even steeper trajectory. For the first time in 30 years, the Hang Seng Index has touched its 250-month moving average, indicating that the current magnitude of capital outflows from Hong Kong stocks is comparable to that seen during the 2008 financial crisis, with market sentiment extremely pessimistic.

Regarding the current state of enterprises, an investor stated, “The current market conditions have placed many companies in a dilemma: they are unable to list on the STAR Market, and while listing in Hong Kong is feasible, they are reluctant to do so. Many companies had originally planned to submit their filings by the end of last year, but given the unfavorable outlook, they have postponed their plans. This is particularly true for companies with existing revenue and profits; they are in no hurry and can afford to wait until market conditions improve before submitting their applications.”

The leaders in the next phase of niche segments still need time to mature, but the secondary market cannot wait.

“Although the broader market environment has had an impact, the overly rapid pace of IPOs, leaving companies insufficient time to mature, is also a contributing factor,” an investor stated candidly.

Corporate growth requires time and follows a cyclical pattern. Whether in biopharmaceuticals or medical devices, the growth cycle is longer than that of traditional manufacturing or fast-moving consumer goods (FMCG). Consequently, the pacing for initial public offerings (IPOs) follows a similar trajectory.

Taking a Class III medical device as an example, the process from project initiation and recruitment to finalizing product design may take 2–3 years. Subsequently, type testing must be submitted, and clinical trials conducted; for some products, the clinical trial period alone lasts 12 months, followed by patient follow-up and data compilation, meaning the entire clinical phase may take another 2–3 years. Product registration then requires an additional year. Consequently, obtaining approval for a Class III medical device may take 5–7 years in total.

Obtaining the medical device registration certificate is merely the first step. Subsequently, the product must be listed on provincial procurement platforms, and an agency distribution network must be established. Completing nationwide platform listings typically takes over a year, in addition to securing reimbursement codes across the country. For a listing on the STAR Market, the first set of standards imposes requirements on operational metrics, such as achieving annual revenue of RMB 100 million. Reaching RMB 100 million is challenging for medical device sales in their early stages; even assuming a doubling of revenue each year, it would still take three to four years to grow from RMB 10 million to RMB 100 million. Therefore, from a temporal perspective, a company requires a relatively long growth cycle to meet the criteria for an initial public offering.

The objective laws of technological evolution dictate that technology investment entails high barriers and long cycles.

Among the first batch of medical companies listed on the STAR Market, most were established before 2010, or even before 2005. For instance, Huitai Medical was founded in 2002, Weigao Orthopedics in 2005, and Chunli Medical dates back to 1998. These pioneering companies on the STAR Market have accumulated substantial experience and undergone prolonged growth. As leaders in their respective niche sectors, they seized the opportunity presented by the STAR Market to make a breakthrough and achieve a remarkable transformation.

Their successful listings on the STAR Market indicate that they have met the required standards in terms of revenue, product robustness, and the richness of their clinical product pipelines. However, building such capabilities requires time to accumulate. Among the 35 healthcare companies that went public on the Hong Kong Stock Exchange last year, more than half were established after 2015. Time will tell which of them will emerge as the next leaders in their respective niche sectors, but the secondary market cannot wait.

In any industry, the fundamental imperative is to provide customers with valuable products and services; this is the basic logic of business. With high-quality products and the tailwind of favorable policies, a company can soar to greater heights. Conversely, even if it achieves temporary success, it will ultimately suffer a sharp decline.

Consequently, investors have adopted a relatively rational perspective on the slowdown in initial public offerings (IPOs): “From a timeline perspective, the secondary market was quite buoyant following the listing of the first batch of companies on the STAR Market in July 2019 and the subsequent stimulus to the entire healthcare industry driven by the COVID-19 pandemic in 2020. By 2021, the market underwent a correction, making it normal to squeeze out some bubbles. This correction is still ongoing, so the deceleration in corporate listings is understandable. Given that many stocks are currently breaking their issue price upon debut, with some even plunging by half shortly thereafter, such performance is unsustainable for any stakeholder. Therefore, the overall slowdown represents a reasonable choice.”

“Among the companies we have invested in, some have already passed the listing hearing; however, we recommend delaying the offering until the market recovers.”

Currently, the cooling trend in the secondary market has not yet fully transmitted to the primary market. This is because valuation in the primary market is a process that increases with product development progress, whereas the secondary market is influenced by various factors, including investor sentiment, the broader economic environment, policy changes, and sales performance. Consequently, there is a lag in this transmission, requiring time for these effects to fully materialize.

Since the second half of 2021, investment institutions have encountered projects that had announced fundraising plans in the first half of 2021 or in 2020 but had not yet completed their financing rounds and remained lingering in the market. Consequently, many investment firms have determined that the current moment may not be an optimal time for deployment. On one hand, companies in the primary market are maintaining high valuation expectations. On the other hand, investment institutions are prioritizing the management and support of their existing portfolio companies while carefully screening current market opportunities, waiting for suitable moments to invest. At present, most institutions have slowed down their pace of investment.

From the perspective of investment institutions, the selection of investment targets will become increasingly prudent. Only companies backed by robust performance, strong revenue figures with positive growth rates, healthy profit margins, and reasonable valuations will become sought-after projects fiercely competed for by investors. In investment, “when to invest” is just as important as “what to invest in.”

Although these remarks may sound clichéd, several investors have indicated that the emergence of a bubble over the past year or so has significantly impacted the mindset of many founders. With inherently high expectations for valuations, the bubble fueled by a overheated market fostered a sense of impetuosity. A tacit understanding developed between founders and investors: push valuations to a certain level before raising the next round, continuing this pattern until an initial public offering (IPO). After the IPO, both parties would wait out the lock-up period and then cash out their stakes. This mentality has been prevalent over the past year or more.

The cooling of the secondary market will take time to transmit to the primary market, particularly to early-stage projects. However, investment firms have already begun taking precautionary measures. “The most immediate impact is a reduction in investments in later-stage rounds, as deployment has become unfeasible,” an investor told VCBeat.

Investment firms hold project initiation meetings, where they must persuade the Investment Committee (IC) to approve a deal. However, for companies in later funding rounds with valuations starting at RMB 5–6 billion, the IC does not need to delve into technical details. By taking a macro-level view and benchmarking against comparable publicly traded companies, they can pose probing, hard-hitting questions: “What justifies such a high valuation?” and “Can you guarantee that the stock market will rise next year?” Consequently, investment institutions are currently exercising extreme caution when evaluating late-stage projects.

For later-stage financing rounds, some investors have noted that in the primary market, companies can highlight their technological advancements, product innovations, and clinical data. However, once these companies enter the secondary market, the narrative becomes simpler and more straightforward: revenue figures speak for themselves. For companies, however, launching a new product or therapy requires considerable time for promotion and widespread adoption. In the secondary market, any shortfall in sales performance is immediately reflected in stock prices, leaving companies no room to build momentum over time.

For investors, what matters more than when and where to list is how far the company can go after its IPO.

Therefore, after a thorough review, many investment firms have temporarily shifted away from late-stage investments, reaffirming their commitment to early-stage investing. From a cost-control perspective, early-stage investments entail lower costs, thereby offering the potential for significantly higher multiples of return. For instance, investing in a project valued at RMB 1–2 billion may yield an exit valuation of only RMB 5–8 billion upon IPO. After accounting for equity dilution and taxes, the net return would be approximately twofold, which is insufficient to justify to limited partners (LPs).

“Many entrepreneurs remain in a wait-and-see mode, observing whether the downward trend can stabilize. For them, failing to manage cash flow properly would place many R&D-focused companies at significant risk in 2022.”An investor stated candidly.

The current landscape poses significant challenges for entrepreneurs. Following the market boom of the past 18 months, valuations for some companies have been driven to exceptionally high levels. At this stage, valuation is no longer solely determined by founders or management teams, as it involves numerous early-stage investors. Persuading these existing shareholders to accept a down round requires both investors and founding teams to demonstrate broad vision and forward-looking courage—a feat that is far from easy to achieve.

First, for companies with certain cash reserves, a strategy can be adopted—cutting the pipeline.Product pipelines that were aggressively planned during favorable market conditions can be temporarily suspended when the market cools down, ensuring the continued advancement of mature pipelines. The revenue from these mature pipelines can sustain operations for 1–2 years while awaiting a market recovery.

“Perhaps it will take a prolonged slump in the secondary market for their mindset to shift, making them realize that securing funding and ensuring survival are the most pressing priorities at present.”

Secondly, in the challenging market environment, early-stage companies are advised to adopt an agile approach—advancing product development rapidly with comparable resources to reach the next stage as soon as possible, thereby leveraging strong data or key milestones to secure the next round of financing.rather than spending excessive time and energy to raise a large sum of money in the early stages.

“Rather than waiting for market sentiment to improve or guessing when the right time window will arrive, it is better to use this current buffer period to enhance competitiveness and differentiation. Given the broader environment, entrepreneurs should focus more on strengthening their capabilities.”

For investment institutions themselves, some investors have stated that in the future, even if a company successfully completes its IPO, exiting by gradually selling shares in the secondary market will become increasingly difficult. Transactions involving the transfer of controlling stakes, or even mergers between listed companies, will become the mainstream approach. The process of going public is challenging, as it requires financial and legal compliance, along with continued product and business development; furthermore, there remains the risk of post-listing share price declines. Consequently, many investment firms are now opting for phased exit strategies, after all, a successful exit matters more than a successful investment.

In the final pre-IPO funding round, the company’s valuation was set relatively high. A portion of the investment was exited in the primary market beforehand, with the remainder to be exited after the lock-up period expired following the official listing. This approach provides an explanation to limited partners (LPs) for the early partial exit and also helps mitigate the risk of the stock price falling below the IPO price in the secondary market. It serves as a risk-diversification strategy for investment institutions.

Regarding when the IPO environment might improve, investors generally stated in interviews with VCBeat that they currently see no strong driving factors for change, emphasizing the need to tighten their belts and prepare for a prolonged downturn. Some investors also noted that challenging market conditions are precisely when investment prowess is truly tested, expressing hope that entrepreneurs will demonstrate their professional capabilities and impress them with concrete data.

Regarding project selection, investors also have their own perspectives: “The market is like life; it is normal to have highs and lows. Without a phoenix-like rebirth from the troughs, how can the capabilities of an entrepreneurial team be demonstrated? I previously invested in a project where the team lacked an impressive background, and their R&D progress within the industry was not among the top tier. However, two aspects strongly attracted me. First, when the project was on the verge of failure, the team members sold their own homes to support it. Second, their fundraising approach was pragmatic: they raised only the amount needed based on actual project progress, clearly defining what milestone events were required to justify a given valuation and the corresponding increase. Unlike many teams that are impetuous, claiming to double their value in one year and triple it in two, these grounded individuals naturally developed solid products. Currently, this enterprise not only has strong performance in its core products but has also leveraged its robust underlying technology to expand into multiple product pipelines. In challenging environments, rationality is essential.”

Another investor noted that certain consumer healthcare products would be more favored in 2022, such as those in dentistry, medical aesthetics, ophthalmology, and sports medicine. Additionally, while investors previously preferred projects eligible for inclusion in the national medical insurance scheme, they are now exercising greater caution toward projects exposed to volume-based procurement (VBP) risks, given the tightening of medical insurance funds and the expanding scope of VBP. An exception is made for platform-type enterprises. A platform-type enterprise refers to one whose core technology can be applied across multiple indications and product lines. For instance, balloon catheters and guidewires can be used in both coronary neuro-interventional and peripheral interventional procedures. If coronary balloons are subject to VBP, the company can modify its bridging technologies to expand applications into peripheral or neuro-interventional fields not yet covered by VBP. Furthermore, domestic competitive pressure is intense; therefore, projects with overseas expansion strategies—particularly those capable of entering mainstream markets in Europe and the United States, or secondary markets in Southeast Asia, Japan, and South Korea—are more attractive to investors.

In other words, aCompanies with proven performance records hold greater value for investment institutions., its value is primarily reflected in two aspects: first, having a rich product portfolio, and second, the ability to convert these product lines into business performance. An irreversible trend is that, as an enterprise, it is not enough to merely possess promising innovative concepts; the market will also scrutinize the company’s capability to translate innovation outcomes into tangible results.

“Given the current landscape, projects with strong direction, teams, and technology remain scarce. Such projects are highly sought-after and command significant bargaining power, regardless of whether the capital market is hot or cold. Even in today’s financing environment, some projects are even more in demand than before.”

Moreover, over the past year or more, many companies have seen their valuations rise in successive rounds despite no significant changes in fundamentals, allowing investors and founders to realize paper wealth. Now that the market has suddenly cooled and the relay race has come to an abrupt halt, previous valuations must be justified by actual corporate growth.

Looking ahead, numerous investors have stated that it is evident from phenomena such as the slowdown in IPOs, terminated IPOs, post-listing price drops below issue price, and 50% declines in market capitalization that market sentiment toward the healthcare sector is cooling. The bubble surrounding the wealth-creation myth of healthcare IPOs, fueled by the pandemic, is gradually deflating, and individuals and companies involved need to return to normalcy.

An IPO is not the end goal; the ultimate objective is the sustained realization of value.