How Google Lost $5.3 Billion in Healthcare: Missteps, Fragmentation, and the Path Forward

Internet-related services and product providers

Recently, Google released its 2021 financial report. In addition to its consistently impressive revenue figures, the company reported a loss of nearly $5.3 billion in non-core businesses such as healthcare. The once highly anticipated Google Health division was also disbanded last year.

Just days before Google released its annual report, IBM, a pioneer among large technology companies in exploring the healthcare sector, sold its underperforming Watson Health division to the private equity firm Francisco Partners. This divestiture comes at a time when tech giants are accelerating their race into the healthcare space, necessitating a reevaluation of how technology companies can sustainably explore the healthcare sector.

We have grown accustomed to tech giants rapidly entering various sectors, empowering them with foundational technologies and creating value. However, in the healthcare field, these tech giants seem to have encountered their own set of challenges. While data sharing clearly offers significant benefits for advancing scientific research, and artificial intelligence has emerged as a novel way to help doctors provide more effective services to patients, the issue remains that tech companies appear ill-suited to the healthcare sector. Today, we take Google as an example, delve into its annual report, and examine how Google lost $5.3 billion over the past year.

Alphabet, Google’s parent company, disclosed its revenue figures for the previous year in its recently released annual report. According to the report, the company’s revenue reached $257.6 billion in 2021, a year-on-year increase of 41%; net income attributable to common shareholders of the parent company was $76.033 billion, representing a year-on-year growth of 88.81%.

Alphabet's Major Revenue in 2021, Data Sourced from Alphabet's Annual Report

Alphabet’s cash reserves increased by nearly $3 billion in 2021, reaching $139.6 billion. However, the numerous antitrust lawsuits facing Google in the advertising and mobile app store markets remain one of the company’s biggest challenges, raising concerns that such regulatory scrutiny could limit its expansion capabilities.

In terms of revenue structure, the primary contributor remains the advertising business, encompassing traditional business units such as Google Search, Gmail, and Google Maps. In terms of growth rate, the most notable surprise is the 45% growth of Google Cloud, which has kept pace with its direct competitors, Microsoft and Amazon. Although its scale still lags significantly behind, it has managed to stay in the race.

Amid these impressive figures, the only less appealing segment is the $750 million “Other Bets” business. “Other Bets” refers to emerging businesses at various stages of development, with revenue primarily derived from the sales of healthcare technologies and internet services.

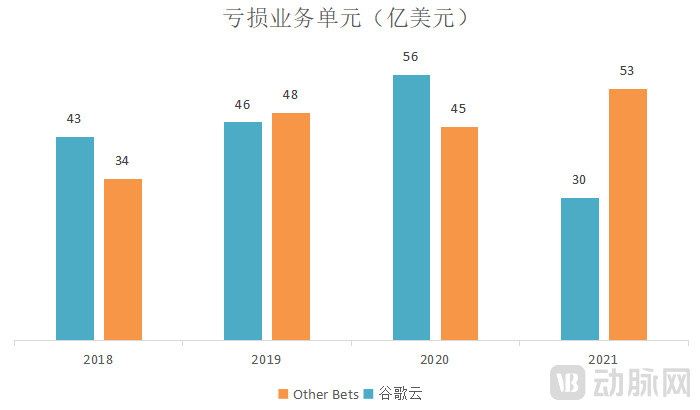

Losses of Other Bets and Google Cloud Over the Past Four Years, Data Sourced from Company Annual Reports

For a behemoth like Google, it is not a major issue if a business unit generates less than $1 billion in revenue; the real concern is the absence of a trend toward profitability. As two of the few loss-making units among Google’s many businesses, Other Bets and Google Cloud have followed markedly different trajectories in recent years.

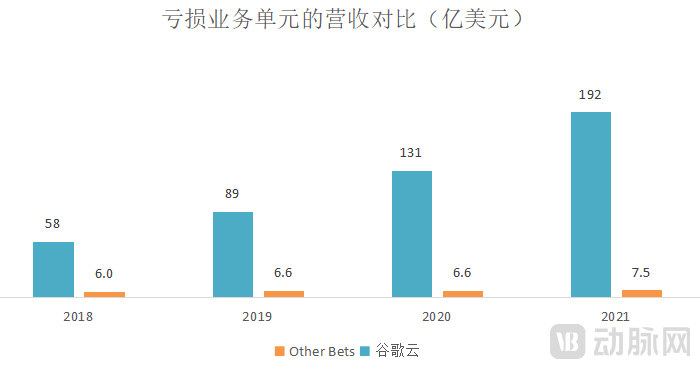

Revenue Performance of Other Bets and Google Cloud Over the Past Four Years, Data Sourced from Company Annual Reports

As can be seen, over the past few years, both Google Cloud and Other Bets have been cash-burning ventures. However, Google Cloud has shown a gradually improving trend, with revenue steadily increasing. In 2021, its losses were significantly reduced by 46%, and its growth rate kept pace with that of its major competitors. In contrast, the revenue from Other Bets has seen no substantial change over the years, while its losses have increased year by year, reaching $5.3 billion (approximately RMB 33.6 billion) in 2021.

Although Google is a massive enterprise, annual losses amounting to billions of dollars are hardly a positive sign. As previously mentioned, Other Bets encompasses multiple business segments, including healthcare. Given that healthcare is a $4 trillion industry in the United States, Google has compelling reasons to remain committed to this sector. Where exactly have these billions of dollars been lost? What factors have contributed to these deficits? These questions warrant in-depth investigation.

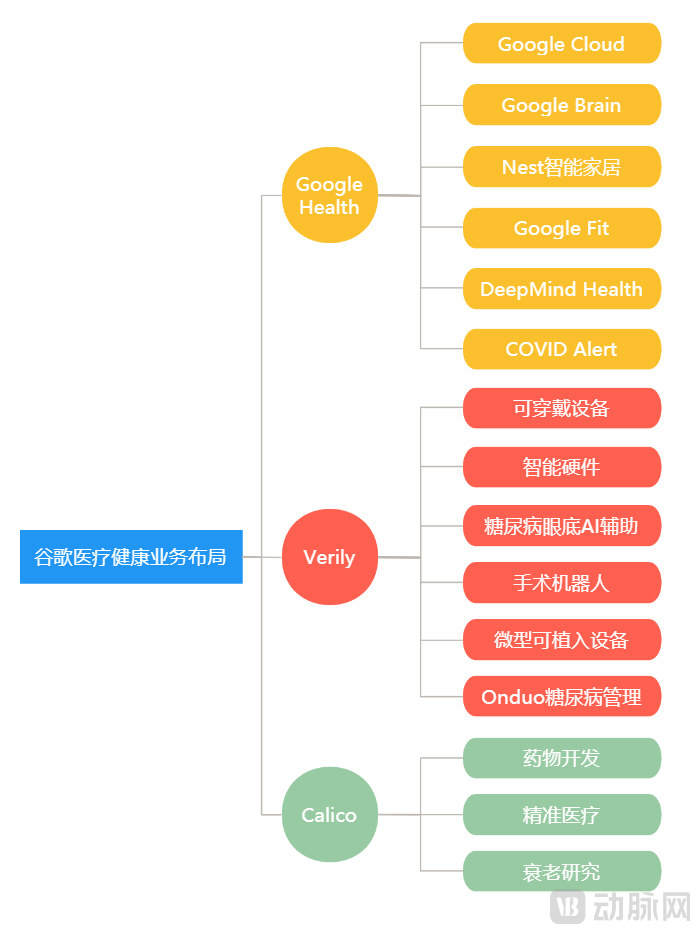

Since 2015, when Google restructured into Alphabet, the new organizational framework has enabled its various businesses to operate relatively independently. It was this adjustment that allowed Google to gradually consolidate its healthcare product lines into dedicated business units. By early 2021, Google’s healthcare operations were broadly divided into three business lines: Google Health, Verily, and Calico.

Let us first clarify the respective strategic layouts of Google’s three business lines. Google Health primarily encompasses Google Cloud’s healthcare services, the deep neural network architecture of Google Brain, Nest smart home devices, the personal health management platform Google Fit, DeepMind, and COVID Alert for pandemic contact tracing. Verily focuses not only on R&D related to diabetes, cancer, and pharmaceuticals, but also on projects involving medical devices such as wearable technology and surgical robots, along with community health management applications and external investments. Calico has a relatively simpler focus, mainly collaborating with pharmaceutical companies to leverage AI technology in developing novel drugs for age-related diseases.

Google's Business Composition in the Healthcare Sector

A further breakdown reveals extensive cross-functional business overlaps.

During the 2015 restructuring, many departments with non-internet businesses became independent subsidiaries under Alphabet. Among them were two hardware divisions with commercialization potential: one was Nest, the smart home company acquired by Google for $3.2 billion; the other was Life Sciences, originally part of Google X Lab, which was later renamed Verily, a life and health company.

Over the years, Verily has made numerous forays into the healthcare sector. For instance, it partnered with Johnson & Johnson to establish a surgical robotics company, collaborated with Dexcom to develop a compact, non-invasive continuous glucose monitor (CGM), and created smart health shoes capable of detecting falls as well as intelligent spoons designed for patients with Parkinson’s disease. Additionally, Verily released 20 million sterile male mosquitoes in the United States to help combat Zika virus infection.

In 2021 alone, Verily devoted considerable effort to its wearable device, the Study Watch, aiming to expand its application scenarios. Meanwhile, Google’s acquisition of Fitbit was finally approved. Notably, Fitbit’s Sense smartwatch, like the Study Watch, features an FDA-cleared electrocardiogram (ECG) function.

In September 2021, Verily’s digital health tool, Onduo, announced that it would provide Fitbit devices to users of its chronic disease management platform. By December, Google further announced that it was developing its own smartwatch, codenamed “Rohan,” to compete directly with the Apple Watch. So, how should we clarify the relationships among Study Watch, Fitbit, and Rohan?

Verily has also entered into a strategic partnership with Colgate-Palmolive to advance oral health research, as part of an initiative known as the Verily Baseline Health Study. In simple terms, the Baseline project aims to map human health by collecting patient data, with its core focus lying on such data. Meanwhile, Google Health has faced significant criticism for its collaboration with Ascension Health, a large hospital chain, due to concerns over the extensive access to patient data involved.

To establish the Baseline clinical trial platform, Verily acquired SignalPath, a remote clinical trial management system. Google also launched Google Health Studies, a health research initiative that recruits Android users to participate in medical studies remotely. Google has collaborated with researchers from Harvard Medical School and Boston Children’s Hospital to conduct a study on acute respiratory diseases using this platform.

Furthermore, Verily and L'Oréal announced a strategic partnership to engage in exclusive collaboration within the beauty sector, driving precision skin health management. Just months earlier, Google announced the use of smartphone cameras to capture skin images, leveraging AI technology to help users address skin concerns.

Not to mention that in the hotly contested field of cancer screening, both Verily and DeepMind (formerly part of Google Health) have established business presences. As early as 2017, DeepMind applied AI-based image recognition technology for breast cancer screening and diagnosis. Verily has not only invested in Freenome, an AI-driven company specializing in early cancer detection, but also built a laboratory for its clinical team.

What is more impressive is that Verily has numerous external investment projects, and even co-invests in Oscar Health alongside Capital G, another investment arm under Alphabet. If Verily’s actions were viewed in isolation as those of an independent healthcare company, these endeavors would be unobjectionable. However, given that Verily is one of the three major business units within Google’s healthcare sector, such practices are open to debate.

Verily, as a company incubated by Google itself, is architecturally independent of Google Health, yet its business operations overlap with those of Google Health. From a corporate perspective, this has resulted in resource wastage. In light of reports from U.S. media in September 2021 that Verily was seeking to spin off from Alphabet to become a fully independent entity, these moves appear justified.

In other words, although Google views Other Bets collectively as investments in the future, it has not fundamentally prioritized them. A company’s organizational structure and its business logic should be mutually permeable, influential, and constraining. Companies establish relevant departments based on the characteristics of their businesses, thereby forming an organizational structure. Once established, this structure in turn influences business operations. Furthermore, technological advancements and changes in the nature of business can render the existing organizational structure inadequate for meeting development needs, necessitating the creation of a new structure. However, Google’s adjustments to its healthcare business have clearly failed to play a positive role.

In terms of impact, the most prominent news about Google in the healthcare sector last year was undoubtedly another failure of Google Health.

Let us briefly review the Google Health incident. On the surface, the immediate trigger was David Feinberg, head of Google Health, leaving to become CEO and President of Cerner, a U.S. giant in electronic health records (EHR). However, a retrospective analysis reveals that beyond the aforementioned business overlaps, the difficulty of commercialization was a significant factor leading to Google Health’s failure. Moreover, this challenge is not unique to Google Health; for Google’s entire healthcare portfolio, achieving successful commercial implementation remains an extremely difficult endeavor.

In the three years following Google Health’s restructuring, the project has continued to operate at a loss. The belief that “technology can unlock wealth” is not only an obsession for Google but also for other major tech giants. The large-platform strategy, in which these giants have traditionally excelled, has not yielded results in the healthcare sector as quickly as they had anticipated.

David Feinberg, the former head of Google Health, stated in a media interview that he was not under pressure to deliver revenue performance but instead focused on generating global impact. However, he also acknowledged feeling the pressure of scale: launching a health product on Google means it will be used by millions of people. This not only subjects the product to intense public scrutiny but also necessitates greater partner involvement and poses challenges in maintaining public trust.

From another perspective, a health product that acquires millions of users upon launch but fails to generate profitability constitutes a failure for any commercial entity.

Not only Google Health, but also Verily seems to have inherited Google’s genetic weakness in hardware development. While they have launched numerous initiatives, very few have achieved commercial success or generated revenue. Products such as smart contact lenses for monitoring diabetes indicators, smart spoons to help Parkinson’s patients control tremors, wearable sensors for multiple sclerosis research, and painless blood-sampling devices similar to watches remain conceptual innovations without translating into actual profits.

Even in a macro environment as favorable to the life sciences as the pandemic, Verily merely launched a website to help governments assess COVID-19 testing, generating little revenue while drawing criticism for information security issues.

Moreover, Google’s AI-powered eye disease detection product, launched in Thailand as the first FDA-approved artificial intelligence diagnostic device, was met with high expectations from both Google and Thai stakeholders. However, the system exhibited significant “acclimatization issues” in Thailand: among the 11 clinics where it was deployed, only two had imaging rooms that met the necessary conditions, and hospital lighting environments were unfavorable for image capture, causing the system to reject more than one-fifth of the images. Rather than improving hospital efficiency, this AI diagnostic system actually increased patient waiting times by two hours.

As for DeepMind, which has been burning cash for years, commercial implementation is even more challenging. No one can deny DeepMind’s prowess in artificial intelligence research, but project deployment is a matter of an entirely different dimension. Streams, the clinical application previously developed by DeepMind, was actively promoted for use in frontline hospitals, yet it was ultimately shut down. Ideals may be full-bodied, but reality is often starkly bare-bones.

Google has long viewed the collection of health data as a natural extension of its core business, fully aware of the immense value of data as an internet giant. To this end, Google has made significant efforts to seek out various partners. However, instead of achieving mutual benefit, these initiatives have ultimately sown seeds of public distrust.

For example, Google Health launched the Nightingale Project and announced a partnership with Ascension Health, a hospital chain operating 2,600 hospitals and clinics. Under this collaboration, Ascension Health will migrate its local data warehouses and analytics environments—including patients’ electronic health records—to Google Cloud, and internally adopt Google G Suite for communication and collaboration.

Although both Google and Ascension Health have stated that the initiative complies with HIPAA (the Health Insurance Portability and Accountability Act privacy rules), the agreement has still faced significant scrutiny. Some industry information experts argue that HIPAA contains loopholes that allow companies to share health data without notifying patients. While such data-sharing arrangements are common in the healthcare industry, Google, as a high-profile company, is subject to the “spotlight effect” and faces far greater levels of scrutiny.

Meanwhile, some media outlets argued that it was clearly non-compliant for Google employees to easily access tens of millions of patient records without strict oversight. Members of the public also contended that the two companies violated relevant regulations by failing to notify patients prior to their collaboration. In short, the interplay between media discourse and public sentiment led to a significant decline in public trust in Google Health, substantially impacting its subsequent development.

Amid these concerns, other companies have also harbored significant reservations about partnering with Google. For instance, Cerner, a healthcare information technology company, once sought a provider to store its hundreds of millions of patient records. At that time, Google offered an exceptionally low “friendship” price. However, Google’s representatives were evasive when answering questions about how Cerner’s data would be used, ultimately leading Cerner’s executives to choose Amazon Web Services (AWS), despite its higher cost.

For Google, driving this deal forward is certainly not about profitability; rather, it aims to further collect, analyze, and aggregate health data from millions of Americans. The failure of the Cerner transaction has unveiled new challenges for Google’s expansion into the healthcare sector: earning the trust of healthcare partners and the public.

For tech giants like Google, clinical data involving patient privacy may be the biggest barrier to entering the healthcare industry. From an R&D perspective, patient data is akin to the blood that fuels the growth of AI-driven medical systems; tech companies aim to leverage this data to build intelligent platforms that deliver value to both patients and the healthcare system. However, as public awareness and concern over personal data privacy and security continue to rise, striking a balance between the “openness” of big medical data and “privacy” protection has become an urgent issue to address.

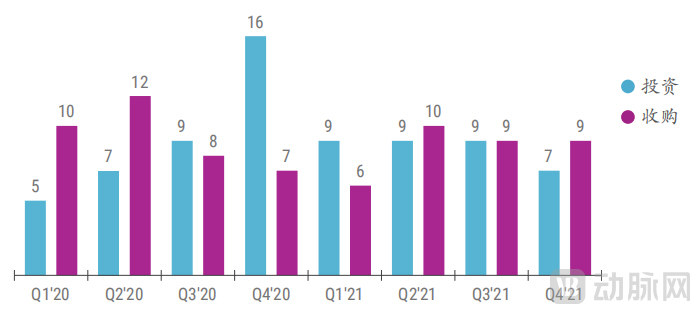

The overall acquisition trend among the five major U.S. tech companies—Google, Microsoft, Amazon, Apple, and Facebook—has begun to slow down. The number of external equity investments stabilized in 2021 after fluctuating in 2020.

For years, these five tech giants have been waving their checkbooks to acquire apps and companies one by one, expanding their own business ecosystems. However, as their strategic layouts have become more complete, their pace of external acquisitions has begun to slow. In 2021, these five companies carried out a total of 34 acquisitions, the lowest number in the past five years. Google made only eight acquisitions over the past year.

Number of Overseas Investments and Acquisitions by the Five Major U.S. Tech Giants Over the Past Two Years, Data Source: CB Insights

In 2021, Google’s acquisitions demonstrated clear strategic intent, as exemplified by its purchase of Tempow, a French Bluetooth software solutions company. As a member of the Bluetooth Special Interest Group (SIG) and a key participant in the Bluetooth Audio Subcommittee, Tempow holds numerous Bluetooth-related patents and possesses a complete Bluetooth protocol stack capable of seamless operation across all chip vendors.

In addition, Google acquired Provino Technologies, a company that develops Network-on-Chip (NoC) systems for machine learning. NoC is a chip communication architecture that enables TPUs to perform machine learning tasks efficiently, thereby driving the evolution of AI.

Looking back to early 2021, when Google’s acquisition of Fitbit finally received approval, these acquisitions—underpinned by Bluetooth and AI technologies—highlighted Google’s ambitions in the wearable device sector.

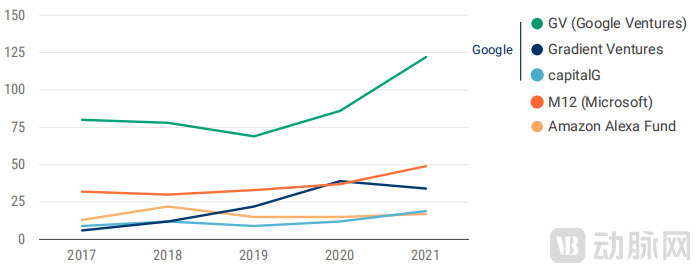

Annual Number of Investments by Specific Venture Capital Arms of Tech Giants Over the Past Five Years, Data Sourced from CB Insights

In terms of outbound investments, Google’s direct investment volume has decreased by approximately half compared to 2020. This does not indicate a weakening of its investment momentum; rather, its parent company, Alphabet, has shifted the majority of its investment activities to other subsidiaries, such as Google Ventures (GV), Gradient Ventures, and CapitalG.

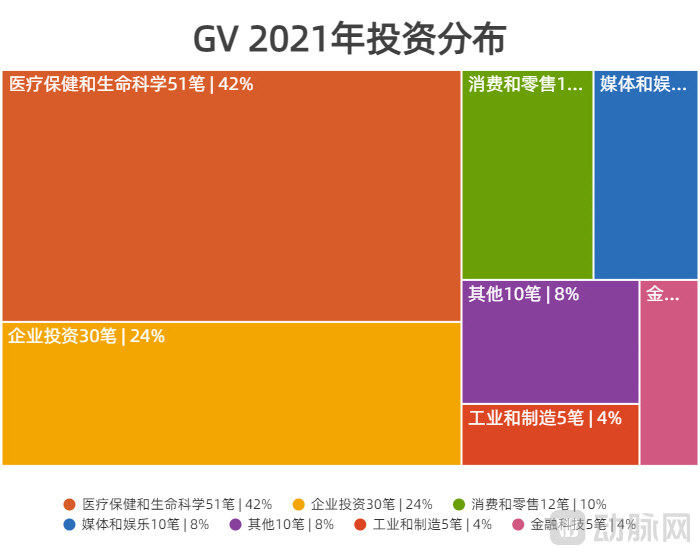

GV 2021 Investment Distribution, Data Source: CB Insights

Thus, Google’s standalone investment performance in 2021 appeared unremarkable, merely serving as a necessary supplement to its overseas markets. However, a categorized analysis of GV’s investment portfolio reveals that nearly half of its projects were allocated to the healthcare and drug development sectors.

For example, GV participated in the Series A and Series B financing rounds of EQRx (short for Equal Quality Rx), a biopharmaceutical company. It also invested in the Series C round of Adagio Therapeutics, a developer of antibody therapies for COVID-19, and participated in the Series C financing of insitro, a startup leveraging machine learning to drive drug development.

In addition, GV has also invested in Dialpad and Cockroach Labs on the cloud platform. Dialpad is an AI-driven enterprise-grade cloud instant messaging platform that offers a variety of services including remote conferencing and call centers. Cockroach Labs, on the other hand, is well-known in the industry for its cloud-native database, CockroachDB.

GV’s investments last year indicate that, despite a $5.3 billion loss and another setback for Google Health, Google will not abandon the healthcare industry in the foreseeable future.

After weathering the turmoil of massive losses and project failures, Google promptly adjusted its strategy. In 2022, Google may have focused its attention onPatient Data、Facilitating Clinical Trial PlatformsandAI Drug DevelopmentAbove.

In the future, healthcare will be centered on consumer experience, and for any company, privacy and security constitute an insurmountable barrier. Having weathered a privacy scandal, Google has clearly learned its lesson, quietly adjusting its data acquisition strategy.

GV’s 2021 Investments in Startups with Patient Data, Sourced from VCBeat Orange

VCBeat reviewed GV’s overseas investments in 2021. Of the total 51 investments in the healthcare sector, 16 were directed toward startups possessing patient data. In addition, Google has successively entered into collaborations with U.S. hospital chains HCA Healthcare, Highmark Health, and Mayo Clinic to leverage patient records for healthcare research and development. Google aims to reassure the public that it will not cause privacy data breaches by relying on these professional medical institutions’ steadfast commitment to data privacy. Even the previously controversial partnership with Ascension will continue to move forward after both parties redesigned the collaboration framework.

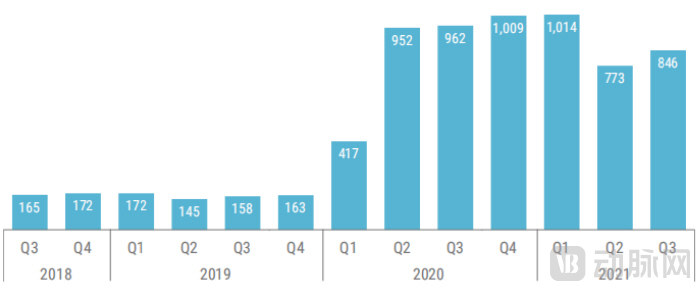

The Number of Mentions of “Remote Clinical Trials” in U.S. Media Before and After the Pandemic

Catalyzed by the pandemic, U.S. healthcare institutions have been compelled to seriously consider the feasibility of decentralized clinical trials. For them, effectively reaching patients poses a significant challenge. However, bridging information gaps is a core competency for Google, presenting no particular difficulty. As previously mentioned, Google Health Studies and SignalPath, acquired by Verily, are both platforms for managing decentralized clinical trials.

Furthermore, Google possesses Verily’s Study Watch, Fitbit wearable devices, and its own smartwatch under development, codenamed “Rohan.” These technologies can provide effective support for remote physiological monitoring of patients and achieve full integration at the data level with remote clinical trial management platforms. This holds considerable appeal for healthcare institutions.

For patients participating in clinical trials, their involvement is in projects conducted by formal medical institutions, eliminating concerns about Google leaking privacy; for medical institutions, Google’s platform reduces their costs; for Google, accessing more medical institutions and clinical projects through this platform, expanding the application boundaries of wearable devices, and obtaining patient data are all more valuable than the revenue generated by the platform itself.

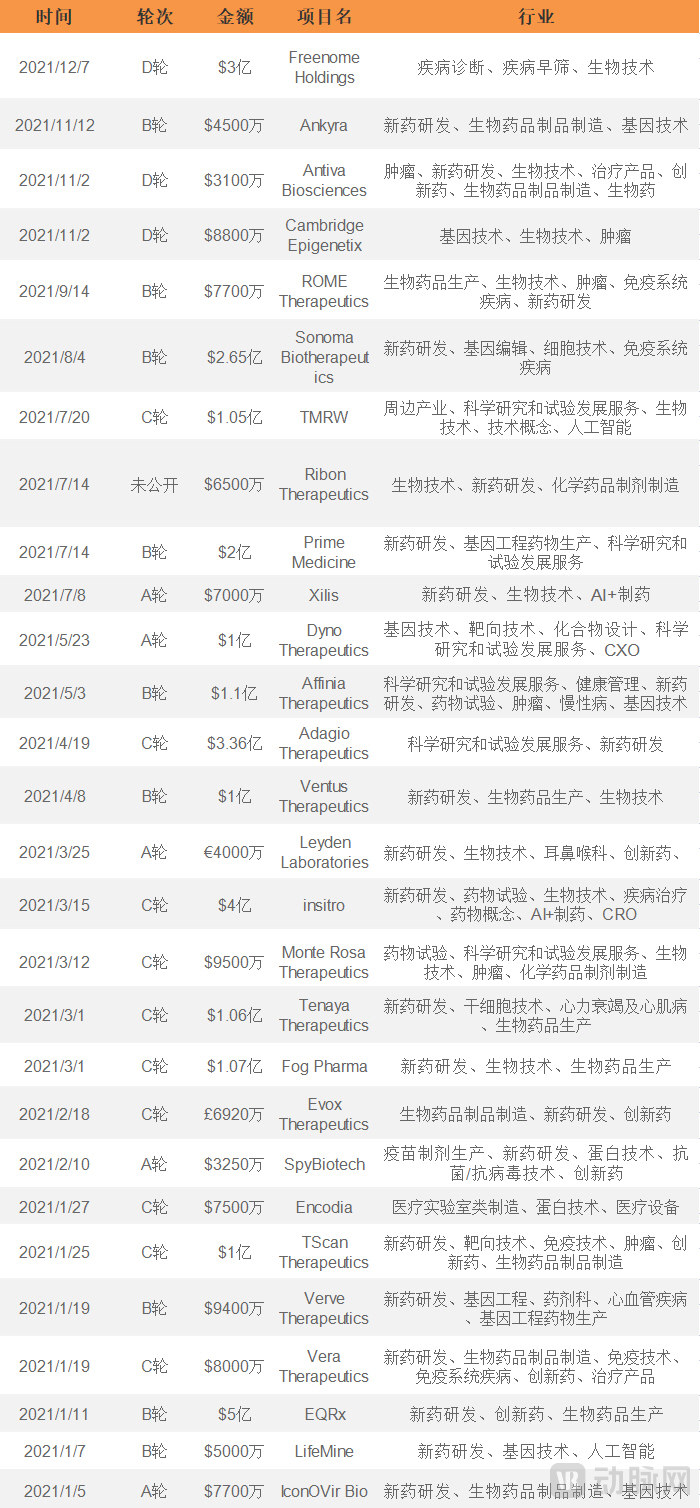

GV’s Investments in Drug R&D Startups in 2021, Data Source: VCBeat Orange

AI-driven drug discovery will also be a key focus for Google in the near future. This assessment is based on GV’s outward investment strategy, as 28 of its 51 healthcare investments this year were in drug development, accounting for more than half.

In addition to the well-known AlphaFold 2 project, Demis Hassabis, CEO of DeepMind, announced in November 2021 the establishment of Isomorphic Labs, a new subsidiary of Alphabet. The new company aims to rebuild the entire drug discovery process using artificial intelligence, modeling and understanding the fundamental mechanisms of life.

Furthermore, Calico should not be overlooked. In partnership with the pharmaceutical company AbbVie, it has launched more than 20 early-stage projects in the fields of oncology and neurology, which are closely linked to aging. Under the terms of the latest agreement between the two parties, their collaboration will be extended by three years beyond the 2022 baseline. Calico will be responsible for research and early development through 2025, and for advancing collaborative projects to Phase 2a by 2030. AbbVie will continue to support Calico’s early R&D efforts and will decide whether to take over late-stage development and commercialization activities after the completion of Phase 2a trials.

Large technology companies like Google have a core mission to sell their products and services to as many industries and customers as possible, viewing the healthcare sector as a significant future business opportunity. By all accounts, these tech giants have performed well in marketing their core offerings. However, unlike technology firms specifically focused on healthcare—particularly electronic health record (EHR) companies—healthcare initiatives receive relatively limited attention from senior leadership within large tech corporations, meaning they are allocated only a fraction of the company’s overall resources. It is unrealistic to expect success in a $4 trillion industry without a coherent, enterprise-level strategy.

Moreover, big tech companies are accustomed to solving all problems in-house, but healthcare is a fragmented industry. While it might be theoretically possible for big tech firms to address these issues systematically at the national level, such an approach remains impractical. Patients value their relationships with physicians—trust built over decades and across generations. For big tech companies that have only recently entered the healthcare sector, the lack of such established relationships results in a deficit of user trust.

In the long run, change is inevitable, a trend already evident in the success of many digital health enterprises. Perhaps tech giants like Google need to learn to think like startups born and bred for healthcare, figuring out how to establish their foothold in this $4 trillion market. However, this is a move most large technology companies are unwilling or unmotivated to make. Google has made its own adjustments, and its developments in the healthcare sector over the coming year warrant our continued attention.