UnitedHealth to Acquire LHC Group for $5.4 Billion: Why Health Insurers Are Betting Big on Home Healthcare

UnitedHealth Group

Health Insurance and Health Information Technology Service Provider

Another Major M&A Deal Emerges in the Health Insurance Industry.

Recently, U.S. health insurance giant UnitedHealth Group decided to acquire the publicly listed home healthcare company LHC Group in its entirety for a hefty $5.4 billion, equivalent to over RMB 34 billion.From the perspective of the industry standing of both parties involved, this is a transaction significant enough to leave a lasting mark on the health insurance industry.

The reason is that, as a party to the transaction, UnitedHealth Group is the world’s largest health insurance company, with a current market capitalization exceeding RMB 3 trillion. Its revenue has continued to rise in recent years, reaching an astonishing USD 287.6 billion in 2021, equivalent to over RMB 1.8 trillion.. This is even higher than the combined total revenue of Alibaba, Tencent, and Baidu in 2021.

The other party to the transaction, LHC Group, is a leading provider of home healthcare services in the United States and has been listed on NASDAQ for 18 years.Current annual revenue exceeds RMB 13 billion, with continued expansion underway.

Following this merger and integration, UnitedHealth Group will be propelled to expand into new business formats such as home health services, thereby achieving greater scale and volume, and potentially driving sustained growth in its total revenue.

According to announcements posted on the websites of both companies, UnitedHealth Group will acquire all outstanding shares of LHC Group in an all-cash transaction, and LHC Group will be delisted following the completion of the merger.The transaction is expected to be completed in the second half of this year.

How will UnitedHealth Group achieve synergies with LHC Group’s operations through this acquisition? What are the potential pathways for future development? And what implications does this hold for China’s health insurance industry? VCBeat will provide a detailed analysis of these questions in the following sections.

Elderly care is a major industry.

Since the 1960s, the United States has gradually transitioned into an aging society, giving rise to a variety of healthcare models centered on elderly care. These include large-scale senior living communities, premium senior living communities, nursing homes, community- and home-based PACE (Program of All-Inclusive Care for the Elderly) models, and Home Health care models.

As a key component of the U.S. elderly care industry, home health care primarily refers to post-discharge rehabilitation and home-based rehabilitation, in which a service team composed of physicians, nurses, rehabilitation therapists, and home health aides provides rehabilitative care to patients at home.

Given the relatively weak medical attributes of in-home healthcare services and the geographic dispersion of patients’ residences, the commercial pathway for this model remains unclear. As a result, it has long constituted an independent and relatively fragmented market.

In 1994, Keith and Ginger Myers decided to launch a venture in the home healthcare sector, founding LHC Group Inc. Initially, LHC operated as a single home health agency, primarily providing basic home care services to rural populations in the southern United States (administrative regions with resident populations ranging from 10,000 to 100,000).

In the view of Keith and Ginger Myers,The advantage of targeting the rural market lies in its higher proportion of medical insurance beneficiaries, yet healthcare service supply remains insufficient compared to urban or suburban markets.

Data provide a glimpse into the state of the industry. According to 2004 statistics from the U.S. Centers for Medicare & Medicaid Services (CMS), total Medicare spending on home health care services that year amounted to $10.2 billion, with approximately 34% allocated to rural markets.

On the other hand, the population size in most rural areas of the United States can only support one or two general acute care hospitals, which has resulted in the persistent unmet demand for home care services among rural patients.

It is precisely based on its forecast of the rural in-home healthcare market that LHC Group has achieved relatively smooth development.In terms of its business trajectory, LHC Group has implemented a clinically oriented business model, primarily through four major initiatives.

· First, establish partnerships with hospitals, physicians, and other healthcare providers serving rural communities across various regions;

· Second, to help local hospitals provide more clinical support services;

· Third, recruit qualified nurses and other healthcare professionals to establish a more comprehensive home healthcare service team;

· Fourth, drive the acquisition of technology platforms and affiliated hospitals to strengthen its service delivery and operational capabilities across various regions.

Ten years after its founding, LHC Group successfully listed on the Nasdaq in 2004. At that time, LHC Group’s service footprint had expanded to 86 regions, with 72.7% located in rural areas or communities with populations under 100,000, and over 80% of its revenue derived from insurance reimbursements.

(LHC Group’s Business Coverage in 2004. Source: LHC Group Prospectus)

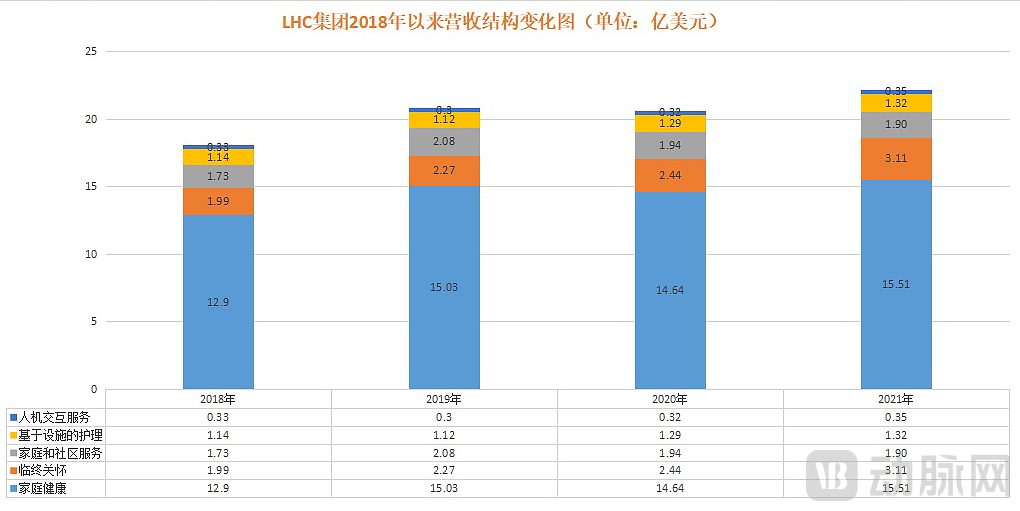

After achieving development in its first phase, LHC Group continuously expanded its business scope over the subsequent 18 yearsIt has expanded into five major services: Home Health Services, Hospice Services, Community-Based Services, Facility-Based Services, and Human-Computer Interaction (HCI) Services.

Specifically, home care services include in-home wound care and dressing changes, cardiac rehabilitation, infusion therapy, pain management, medication management, observation and assessment, and patient education. Hospice care services primarily provide pain and symptom management, emotional and spiritual support, inpatient and respite care, dietary counseling, and bereavement counseling and companionship for elderly patients.

Community-based services and facility-based services constitute a suite of extended offerings provided by LHC Group to its users. These include community-based services such as medication reminders, meal preparation, respite care, transportation and errand assistance, and personal care services, as well as facility-based services delivered through the operation of long-term acute care hospitals (LTACHs), which provide treatment for patients with severe medical conditions requiring intensive care and frequent monitoring by physicians and other clinical staff.

The core of human-computer interaction services is to provide wearable devices for monitoring users’ vital signs, which falls under supportive services. In addition, LHC Group operates medical service institutions such as institutional pharmacies, home health agencies, and home health clinics to offer more diversified service support.

According to LHC Group’s financial reports over the past four years, home health services have consistently been the primary revenue driver, generating approximately $1.5 billion in annual revenue, although growth momentum has slowed.On the other hand, revenue growth from community-based services has also begun to weaken.

This is linked to the growing challenges in expanding LHC Group’s home-based care services: To date, LHC Group has covered most rural areas in the southern United States with populations ranging from 10,000 to 100,000, and its geography-driven expansion strategy has hit a bottleneck.

(Data source: LHC Group financial reports; graphic by VCBeat)

(Data source: LHC Group financial reports; graphic by VCBeat)

Notably, hospice care services have become a key growth driver for LHC Group, with revenue increasing by 27.5% in 2021 compared to 2020, and its share of total revenue rising from 11% in 2018 to 14% in 2021.

From a business model perspective, the growth of the hospice care business is primarily driven by the secondary extension of home healthcare services. This is because home healthcare operations must comply with U.S. government Medicare certification standards, which impose a ceiling on revenue potential. In contrast, in addition to government Medicare reimbursement, the hospice care business can cater to high-net-worth individuals who seek additional private services while receiving home-based care provided by LHC Group. Furthermore, the inherently non-medical nature of hospice care results in lower entry barriers.

In addition to expanding its new businesses, LHC Group is also continuously driving mergers and acquisitions and consolidation within the industry.On April 2, 2018, LHC Group and Almost Family completed their merger, making the combined entity the second-largest home healthcare provider in the United States.

In October 2021, LHC Group completed the acquisition of Generations Home Health and Freda H. Gordon Hospice and Palliative Care, thereby expanding its service portfolio. In November of the same year, LHC Group acquired assets from HCA Healthcare and Brookdale Senior Living Inc., securing 23 home health centers, 11 hospice agencies, and 13 therapy facilities.

Since then, after nearly 30 years of development, LHC Group has grown into a leading home healthcare enterprise with annual revenues exceeding RMB 13 billion, integrating services such as home health, hospice care, and personal care., with a workforce of 30,000 employees, serving 60% of the U.S. population aged 65 and older, and is the preferred home healthcare partner for 435 hospitals across the United States.

$5.4 billion. This is the price UnitedHealth Group has offered to acquire LHC Group, which currently has a market capitalization of $5.195 billion, representing a premium of approximately 4%.

As the largest health insurance company in the United States,UnitedHealth Group’s acquisition of LHC Group marks its entry into the home healthcare sector, thereby expanding its business to encompass a diversified service system that includes physician groups, clinics, ambulatory surgery centers, and home health services.

Beyond expanding business coverage, what other synergies can this acquisition bring to UnitedHealth Group?

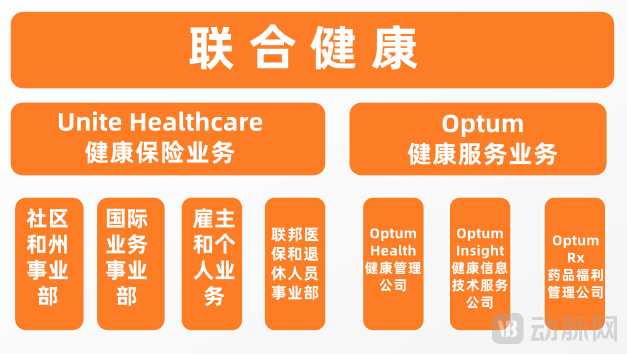

This requires a return to the fundamentals of UnitedHealth Group. First, UnitedHealth Group has adopted a strategy of building a commercial closed loop integrating “health insurance + healthcare services.” In this regard,UnitedHealth Group has built its business around two main segments: one is the insurance business primarily under UnitedHealthcare, and the other is health management and related services primarily under Optum.

(UnitedHealth Group Organizational and Business Architecture Diagram, created by VCBeat)

(UnitedHealth Group Organizational and Business Architecture Diagram, created by VCBeat)

Among them, Optum comprises Optum Health (a health management company), Optum Insight (a health information technology services company), and Optum Rx (a pharmacy benefit management company). The business unit undergoing merger integration in this instance is Optum Health. In other words,LHC Group’s home healthcare business will subsequently become a component of UnitedHealth Group’s health management services.

According to the merger announcement, following the acquisition, LHC Group will integrate its high-quality home and community-based healthcare services with Optum’s value-based care expertise and resources, thereby improving care outcomes and patient experience.

It is worth noting that Optum Health’s business accounts for approximately 8% of UnitedHealth Group’s total revenue, with revenues reaching $24.831 billion in 2021, while LHC Group reported total revenues of $2.22 billion last year.

Therefore, from a revenue perspective,LHC Group is expected to drive an approximately 10% increase in UnitedHealth Group’s health management services revenue; however, its contribution to the overall growth of the entire group will be quite limited (the group’s total revenue in 2021 was $287.6 billion, with LHC’s revenue accounting for roughly 1%).

However, it is important to recognize that UnitedHealth Group’s historical development demonstrates that continuous mergers, acquisitions, and integration have significantly propelled the momentum of its business flywheel.

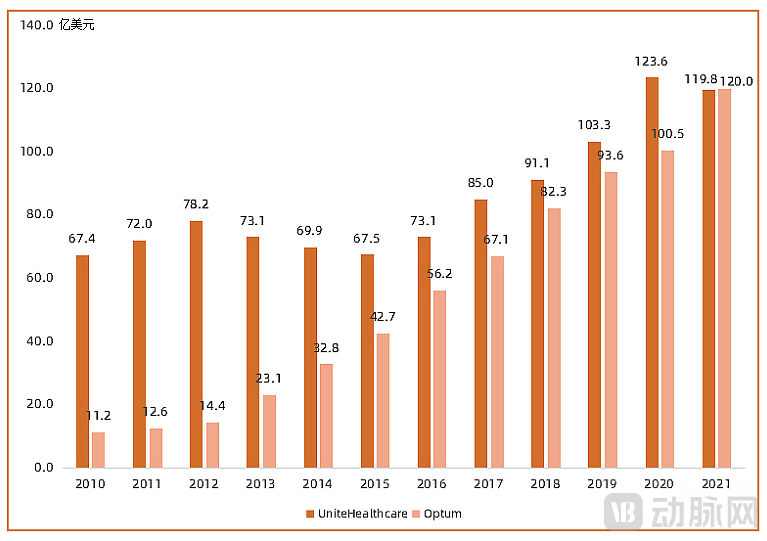

Since 2004, UnitedHealth Group has divided its overall business into two major segments: UnitedHealthcare and Optum. Initially, the development of its insurance business and health management services was unbalanced, with Optum contributing poorly to the group’s overall revenue. This was because, despite UnitedHealth’s substantial commercial insurance payment volume, it lacked sufficient resources on the service delivery side, failing to establish an efficient supply system.

Ultimately, the core of the “health insurance + healthcare services” model lies in economies of scale: by delivering superior services to reach a broader population, the enlarged user base helps drive down healthcare expenditure costs; the resulting savings are then reinvested into the service side, enabling more and better services, thereby creating a positive flywheel effect.

Thus, it can be seen that since 2010, UnitedHealth Group has continuously promoted mergers and acquisitions and integration on the service side, spending hundreds of billions of dollars to acquire PBM provider Catamaran Corp., the physician group under DaVita Inc., surgical care operator Surgical Care Affiliates, rapid diagnostics company Alere Health, and healthcare payment company Equian LLC, among others.

Continuous integration has also enabled UnitedHealth Group’s business to continue expanding.According to the latest 2022 fiscal year annual report, UnitedHealth Group’s revenue exceeded RMB 1.8 trillion. Notably, profits from its health management services business, primarily driven by Optum, surpassed those of its insurance business for the first time.

(Trend of Profit Growth in UnitedHealth Group’s Two Major Business Segments; Chart by VCBeat)

(Trend of Profit Growth in UnitedHealth Group’s Two Major Business Segments; Chart by VCBeat)

Following the acquisition of LHC Group, UnitedHealth is poised to further expand its supply capacity in health services.

Health insurance giants are constantly expanding their turf.

In addition to UnitedHealth Group’s acquisition of LHC Group, Humana, another U.S. health insurance giant, also completed its 100% controlling acquisition of KAH (Kindred at Home), the leading U.S. home healthcare provider, for $8.1 billion last year. The deal took a total of four years to complete, having begun in 2017. This marks Humana’s largest acquisition in its history.

Prior to the acquisition, Kindred at Home was the largest home-based healthcare provider in the United States, with three core business lines: Home Health, Hospice, and Community Care Services. In 2017, it generated $1.822 billion in revenue, 63.6% of which came from the U.S. government’s Medicare program.

According to Broussard, founder of Humana, the integration of Kindred at Home can effectively enhance Humana’s business synergy efficiency. He stated that, compared with individual Medicare Advantage enrollees who do not use home health services,Users' quality of life is significantly improved, and the likelihood of hospitalization is markedly reduced with home-based healthcare support.

More importantly, the addition of home-based healthcare services has enabled Humana to offer one-stop solutions ranging from primary care and pharmacy services to home care, thereby better providing insurance members with diversified services and products.

From the current point in time,The acquisitions of Kindred at Home and LHC Group signal the onset of a wave of mergers and acquisitions in the health insurance industry, centered on home-based healthcare.This reflects both the inevitable strategic choice for U.S. health insurance giants as their businesses mature, and the heightened prominence of home-based healthcare services during the COVID-19 pandemic, as public acceptance and demand for such services continue to rise.

In addition to Kindred at Home and LHC Group, other leading home healthcare providers in the United States include ComForCare and Amis Health; however, high-quality investment targets remain scarce overall.

Of course, the “big fish eat small fish” dynamic in capital markets, while driving the growth of an increasing number of enterprises, also entails significant risks and has therefore drawn scrutiny from public opinion and relevant regulatory authorities. For example, UnitedHealth Group’s prior acquisition of the healthcare IT company Change Healthcare is currently facing an antitrust lawsuit brought by the U.S. Department of Justice. The core allegation is that UnitedHealth may gain control over vast amounts of healthcare data and leverage its digital assets to secure an unfair competitive advantage for its insurance division against rivals.

If the merger integration proves successful, UnitedHealth Group could continue to elevate market expectations for the health insurance industry, given that its market capitalization, which has already surpassed RMB 3 trillion, has made it a unique benchmark.This means that, amid the snowballing scale-up expansion, healthcare services can also sustain substantial revenue and market capitalization, while delivering robust profits.

With U.S. health insurers setting a precedent, will China’s health insurance industry follow the American path and trigger a wave of mergers and acquisitions in the short to medium term? The likelihood is extremely low.

First, from the perspective of industry development, China’s health insurance sector has yet to produce a top-tier market leader, and the local “insurance + healthcare services” model remains to be further validated. Second, companies such as LHC Group have highly dispersed ownership structures, which enables giants like UnitedHealth Group to more conveniently buy and sell shares of these target companies in the secondary market.

Therefore, the domestic health insurance industry in China still requires ample patience for gradual growth and development. What is certain, however, is that the path of continuously enhancing the diversity and accessibility of medical services has been proven viable. For Chinese companies, though, greater localization-driven experimentation and innovation are needed in implementation strategies.

As UnitedHealth Group has adhered to since its inception: “We are working to help people live healthier lives and help make the health system work better for everyone.”

As can be seen,All forms of capital are merely means, while delivering true patient value is the ultimate goal of healthcare enterprises.Only by achieving this can healthcare enterprises unlock greater market potential.

References:

1: "LHC Group Prospectus S-1"

https://www.sec.gov/Archives/edgar/data/0001303313/000095014405001444/g92064a2sv1za.htm

2: “Examining the U.S. Home-Based Health and Elderly Care Industry Through Listed Companies” by Xiang Wendong

https://mp.weixin.qq.com/s/eI67pBhU6x1Q8OiafOom7g

3: LHC Group Official Website

4:《UnitedHealth to buy LHC Group for $5.4 billion》 CNBC

https://www.cnbc.com/2022/03/29/unitedhealth-to-buy-lhc-group-for-5point4-billion.html