Breakthrough in China's Imaging Upstream Sector: Revenue Soars as 'Bottleneck' Technologies Are Resolved

The once-obscure upstream segment of medical imaging is beginning to enter an era of profitability.

In the past, domestic breakthroughs in this field were long regarded as an insurmountable chasm.

An investor stated, “There is a wide variety of imaging equipment, with each type involving multiple core components, materials, and algorithms. The extensive supply chain poses significant challenges for breakthroughs by Chinese manufacturers. Meanwhile, international giants maintain stringent blockades on upstream source technologies.”

To better control the upstream supply chain, Trixell, a global leading supplier of digital flat-panel detectors, was jointly established by Siemens and Philips.

Over the past decade, although domestically produced core components have achieved isolated breakthroughs, they have yet to gain significant traction in terms of commercialization and market share. However, the upstream sector of the domestic medical imaging industry is now entering an accelerated phase of import substitution.

Data from the 2021 annual report of iRay Technology, the leading domestic X-ray detector manufacturer, showed that the company achieved an operating revenue of RMB 1.187 billion in 2021, a year-on-year increase of 51.43%; the net profit attributable to shareholders of the parent company was RMB 484 million, up 117.79% year on year; and the net profit attributable to shareholders of the parent company after deducting non-recurring gains and losses was RMB 342 million, representing a year-on-year growth of 72.29%, indicating rapid performance growth. Another X-ray detector manufacturer, Kangzhong Medical, reported an operating revenue of approximately RMB 342 million and a net profit of RMB 89.5268 million for the year 2021.

The gross profits of both companies are also on the rise. In 2021, iRay Technology’s gross profit margin reached 56.89%, an increase of 4.58 percentage points year-over-year; Kangzhong Medical’s gross profit margin rose from 44% in 2020 to 46%.

Meanwhile, the upstream imaging sector has also seen multiple rounds of financing. Previously, Sequoia Capital had invested in iRay Technology, which went public on the STAR Market with a market capitalization exceeding RMB 20 billion. Investors including Sequoia Capital, Northern Light Venture Capital, and Chende Capital collectively realized gains totaling RMB 1.546 billion through share reductions. The upstream core components segment, characterized by high investment requirements and challenging returns, is now beginning to reap the rewards of long-termism.

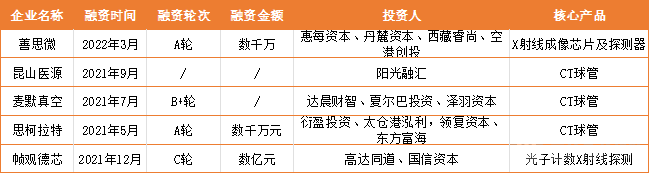

Upstream Financing Events in Medical Imaging

The performance of the detector largely determines the image quality, imaging speed, and dose rate of medical imaging equipment, making it the most critical component in such systems.

Why Have X-ray Detectors Broken Through in the High-Barrier Medical Imaging Market? What Insights Does Their Development History Offer for the Domestic Substitution of Upstream Imaging Components in China? VCBeat Has Analyzed This Sector.

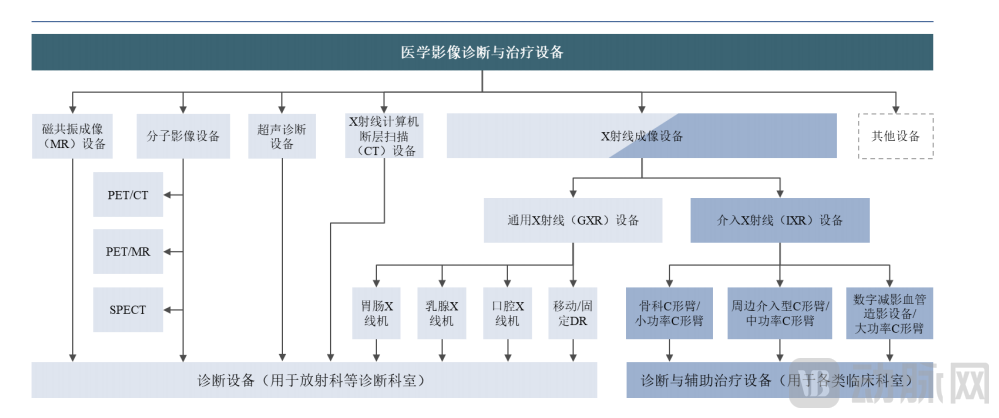

Medical imaging equipment is the largest subsector of China's medical device industry, with its market size reaching RMB 53.7 billion in 2020 and projected to approach RMB 110 billion by 2030.

In terms of the market size by segment, according to the prospectus of United Imaging Healthcare, the market size of magnetic resonance imaging (MR) systems in China reached RMB 8.92 billion in 2020 and is expected to grow to RMB 24.42 billion by 2030; driven by the strong demand brought by the COVID-19 pandemic in 2020, the market size of X-ray computed tomography (CT) systems in China reached approximately RMB 17.27 billion, and is expected to reach RMB 29.05 billion by 2030.

X-ray Imaging Systems (XR) include products such as DR, mobile DR, mammography units, gastrointestinal imaging systems, and C-arms. In 2020, the market size of XR in China was approximately RMB 12.38 billion, and it is projected to reach RMB 20.60 billion by 2030.

Classification of Medical Imaging Equipment

X-ray detectors are widely used in X-ray medical imaging equipment, including diagnostic X-ray systems (DR/digital mammography systems), therapeutic auxiliary devices (radiotherapy positioning systems/medical linear accelerators), interventional surgical equipment (DSA/C-arms), CBCT, and CT scanners.

The compound annual growth rate (CAGR) for both CT and XR products over the next five years is projected to be approximately 5%, a rate that is not particularly high compared to many rapidly growing segments within the medical device market.

How Can X-ray Detectors Achieve Counter-trend Growth Amid Limited Growth in Downstream Application Markets? The Rapid Growth of X-ray Detectors in 2021 Was Driven by Three Factors:

First, driven by the strong demand brought about by the COVID-19 pandemic in 2020, China's CT and DR markets experienced rapid growth.. The CT market size grew from RMB 11.76 billion in 2019 to RMB 17.27 billion in 2020. The COVID-19 pandemic also drove growth in the market for mobile DR products. A surge in downstream demand propelled the volume expansion of upstream X-ray detectors.

Apart from the fluctuations caused by the pandemic, the primary growth driver for X-ray detectors has consistently been the replacement of CCD-DR, CR, and film-based systems by new DR products.

The second major growth driver stems from the rapid expansion of cone-beam computed tomography (CBCT) and intraoral X-ray imaging systems in the dental market.Both CBCT systems and intraoral X-ray sensors used in dental clinics require X-ray detectors, and the penetration rates of both products remain relatively low in China. In recent years, with the rapid development of private dental healthcare services, the markets for CBCT and intraoral scanners have experienced significant growth.

In the field of dentistry, as the cost of complete systems decreases and dental implant technology becomes more widespread, CBCT all-in-one systems are gradually replacing standalone dental panoramic systems. Dental panoramic machines typically use a single set of linear array detectors, whereas CBCT all-in-one systems employ either two sets of linear array detectors plus one flat-panel detector, or one set of linear array detectors plus two flat-panel detectors. The transition from dental panoramic machines to CBCT all-in-one systems will drive growth in the application and market for digital X-ray detectors in the dental sector.

In 2021, the dental sector generated RMB 200 million in revenue for iRay Technology. Both cone-beam computed tomography (CBCT) systems and intraoral X-ray units used in oral diagnostics require X-ray detectors. iRay Technology’s dental customers include Meyer Optoelectronic, LargeV, Born Dental, Fussen, and Woodpecker.

In the dental market, domestic substitution is relatively easier to achieve. Public hospitals tend to prefer imported brands, while private hospitals are more inclined to adopt domestically produced brands due to cost-effectiveness considerations. Domestic X-ray detectors can expand their market share by leveraging their cost-performance advantage.

In ultra-tier-1 cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, the penetration rate of CBCT may have already reached 50%. According to estimates by Debon Capital, the domestic CBCT penetration rate in China remains below 30%, indicating substantial room for future growth.Intraoral Dental X-ray Imaging DeviceIt typically consists of an X-ray generation unit and its supporting components. It is used for dental X-ray imaging to obtain images for clinical diagnosis.

Cao Peiyan, founder of FrameSens, stated, “The global dental market is dominated by private clinics. In the past, domestic dental clinics in China primarily focused on procedures such as tooth extractions and fillings. With the emergence of diverse services like dental implants and orthodontics, clinics have a growing demand for digital tools. We believe that the rapid growth in dental X-ray imaging will continue to be sustained over the next five years.”

The third major growth driver comes from the industrial market and the veterinary market.In industrial applications, X-ray detectors can be used for industrial non-destructive testing. In the industrial sector, power battery inspection and semiconductor back-end packaging inspection have become new growth points for the application of X-ray detectors in recent years, especially with the increasing demand for new energy battery inspection. New energy battery companies have also begun to become core customers of X-ray detectors.

Large imaging equipment has entered a “technological silence period” in recent years, with no transformative breakthroughs in the industry, providing Chinese brands with a favorable opportunity to “catch up” with European and American brands.

In the past, the main battlefield for domestic substitution was in the mid-to-low-end market. In the field of X-ray detectors, there is a wide variety of detector types. What technical directions should future domestic substitution efforts focus on?

Since their inception, X-ray imaging devices have consistently pursued higher density, spatial, temporal, and spectral resolution, along with reduced X-ray dosage. From the 1980s to the present, X-ray imaging equipment has roughly undergone three developmental stages: the analog imaging stage, the indirect digitalization stage, and the direct digitalization stage.

X-ray detectors are continuously evolving in three major directions: ever-improving image quality, faster imaging speed, and progressively lower radiation dose. From the perspective of technological development trends, digital X-ray detectors are moving toward greater sensitivity and lower noise.

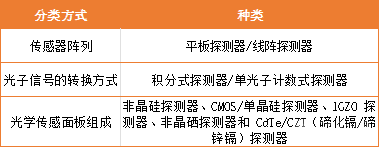

X detectors are classified into various categories using multiple classification methods.The most common classification is into direct conversion and indirect conversion.

Other Classification Methods for X-ray Detectors

Indirect-conversion X-ray imaging first requires a scintillator layer, which converts X-rays into visible light for detection by other technologies, such as CMOS detectors or amorphous silicon detectors. Scattering occurs during the conversion of X-rays into visible light.

In terms of characteristics, CMOS detectors offer the advantages of high resolution, low image noise, and fast acquisition speed. However, due to limitations on wafer sizes in the semiconductor industry, both process and raw material costs are higher than those for amorphous silicon. Consequently, CMOS detectors currently hold a distinct advantage in applications involving small-sized dynamic X-ray imaging equipment.

Amorphous silicon flat-panel detectors generally require a scintillator coating on the surface, primarily consisting of cesium iodide or gadolinium oxysulfide. Among these, cesium iodide offers high photoelectric conversion efficiency and superior image quality, but at a higher cost. Currently, amorphous silicon flat-panel detectors are the mainstream products in the market, characterized by mature technology, good image quality, and high stability.

Direct conversion refers to the direct conversion of X-rays. X-rays pass through the object being imaged and are directly converted into electrical signals by a detector array, which are then converted into digital signals to achieve direct imaging.

Currently, two technologies are used for direct conversion: amorphous selenium technology and photon-counting technology. Due to limitations in material science, amorphous selenium exhibits poor stability, is highly susceptible to external environmental factors, and is prone to damage, resulting in high maintenance costs. Nevertheless, many hospitals continue to adopt amorphous selenium detectors because of their superior imaging quality.

Hologic, a global leader in medical diagnostics, employs dedicated amorphous selenium direct digital flat-panel detectors in its mammography systems. In developed markets, Hologic holds a market share exceeding 70%. Mammography demands high spatial and contrast resolution, areas where indirect detection technologies underperform; consequently, Hologic’s products are highly favored in developed countries due to their superior image quality. However, owing to cost constraints, amorphous selenium imaging is primarily limited to breast imaging applications.

In direct detection, photon-counting detectors count X-ray photons individually by employing high-speed application-specific integrated circuits (ASICs). Compared with traditional integrating photodetectors, photon counters introduce no additional electronic noise, thereby effectively reducing radiation dose. Meanwhile, optimized multi-energy spectrum experimental designs provide a foundation for material identification, which will significantly improve detection rates. The acquired image signals are free of dark noise, exhibit high grayscale resolution, and offer an ultra-wide dynamic range. Single-photon counting flat-panel detectors can measure not only the intensity distribution of the incident light field but also its energy spectrum distribution. Compared with amorphous selenium flat-panel detectors, photon-counting detectors are less sensitive to ambient temperature and humidity, resulting in higher reliability and lower maintenance costs.

Photon-counting detectors are widely recognized as the next-generation X-ray imaging technology. However, a current limitation of photon-counting detectors is their inability to form large-area, seamless detector panels, which is related to their reliance on CMOS integrated circuit chips for signal readout. In contrast, large-area detectors typically employ TFT sensors.

Therefore, photon-counting detector products are currently mainly applied in mammography systems, intraoral scanners, and CBCT. Siemens has implemented photon-counting detectors in CT systems.

From the perspective of R&D challenges, photon-counting X-ray detectors involve multiple technologies, including semiconductor materials, chip design, packaging processes, and algorithms. Few companies worldwide have fully mastered this technology.

Photon-counting X-ray detector technology also provides domestic companies with an opportunity to overtake competitors on the curve. FrameView, a Chinese company, is dedicated to the development and manufacturing of photon-counting X-ray detectors and complete systems. It currently offers mammography systems, dental imaging systems, and a range of research-grade detectors.

Furthermore, technologies such as CMOS, IGZO, flexible substrates, spectral detection, and CT detectors are also key R&D directions within the industry.

Within the overall landscape of medical imaging, only digital radiography (DR) has achieved a high rate of domestic substitution. Currently, the localization rate for DR equipment in China has reached 70%. The main domestic brands in the DR equipment market include Wandong, Angell, Mindray, Perlove, United Imaging, Lanying, and ShenTu.

For other imaging products to achieve domestic substitution, it is first essential to recognize that DR’s success in replacing imported alternatives among numerous medical imaging products is closely linked to its underlying industrial chain.

An imaging industry practitioner stated, “The underlying technology of DR originates from display screens. Domestic panel manufacturers, represented by BOE, have achieved high maturity in amorphous silicon technology. The maturity of the industrial chain has laid a solid foundation for domestic imaging companies to achieve import substitution.”

Among other medical imaging products, domestically produced devices face the challenge of overcoming numerous component-related bottlenecks. Taking the core ADC (Analog-to-Digital Converter) chips in CT detectors as an example, these chips are responsible for converting X-rays and other radiation into images visible to users during CT scanner operation. Currently, most ADC chips used by Chinese CT manufacturers are sourced from foreign chipmakers. From a materials perspective, another significant hurdle is whether domestic manufacturers can produce stable and reliable cesium iodide and gadolinium oxysulfide scintillator coating materials.

“Therefore, the challenge in this field is that overcoming a single technical barrier yields minimal results, as there are still multiple hurdles across the entire industrial chain.”

This is also why imaging equipment comprises numerous components, attracting many domestic manufacturers. Chinese producers of high-voltage generators include Wandong, Neusoft, Derunte, and Guangxi Junlong; domestic manufacturers of X-ray tubes include Hangzhou Wandong and Kailong, though they have not secured a significant market share.

How Can Domestically Produced Core Imaging Components Break Through in the Future?

Cao Peiyan, founder of FrameSight, stated, “Replacing imported medical imaging systems in China is exceptionally challenging. Given the gaps in the domestic supply chain, we would need to build a complete ‘wheel’ from scratch. Meanwhile, others are already developing ‘jet engines.’ Therefore, instead of redundantly reinventing the wheel, we have focused on the latest technologies in the imaging field, pursuing independent innovation and achieving R&D breakthroughs.”

China’s medical imaging equipment sector is still undergoing continuous consolidation. Companies with weak technical capabilities will be eliminated, and those opting for low-barrier, follower-style innovation are highly prone to falling into a trap of product homogenization and price-based competition. Only companies with globally innovative capabilities can secure a certain share in the broader global market.