Can a RMB 20-per-Use Medical Imaging AI Fee Support a Hundred-Billion-Yuan Market?

Airdoc

Retinal Imaging Artificial Intelligence Field Product Developer

In mid-March, less than six months after its listing on the Hong Kong Stock Exchange, Airdoc, the first AI-driven medical technology company to go public, released its 2021 financial results.

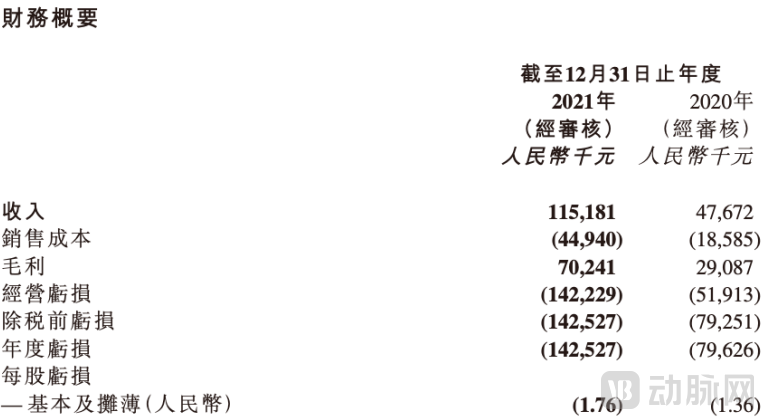

Airdoc 2021 Financial Summary (Source: Airdoc 2021 Annual Report)

The annual report highlights four key points: First, revenue reached RMB 115 million, a year-on-year increase of 141.6%, marking Airdoc’s entry into the club of companies with annual revenues exceeding RMB 100 million. Second, the net loss amounted to RMB 143 million in 2021, a year-on-year increase of 79.8%, primarily driven by sharp rises in R&D, sales, and administrative expenses. Third, the number of clients grew from 85 to 244; excluding approximately RMB 46 million in revenue contributed by Client A (a health checkup center) and Client B (an optometry center), the average revenue per client was RMB 285,000. Fourth, regarding AI service fees, Airdoc estimates that its AI system was utilized 4.86 million times in 2021, with an average fee of RMB 19.9 per AI screening (calculated by dividing the revenue from AI-based software solutions by the number of screenings).

Airdoc’s RMB 115 million in revenue was primarily driven by health examination centers, optometry centers, and insurance institutions. With price approvals secured only in select provinces and municipalities, Airdoc has a limited hospital client base of just 41 facilities. In contrast, its health examination and optometry centers demonstrated strong revenue performance, with individual clients contributing over RMB 10 million each.

Given the linear correlation between the revenues of physical examination centers and optometry centers and the number of software API calls, it can be inferred that Airdoc’s AI invocation volume for a single major client ranges from 300,000 to 1 million times. Fundus examination is a routine screening procedure. Using Meinian Onehealth’s approximately 18 million annual physical examinations in 2021 as a benchmark, Airdoc’s AI invocation volume accounts for only 2%–5%, indicating substantial room for growth.

Last year marked the first year of sales for Airdoc-AIFUNDUS (1.0), an integrated hardware-software device for fundus screening. Airdoc achieved RMB 18.7 million in sales across 41 hospitals and 36 community clinics. This new type of imaging equipment, which combines software and hardware, may hold significant promise for the future.

Regarding losses, Airdoc’s various expenses continued to rise, with increases in R&D, sales, and administrative expenses all exceeding 50%. However, while every yuan invested in 2020 generated only RMB 0.60 in revenue, this figure rose to RMB 0.80 in 2021. Currently, Airdoc holds RMB 1.8 billion in cash and cash equivalents on its balance sheet. If the current development trend remains unchanged, the company is highly likely to turn a profit within a few years.

In 2021, Airdoc experienced significant changes in its customer base. Optometry chain platforms such as Jinggong Glasses, Jingyi Glasses, and Glasses 88 joined its partnership network, while the number of hospital clients also saw a certain increase, resulting in the total number of customers nearly tripling. However, the low revenue contribution per customer remains a serious challenge for Airdoc. As collaborations deepen, if Airdoc can deliver tangible value to the actual operations of enterprises and medical institutions, or gain further recognition from end consumers, its revenue is expected to rise further.

Finally, let’s focus on Airdoc’s AI invocation fees. We often say that pay-per-use is the ideal future business model for artificial intelligence. But can a medical imaging AI service priced at RMB 20 per use support a market worth hundreds of billions?

As of early March, with the release of the landmark AI review and approval policy, the “Guiding Principles for the Registration and Review of Artificial Intelligence Medical Devices,” a total of 33 Class III medical artificial intelligence products had gained approval from China’s National Medical Products Administration (NMPA). By this time, several leading companies had already secured two to three Class III certificates and multiple Class II certificates, indicating that the review and approval process was no longer a critical bottleneck hindering the progress of medical enterprises.

An analysis of operational data for medical AI companies post-2020 reveals that every enterprise that filed a prospectus achieved multi-fold revenue growth, reaching the tens of millions, after obtaining regulatory approval and certification. This phenomenon can be attributed to two main factors: first, the pre-approval sales base was exceedingly low; second, the strategic deployments made by medical AI firms over the past few years have gradually begun to yield results.

2022 marked a watershed moment for medical AI companies. The inclusion of AI products in provincial hospital price catalogs enabled more healthcare institutions to purchase these solutions through bidding and other procurement channels, thereby driving up corporate sales volumes. However, since sales in 2021 had already converted a significant proportion of the existing customer base, acquiring an equivalent number of new users in 2022 would necessitate higher sales costs, excluding the impact of the pandemic.

The opposing trends in revenue and costs make it difficult to determine the revenue growth trajectory of medical AI; however, based on an AI invocation fee of RMB 20 per use, we can roughly estimate the market’s ceiling.

According to the data released by the Statistical Information Center of the National Health Commission in “Number of Medical and Health Institutions Nationwide as of the End of October 2021,” there were 3,147 tertiary hospitals and 10,664 secondary hospitals across China as of the end of October 2021. Furthermore, based on CT scan volumes compiled by VCBeat from publicly available sources, tertiary hospitals perform 200–500 CT scans per day, while secondary hospitals perform 50–200 CT scans per day.

Based on the above data, assuming 300 and 100 scans respectively, with each CT scan requiring an AI invocation, healthcare institutions would need to pay CNY 14.673 billion annually in invocation fees to CT-related AI companies. This implies that if a per-case payment model is implemented, medical AI companies could still achieve substantial revenue even if the actual volume is only 20% of the ideal scenario.

The ideal sales model remains a distant reality. Airdoc has pioneered the integration of two high-volume scenarios—health examination centers and optometry centers—into its ecosystem, thereby achieving 4.86 million API calls. However, for AI companies focusing on applications such as pulmonary nodule detection and CT angiography (CTA), shifting from entering strictly regulated hospitals through bidding processes and selling via perpetual software licenses to an on-demand calling model with true per-case pricing requires overcoming two major hurdles: price approval and medical insurance reimbursement eligibility.

To date, leading medical AI products remain in the stage of securing pricing approval. Even after pricing is established, it typically takes another 1–2 years of operation before they are likely to be included in the national medical insurance coverage.

Currently, no company has achieved a breakthrough in gaining inclusion in the national medical insurance reimbursement list. Medical AI enterprises still face a long journey ahead.

To raise the various funds needed to advance to the next stage and to help private equity (PE) firms, which had been waiting for years, find exit pathways, multiple medical AI companies filed prospectuses with the Hong Kong Stock Exchange in 2021 in pursuit of initial public offerings.

A year has passed, and apart from Airdoc’s successful listing, Keya Medical, Shukun Technology, and Infervision have all seen their registration documents expire. Recently, Shukun Technology publicly announced that it has obtained preliminary approval from the regulators and will resubmit its prospectus in the near future.

VCBeat recently reached out to various AI companies for updates. Regardless of whether they were firms that had unsuccessfully filed for an IPO or those targeting the consumer market and preparing for a public listing, all stated that they were in a quiet period and thus unable to provide detailed responses.

Synthesizing the fragmented statements from various companies, the IPO challenges faced by medical AI enterprises do not lie in their business operations, but rather at the macro level.

Under the combined impact of surging stamp duty on Hong Kong stocks, the erratic pandemic situation, and the rising tide of de-globalization amid geopolitical crises, valuations for companies in both primary and secondary markets have plummeted. Public pessimism has taken hold, driving overall market investment sentiment to a freezing point. With crises looming on all fronts, neither enterprises nor investors are willing to advance to the next stage at this juncture.

For AI companies planning to go public, a delayed entry into the secondary market will not significantly impact their operations. On the eve of their IPOs, each company secured over RMB 1 billion in funding, leaving them with ample resources to expand their market share.

A Year in Crisis: Medical AI Companies Take Divergent Paths

For medical AI companies that take smaller steps and lack significant capital backing, they choose to promote their AI products in local hospitals and those in neighboring provinces and cities. Such companies either have close cooperative relationships with hospitals in the region or partner with listed companies like Winning Health to provide new service support for hospitals, achieving small-scale profitability through medical AI, with a strategy consistent with traditional informatization.

AI companies that have attracted substantial capital but have not yet reached the IPO stage, such as Deepwise and Zhiyuan Huitu, continue to focus on deepening their product offerings. Deepwise adopts a comprehensive medical imaging strategy, with an emphasis on the detection of breast and lung diseases, while Zhiyuan Huitu employs a strategy similar to that of Airdoc, deeply focusing on the detection of fundus diseases.

In contrast, Huiyi Huiying and Deepwise Medical have begun to explore the construction of industrial ecosystems, creating a synergistic closed loop between medical IT infrastructure and technical/clinical departments, with an emphasis on the closed-loop flow of data and applications. Under this strategic layout, these companies are betting on the future digitalization of clinical application workflows. Huiyi Huiying’s product portfolio includes a big data cloud platform, a data middle platform, and AI-assisted diagnostic tools for the aorta, bones, breast, and other areas; its entire closed-loop system is already operational. Deepwise, meanwhile, holds a strong position in assisted diagnosis, having secured multiple Class III medical device registrations and published numerous medical AI-related papers in authoritative journals. Following its acquisition of Yitu Healthcare in July last year, Deepwise Medical has achieved a highly mature presence in the medical IT sector.

In response to Airdoc’s innovations, Shukun Technology, Keya Medical, and Bodong Medical are all striving to expand their respective business scopes. On one hand, they are pursuing horizontal expansion from “AI imaging” to “AI informatics” and “AI health management.” On the other hand, they are engaging in vertical expansion by shifting from standalone software solutions to integrated hardware-software offerings; for instance, Keya Medical has participated in the research and development of products such as balloons, while Shukun Technology has entered the chronic disease management sector. Regardless of the approach, these companies are making every effort to explore new application scenarios for AI implementation, capture greater market share, and maximize their valuations.

During the production line expansion, the “three highs” cost issue faced by Airdoc in its annual report also appeared in the prospectuses of the aforementioned three companies, particularly with selling expenses expected to increase year by year.

According to a medical AI company, all medical AI products sold through bidding processes come with a three-year service-fee waiver policy, under which no charges will be levied on hospitals for updates or maintenance during this period. In other words, once a hospital purchases products from this medical AI company, it is unlikely to have the opportunity to procure competing products within the subsequent three years.

Before 2020, when discussing medical AI, entrepreneurs could attribute the various commercialization challenges facing the industry to restrictions in the registration and market access phase. However, as this hurdle has been overcome, the once-pervasive skepticism has begun to dissipate, replaced by a range of concrete, tangible issues.

This is a positive development for medical AI companies. Deeper collaboration between physicians and developers has mitigated information asymmetry, enabling these enterprises to meticulously design their products in line with clinicians’ practical and research needs, much like traditional medical device manufacturers. Consequently, capital allocation will become more efficient throughout this process.

The era of rapid, breakthrough advancements in early-stage medical AI across various fields has passed, giving way to slow, detail-oriented innovation.

In any case, both doctors and patients indeed benefit from this intelligent transformation. Doctors have more time for rest or scientific research, while patients gain access to more timely and efficient treatment opportunities due to the acceleration of medical efficiency.

Returning to the initial question. For disruptive innovations like medical AI, substantial R&D investment is required to drive technological iteration and clinical trials, while significant sales and marketing expenditures are necessary to build consensus among physicians and patients. Without substantial capital infusion, how can we overcome the limitations of both the product itself and the prevailing perceptions?

From this perspective, under the current domestic healthcare system, the price of RMB 20 per medical imaging AI analysis may be too low compared to the high returns generated by pharmaceutical and medical device innovations. It makes it very difficult for doctors and patients, who benefit from the convenience, to bear the cost; yet without financial support, how can innovation thrive?