Q1 2022 Global Healthcare Industry Capital Report: Investment Sentiment Turns Cautious, Hong Kong Emerges as Preferred IPO Destination for Chinese Healthcare Firms

I. The mutation of the novel coronavirus, energy shocks, significant market volatility, and economic inflation negatively impacted global healthcare financing in Q1 2022. Compared with the same period in 2021, although the number of financing deals reached a record high, the total amount of healthcare financing decreased, reflecting investors’ widespread caution.

II. In the medical device industry, capital continues to concentrate on high-valuation “golden” sectors such as early cancer screening and genetic testing. Additionally, the recurring nature of the COVID-19 pandemic has created new opportunities for antigen self-testing products. Investment in the digital health sector cooled in the first quarter, with investors prioritizing the efficacy of clinical solutions.

III. Leading institutions are adopting a more cautious approach to investing in the healthcare sector, while domestic investment firms favor innovative medical technologies.

4. Israel leverages innovative technology to drive the development of its healthcare industry, while the Jiangsu-Zhejiang-Shanghai region accounts for half of all healthcare financing deals in China.

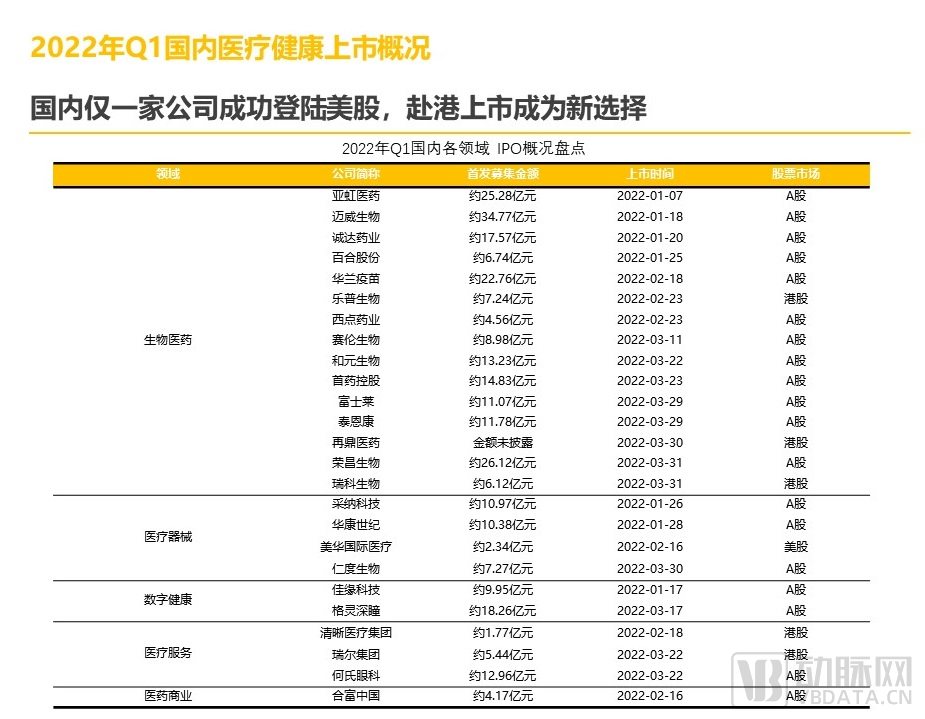

V. Chinese healthcare companies face setbacks in U.S. IPOs, turning to Hong Kong as a new alternative.

VI. Top 10 Most-Funded Companies in Q1 2022: NovuHealth Leads Globally with $760 Million in Financing, While Domestic Synthetic Biology and Large-Molecule CDMO Sectors Attract Significant Capital Interest.

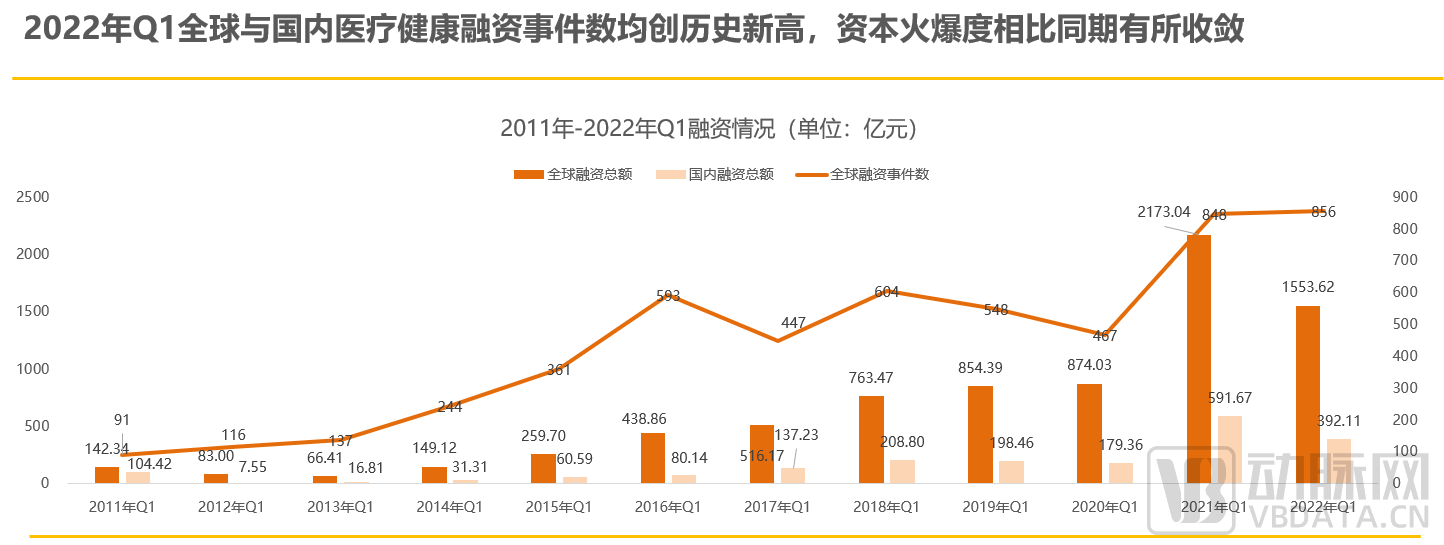

1.1 In Q1 2022, the number of healthcare financing deals globally and in China both hit record highs, while capital enthusiasm moderated compared to the same period.

In Q1 2022, there were a total of 856 financing deals in the global healthcare primary market, representing a slight year-on-year increase. The total financing amount declined significantly but remained the second highest on record, reaching approximately RMB 155.3 billion. Compared to the capital surge in the healthcare industry in 2021, investor sentiment cooled in Q1 2022: while the number of financing deals increased, the total financing amount decreased. In China, trends largely mirrored the global pattern, with the number of financing deals hitting a historical high of 326 in Q1 2022. Although overall market enthusiasm did not match that of the same period in 2021, capital remained optimistic about the healthcare industry in 2022.

Considering multiple factors, we judge that the catalytic effect of the COVID-19 pandemic on the influx of capital into healthcare remains intact, and investor enthusiasm for the healthcare industry has not waned. Furthermore, compared with the herd-like investment behavior observed in 2020, capital in Q1 2022 continued the attitude toward startups seen in 2021: tolerance has increased, enabling more promising and high-growth startups to secure funding.

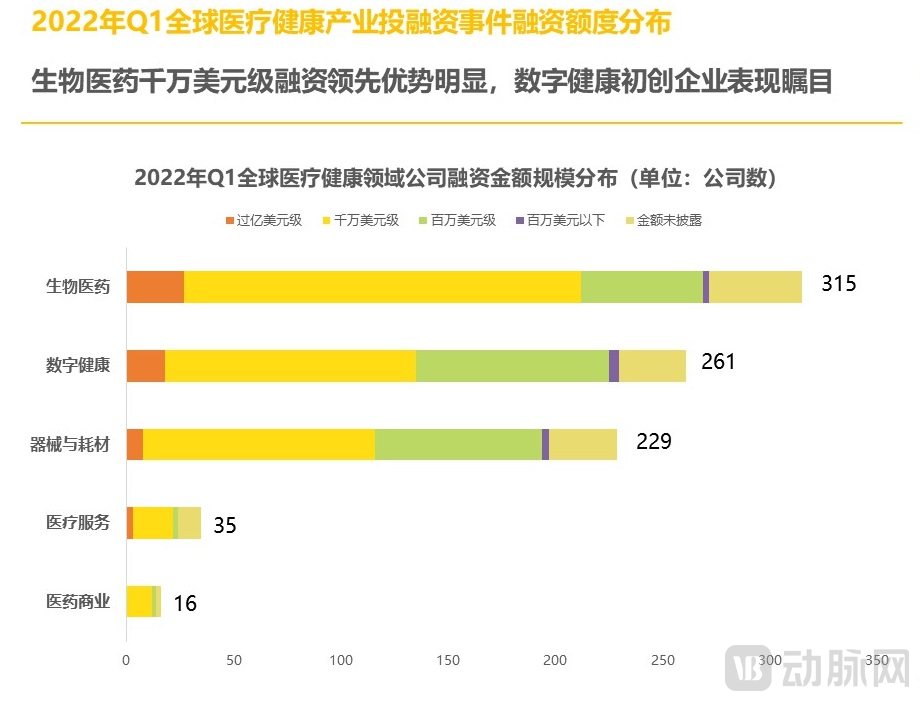

1.2 A total of 56 financing deals exceeding $100 million occurred in the first quarter, with financing rounds in the tens of millions of dollars increasing year-on-year.

In Q1 2022, there were 56 financing deals exceeding $100 million globally in the healthcare industry, accounting for over 6% of the total financing amount in Q1, which was lower than the same period in 2021; more than half of these deals involved companies in the biopharmaceutical sector.

Financing deals in the tens of millions of dollars were the most numerous. Meanwhile, biopharmaceutical companies accounted for the largest share and demonstrated clear advantages, widening the gap with companies in the digital health and medical device sectors.

However, among financing deals valued in the millions of dollars, digital health companies accounted for the largest share, with most concentrated in seed and Series A rounds, indicating that capital was particularly focused on early-stage startups in the digital health sector this quarter.

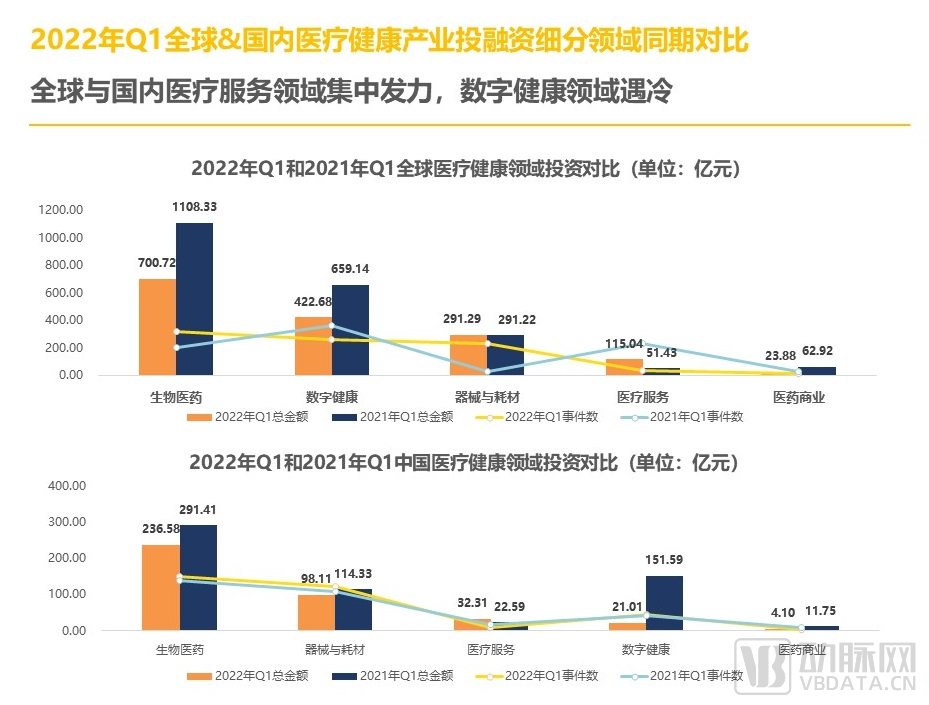

2.1 Concentrated Efforts in Global and Domestic Healthcare Services, While Digital Health Cools Down

In Q1 2022, total financing in the global biopharmaceutical sector and the medical devices and consumables sector both declined compared to the same period in 2021. The digital health sector, which saw robust activity throughout 2021, cooled down in the first quarter, with this trend being particularly pronounced in China.

Part of the reason lies in the fact that some companies in the digital health sector, particularly in digital therapeutics, achieved exits through SPACs in 2021, while their average stock prices experienced a significant decline. This has sent unsettling signals to investors in the digital health space, forcing investment to become more cautious. In China, funding for the digital health sector has become more concentrated, and the activity level of emerging enterprises is far lower than it was in Q1 2021.

Furthermore, the number of financing deals in the global healthcare services sector increased by approximately 125.5% year-on-year, with third-party service providers remaining the primary magnet for capital in this field.

2.2 Top Global Financing Tags: Biopharmaceuticals, Healthcare Informatics, R&D and Manufacturing Outsourcing, IVD, Internet + Healthcare

In Q1 2022, tags such as biopharmaceuticals, healthcare informatization, R&D and manufacturing outsourcing, and IVD exhibited high popularity.

In terms of funding round distribution, Series A financing events occurred most frequently, with 273 deals accounting for over 30% of all financing activities in Q1. Unlike the 2021 trend, where capital was more focused on companies approaching maturity, startups demonstrated more prominent performance in Q1 2022.

It is worth noting that in 2021, the number of healthcare projects exiting via IPOs reached a record high of 373. In particular, the biopharmaceutical sector accounted for 217 deals, doubling year-on-year. This trend has drawn even greater capital attention to emerging enterprises at the start of 2022.

2.3 Global IVD and Domestic CXO Sectors See Steady Rise in Popularity, with Large Capital Flows Directed Toward Mature Overseas Virtual Care Companies

In the first quarter of 2022, there were a total of 73 financing events in the IVD sector, with the total financing amount exceeding RMB 11 billion, representing a 25% quarter-on-quarter increase during the same period.

The IVD sector continues to gain momentum, driven primarily by two factors. First, although two years have passed since the initial outbreak of COVID-19 in 2020, the recurring nature of the pandemic has created new opportunities for antigen self-testing products. As of March 31, 2022, 23 SARS-CoV-2 antigen detection reagents had been approved in China. Second, capital remains focused on high-valuation “golden tracks” such as early cancer screening and genetic testing, particularly early-stage seed projects. A notable example is Zhenzhun Biology, which received exclusive investment from Huiyuan Capital. The company has launched a digital PCR product with independent intellectual property rights, capable of absolute quantification of nucleic acid molecules with extremely high sensitivity. This technology holds broad application prospects in areas including liquid biopsy for tumor genes, non-invasive prenatal testing, pathogenic microorganism detection, gene therapy, and gene editing.

In 2021, the digital health sector in the capital markets closely followed the leading biopharmaceutical industry and surpassed the medical device sector. However, the situation changed in Q1 2022. In addition to a decline in both the number of financing deals and the total amount raised, funding in several niche segments also decreased significantly, making it difficult to predict annual trend shifts. Meanwhile, factors such as emerging variants of the coronavirus and energy shocks have sent unsettling signals to digital health investors.

Currently, investors are responding by focusing on clinical solutions that deliver tangible improvements, with virtual care—a field with broad application scenarios—being a prime example.

This risk-averse investment trend is evident in the concentration of substantial capital into remote care: In the realm of mental/behavioral health, Omada Health closed a $192 million Series E financing round and announced the integration of behavioral health into all its virtual care programs; meanwhile, funding for specialized care flowed to Ro, the senior care platform A Place for Mom, and the pediatric care platform Brightline.

In the first quarter of 2022, there were 33 financing deals in China’s CXO sector, with a total amount nearing RMB 8.4 billion, representing an increase compared to the same period in 2021, when capital markets were particularly hot.

It is worth noting that the outbreak of the COVID-19 pandemic in 2020 made the research and development (R&D) of vaccines and drugs a key focus of epidemic prevention and control efforts worldwide. As a critical link in the biomedical R&D industry chain, Contract Research Organizations (CROs) have played an increasingly significant role in shortening R&D cycles and reducing costs, thereby driving the rapid growth of the CRO industry from the demand side. Financing in China’s CRO sector surged in 2020, and the CXO industry maintained a steady growth trend from 2020 through the first quarter of 2022.

Among them, Novogene Health, which secured $760 million in financing, became the company with the largest single-round funding amount in Q1 2022. In September 2021, Novogene Health suspended its Hong Kong IPO process and turned to private market financing. This latest round demonstrates that Novogene Health remains highly attractive to private investors. According to foreign media reports, the company will continue to evaluate the possibility of going public.

3.1 The Gap in Deal Activity Among Active Investors Narrows as Top-Tier Firms Adopt a More Cautious Stance on Healthcare Investments

In Q1 2022, the most active investors in global healthcare were Sequoia Capital China and Qiming Venture Partners. Chinese investment firms demonstrated significant momentum this quarter, occupying five of the top ten spots globally. Compared with the first quarter of the previous year, the total number of deals by the top 10 most active global investors remained stable, but enthusiasm among leading firms for the healthcare sector declined.

Specifically, Sequoia Capital China Fund invested in 22 healthcare-related companies in Q1 2022, including 11 biopharmaceutical firms such as Metagenomi.

Notably, Sequoia Capital China and Qiming Venture Partners, the top two investors on the list, have jointly invested in Shize Bio, a developer of novel stem cell therapies. In January 2022, Shize Bio secured another round of financing amounting to nearly RMB 100 million. Its core team possesses unique and robust expertise in cutting-edge technological innovation and translational applications within the field of stem cell therapy.

3.2 Domestic Investment Institutions More Active Than Overseas Counterparts; Gene Technology and Innovative Medical Devices Become Top Capital Magnets

Sequoia Capital China Fund made 22 investments this quarter, followed by Qiming Venture Partners and Hillhouse Investment with 14 and 13 deals respectively, all continuing to focus on early-stage healthcare startups.

In terms of investment preferences, domestic investment institutions in China mostly favor companies linked to innovative medical technologies. Apart from some enterprises focusing on internet healthcare and medical informatization, companies leading in areas such as gene therapy drug development and innovative high-tech medical device R&D have taken the forefront. Examples include Jingyu Medical and Yuanhua Intelligence, whose fundraising capabilities have surpassed those of traditional pharmaceutical and medical device companies.

4.1 Global: The US Leads the World, Emerging Dark Horse Israel Ranks Among the Top Five

In Q1 2022, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, Israel, and Canada.

In 2022, the United States led globally with 424 financing deals totaling $16.154 billion (approximately RMB 105 billion), followed closely by China; together, the two countries accounted for 94% of the total global financing amount.

Meanwhile, Asia is playing an increasingly indispensable role in driving innovation within the healthcare industry. In 2022, Israel, an emerging “dark horse,” successfully broke into the top five global hotspots for healthcare investment and financing. Israeli healthcare companies have primarily focused on health informatics and smart healthcare, carving out a distinctive niche of their own.

4.2 China: Shanghai Leads in Total Financing, While Jiangsu Steadily Advances to Overtake Beijing

In Q1 2022, the five regions in China with the most concentrated healthcare and medical investment and financing activities were Shanghai, Jiangsu, Beijing, Guangdong, and Zhejiang, in descending order.

Since Shanghai surpassed Beijing for the first time in 2020 to become the hottest region for primary market investments in healthcare, it has consistently maintained its leading position. In Q1 2022, Shanghai recorded a total of 76 financing deals, raising over RMB 18 billion, thereby outpacing Jiangsu, the second-ranked province, by nearly RMB 9.1 billion.

The Jiangsu-Zhejiang-Shanghai region remains the backbone of healthcare innovation in China, accounting for half of the nation’s healthcare financing deals in Q1 2022 with 194 transactions. Financing activity in Jiangsu’s healthcare sector continued to gain momentum, reaching RMB 8.9 billion in Q1 2022, surpassing Beijing to rank second nationwide.

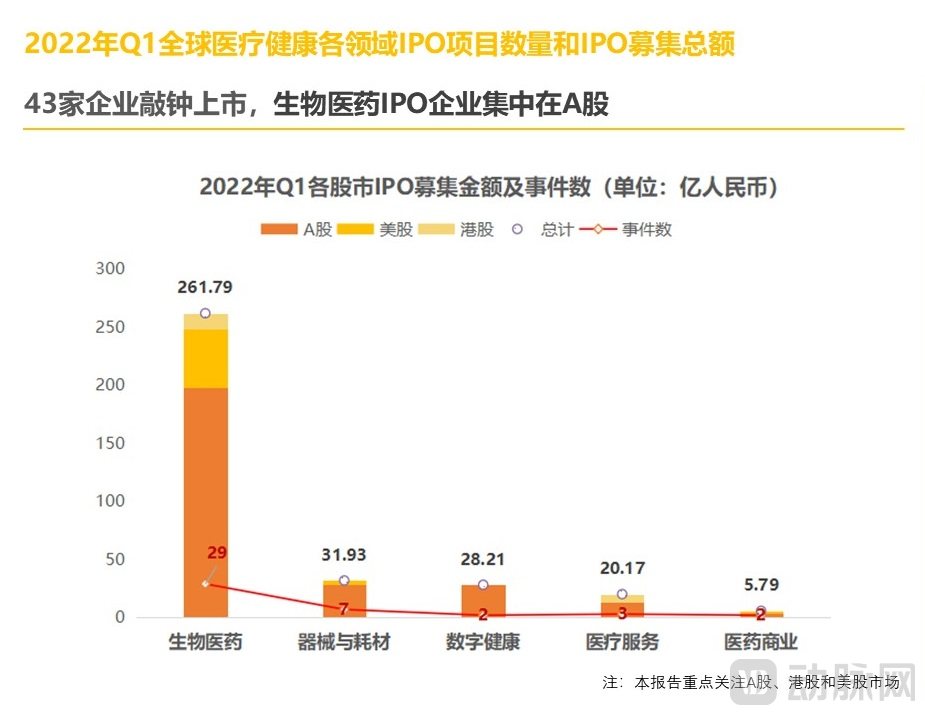

5.1 43 Companies Ring the Bell for IPOs, with Biopharmaceutical IPOs Concentrated on the A-Share Market

In the first quarter of 2022, a total of 43 companies completed initial public offerings (IPOs) worldwide, raising approximately RMB 34.8 billion, representing a 64% quarter-on-quarter decline.

Compared with the boom in 2021, when as many as 86 companies rushed to go public in Q1 alone, the healthcare industry got off to a shaky start in 2022.

Specifically, biopharmaceutical companies were predominantly listed on the A-share market, with 12 listings compared to only two in the same period last year. However, performance in the U.S. stock market was lackluster, with only 14 listings—far below the 46 recorded in Q1 2021—and fundraising amounts decreased by 86% quarter-on-quarter. The medical device sector also showed mediocre performance across the three major stock markets. In the digital health sector, only DeepGlint and Jiayuan Technology completed their IPOs in the first quarter of 2022.

5.2 Only One Company in China Has Successfully Listed on the U.S. Stock Market, Making Hong Kong Listing a New Option

In Q1 2022, the number of companies ringing the bell for IPOs on the three major stock exchanges declined.

Regarding the U.S. and Hong Kong stock markets, factors such as changes in policies and regulations slowed the pace of Chinese companies’ U.S. listings in the second half of 2021, prompting a significant number of healthcare firms to shift their focus to the Hong Kong Stock Exchange (HKEX). Since the HKEX allowed pre-revenue biotechnology companies to list in 2018, there has been a steady stream of pharmaceutical companies submitting prospectuses.

From Q4 2021 to Q1 2022, there was a surge in healthcare companies seeking listings on the Hong Kong Stock Exchange, causing those that had already submitted prospectuses to “queue” for approval. Some even postponed their listing timelines, resulting in very few healthcare firms going public in Hong Kong during Q1. Besides Newlight Vision, three other companies—Meinian Genomics, Northcore Life, and Infervision—are all expected to list on the HKEX after the first quarter.

6.1 Top 10 Global Financing Amounts: Chinese CXO Companies Lead Globally with $760 Million in Financing, Valued at $3 Billion

6.2 Top 10 Financing Amounts in China: Domestic Synthetic Biology and Macromolecule CDMO Sectors Are Highly Favored by Capital