How GPS Navigates the Looming Closure of MR and CT Equipment Import Channels in China

Philips Healthcare

Integrated service provider in healthcare, quality living, and lighting fields

In March 2022, Philips’ exclusive strategic investment in Sinounion, a Chinese manufacturer of PET/CT systems, sent shockwaves through the industry. In its official press release, Philips characterized this strategic investment and partnership as a pivotal step in its “localization” strategy.

Proactive measures should be well-founded. In October 2021, an internal document titled “Guidance Standards for Reviewing Government Procurement of Imported Products” (2021 Edition) circulated online, presenting detailed data tables covering multiple categories, including patient monitors, imaging equipment, in vitro diagnostics, and high-value consumables.

Document Recommendation: 100% of the 137 types of medical devices listed in the table are required to be domestically produced; 75% of the 12 types of medical devices are required to be domestically produced; 50% of the 24 types of medical devices are required to be domestically produced; and 25% of the 5 types of medical devices are required to be domestically produced.Among them, common large-scale medical equipment such as MRI (1.5T, 3T), PET/CT, PET/MR, and DR are prominently listed, all of which require “exclusive procurement of domestically produced products.”

(Screenshot of the document circulating online (partial))

(Screenshot of the document circulating online (partial))

Although the authenticity of this document has not been officially verified, a wave of domestic substitution for medical devices is intensifying across the industry, driven by factors such as the rise of high-tech enterprises in China and the worsening geopolitical landscape.

In addition, documents such as the Catalogue of Major Technical Equipment and Products Supported by the State (2021 Edition), the Implementation Rules for the Administration of Import Tax Policies for Major Technical Equipment, and the Catalogue of Major Technical Equipment and Products Supported by the State have been successively released, encouraging the development of domestically produced high-end medical devices through subsidies, tariffs, and other measures.

However, the current boom among domestic medical device startups is a crisis that GE Healthcare, Philips, and Siemens Healthineers (GPS) must spare no effort to address.

For GPS, the Chinese market is an exceptional entity.

According to the 2021 annual report, GE Healthcare’s China region contributed a total of $2.7 billion in revenue, representing a year-on-year increase of 16.4% and accounting for 15.3% of the company’s total healthcare revenue—the highest proportion among the “GPS” competitors—making it one of GE Healthcare’s most stable regions.

Siemens Healthineers’ situation is similar to that of GE. In 2021, its revenue in China reached €2.354 billion, a year-on-year increase of 24%, with particularly notable growth in the imaging and diagnostics business. China became the fastest-growing region globally for Siemens Healthineers outside its home market of Germany.

Although Philips’ revenue growth in China remained relatively stable last year, its approximately 13.6% share of total revenue, coupled with the establishment of key R&D hubs such as the Philips (China) Research Institute and the China Digital Innovation Center, underscores the increasingly important role of the Chinese market within Philips Healthcare’s global landscape.

Against the backdrop of GPS’s recent growth stagnation, with revenue and profit growth slowing or even turning negative, its medical business in China has become a cornerstone, playing an increasingly vital role in stabilizing the company’s overall revenue. However, this very segment has frequently faced challenges from both the regulatory environment and competitors in recent years.

Unit: 100 million yuan (euros) | GE | Philips | Siemens Healthineers |

Total Revenue | 675.18 | 171.56 | 180 |

Year-on-Year Change | -2.16% | -1% | 24% |

Healthcare Business Revenue | 161.07 | 132.26 | 180 |

Year-over-Year Change | -1.58% | -4% | 24% |

Healthcare Business Profit | 27.03 | / | 15.6 |

Year-over-Year Change | -3.07% | / | 9.6% |

Proportion of China's Medical Business Revenue to Total Medical Business Revenue | 15.3% | 13.6% (Group) | 13.1% |

Revenue Growth Rate in China Region | 16.4% | 0 (Group) | 24.4% |

Comparison of GPS Data for Fiscal Year 2021

(Note: Due to differences in listing exchanges, there are variations in the decimal places of the data; the USD/EUR exchange rate is calculated at 1:0.91)

The Rise of Domestic Medical Device ManufacturersThis represents the greatest threat to GPS. Led by United Imaging Healthcare, Neusoft Medical, and Wandong Medical, Chinese medical imaging equipment manufacturers are seeing their technologies mature and their product lines gradually expand. They are able to surpass GPS in cost-effectiveness for specific products, thereby capturing the mid-to-low-end market.

Distribution of Product Lines Among Domestic and International Medical Imaging Equipment Companies (Data Source: United Imaging Healthcare Prospectus, VCBeat)

Distribution of Product Lines Among Domestic and International Medical Imaging Equipment Companies (Data Source: United Imaging Healthcare Prospectus, VCBeat)

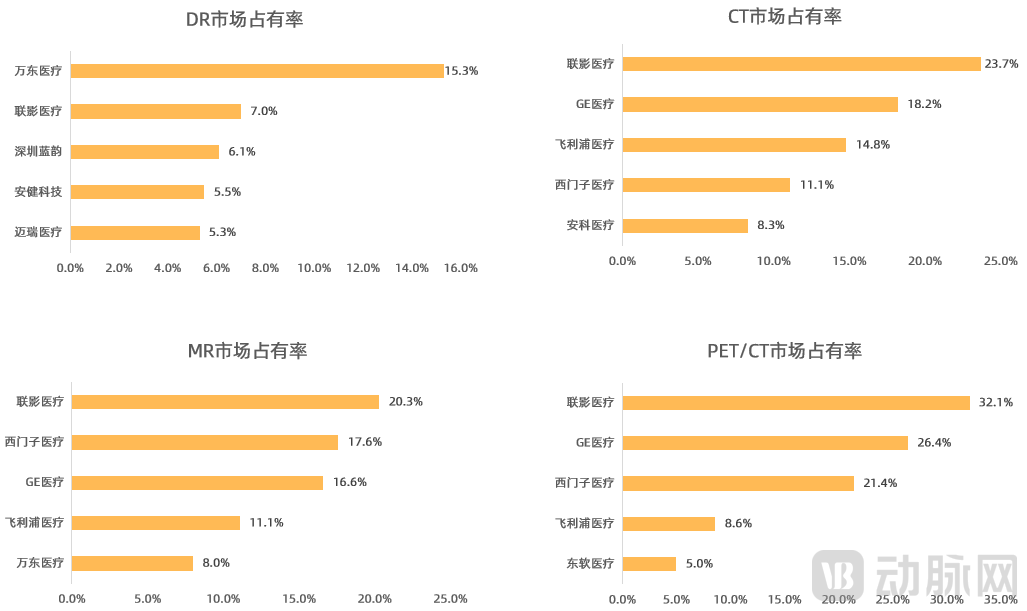

In its prospectus filed at the end of 2021, United Imaging Healthcare provided a quantitative analysis of the dissolving oligopoly in the medical imaging market. Data show that GPS (GE Healthcare, Philips, and Siemens Healthineers) continues to dominate major imaging segments, with United Imaging Healthcare being the sole disruptor. This unicorn company has surpassed GPS in market share for MR, CT, DR, PET/CT, and PET/MR systems.

Market Share Distribution of Medical Imaging Modalities (Source: United Imaging Healthcare IPO Prospectus)

Market Share Distribution of Medical Imaging Modalities (Source: United Imaging Healthcare IPO Prospectus)

The changes displayed on the data front are somewhat misleading. On the surface, the rise of domestic enterprises is continuously encroaching upon the market share once held by GPS; however, from a practical standpoint,The implementation of tiered diagnosis and treatment and the high-quality development of public hospitals have opened up the mid-to-low-end markets represented by second- and third-tier cities. Tasked with alleviating the burden on tertiary hospitals, these markets prefer purchasing cost-effective domestic medical equipment, thereby diluting the market share held by GPS.

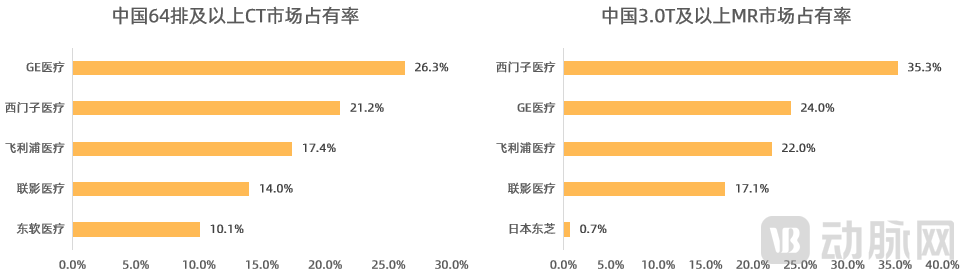

In other words, high-end equipment, which embodies the core technological capabilities of enterprises, remains firmly in the hands of GPS. The existence of cutting-edge technologies and comprehensive solutions, such as photon-counting CT and MRI sequence development platforms, has created a competitive advantage that domestic companies cannot match in the short term. Consequently, most Grade A tertiary hospitals still prefer to procure the latest equipment from GPS for medical research.

Distribution of High-End Market Share Among Medical Device Companies (Source: United Imaging Healthcare Prospectus)

Distribution of High-End Market Share Among Medical Device Companies (Source: United Imaging Healthcare Prospectus)

Is there absolutely no possibility of this market segment collapsing? Not necessarily.

Zheng Hairong, Deputy Director of the Shenzhen Institute of Advanced Technology, Chinese Academy of Sciences, once stated: “For a comprehensive, modernized industrial manufacturing system, high-end medical imaging equipment is more than just a medical product. Its production can drive the development of a range of high-end industrial chains in China, spanning materials, chips, components, and electronics—a challenge that cannot be resolved simply by purchasing from abroad, as might be feasible for a smaller country.” In other words, the competitors faced by the “GPS” companies are not merely domestic latecomer startups.

This brings us to another issue: the deteriorating geopolitical landscape.

Following the Russia-Ukraine conflict, the fractures accumulated during the era of deglobalization have been fully magnified. Actions such as Apple’s closure of the App Store in Russia and the potential nationalization of foreign corporate assets have cast a shadow over buyers and sellers in cross-border transactions, thereby driving a shift from “highly specialized” global industrial chains to “fully domesticated” supply chains.

In the field of medical imaging, calls for domestic substitution have persisted for years. At this juncture, “localization” may be the only viable strategy for GPS to further expand their market share.

The “localization” strategy championed by Philips and Siemens Healthineers, and the “comprehensive domestic production” advocated by GE Healthcare, are essentially aimed at establishing manufacturing bases in China, introducing imaging equipment production lines, achieving full-scale production at Chinese factories, further expanding into the Chinese market, while mitigating unpredictable geopolitical risks.

“Localization”: GPS shares similar philosophies, yet they are not entirely the same.

Philips places particular emphasis on in-house R&D, innovation, and alignment with market needs. In addition to large-scale factory construction in China, Philips has established the “China Digital Innovation Center” to bolster its local R&D capabilities and enhance customized design, thereby better addressing China’s diverse and localized demands.

GE Healthcare focuses on exports from its Chinese factories. Data shows that 60% of GE’s global CT scanners are produced in Beijing, 50% of its MRI systems come from Tianjin, and 40% of its ultrasound devices are manufactured in Wuxi; meanwhile, 90% of the products from its contrast media plant in Shanghai are exported overseas.

Siemens’ strategy in China mirrors that of Philips, under the banner of “customer-centricity.” This approach involves segmenting Chinese customers by distinct characteristics—ranging from tertiary, secondary, and primary hospitals to regional medical centers, private hospitals, and private hospital chains—and establishing dedicated teams tailored to each segment’s specific needs, thereby upgrading service delivery.

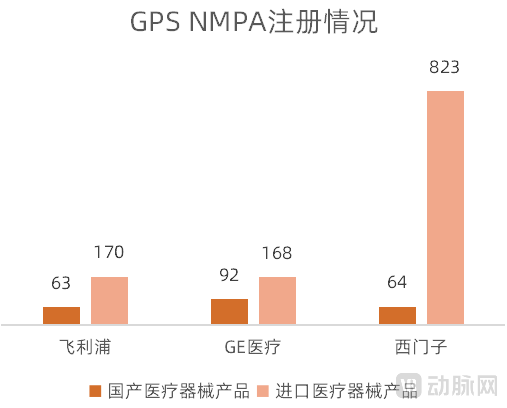

A further comparison of medical device registration certificates can, to some extent, quantify the “localization” achievements of GPS.

Data from the Center for Medical Device Evaluation’s medical device product database (as of March 30, 2022) shows that Philips has obtained more than one-third of its domestic medical device registration certificates in China, GE has exceeded one-half, and Siemens Healthineers holds a large number of registration certificates for reagent kits and detectors. Although Siemens’ localization rate is relatively low, its total number of certificates has already reached parity with Philips.

A brief statistical overview shows that Philips offers 1.5T MRI, CT scanners and core components, mammography systems, mobile DR, small and medium C-arm systems, and color Doppler ultrasound devices; GE provides 1.5T MRI, mobile DR, CT scanners, mammography systems, mobile DR, small and medium C-arm systems, digital subtraction angiography (DSA), and color Doppler ultrasound devices; Siemens offers 1.5T MRI, CT scanners and core components, mammography systems, mobile DR, small and medium C-arm systems, and DSA.

GPS NMPA Registration Status (Data Source: Compiled by VCBeat)

It is worth noting that the domestically produced medical device products approved by the NMPA mentioned above are almost entirely derived from low- to mid-end imaging-related equipment. However, when it comes to high-end devices such as 3.0T and above MR systems and high-slice CT scanners, the joint ventures of GPS (GE, Philips, and Siemens) in China only hold “Imported Medical Device Registration Certificates” and can only meet hospital demand through imports. This means that high-end medical devices, which constitute the core strength of GPS, are facing significant policy risks.

Ten years ago, against the backdrop of domestic medical imaging equipment manufacturers’ lack of core technologies, the “GPS” companies (GE Healthcare, Philips Healthcare, and Siemens Healthineers) faced no issues in maintaining their initial “localization” strategy of “domestic products for the low-to-mid-end market, imported products for the high-end segment.” However, multinational corporations have now lost their cost-performance advantage in the low-to-mid-end market, while facing policy constraints and competitive pressures in the high-end segment (United Imaging Healthcare has captured 32.1% of the domestic PET/CT market share). To reverse this downward trend, multinational enterprises need to identify new strategic responses.

Despite facing multifaceted pressures, GPS still holds many key cards. They can choose to regain the mid-to-low-end market through low-price strategies, or restrict the sales of core components; however, the approach most conducive to a win-win outcome for the market is likely an upgraded, advanced form of “localization.”

Currently, GE HealthCare and Siemens have not yet disclosed details regarding their “localization/full domestic production” strategies, but Philips is already poised for action.

Chen Shengyu, Senior Vice President of Philips Greater China and General Manager of the Precision Diagnosis Business Group, reiterated in an interview the importance of “localization” for Philips, breaking down the business unit’s localization initiatives for this year into four key points.

1. “Yuexiang” Series: Comprising the full range of ultra-high-end ultrasound products, this series will gradually expand its portfolio of China-made ultrasound systems over the next 1–3 years, achieving 90% local content by 2022 and 100% local content by 2024.

2. Molecular Diagnostics Series: Build an “end-to-end” complete value chain covering R&D, manufacturing, market access, sales, and services; make strategic investments in Sino United Health to co-create localized solutions.

3. MR: Achieving helium-free magnetic resonance imaging with the localization of high-end MRI systems such as Ingenia Ambition and 3.0T Elition. Prodiva, developed and manufactured locally, is sold to 57 countries worldwide, with the 1,000th unit scheduled for installation this year.

4. CT: Philips’ next-generation photon-counting CT, Hoeke, was launched globally and has achieved localization in China, with registration certification to be completed within the year. The Aurora CT, independently developed and manufactured by the Shenyang Product Innovation Center and the Suzhou Medical Imaging Base, is also a representative example of localized production.

“Currently, the R&D of CT and MR has largely been relocated to China,”The Suzhou R&D Center is responsible for 90% of the global R&D in the CT industry. The intellectual property rights generated from R&D and NMPA certifications are all held in China. In the future, 100% of the product lines of the Precision Diagnosis Business Group will be manufactured in China..” Chen Shengyu told VCBeat.

For multinational corporations, Philips’ localization has broken two barriers constraining its development. On the one hand,Products manufactured in China with intellectual property rights held by Chinese teams can be regarded as entirely domestically produced, thereby circumventing the policy constraints mentioned above.; On the other hand,This decision will help Philips consolidate its position in the high-end market and further gain market share.。

For a long time, after multinational corporations completed the research and development of new medical devices, they would typically apply for regulatory review and approval in their home countries, with market launch in China occurring several months or even years later.

For hospitals with substantial research demands, delayed market entry means that physicians are unable to access cutting-edge medical technologies, thereby preventing them from leveraging technological breakthroughs to overcome previous research bottlenecks. This results in a temporal lag in domestic R&D compared to international counterparts.

According to Philips, the comprehensive localization of CT and MR systems means that researchers in China are expected to gain immediate access to cutting-edge technologies, thereby bridging the research gaps previously caused by time lags.

Philips did not disclose the specific progress of PET/CT localization during the interview, stating that its strategic investment in and partnership with Sino Union constitute a key step in its “localization” strategy. VCBeat speculates that capturing market share through strategic investments and collaborations may be a more efficient approach.

Looking back over the past three decades, GPS has been able to rapidly take root in China thanks to its absolute technological leadership. Therefore, in a fully competitive market, the best strategy for domestic companies to break through is to “defeat technology with technology.”

A doctor from the Second Affiliated Hospital of Zhejiang University School of Medicine told VCBeat, “Radiologists’ preferences for medical imaging equipment are primarily driven by failure rates during operation and image quality after use. The equipment must not fail at critical moments of diagnosis and treatment, nor should it produce substandard images post-scan. Imported equipment has consistently been stable and reliable. While some domestically produced devices had issues in the past, their quality has now improved significantly, making them competitive with imported alternatives.”

However, healthcare is an industry with an exceptionally low tolerance for error. Many physicians have spent years using equipment from companies like GE and Philips Healthcare, becoming accustomed to the associated hardware and software operations. They have confidence in these devices, which ensures the normal conduct of diagnosis and treatment. Now that domestically produced equipment has caught up in terms of quality, it is essential to maintain this standard and gradually build trust over time.”

Therefore, rather than fixating on whether the equipment is domestically produced, we should focus on the quality of the devices themselves, as well as on the physicians who use them and the patients who receive care.

Medical development is slow and burdensome; we cannot always rely on policy to replace market choices.