Revenue Surge Amid Persistent Losses: How Far Are China's Biotechs From Becoming Biopharma?

In 2021, biopharmaceutical companies achieved a surge in operating revenue, with some even doubling their figures. This once again demonstrates that the earliest batch of domestic biopharmaceutical companies has entered an exciting harvest period following the market launch of their core products.

Yet, in the face of such data, the secondary market remained calm, adopting an attitude of sheer complacency.

Revenue of Selected Biopharmaceutical Companies in 2021 (Unit: CNY; CNY/USD Exchange Rate: 1:0.16)

Amid the continuous decline of the biopharmaceutical sector over the past six months, the secondary market has by no means lowered its expectations for biopharmaceutical companies. This pressure from the capital markets is driving companies to rush toward their next milestone. Where does this new milestone lie? Thus, between Biotech and Big Pharma, the industry has identified a new stage of development: Biopharma.

So, have these Chinese biotech companies become biopharmas?

Diversified Commercialization Strategies

Toward the goal of becoming biopharma companies, Chinese biopharmaceutical enterprises have formed distinct tiers in terms of revenue scale.

Three Companies That Started with PD-1 Monoclonal Antibodies

At the forefront of the journey toward becoming global biopharmaceutical companies are BeiGene, Innovent Biologics, and Junshi Biosciences—three innovative pharmaceutical firms that built their foundations on PD-1 inhibitors.

Over the past few years, the three companies have gradually diverged in their commercialization strategies, while remaining aligned in other areas.

BeiGene’s commercialization strategy is comprehensive globalization.Building on the PD-1 inhibitor Baizean (tislelizumab), BeiGene continues to expand its commercial footprint. By the end of 2021, BeiGene’s commercial product portfolio had grown to 16 products, with its self-developed Baizean (tislelizumab) and in-licensed products such as Revlimid and Xgeva maintaining steady revenue growth. The fastest-growing contributor, however, was Brukinsa.

Driven by John Oyler’s influence, globalization is embedded in BeiGene’s DNA. More than half of Brukinsa’s sales, amounting to $115 million, came from the U.S. market. Sales of Brukinsa in the United States were conducted entirely through BeiGene’s in-house team. Propelled by products such as Brukinsa, BeiGene’s product revenue reached approximately RMB 4 billion in 2021, representing a year-over-year increase of 105%.

Junshi Biosciences has also performed strongly in overseas markets; however, unlike BeiGene, which built its own international team, Junshi Biosciences opted for an aggressive out-licensing strategy.Of Junshi Biosciences’ total revenue of RMB 4.025 billion, overseas income accounted for the largest share, with foreign revenue reaching RMB 3.341 billion, a year-on-year surge of 562.66%, primarily driven by licensing revenue from the COVID-19 specific therapeutic antibody etesevimab. This figure underscores Junshi Biosciences’ outstanding performance in overseas commercialization.

In contrast, Tuoyi (toripalimab), once Junshi Biosciences’ flagship product, performed slightly less impressively, generating only RMB 412 million in revenue in 2021. This outcome was also attributable to adjustments in Junshi Biosciences’ commercialization strategy in 2021.

Perhaps emboldened by its success with etesevimab, AstraZeneca partnered with Junshi Biosciences in February 2021, securing the rights to promote Tuoyi in non-core markets within China. However, by December 2021, Junshi Biosciences had reclaimed these rights. In light of Tuoyi’s overall sales performance in 2021, this collaboration between the two companies likely failed to achieve a synergistic effect greater than the sum of its parts.

Innovent Biologics continues to focus on the domestic promotion of its PD-1 monoclonal antibody, Tyvyt (sintilimab), which has resulted in Tyvyt’s sales significantly surpassing those of Baizean and Tuoyi.Innovent Biologics’ product revenue reached RMB 4 billion, with Tyvyt contributing 70% of this amount.

Innovent Biologics’ decision stems from its determination to develop Tyvyt. To date, Tyvyt has received approval for four first-line indications, the highest number among the four PD-1 monoclonal antibodies covered by China’s National Reimbursement Drug List (NRDL). Furthermore, new drug applications (NDAs) have been submitted for additional first-line indications in gastric cancer and esophageal cancer, as well as a second-line indication in EGFR-mutated lung cancer. This positions Tyvyt with the potential to become a blockbuster drug.

Innovent Biologics’ other revenue streams are derived from biosimilars and licensed-in products. Unlike BeiGene, which focuses more on channel-oriented licensed products, Innovent’s licensed-in products, such as olverembatinib tablets and Taibentan (pemigatinib tablets), are more oriented toward collaborative research and development.

There is no inherent superiority or inferiority in the current strategic choices made by these three companies; each has simply prioritized areas better suited to its own strengths. However, to transition from a biotech firm to a biopharma company, their business models must become more diversified. Signs of such diversification are increasingly evident across all three enterprises.

BeiGene has gradually begun to out-license its products, including granting Novartis partial rights to its TIGIT monoclonal antibody and partnering with pharmaceutical companies worldwide for the commercialization of zanubrutinib. Junshi Biosciences refocused on Tuoyi (toripalimab) in late 2021, appointing Li Cong as Co-CEO to prioritize breakthroughs in county-level markets. Meanwhile, Innovent Biologics has started making inroads into the global market; although it has encountered some setbacks, these are not significant, as we previously analyzed.

As the business models of these three companies begin to converge, ultimately forming a multi-pronged structure encompassing the domestic market, overseas markets, out-licensing, and in-licensing of products, they move one step closer to truly becoming biopharmaceutical companies.

Henlius: From Biosimilars to Innovative Drugs

Following closely behind the three PD-1 companies is Henlius.

Henlius, with a focus on biosimilars, experienced rapid growth in 2021. Its revenue primarily stemmed from sales generated by the commercialization of multiple products and licensing income. The company’s flagship product, Hanquyou (trastuzumab), emerged as the most prominent driver of performance growth in 2021. In the Chinese market, Hanquyou was the first product for which Henlius established its own commercial team to handle sales and promotion. This team’s efficient market deployment laid a solid foundation for the comprehensive increase in Hanquyou’s sales volume.

Over the past two years, Henlius has been striving to transition from developing biosimilars to innovating novel drugs, with a focus on creating differentiated products. Its PD-1 inhibitor, HANSIZHUANG (serplulimab), was approved for marketing in March 2022 as a monotherapy for unresectable, metastatic microsatellite instability-high (MSI-H) solid tumors after failure of standard treatment, becoming the first domestically produced “pan-cancer” PD-1 inhibitor in China.

Amidst the fiercely competitive landscape, with six PD-1 products already launched in China and over 4,000 global clinical trials on PD-1 inhibitors underway, Henlius has carved out a differentiated path by focusing on “pan-cancer” indications, thereby securing a strong foothold in the PD-1 market. This strategic differentiation, coupled with its prowess in channel sales, positions Henlius with greater potential to catch up with the industry’s first-tier players.

Enterprises Focused on Specific Fields

Other companies, though not yet achieving scale in sales volume, are also on the path to becoming biopharma enterprises.

As an innovative pharmaceutical company whose primary business model is license-in, Zai Lab, despite not having the highest total revenue among the eight companies, achieved rapid product monetization with growth approaching twofold. According to its financial reports, sales volumes of Zai Lab’s three main products—Zejuca, Optune, and Qinlock—continued to increase in 2021, with their respective sales revenues reaching USD 93.58 million, USD 38.90 million, and USD 11.62 million.

Canbridge Pharmaceuticals, which focuses on treating rare diseases, and Ascletis Pharma, which specializes in developing therapies for viral diseases, are also catching up in the commercialization of their marketed products. Although there is a cliff-like gap in revenue compared to other companies, they have carved out their own niche by leveraging differentiated product pipelines.

Among them, Canbridge Pharma’s Hunterase, a treatment for Hunter syndrome, entered the Chinese non-reimbursed market in May 2021, marking the beginning of Canbridge Pharma’s commercialization efforts. As for Ascletis Pharma, although its original hepatitis C drug missed the opportunity to be included in the national reimbursement list in 2019, dealing a severe blow to its commercialization prospects, the COVID-19 pandemic may help turn the tide. With Pfizer’s COVID-19 antiviral drug Paxlovid approved in China, Ascletis Pharma is poised to become a key supplier of ritonavir tablets for this combination therapy. Currently, Ascletis Pharma has expanded its annual production capacity of ritonavir tablets to approximately 530 million tablets and has submitted marketing authorization applications to 12 European countries through distributors. The springtime of Ascletis Pharma’s commercialization success may thus be on the horizon.

Chipscreen Biosciences is the company among those we monitor that has recorded the lowest revenue growth but also the smallest net loss. Since its establishment in 2001, Chipscreen Biosciences has been committed to the development of original innovative drugs. Currently, the company holds two national Class-1 original innovative drugs: chidamide for oncology and chiglitazar sodium for diabetes. To achieve more effective commercialization, it has established dedicated Oncology Product and Metabolic Disease Product divisions responsible for the academic promotion and sales of these two products, achieving a revenue target of over RMB 400 million in 2021.

Medical Insurance: The Inevitable Path

For Chinese pharmaceutical companies, health insurance is an inescapable topic.Based on annual report data from various companies, inclusion in the National Reimbursement Drug List (NRDL) has become a powerful driver for doubling sales of innovative drugs.Therefore, within China’s unique context, inclusion in the national medical insurance reimbursement list has become an indispensable pathway for biopharmaceutical companies.Following the inclusion of their products and new indications in the National Reimbursement Drug List (NRDL), BeiGene, Innovent Biologics, and Henlius reported substantial revenue growth, creating a significant gap with Ascletis Pharma, which has only recently had products included in the NRDL, as well as with北海康成 (Beihai Kangcheng) and Chipscreen Biosciences, neither of which has yet had any products listed.

Notably, Brukinsa (zanubrutinib), the BTK inhibitor independently developed by BeiGene, demonstrated remarkable growth in 2021. Data show that global cumulative sales of Brukinsa reached approximately RMB 1.4 billion in 2021, representing a year-on-year increase of 423%. In the United States, revenue from Brukinsa amounted to roughly RMB 700 million in 2021, driven by the approval of multiple indications and expanding market demand.

In China, Brukinsa’s sales revenue increased by approximately RMB 600 million, representing a year-on-year growth of 331%. Domestically, following the inclusion of two indications in the National Reimbursement Drug List (NRDL) in 2020, an additional indication for Brukinsa was added to the NRDL at the end of 2021. After a second round of price reductions under the NRDL, it has become the BTK inhibitor with the lowest monthly treatment cost in China. Leveraging its best-in-class efficacy potential and high cost-effectiveness, Brukinsa is expected to further drive sales volume growth in the future.

Meanwhile, the PD-1 monoclonal antibody product Baizean has secured five indications included in China’s National Reimbursement Drug List, driving its sales in the Chinese market to RMB 1.59 billion, a year-on-year increase of 56%.

Zejula, the first commercialized product of Zai Lab, became a driver for its revenue growth in 2021 after being included in the National Reimbursement Drug List (NRDL) at the end of 2020. According to data disclosed in the annual report, Zejula achieved sales revenue of $93.58 million in 2021, representing a year-on-year increase of 190.68%. Furthermore, Zai Lab successfully expanded the NRDL-covered indications for Zejula to include first-line maintenance treatment for ovarian cancer during the 2021 NRDL negotiations, which is expected to accelerate hospital listings and sales volume growth in 2022.

Excluding BeiGene and Zai Lab, Henlius achieved rapid revenue growth by leveraging the advantages of its biosimilars, Hanquyou (trastuzumab) and Handayuan (adalimumab), being included in the National Reimbursement Drug List (NRDL). Notably, the blockbuster product Hanquyou saw steady sales growth in China and Europe, generating approximately RMB 870 million in domestic sales revenue, a year-on-year increase of about 692.7% compared to 2020. Meanwhile, Innovent Biologics’ core PD-1 inhibitor, Tyvyt (sintilimab), successfully renewed its NRDL coverage at the end of 2021 after initially being included in 2019, while also gaining approval for three additional indications. These factors drove Tyvyt’s product revenue to nearly RMB 3.1 billion in 2021.

Based on the annual report data of the aforementioned leading biotech companies, inclusion of products in the National Reimbursement Drug List (NRDL) will serve as a strong guarantee for sustainable corporate development; however, this also requires alignment with commercial strategies. Ascletis Pharma’s products were included in the NRDL at the end of 2021, with their revenue impact yet to be reflected. Furthermore, since Chipscreen Biosciences and Bohui Kangcheng currently have no products listed in the NRDL, the influence of national reimbursement policies on the current development of biotech enterprises warrants further exploration.

R&D Investment, Commercial Value, and Globalization

Revenue is a hard metric for becoming a biopharma company. Meanwhile, other data points also serve as important criteria for assessing whether a company has the potential to become a biopharma enterprise.

First is the continuous investment by enterprises in research and development.

Beigene, the most profitable company, is also the biggest cash burner; its R&D investment of nearly RMB 10 billion even surpasses that of Hengrui Medicine. The R&D expenditures of Innovent Biologics, Junshi Biosciences, Zai Lab, and Henlius range from over RMB 1 billion to RMB 3 billion.

R&D investment reflects a company’s sustained commitment to innovation. Although China’s pharmaceutical industry is showing signs of entering a downturn, with financing windows for biotech firms gradually closing, companies must not compromise on their R&D spending. Currently, these enterprises maintain robust cash reserves to mitigate potential future risks. Moreover, as an increasing number of products advance into the commercialization phase, this momentum may well propel these biotech firms to transition into biopharma companies.

Second, whether the substantial R&D investment has yielded corresponding commercial and clinical value.

In the current landscape, where multiple biopharmaceutical products are exhibiting signs of intense market saturation and homogenization, whether a company possesses a robust, high-value, and differentiated pipeline of reserve products will lay a solid foundation for its future breakthrough and success in the industry.

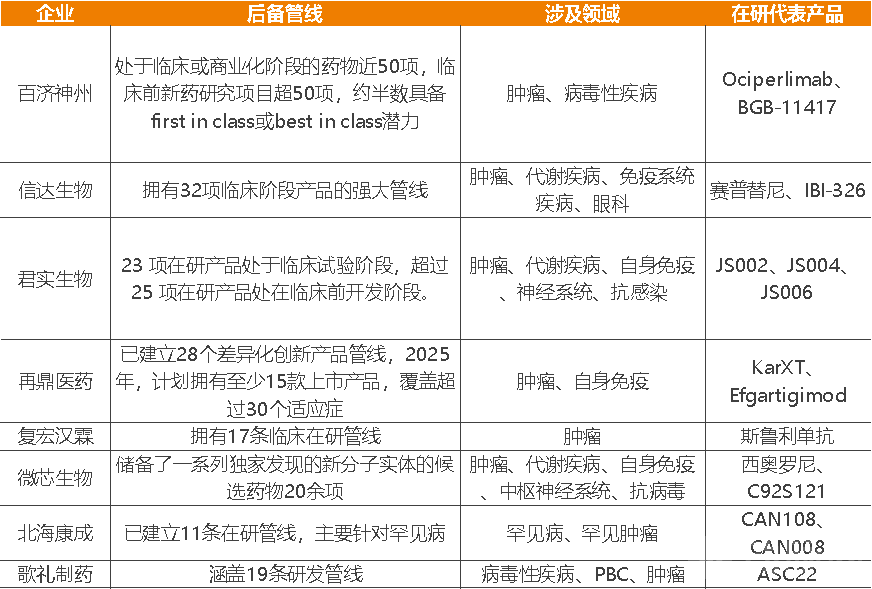

An analysis of the R&D strategies of these eight companies reveals that each has essentially established a comprehensive or differentiated drug development portfolio. BeiGene leads with the largest pipeline by absolute number, primarily targeting best-in-class or first-in-class novel therapeutics. In contrast, the pipelines of Innovent, Junshi, Zai Lab, Chipscreen Biosciences, and Ascletis broadly cover currently high-profile disease areas. Amidst the COVID-19 pandemic, Junshi Biosciences and Ascletis have even expanded their product pipelines into the anti-SARS-CoV-2 space, achieving notable progress. Henlius and Bohai Biotech maintain highly focused R&D efforts, aiming to develop core competencies and unique advantages in oncology and rare diseases, respectively.

Following regulatory adjustments under national policies, the clinical value of remaining products can be largely confirmed. However, their commercial value will only be ultimately tested upon market launch.

Third, there is the global vision of the enterprise. Biotech companies can focus solely on the domestic market, but biopharmaceutical companies must target the global market.

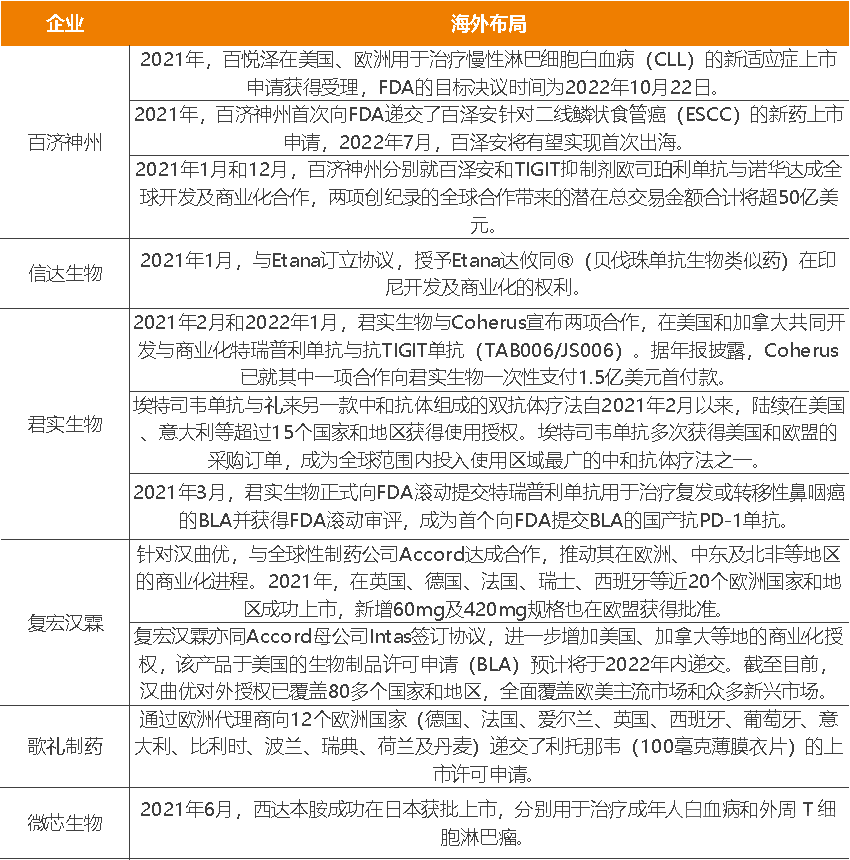

In early 2022, the U.S. marketing application for sintilimab, Innovent Biologics’ PD-1 inhibitor, was rejected by the FDA, making “global expansion” a topic of intense discussion within China’s pharmaceutical industry. Today, domestically commercialized biopharmaceutical companies with relatively mature operations are no longer satisfied with domestic approvals alone; instead, they are prioritizing overseas regulatory approvals and commercial collaborations with international pharmaceutical firms. As some industry insiders have noted, the internationalization of flagship products is also evidencing the transition of Chinese biotech firms into biopharma companies.

Among the eight companies, except for Zai Lab and CanSino Biologics, which primarily rely on the license-in model, the others have already initiated overseas commercialization. Taking BeiGene as an example, its BTK inhibitor, the first innovative drug from China to go global, has been approved in 45 countries and regions worldwide, demonstrating a significant lead in global expansion. Meanwhile, its PD-1 product, Baizean (tislelizumab), is also seeking approval for marketing in the United States and pursuing global commercial development. In addition to BeiGene, Junshi Biosciences has continuously made breakthroughs in “going global,” delivering impressive results in overseas commercialization in 2021. Furthermore, Henlius, Ascletis Pharma, and Chipscreen Biosciences “set sail” for international markets in 2021, beginning to establish overseas partnerships and pursue international commercialization.

Although Innovent Biologics has encountered minor setbacks with Tyvyt, the international expansion of several other projects continues to advance steadily. In addition to its commercialization launch in Indonesia in 2021, these efforts include a BCMA CAR-T candidate co-developed with IASO Biotherapeutics, which has recently been granted Orphan Drug Designation by the U.S. FDA.

From this perspective, Chinese biopharmaceutical companies, having achieved mature product commercialization, have naturally transitioned to considering international market expansion. However, the setbacks encountered by Innovent in its overseas endeavors will prompt Chinese biotech firms to re-evaluate their products and subject them further to the scrutiny of the international clinical market.

They may not yet be biopharma companies, but they are already beginning to take on the appearance of one.