Commercializing MedTech Innovation: Reconstructing Ourselves, Deconstructing the Market

Currently, China's healthcare industryIn a transitional phase marked by the rapid evolution and convergence of multiple technologies, and therefore, future opportunities will inevitably arise from interdisciplinary innovation; hence“Integration of Medicine and Engineering”This entirely new model is becoming a consensus among healthcare innovators.

However, this is not easy, and the problems at hand remain obvious. First, from the perspective of the technology itself, there existSignificant Challenges in Integrating Medicine and Engineering, Coupled with Insufficient Capacity for Original Innovationchallenges; from the perspective of market application, there currently existMisaligned with market demand and weak commercialization capabilitiessuch drawbacks. These “adverse factors” have resulted in a remarkably low rate of medical-engineering translation in China.

To address these contradictions, in the new issue of "CNIT Innovation Weekly Talk,"Dr. Chen Yang, M.D. from Peking Union Medical College, startup mentor at multiple domestic clinical translation centers, and senior investorRegarding "“Deconstruction and Reconstruction of the Integration of Medicine, Industry, and Commerce”In-depth sharing on this topic was conducted.

The following areDr. Chen YangTranscript of the Speech, for the convenience of readers,VCBeat Orange BureauThe text has been edited without altering its original meaning.

The Fundamentals of Business: Roles and Positions

When you become a company founder, you must clearly understand your own position and that of the person across from you. The first point to mention here is“Who is sitting opposite you?”。

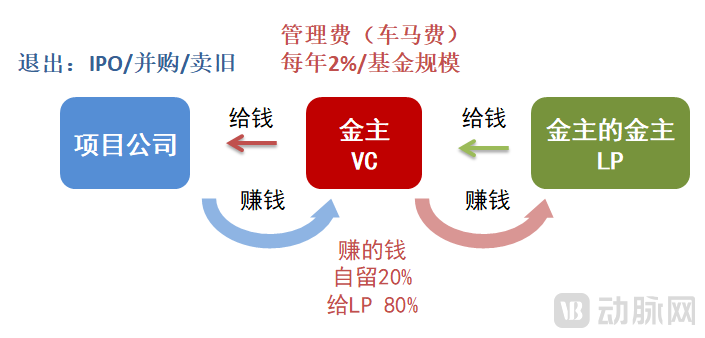

As a company founder, it is inevitable to engage with investors, as securing their favor is essential for the establishment and growth of an enterprise. This primarily refers to early-stage investment, commonly known as VC or venture capital.

Investment Return Diagram

Early-stage investment funds are typically provided by venture capital (VC) firms, but the capital they deploy is generally not their own; they too have their own backers, known as limited partners (LPs).

So, where does the LP's money come from?

Its sources fall into two categories, one of which isHigh-net-worth individuals, such as owners of listed companies or individuals formerly in the real estate sector. These individuals typically hold assets exceeding several hundred million yuan; if each contributes a portion, fundraising can generally be successfully completed.

There is another category thatInstitutional Investors, which are the common "five social insurances and one housing fund," pensions, and social security benefits we typically encounter.Social Security Funds, including commercial insurance productsInsurance Capital, these constitute a major category. In addition, they includeSDIC, CICThese national-level large-scale funds, each with a scale of hundreds of billions of yuan, represent a model in which capital is managed by the state or through larger capital pools.

How do LPs and VCs make money?

For LPs, after providing capital to VCs, they receive an annual return of 2% on the committed capital. Meanwhile, VCs incur relatively low costs, as they are managing other people’s money; once invested in portfolio companies, these companies generate returns throughExit, that is, a model in which funds can be converted back into cash and returned to the VC’s account, thereby generating a certain return.

The exit strategy is essentially what everyone knows as an initial public offering (IPO)., or what is known as "selling old shares," where equity interests are transferred between parties—such as from investors in one round to those in the next—facilitating the reciprocal exchange of ownership stakes. If a project generates a profit of RMB 100 million, the venture capital (VC) firm retains 20%, amounting to RMB 20 million, and returns the remaining RMB 80 million to its financial backers, namely the limited partners (LPs).

Having understood the capital structure and return mechanisms of VCs and LPs, the next question to consider is:How much will your “financial backer” intervene in your operations?

Whether founders or investors,In essence, both parties are engaging in an equity-for-equity swap, but this arrangement is highly intangible; you must be willing to relinquish a certain degree of control.However, everyone may ultimately become deeply concerned that, with equity being divided into many fragments, the company will no longer truly be theirs.

In fact, there are several critical thresholds involved.When you hold more than 51% of the shares, you still have absolute control over the enterprise., it is just that in the later stages of modern corporate governance, different governance structures can be implemented to ensure distinct levels of control for corporate financing, control, and normal operations.

Having identified the counterpart, now return to your own role. At this point, you are no longer a natural person in the legal sense, such as a physician or an engineer, but rather represent an enterprise, with yourself acting as the corporate entity.

This raises an issue of choice; while the two can sometimes be aligned, they may also diverge, necessitatingDoctors Clarify Their Fundamental Roles and Stances。

On the one hand, individuals with a medical education or clinical background often have relatively pure or idealistic motivations, typically entering the profession out of a desire to save lives and heal the wounded. As seen when some physicians embark on entrepreneurial ventures or drive medical device innovations, they tend to be quite idealistic; their primary objective is not profit generation, but rather saving patients’ lives and addressing what they perceive as urgent clinical needs.

On the other hand, if you choose to establish a company, or if you plan to pursue equity financing, you must clearly define the purpose behind the company’s inception.From an economic perspective, the purpose of a company is to pursue profit from the moment it is established., this may represent a completely different developmental path from that of individuals who are genuinely committed to pursuing a career in medicine.

Of course, in addition to understanding one’s own position, it is essential to continuously monitor market trends. Among these, two markets have consistently exerted control over corporate development.One is the industry market, and the other is the capital market.

Let’s begin with the industry market. The healthcare sector comprises numerous distinct subsectors. In the realm of medical devices, for instance, there are stents, catheters, and more. Each subsector represents a separate niche track, constituting an entirely distinct industry market.

Next is the capital market. In fact, from the moment a company begins financing, it becomes a different kind of commodity that is traded or circulated in the capital market. Initially, this takes place in the primary market, which focuses mainly on investment and financing. After the company goes public, it enters the secondary market, i.e., the stock trading market.

After understanding the roles and positions of “who is opposite you” and “who you are,” the next step is to examine your own role, namelyFrom an enterprise perspective, what adjustments are required in one’s mindset?

From an economic perspective, the "rational agent" theory can provide some answers. Economics operates on the assumption that if an individual is perfectly rational, then whether acting as a corporate entity or as a consumer making choices, they would theoretically exhibit several characteristics.

The first one isMotivation. The preceding discussion emphasizes that enterprises are established from the outset to pursue their own interests or maximize efficiency. Similarly, whether in the healthcare industry or the consumer goods sector, all decisions made during product development are aimed at maximizing self-interest.

The second isSelection. That is, when selecting a target, one will inevitably conduct a comprehensive assessment of the potential or tangible costs and benefits associated with achieving that target, ultimately making a choice that maximizes personal benefit. Therefore, in economic activities, when faced with multiple different options, individuals always tend to choose the opportunity that brings them greater economic benefits.

This is the first perspective that needs to be changed, namely, recognizing that enterprises need to make profits and pursue profit maximization. The second perspective that needs to be changed isBottom-uptoTop-Down, meaning that physicians must not focus solely on their technical expertise but should also weigh every aspect related to the enterprise.

Specifically, physicians must transcend their technical silos to observe the broader developmental patterns of the industry, including the evolution of disease spectra, technological advancements, and corporate operational dynamics. Only by aligning strategic business layouts with these macro trends can enterprises achieve success by riding the tide of industry development.

Defining Innovation Value from an Investor’s Perspective

There is a saying in the early-stage investment industry:"Investment is about investing in people"。

Overall, this sentence presents no major issues, but in actual practiceEarly-Stage InvestmentWhen looking at startups before Series A (seed round, angel round, Pre-A round), it is like observing a three-year-old child,At that time, many of his characteristics had not yet manifested, making it impossible to predict his future development.Therefore, it is incorrect to claim that investment is solely about betting on people at this stage. Instead, a systematic evaluation is required to make informed projections about the future of the enterprise or the industry, before returning to the Series A investment decision point to determine whether or not to invest.

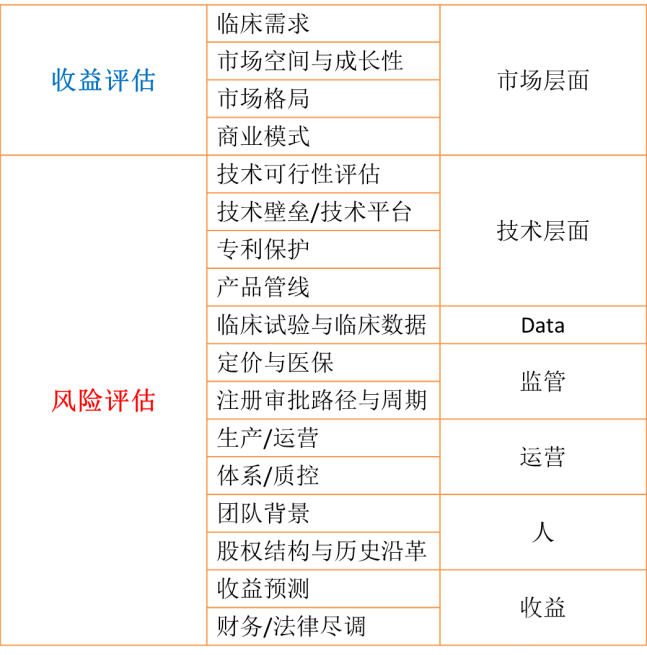

Fundamental Analysis of the Investor Evaluation System

When making early-stage investments, investors generally evaluate startup projects across three dimensions: First, what is the market size and growth ceiling of the specific niche to which the innovative medical device belongs? Second, what market share can the innovative device capture? Is it entering a blue ocean or a red ocean market? What are the barriers to entry and regulatory requirements for market access, and how strong is its core competitiveness? Third, what are the investor’s valuation and investment cost, expected returns, investment horizon, and risk level?

Therefore,At the outset of their venture, founders should take a comprehensive investment perspective, carefully selecting sectors with large market sizes and high growth potential.

This is because, during the earliest stage of building a business from 0 to 1, even the most exceptional entrepreneurs will struggle to revitalize the company if the market is small—much like the saying, “Even the cleverest housewife cannot cook without rice.” Therefore, in the 0-to-1 phase, market and product must take precedence. When selecting different tracks and developing different products, it is essential to assess the total addressable market size.

Thereafter, it is essential to identify products with strong, inelastic demand—namely, those addressing substantial unmet clinical needs. This constitutes the essence of medical innovation and is the key determinant of a startup’s success.

Products with relatively high inelastic demand mostly involve volume and price, i.e.The total volume of clinical applications and the final pricing of the product.In addition, accurate calculations of the target market are essential. Factors such as product-specific inelastic demand, patient population, market size, target market segmentation, and the learning curve for operational proficiency vary across products and must be considered by physicians pursuing innovation.

One consideration is the perspective of vested interests.It is important to recognize that physicians, patients, the entire medical insurance fund (including certain commercial insurance plans), and manufacturers all have distinct interests. From a physician’s perspective, self-assessment is essential: Does your innovative medical device, for example, increase overall bed turnover rates, reduce hospital operational costs, boost outpatient volume and overall efficiency, and shorten the learning curve and associated costs for physicians?

On the other hand, there is the issue of competitive landscape.. The competitive landscape should be examined from multiple perspectives. At times, observers only see the “above-water” players, such as major industry participants and startups. However, there are also “under-the-radar” players that have yet to emerge into the spotlight. These entities may offer different therapeutic approaches, entirely distinct solutions, or alternative technological pathways; they may even represent different products within the same technological paradigm.

In fact, when developing early-stage innovative medical devices, your potential competitors may be competing with you in different directions and may only emerge into the spotlight two or three years later. Therefore, for physicians,Innovation cannot rely solely on sticking to one’s own technological path; it is also essential to listen closely to market signals. Otherwise, there is a significant risk of being overtaken by competitors pursuing alternative technological routes.

Restructuring the Medical-Industrial-Commercial Nexus: Products, Strategy, and Market

“The three characters ‘medicine, industry, and commerce’ can actually be broken down into two questions: one is”“Where lies the focal point of medical-engineering integration?”; the other is“Where is the intersection of medical engineering and business?”?

Developing a completely innovative product must start from clinical needs, but how to define and quantify these clinical needs, and transform them into tangible components of medical devices, remains a major barrier in the current integration of medicine and engineering.

Currently, in medical device innovation, there is a tendency to focus excessively on the tangible aspects—the “form”—such as design angles or curvature, while overlooking the fundamental principles—the “Dao”—including clinical needs, physicians’ practical operational workflows, and the anatomical characteristics of patients’ diseases.

In fact, genuine innovation and R&D should synthesize clinical and patient needs, deriving solutions through forward deduction from first principles (“Dao”), while the tangible components of medical devices are ultimately designed to address these clinical needs.

This also involvesInterface Issues from Clinical Practice to EngineeringMost importantly, physicians and engineers must share a common mindset to speak the same language and jointly develop innovative products.

Based on years of clinical R&D practice,In clinical R&D, it is essential to deconstruct clinical needs into their fundamental underlying elements., only then is it possible to truly engage in engineering-driven innovation. ByUser Requirements Specification (URS)For example, the User Requirements Specification (URS) needs to cover four key aspects: the core of the R&D device, user requirements (patients and physicians), product requirements and performance characteristics, as well as regulatory and approval compliance requirements. If physicians attempt to draft the URS themselves, they can identify previously overlooked blind spots, thereby facilitating more effective communication with engineers.

From the perspective of corporate strategy, there are three levels, namelyMedicine, Market, and Channels。

First is medicine, which involves considering product indications or patient flows before determining which products to develop; second is the market, where indications and patient flows are mapped against the product’s target users and differentiation in clinical practice, with the latter two constituting key considerations at the market level; third is distribution channels, which entails deciding which hospital departments, hospital tiers, and geographic regions to target for product sales.

Among these three levels, the medical level is most relevant to physicians. From a medical perspective, indications and patient flow are defined; at the second level, it is determined which products will be used to address specific problems and in which patient populations; finally, channel considerations are addressed, specifically where the products will ultimately be utilized.

In fact, once the issues at the first two levels are resolved, channel-related challenges will be readily addressed. This constitutes the comprehensive framework for innovative R&D. When integrated with the aforementioned concepts of commercial roles and positions, as well as value assessment, it forms the reconstruction of medical-industrial-commercial integration.