What's Driving the Surge in Early-Stage Medical Investments? 56 Deals and Over $5.3B Raised in Q1

For investors, the just-concluded first quarter was not particularly conducive to work, primarily due to two factors: first, the Spring Festival holiday from late January to early February; and second, the COVID-19 pandemic, which has persisted since early March and continues to worsen.

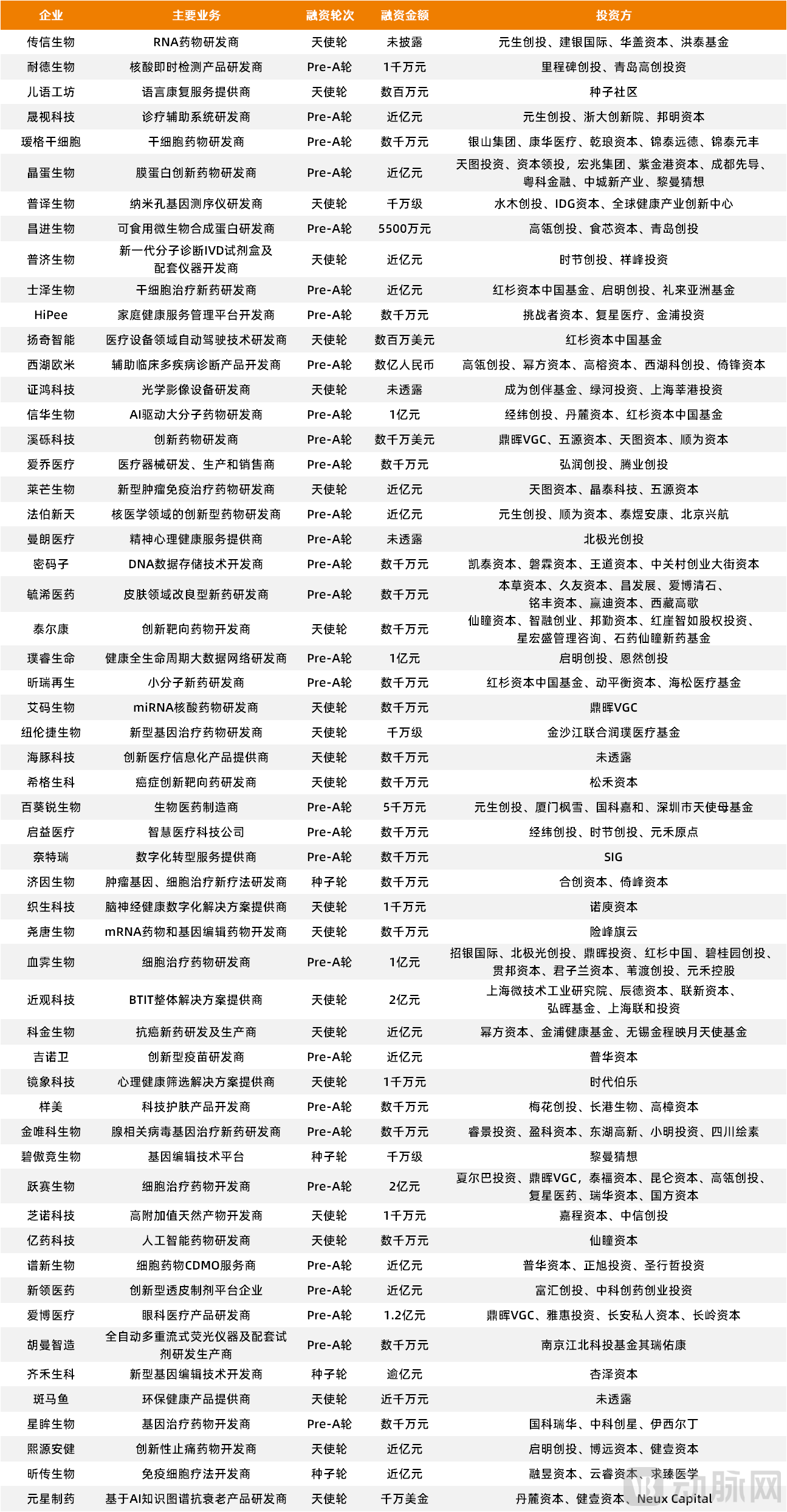

Logically, investors should take this opportunity to “rest,” but in reality, they are working harder than ever before, particularly in investing in early-stage medical projects. According to statistics from VCBeat’s Orange Fruit Bureau, there were 56 early-stage financing and investment events in China’s healthcare sector in the first quarter of 2022, with total financing exceeding RMB 3.5 billion.

If this still doesn’t give you a “jolt,” let’s make a side-by-side comparison of the data. In 2021, there were 59 early-stage investment and financing deals in China’s healthcare sector, with total funding reaching RMB 2.5 billion, indicating that the first quarter of this year has essentially completed the “workload” for the entire previous year.

Additionally, regarding investment proportions, statistics show that in the first quarter of 2022, a total of 160 financing events occurred in China’s healthcare sector, with early-stage financing accounting for 35%, reaching a record high.

While people may deceive, data never lies; every authentic data point strongly reflects the current investment fervor in the early-stage healthcare market. So, what exactly is “hot” in the early-stage healthcare sector? In response, VCBeat’s Orange Fruit Bureau has summarized five major trends.

Trend 1: Scientists Are Making Major Inroads, Raising the Bar for Entrepreneurship

“Scientists Starting Businesses” is becoming a hot topic in the current medical field, as clearly evidenced by the recent actions of many industry leaders who are guiding scientists on how to start businesses.

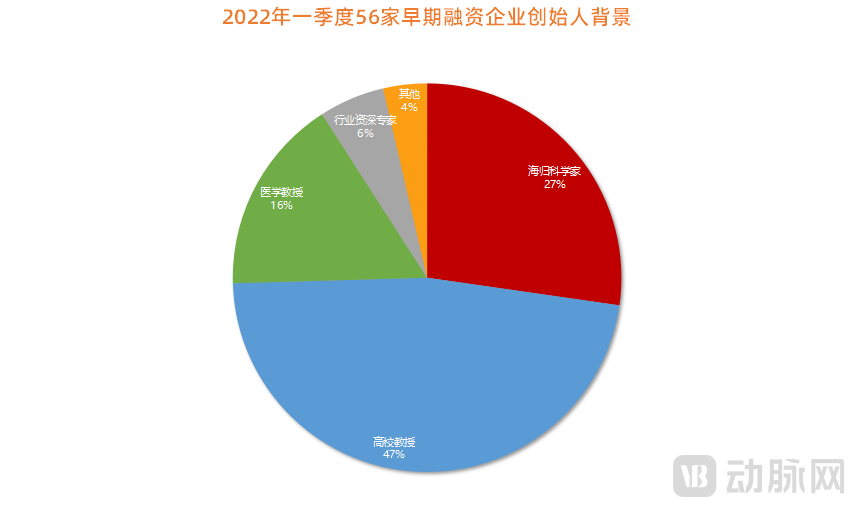

In fact, this is necessary. According to statistics from VCBeat’s Orange Fruit Bureau, among the 56 companies that completed early-stage financing in the first quarter of this year, over 90% of the founders have a scientific background, and most graduated from top-tier domestic or international research institutions.

For instance, Dr. Chen Chang, founder of Jinguan Technology, which completed a RMB 200 million angel financing round, earned his bachelor’s and master’s degrees from Zhejiang University and his Ph.D. from KU Leuven and imec in Belgium.

Another example is Dr. Shi Jiahai, co-founder of Kemexin, which completed a seed financing round exceeding RMB 100 million. Dr. Shi earned his bachelor’s degree from Xiamen University, obtained his Ph.D. from the National University of Singapore, and subsequently pursued further studies at the Massachusetts Institute of Technology in the United States.

Another example is Xige Life Sciences, which completed an angel financing round of approximately RMB 60 million; its founding team all hail from the Dana-Farber Cancer Institute at Harvard University.

This also aligns with the fundamental principles of entrepreneurship in the current medical field. On one hand, research institutes have vigorously encouraged scientists to start businesses in recent years and created a favorable entrepreneurial environment for them, which has, to some extent, motivated a group of scientists to step out of their laboratories.

On the other hand, the healthcare sector is increasingly extending into high-tech domains, meaning that today’s startups require greater “hard” technological capabilities than in the past, thereby raising the bar for founders.

In reality, entrepreneurship for scientists is a process of “survival of the fittest,” with only a very small minority ultimately succeeding, as the transition from scientist to entrepreneur entails a long and arduous journey.

First, a shift in mindset is required, with scientists consciously pursuing entrepreneurship. Second, technological innovation must be driven by market demand, featuring originality and irreplaceability in the marketplace.

Next is the linkage to market resources. Scientists need channels to connect with market resources and must know how to identify and effectively leverage them. Finally, there is corporate management capability, which includes controlling the pace of business operations, recruiting and managing teams, and advancing the commercialization of core products.

This is clearly not an easy task, especially for scientists today, who are constrained by various limitations and find it difficult to master these core competencies in a short period of time.

However, this is not without solutions. Among the 56 companies that completed early-stage financing in the first quarter of this year, many startups have adopted a “scientist + professional manager” team management model, where scientists are responsible for technical research and professional managers oversee corporate operations.

Such “collaborative partnerships” not only help scientists address blind spots when launching startups, but also maximize the complementary strengths of both parties, a trend that is bound to shape the future.

Trend 2: Blurring Investment Boundaries—Early-Stage Investing Is Both a Consensus and a Challenge

Investors are currently chasing after scientists.

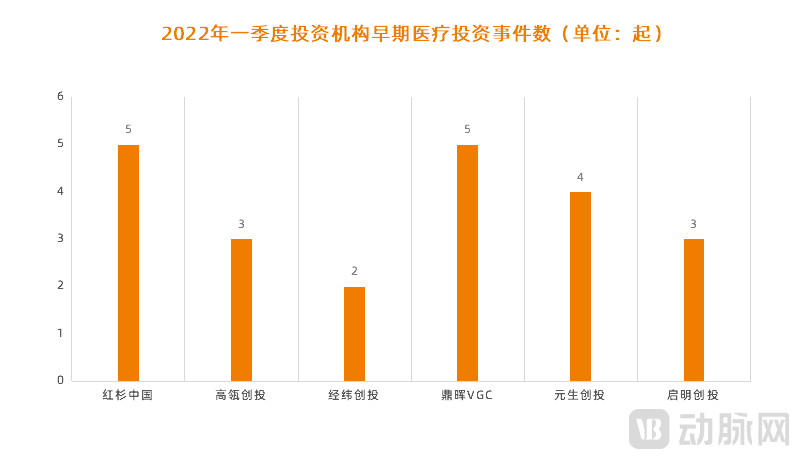

According to statistics, a total of 137 investment institutions participated in the 56 early-stage financing deals that occurred in the first quarter. These investors primarily included well-known firms such as Sequoia Capital China, Matrix Partners China, Hillhouse Ventures, Legend Capital, Yisheng Venture Capital, and CDH VGC.

Among them, Sequoia Capital and CDH VGC were the most active, collectively participating in five early-stage investment and financing deals in the first quarter. Sequoia Capital’s portfolio companies included Shize Biotechnology, Yangqi Intelligence, Xinhua Biotechnology, Xinrui Regenerative Medicine, and Xueji Biotechnology; CDH VGC’s portfolio companies included Xili Technology, Aima Biotechnology, Xueji Biotechnology, Yuesai Biotechnology, and Aibo Medical.

In fact, the shift of investment institutions toward earlier-stage investments is a change forced by circumstances. In recent years, the trend of younger listed companies in the healthcare sector has become increasingly pronounced. Taking 2021 as an example, among the 98 companies that went public, 31 had been established for less than 10 years, indicating a significant compression compared to the previous 15–20 year IPO cycle typical of the healthcare industry.

As going public has become increasingly “easy,” the pace of investment and financing has accelerated accordingly. According to the 2021 Global Healthcare Industry Capital Report released by VCBeat, China’s total healthcare industry investment and financing reached a record high of RMB 219.2 billion in 2021, a year-on-year increase of 32.84%; the number of financing transactions reached 1,362, a year-on-year increase of 77.57%.

It is worth noting that several companies, including Huamai Medical, Mayo Heart Magnetism, Jinyi Shengshi, Yizhun Intelligence, and Caike Biotechnology, have completed two or even three rounds of financing within a single year—a pace far exceeding previous norms.

Therefore, in such an investment environment characterized by “rapid matching,” the boundaries of investment will become increasingly blurred. Investment institutions that previously focused solely on mid-to-late stages will find it difficult to identify suitable entry points; consequently, they will have to shift their focus to early-stage projects and cultivate them from “zero.”

However, for investors, “moving earlier” is not easy; much like scientists launching startups, it presents numerous challenges.

First, how to precisely access scientific resources. Research institutions are relatively closed, and without a "bridge," it is difficult for investors to intervene through intermediaries.

Secondly, how to identify scientist-led projects. Unlike mid-to-late-stage investments, which target relatively mature projects that have been validated by the market, early-stage medical projects are characterized by high uncertainty. Therefore, the evaluation dimensions are more numerous and complex, requiring investors to possess more diversified capabilities in project screening and due diligence.

Next is how to communicate effectively with scientists. Just as most scientists do not know how to interact with investors, investors often lack the ability to communicate effectively with scientists. This issue lies less in the investors’ professionalism and more in their shift in mindset, as today’s scientists may not wish to be “led by the nose” but rather hope to achieve synergy with investors on the project itself.

Finally, how to provide post-investment services for startup projects. For early-stage projects, funding may not be the only important factor; what is more crucial is whether the investment institution can provide them with the necessary market resources, such as team building, product development, and commercialization. This is more valuable than just "money."

Trend 3: Hard tech is the mainstream; high-quality early-stage projects are always “tied” to clinical needs

Regardless of market fluctuations, startups with sustained innovation capabilities will always be “preferred.”

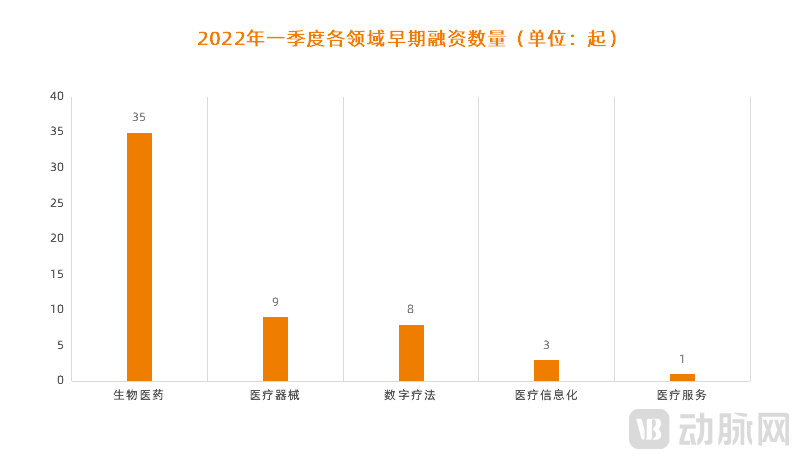

According to statistics, among the 56 companies that completed early-stage financing in the first quarter of this year, 44 were “hard tech” enterprises, accounting for 78.6%. Of these, 35 were biopharmaceutical companies and 9 were medical device companies.

Upon further analysis, more than 70% of these 44 companies are focused on medical sub-sectors with substantial current demand, such as oncology treatment and pandemic testing.

Take Laimang Biotech, which completed a nearly RMB 100 million angel financing round in January this year, as an example. It is a developer of novel tumor immunotherapy drugs based on immune metabolic reprogramming and artificial intelligence, and its product pipeline holds breakthrough significance for the clinical treatment of solid tumors.

In addition, startups such as Sige Biotech, Jiyin Biology, and Kejin Biology are also focusing their efforts on cancer treatment.

Startups must tackle these “hard nuts” because China’s healthcare sector has moved beyond the entrepreneurial era dominated by “domestic substitution” under traditional business models. The low-hanging “fruit” has largely been picked, and future opportunities will inevitably favor innovative enterprises that possess genuine original technologies and can meet clinical needs.

This is, in fact, a straightforward principle. In the current healthcare industry, leading companies have already emerged in virtually every niche sector. Therefore, in such a market environment, startups seeking to capture a share of the market must possess key technologies capable of breaking industry monopolies or driving sector-wide transformation. These technologies must genuinely address clinical needs and exhibit irreplaceability.

A senior investor told VCBeat’s Orange Bureau that “investing early” is not actually about the founders, but rather focuses more on the technology itself and sector selection. This is because many characteristics of founders have not yet manifested in the early stages, making it difficult to predict their future development. Even if founders have “shortcomings,” it is not a major concern, as these can be gradually addressed and improved over time.

However, a company’s “strengths” must be substantial; specifically, startups should target markets with significant growth potential and possess robust technological capabilities, which are the true core drivers of corporate growth.

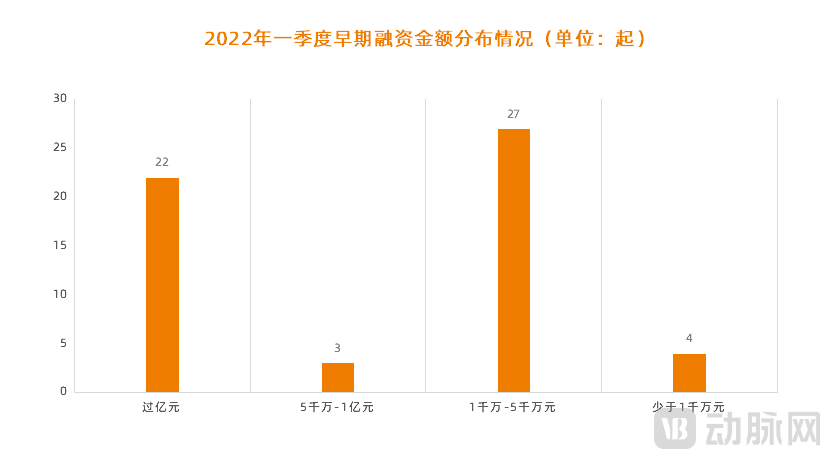

Trend 4: The number of startups valued at over RMB 100 million is increasing; early-stage investment is no longer “cheap.”

Historical data shows that early-stage healthcare financing amounts were mostly in the millions and tens of millions, but now they have “risen with the tide,” with an increasing number of startups becoming “100-million-yuan clubs.”

According to statistics, among the 56 companies that completed early-stage financing in the first quarter of this year, 22 raised over RMB 100 million, accounting for 40%. Among them, NearView Technology, a provider of BTIT integrated solutions, and Yuesai Biologics, a developer of cell therapy drugs, emerged as the most well-funded startups, each raising RMB 200 million.

There are indeed reasons behind the “price increase” in early-stage financing.

First, from the perspective of the investment market. Currently, a large number of investment institutions are flocking to the early-stage market, with the number of investors increasing significantly. However, the number of investees has not grown proportionally, and high-quality startup projects are extremely scarce.

Therefore, “poaching scientists” is becoming the norm for current investors, and in such a “supply falls short of demand” market environment, the “unit price” of investments in startup projects will inevitably rise significantly.

Secondly, from the perspective of the enterprises themselves. Since most current startups are rooted in "hard technology," they inevitably require substantial investment in research and development (R&D). This trend is clearly evident from their use of proceeds: the vast majority allocate early-stage funding to the R&D of their product pipelines.

This is, in fact, a highly sound decision, as R&D is undoubtedly the lifeline of startups and will inevitably drive their future growth trajectory.

As for how to balance the discrepancy between R&D investment and corporate revenue, a senior investor told VCBeat’s Orange Bureau that, at present, both primary and secondary markets recognize the hard-tech innovations of startups. As long as technological and product advancement is ensured, coupled with substantial market potential and room for growth, a one- to two-year delay in reaching the break-even point due to new R&D investments is not necessarily a bad thing. After all, entrepreneurship is a future-oriented endeavor.

Finally, from the perspective of team building. For startups, funding is often not the issue; the challenge lies in building a high-performing team.

This is not only a challenge for founders but also for investors. Therefore, when it comes to “recruiting” talent, startups must not only demonstrate sincerity but also be willing to invest significantly. It is reported that current spending on team building by startups is roughly on par with, or even exceeds, their R&D expenditures.

Trend 5: Research institutions and universities are establishing “self-funded pools,” leading to rapid yet closed early-stage financing.

Currently, research institutes and universities are incorporating more "market elements" into the incubation of early-stage projects.

Several clear trends are evident: first, a shift in mindset, with research institutions and universities gradually moving from resisting the market to accepting it, and even actively participating.

Second, the vigorous recruitment of market-oriented talent. Currently, research institutions and universities have established technology transfer centers, but their staff are predominantly administrative personnel, making it difficult for them to meaningfully engage in specific commercialization activities.

To address this drawback, research institutes and universities are currently intensifying their efforts to recruit market-oriented professionals, primarily including technology transfer specialists, investors, and professional managers.

Third, they are actively establishing their own “capital pools.” To accelerate the incubation of innovative projects, research universities and institutes are currently raising angel funds. The fundraising approaches generally fall into two categories: one is led by the institutions themselves, such as holding funds managed by the research universities and institutes, and alumni funds established by alumni; the other is market-oriented, whereby research universities and institutes select a group of high-quality investment firms to make targeted investments in innovative projects.

Take Shengshi Technology, which completed a Pre-A financing round of nearly RMB 100 million in the first quarter of this year, as an example. Among its investors is the Zhejiang University Innovation Institute, which provides incubation funding for outstanding research teams and scientific and technological achievements at Zhejiang University.

Take Puyi Bio, which completed an angel financing round worth tens of millions of yuan in the first quarter of this year, as another example. Among its investors is Shuimu Ventures, a professional investment institution dedicated to the commercialization of scientific and technological achievements, established under the Tsinghua University Industrial Technology Research Institute.

Looking further back, Lingxin Intelligence, which completed its angel round of financing at the end of last year, received investment primarily from Tsinghua University alumni.

In fact, such early-stage financing models are already highly mature in developed countries, and practical outcomes have demonstrated their significant advantages in incubating early-stage medical projects.

First, it provides scientists with more investment options, reducing the cost of blindly seeking investment institutions; second, it achieves "precise investment," meaning that these investment institutions can provide startups with market-oriented resources that are synergistic with their own businesses.

Finally, it effectively “protects” scientists. Due to their unique characteristics, startup projects are not well-suited for excessive public exposure in the early stages. Therefore, within this relatively closed investment environment, scientists can quickly build trust with investors while also safeguarding the “privacy” of their startups.