Digital Transformation Drives Health Insurance Breakthrough in a CAGR 20% Market Serving a 2 Trillion RMB Blue Ocean

Amidst the wave of development in the insurance industry, the focus of attention has undergone iterations,From property insurance to life insurance and then to health insurance, the shift in what humanity values most also mirrors the evolutionary trajectory of human values.——From valuing property and life to prioritizing health.

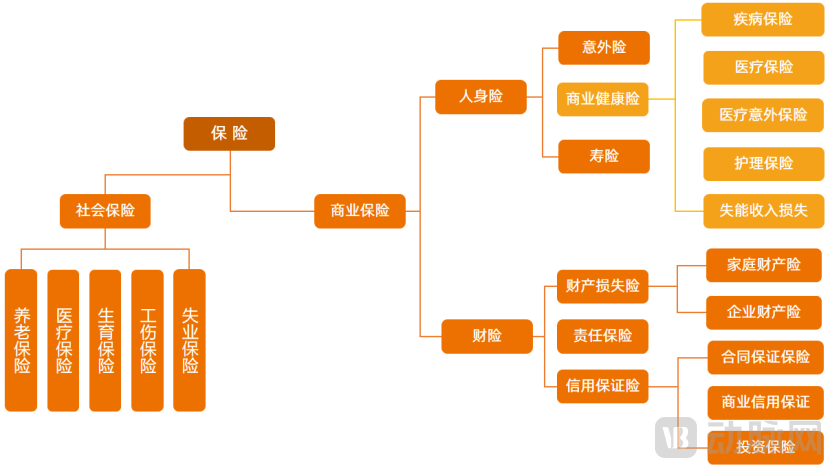

Insurance products are categorized into life insurance and property insurance. Within life insurance, health insurance differs significantly from life assurance.Life insurance transfers the risks of survival or death, while commercial health insurance transfers the risk of disease. Life insurance does not require process management, whereas health insurance requires management of the medical service delivery process.

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), commercial health insurance products currently sold by the insurance industry fall into five major categories: critical illness insurance, medical insurance, medical accident insurance, long-term care insurance, and disability income loss insurance (as shown in the figure below), with more than 5,000 products available.

Category of Health Insurance in the Insurance Industry, as Shown by the Light Yellow Legend (Data Source: VCBeat)

Health insurance has achieved rapid development in recent years. According to data from the China Banking and Insurance Regulatory Commission, as of December 2021, health insurance premiums across China reached RMB 844.7 billion, accounting for 18.81% of total gross written premiums and maintaining a year-on-year growth trend. Over the past five years, the share of health insurance premiums within the entire insurance industry has increased significantly.

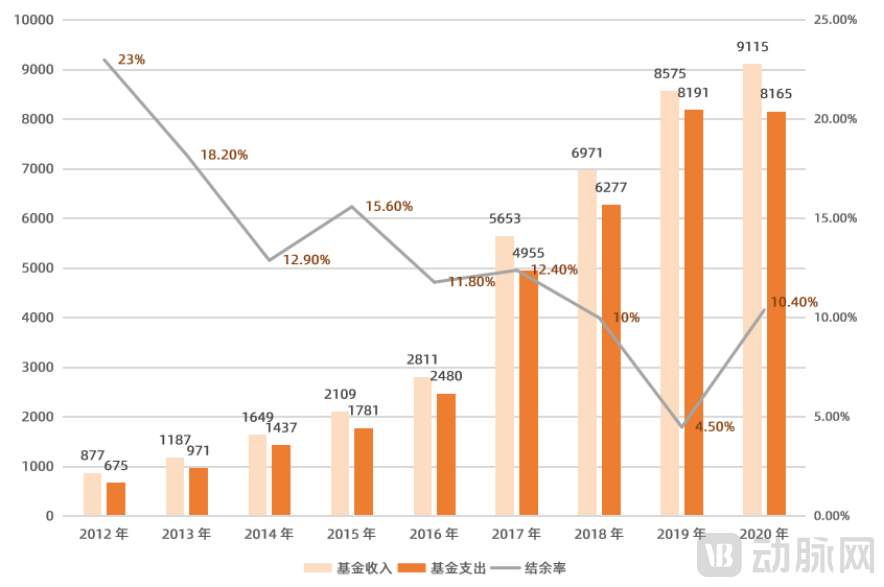

Revenue and Expenditure of the Basic Medical Insurance Fund for Urban and Rural Residents, 2012–2020 (Unit: RMB 100 million) (Data Source: National Healthcare Security Administration; Prepared by VCBeat)

Behind the data explosion lies not only the pandemic-driven surge in public health awareness, but also the profound impact of the digital technology revolution, further amplified by favorable regulatory policies. These factors have collectively propelled health insurance into a highly coveted sector. On the other hand,As the health insurance market expands rapidly, competition is intensifying and industry pain points are becoming increasingly prominent.

Client: Insufficient product coverage, with low awareness and purchase intent.

In China, the coverage rate of commercial health insurance is less than 10%, indicating low insurance penetration and insufficient market reach. In terms of awareness of short-term health insurance, 40% of respondents reported having only “heard a little about it,” while 10% stated they had “no knowledge at all.” This highlights an urgent need for market education to improve Chinese residents’ understanding of health insurance.

Enterprise Side: Difficulty in Customer Acquisition, Homogeneous Product Offerings, Low Information Sharing, and Disconnection from Medical Services

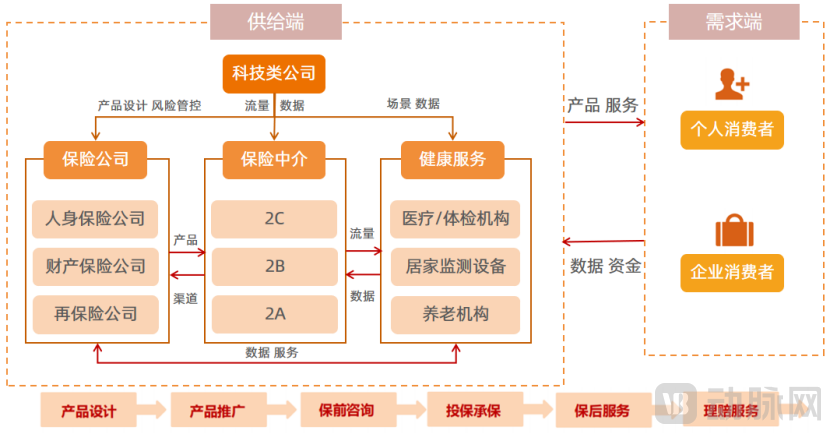

InRisk ProtectionOn the one hand, commercial health insurance products suffer from severe homogenization and fail to provide an effective supplement to basic medical insurance. InBusiness ManagementIn terms of professional operational capabilities, commercial health insurance exhibits a low level of specialization and insufficient integration with health management.Customer Acquisition ChannelsIn terms of customer acquisition, the reliance on a single channel is a major challenge for insurance companies. Conventional industry channels are hitting a growth ceiling, with low transparency, limited autonomy, and poor conversion efficiency.Big Data Applicationsaspect, big data infrastructure requires urgent strengthening. InMarketing Phase, inaccurate customer profiling, difficulty in reaching customers, and low efficiency in channel expansion are major obstacles encountered by insurance companies in their marketing efforts. InClaims Process, low levels of digitalization and automation pose significant challenges to fraud prevention.

>>>>Government Side: Mounting Pressure on Medical Insurance, Accelerating Aging Population, and Urgent Need for a Diversified Insurance System

Relying solely on social security will fail to meet residents’ diverse needs for medical protection. Commercial health insurance plays a supplementary role within the commercial medical insurance system, yet in 2019, China’s commercial insurance expenditure accounted for only 5.7%. Meanwhile, according to the World Health Organization’s definition, China has entered an aging society.

In response to the numerous pain points currently plaguing commercial health insurance, we propose several recommendations in the main text:

This article excerpts the core content of the report. You can scan the mini-program code to access the full report for free:

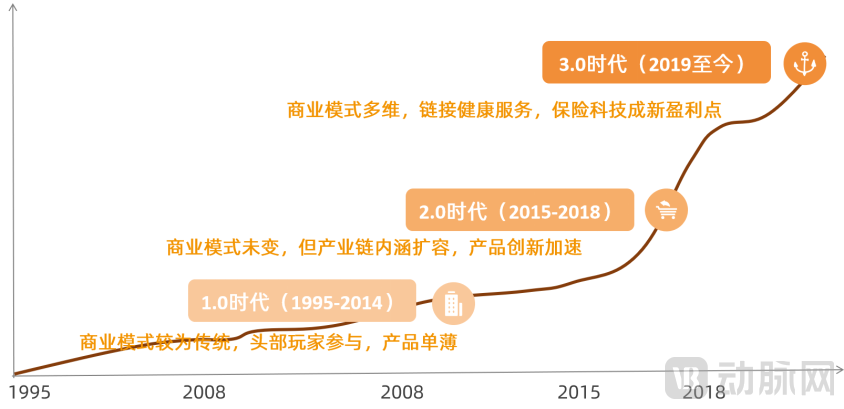

Looking back at the development of health insurance in China, since its inception in 1995, health insurance has continuously expanded its connotation and extension over the past three decades of societal change, keeping pace with market trends and evolving demands.

During the nearly two decades of its early development, the health insurance sector experienced sluggish growth, characterized primarily by traditional business models and limited product offerings. With the entry of leading internet companies, the participation of numerous small and medium-sized enterprises, a significant rise in third-party service providers, and the rapid supplementation and refinement of the industry chain, the launch of “Million-Yuan Medical Insurance” marked a growing emphasis on innovation in health insurance products.

Considering factors such as industry participants and product features, VCBeat categorizes the evolution of business models in the health insurance industry into three stages:

Era 1.0 (1995-2014),The business model is relatively traditional, with participation from leading players, but the product offerings are thin.

During this initial phase, the industry was in its early stages of development, characterized by traditional business models, relatively limited product offerings, and few additional policyholder benefits. In 1995, critical illness insurance was introduced in China, initially as a rider to life insurance policies. It covered a narrow range of conditions, typically including only seven major diseases, with the primary health insurance products being offered by leading large insurers. Comprehensive industry growth began in 1998, marked by an increasing number of health insurance providers and the expansion of individual insurance agents, both of which facilitated the development of the health insurance sector.

Era 2.0 (2015–2018), the mainstream business model remains unchanged, but the connotation of the industrial chain has expanded, and product innovation is accelerating

Phase II: The business model remained predominantly focused on covering disease-related risks, yet product innovation accelerated and the scope of the industry chain expanded. On the supply side, the number of participating enterprises increased significantly. In addition to traditional insurers, leading internet companies began entering this sector, a large number of small and medium-sized enterprises flocked in, third-party service providers multiplied, distribution channels expanded, and the industry chain rapidly matured, thereby intensifying competition within the sector. Regarding products, the launch of “Million-Yuan Medical Insurance” marked a growing emphasis on the breadth of disease coverage. However, as numerous insurers subsequently flooded the market with similar million-yuan medical insurance products, the issue of high product homogenization persisted.

Source: VCBeat.

Era 3.0 (2019–Present),Multidimensional Business Model Links Health Services; Insurtech Emerges as a New Profit Driver

In November 2019, the China Banking and Insurance Regulatory Commission (CBIRC) issued the Administrative Measures for Health Insurance, encouraging insurance companies to integrate health insurance products with health management services. In September 2020, it released the Notice on Regulating Health Management Services Provided by Insurance Companies, which clarified the concept of health management and stipulated that the cost proportion of health management services in insurance products could be up to 20%.This marks a clear trend: the future of commercial health insurance lies in integration with health services, and health insurance business models will become deeply intertwined with health service provision.

As policies become clearer and representative insurers and health service providers such as ZhongAn Insurance, Si Pai Health, and Yuanxin Huibao continue to grow and expand, integrating insurance with health services has become a key component of the business model for health insurance offered by insurers.

Meanwhile, insurtech is emerging as a new profit driver for insurers. In addition to offering insurance products, insurance companies are actively providing digital services.

Taking ZhongAn Online as an example, according to its disclosed semi-annual report, the company generated approximately RMB 260 million in technology export revenue in the first half of 2021, representing a year-on-year increase of 122%. In terms of client acquisition, ZhongAn signed contracts with 44 clients during the period, adding 16 new clients compared to the same period last year. These clients included leading insurance institutions such as China Taiping Insurance Group, China Pacific Insurance Group, AIA Life Insurance, Manulife-Sinochem Life Insurance, and HSBC Life Insurance. Meanwhile, approximately 75% of clients across the insurance industry chain made repeat purchases, demonstrating exceptionally high customer stickiness.

Globally, in the aftermath of the pandemic outbreak, stakeholders in the insurance industry have demonstrated strong and sustained demand for digitalization, while domestic regulatory policies have accelerated the industry’s digital transformation.

In terms of macro policy, from 2019 to February 2022, China’s banking and insurance regulatory authorities and the Insurance Association jointly issued nine policy documents related to insurance digitalization, including the top-level design document for insurtech, the “14th Five-Year Plan for Insurtech.” This fully demonstrates the state’s emphasis on the insurtech sector.

Since this period, there has been a surge in the number of small and medium-sized insurtech enterprises, and the industry is currently in the early stages of forming its competitive landscape. Meanwhile, mid-tier and leading insurance companies are either building their own health technology divisions or partnering with external players. On one hand, they leverage insurtech to enhance their own products, thereby reducing costs and improving efficiency; on the other hand, these insurers are also exporting technological services to create additional revenue streams.

Products – The Emergence of New Inclusive Health Insurance Plans

According to statistics from the China Banking and Insurance Regulatory Commission, local healthcare security administrations, insurance companies, and official operating platforms for local Huiminbao schemes, approximately 140 million people nationwide participated in Huiminbao in 2021, an increase of 100 million compared to the 40 million participants in 2020.

The explosive growth of “Huiminbao” reflects the substantial demand for health protection among urban populations and has made a significant contribution to building a multi-tiered medical security system with commercial health insurance. However, based on its current development and operational status, Huiminbao still faces various challenges and issues, including loss ratios and policy renewal rates.

Magellan Health stated in its survey with VCBeat that, based on the current development status of Huiminbao (city-specific supplemental medical insurance) products, future operational management should evolve in multiple directions. First, product design should be further refined, particularly by establishing comprehensive lists of out-of-pocket pharmaceuticals, in-hospital diagnostic and treatment services, and self-paid medical devices and consumables. Second, fundraising efficiency should be enhanced to ensure the sustainable development of these programs. Third, claims payment management should be streamlined to improve payment efficiency. Fourth, policyholders’ sense of benefit should be strengthened by providing value-added services tailored to users’ healthcare-seeking behaviors and perceived value.

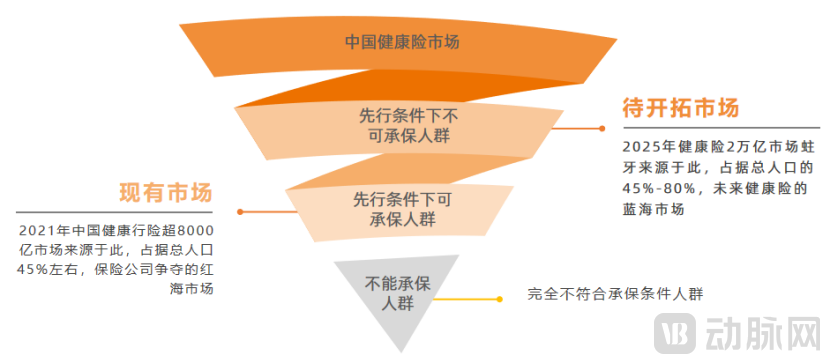

Coverage—Insuring Individuals with Pre-existing Conditions

Traditional critical illness and life insurance products have predominantly focused on covering healthy individuals. In the current health insurance market, valued at over RMB 800 billion, the majority of premiums come from currently insurable populations, making this segment a highly competitive “red ocean” from a corporate competition standpoint. Insurance product options for individuals with pre-existing conditions are limited, and most applications from such individuals require additional manual underwriting verification, which deters the majority of potential policyholders with coverage needs.

According to data from iSelect Technology, individuals with pre-existing conditions—who are currently excluded from coverage for major critical illnesses and other insurance products—account for more than 45% of China’s total health insurance market. With the rise of the health insurance sector, future breakthroughs toward a RMB 2 trillion market will depend primarily on developing and matching solutions to meet the needs of this population with pre-existing conditions.

Source: Chart by VCBeat

From a trend perspective, the shift in insurance product focus from covering “healthy individuals” to safeguarding “human health” is an inevitable path for the sound future development of the insurance industry. Expanding into the blue-ocean market of non-standard risks, providing better coverage for individuals with pre-existing conditions, further enhancing access to advanced medical care, and leveraging health insurance’s role in aggregated payment and efficiency improvement will serve as the foundation for the existence and continued growth of health insurance.

Users — The Rejuvenation of the Subject

According to data from Huize.com, a survey of post-1990s policyholders sampled from over 30 million internet insurance customers this year revealed that individuals in this age group hold an average of four insurance policies. Health insurance is the most preferred, accounting for 2.7 policies per person, followed by accident insurance, life insurance, and education endowment insurance.

Compared with other age groups, both the number of insurance policies purchased and the premium contributions by internet-savvy insured individuals born in the 1990s have shown a significant year-on-year upward trend. The average revenue per user (ARPU) has increased from RMB 547 to RMB 2,193, representing a fourfold growth. An analysis of policyholders born in the 1990s reveals that more than half are concentrated between the ages of 26 and 28. As this cohort enters their peak period for marriage and childbearing, they are more likely to make insurance plans for themselves and their families, which facilitates repeat purchases of insurance products.

Technology empowerment, namely insurtech, is becoming the outlet for breaking out of involution in the Health Insurance 3.0 era.

By integrating with technology and leveraging the power of big data, insurance companies have significantly enhanced product competitiveness and corporate management efficiency across various stages, including precise customer engagement, improved underwriting and pricing capabilities, risk control and claims management, and back-end services.

At present, China’s insurance intermediation sector remains in a phase of relatively extensive, high-speed growth. This stage is still characterized by the contradiction between the high complexity of intermediary informatization and low investment in intermediary information systems. Meanwhile, as customer segments become increasingly differentiated, institutions are demonstrating diverse market demands for technology-enabled services.

The Position and Role of Technology Companies in the Insurance Industry Chain (Data Source: Tencent Cloud University, VCBeat, Tianfeng Securities Research Institute)

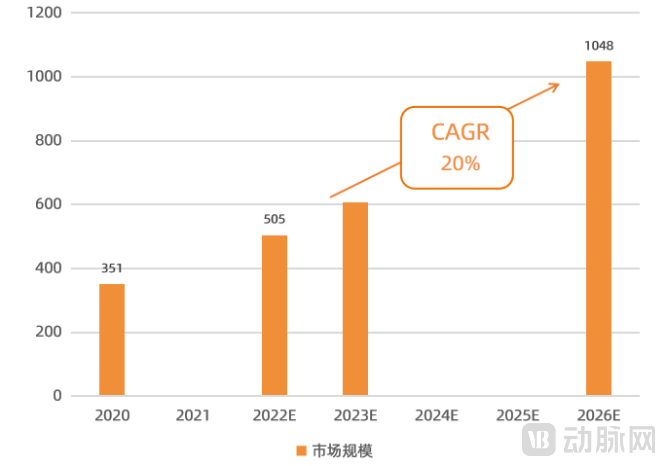

Data from the China Banking and Insurance Regulatory Commission (CBIRC) show that in 2020, insurance institutions’ total investment in information technology reached RMB 35.1 billion, a year-on-year increase of 27%.

Insurtech Market Size Forecast (Unit: RMB 100 Million)(Data source: China Banking and Insurance Regulatory Commission, VCBeat)

The total IT investment by insurance institutions is primarily influenced by the development of new insurance products, as well as the operation and maintenance and functional upgrades of existing insurers’ systems. With the growing trend of digitalization in the insurance industry, shifts in lifestyle and consumption habits in the post-pandemic era, and emerging insurance demands driven by new technologies, insurers are expected to allocate more funds toward system updates and transformations in the future.

Currently, most insurance companies allocate less than 1% of their premium income to technology investment. If this allocation increases to 2–3% of premium income for R&D in the future, the insurtech market size will experience a Davis double play, with the potential for breakthrough growth.Based on a compound annual growth rate (CAGR) of 20%, VCBeat estimates that the insurance technology market size will reach RMB 50 billion by 2022 and exceed RMB 100 billion by 2026.

Overseas Investment and Financing Overview

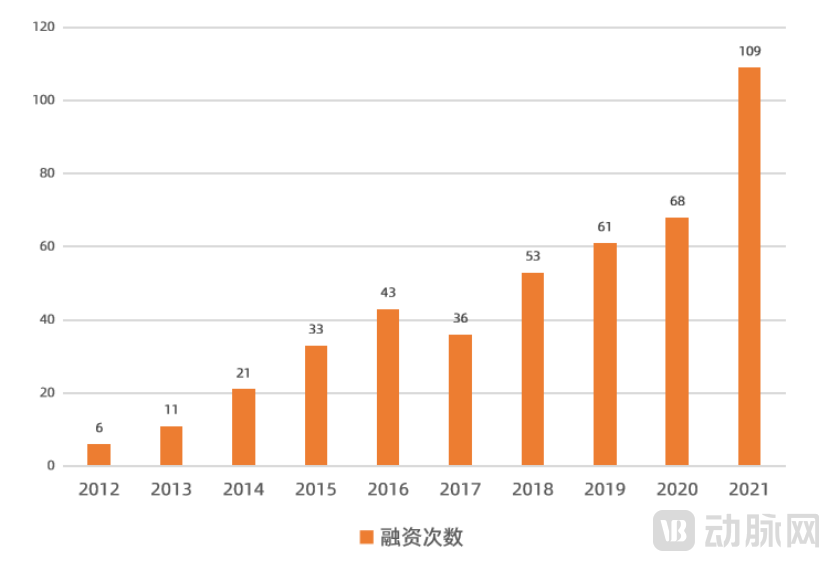

Global Investment and Financing in the Insurance Sector Continues to Heat Up. According to data from the Artery Orange database, the number of financing rounds in the global insurtech sector surged from 6 in 2012 to 68 in 2020, and further climbed to 109 in 2021, nearly doubling year-on-year. In terms of financing amount, the global insurtech investment and financing sector experienced rapid growth after 2015, with total funding reaching $3.89 billion in 2018 and $6.16 billion in 2019, representing a year-on-year growth rate as high as 56%. According to statistics as of February 2022, the total financing amount for the previous full year had exceeded $100 billion.

Global Insurtech Investment and Financing Continue to Grow (Data Source: Beijing Fintech Institute, VCBeat Database)

In terms of financing share, emerging markets such as Asia have performed exceptionally well. In 2019, China’s insurance technology sector accounted for 12% of global financing volume. However, despite China ranking second worldwide in total gross written premiums, the penetration of insurance technology remains insufficient. As insurers enhance their digital application capabilities in the future, China’s insurance technology market is poised for significant growth.

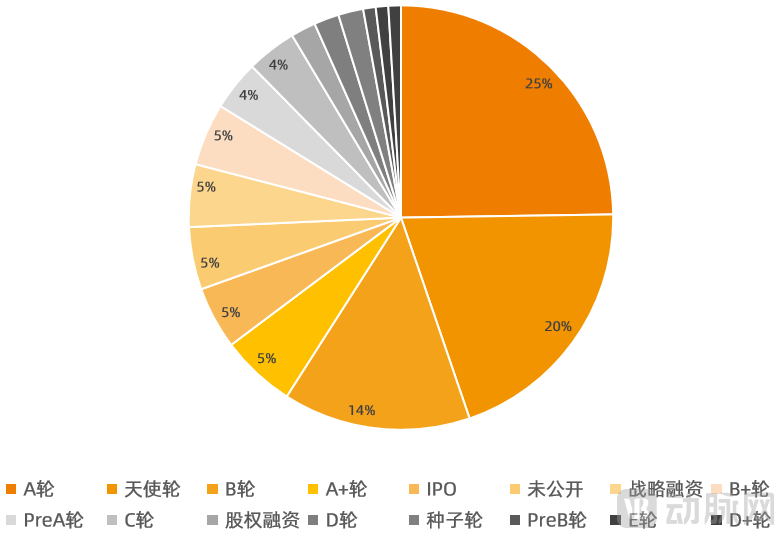

From the perspective of investment rounds, global health insurance financing is currently concentrated primarily in Series A, followed by angel and Series B rounds. IPOs are relatively few, accounting for 5% of all financing cases, while the proportion of strategic financing and Series C and D rounds has increased. The overall development stage of the health insurance sector remains relatively early; as industry maturity increases in the future, financing rounds will gradually shift toward later stages, and the market landscape will become more consolidated. In terms of financing amounts, deals in the tens of millions range account for the highest proportion, at 26%.

Distribution of Investment and Financing Rounds in Health Insurance (Data Source: VCBeat Orange Database)

From the perspective of investment entities, the number of global institutional investors entering the insurance and insurtech sectors is steadily increasing. Among these, insurtech remains an emerging sector, and will gradually exhibit a trend of diversified growth alongside concentrated large-scale financing in leading companies.

Domestic Investment and Financing Situation

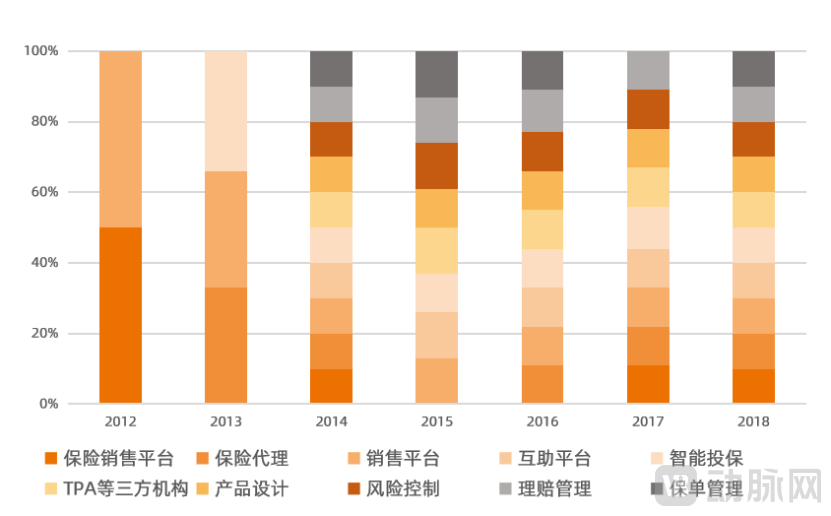

Investment and financing hotspots in China’s traditional insurance sector have shifted from online insurance sales platforms to mutual aid platforms, then to third-party administrators (TPAs) and other third-party entities, with current focus increasingly centered on the insurtech track. In recent years, projects in specialized segments of the insurance industry—such as product design, risk control, and claims management—have garnered greater favor from investors compared to previous years.

Shifts in Investment Hotspots: From Platform-Based Insurance to Intelligent Insurance (Data Source: Beijing Fintech Research Institute, VCBeat Database)

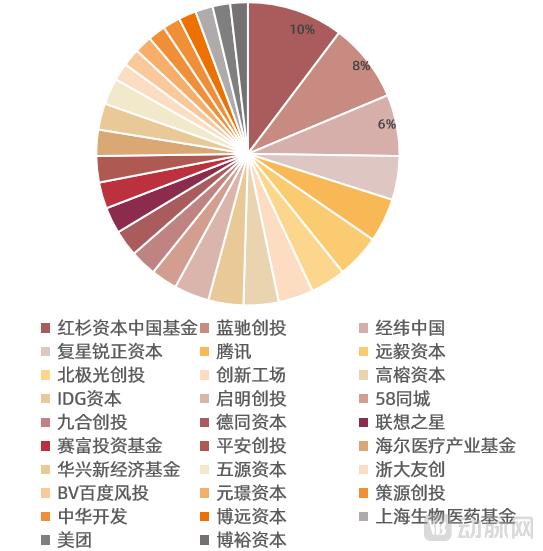

Over the past five years, more than 50 companies in China’s health insurance sector have secured financing, with hundreds of billions of yuan invested. Records for both the frequency and volume of industry funding have been repeatedly broken.

Since 2020, financing activities in the insurance technology sector have occurred frequently, with companies such as iSelect Technology, Huamei Haolian, UPlus Health, Nuanwa Technology, Junling Technology, Baolian Technology, and Shangyong Technology all attracting attention from multiple institutional investors.

We believe that asThe Era of Health Insurance 3.0in-depth development,InsurTechThe market size will continue to expand. Over the next 3–5 years, the insurtech sector is expected to undergo an initial round of industry consolidation, with a competitive landscape gradually taking shape. Currently,The insurtech sector will become the primary arena for competition in health insurance investment and financing, as well as a high-growth blue-ocean market that investors should focus on.

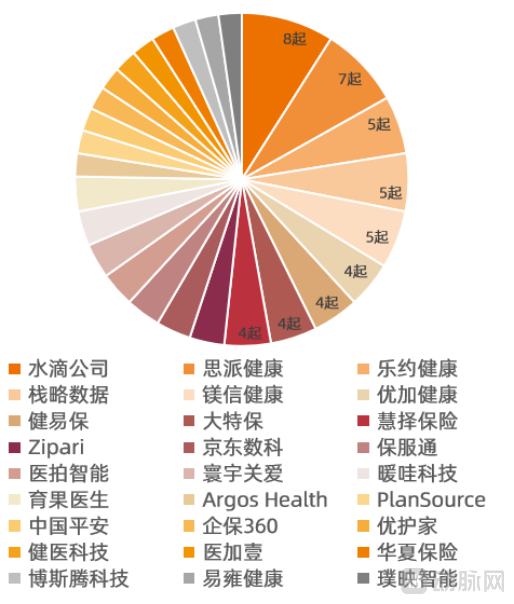

Frequency of Financing Rounds in the Health Insurance and InsurTech Sectors, by Company (Source: VCBeat)

Overall, companies favored by capital fall into three categories: product innovation, marketing channel innovation, and service innovation. We have compiled data on health insurance financing rounds in China from 2012 to the present. Waterdrop Inc., Sipi Health, Leyue Health, Zhanlve Data, and Magin Health lead their peers in financing activity. Among comprehensive insurance service providers that have received multiple rounds of additional investment, technology service companies offering enterprise-grade big data risk control platforms—such as Zhanlve Data, Junling Technology, Nuanwa Technology, and Aixuan Technology—are beginning to attract market attention.

Investment Frequency in the Health Insurance and Insurtech Sectors, by Company (Source: VCBeat Research Institute)

Market Sizing

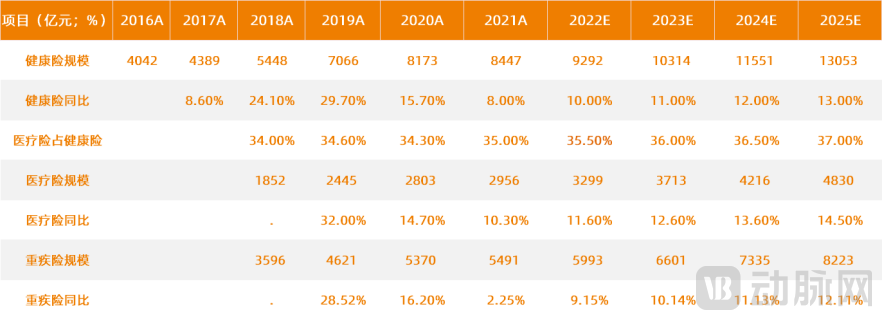

Under conservative assumptions, with a 10% growth rate in 2023 and a 13% growth rate in 2025, we project that the scale of health insurance will reach RMB 1.3 trillion by 2025, with medical insurance accounting for RMB 483 billion.

Market Size Estimation under Conservative Assumptions (Data Source: China Banking and Insurance Regulatory Commission, VCBeat)

Under conservative assumptions, we primarily consider factors such as the pandemic’s impact exceeding expectations and attrition within the agent workforce, which could lead to life insurance premium income falling short of projections, thereby affecting the market’s short-term accelerated expansion.

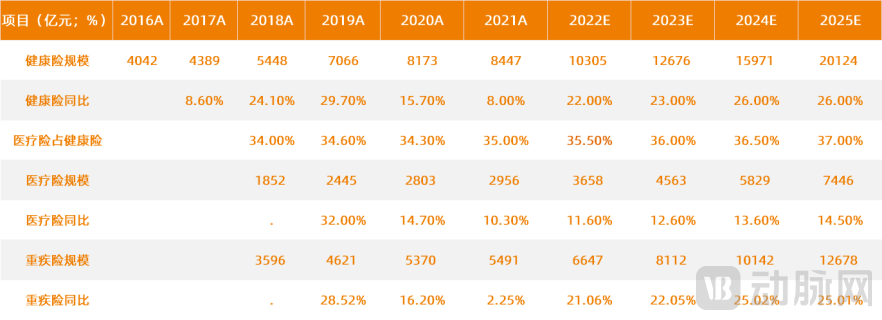

Market Size Estimation Under Optimistic Scenario (Data Source: China Banking and Insurance Regulatory Commission, VCBeat)

In an optimistic scenario, assuming that the year-on-year growth of health insurance will gradually improve from 2021 to 2025 following the post-pandemic recovery and the digital transformation of the insurance industry, with the share of medical insurance within health insurance increasing by 1 percentage point annually, and the overall growth rate of health insurance rising from +22.0% in 2022 to 26.0% in 2025 driven by the expansion of the insurable population, improved consumer awareness, and product diversification, the projected scale of health insurance premiums in 2025 is expected to exceed RMB 2 trillion, while medical insurance premiums are projected to surpass RMB 700 billion, indicating significant growth potential.

Strengthening Technology Empowerment

As the advantages of integrating technology with healthcare become increasingly prominent, technology will further empower health insurance in the future. By leveraging big data and artificial intelligence, it will significantly enhance insurance services in areas such as channel expansion, precision marketing, differentiated services, product design, actuarial pricing, operational optimization, risk control, and medical health management.

According to iResearch data, China's insurance institutions invested RMB 31.9 billion in technology in 2019. In 2020, their total IT spending increased by 27% year-on-year, and is projected to reach RMB 53.4 billion by 2022.

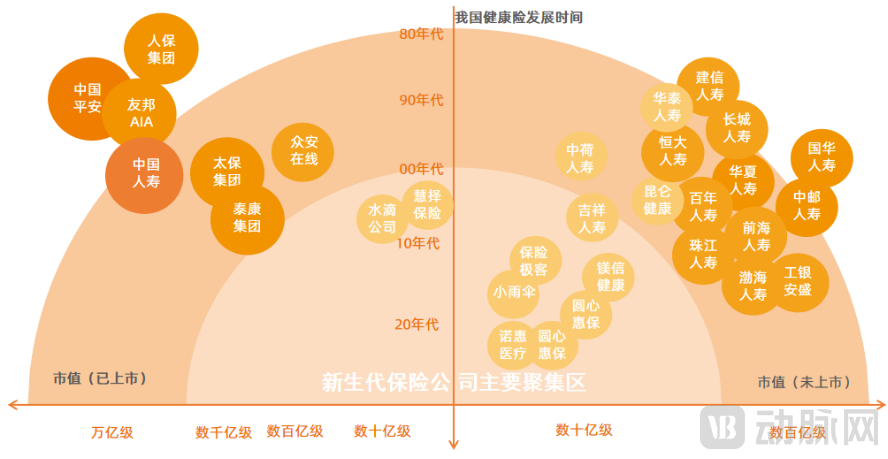

Overview of Insurance Companies’ Market Size, Timing of Health Insurance Expansion, and Technology Application (Data Sources: Choice Financial Terminal, Official Websites of Insurance Companies, etc.; Chart by VCBeat)

Among insurers with assets exceeding RMB 100 billion, many were established earlier; some have opted to build in-house capabilities, while others have chosen to collaborate with third-party providers, with sustained increases in technology investment. For instance, Ping An Insurance, a company with a market capitalization in the trillions of yuan, has stated that its digitalization investments will reach RMB 100 billion over the next decade. In contrast, most non-listed insurers with assets in the tens of billions primarily partner with third-party insurers. Meanwhile, newer-generation insurers valued in the single-digit billions, which have entered the health insurance market more recently, inherently possess digital attributes, such as Yuanxin Huibao.

Technology-driven high-quality development is an inevitable path for the industry, and traditional insurance enterprises are actively investing in digital transformation. The advancement of artificial intelligence, big data, blockchain, and cloud computing has reshaped the landscape of health insurance operations, enhanced operational efficiency, optimized internal management, and enabled precise risk control. Furthermore, these technologies facilitate deeper integration with health management services, thereby providing comprehensive and long-term health risk protection.

In-Depth Health Management

On November 12, 2019, the China Banking and Insurance Regulatory Commission (CBIRC) promulgated the “Administrative Measures for Health Insurance,” which for the first time included medical accident insurance within the scope of health insurance. As a result, health insurance primarily comprises five categories: medical insurance, critical illness insurance, disability income loss insurance, long-term care insurance, and medical accident insurance. The Measures also dedicated a separate chapter to health management for the first time, encouraging insurers to integrate health insurance products with health management services. These Measures came into effect on December 1, 2019.

On September 9, 2020, the General Office of the China Banking and Insurance Regulatory Commission (CBIRC) issued the “Notice on Regulating Health Management Services Provided by Insurance Companies” (hereinafter referred to as the “Notice”). The new regulations clarified the concept of health management and stipulated that the cost proportion of health management services in insurance products may reach up to 20%. In January 2020, the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector” proposed striving to expand the market size of commercial health insurance to exceed RMB 2 trillion by 2025.

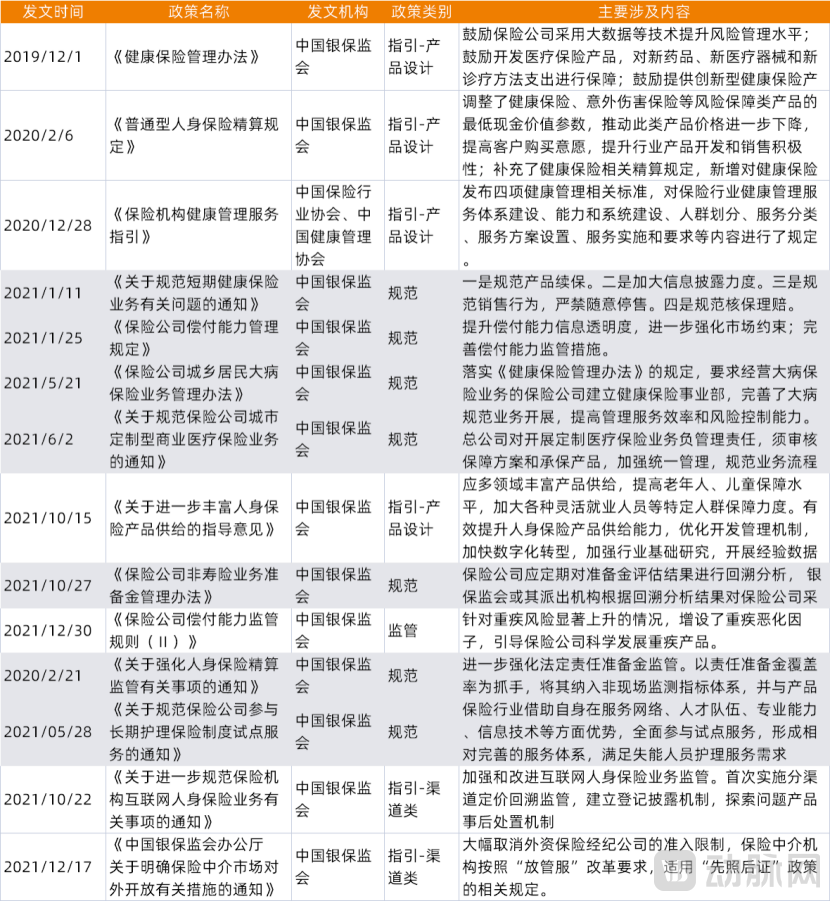

Health Insurance Industry Policies in Recent Years (Data Source: Arterial Orange Database, VCBeat Research Institute)

Within the health insurance sector, the health management market holds immense potential. In the future development of health insurance, services such as health consultations, health interventions, and chronic disease management will enhance service quality in areas like disease prevention and rehabilitative care. By shifting risk control to the front end, these measures will truly reflect the role of commercial insurance in supplementing and improving the social security system. During research interviews, Xu Bingyu, CEO of Huamei Haolian, stated to VCBeat that as professional service standards in the health insurance sector continue to rise, health management capabilities will become a key performance indicator. Companies with comprehensive lifecycle health management capabilities will stand out in industry competition.

Investment and Financing to Build an Ecosystem

In the past five years, more than 50 companies in the health insurance sector have secured financing, with tens of billions of yuan invested in the field. In 2019 alone, over 25 companies raised funds, frequently breaking records for both the frequency and volume of industry financing.

In the realm of investment, unlike other healthcare sectors that are primarily driven by financial investments, numerous deals in the health insurance sector are characterized by strategic investments. Investment firms are forming equity alliances with portfolio companies to build a healthy industrial ecosystem and expand their respective competitive moats. For instance, on March 5, 2021, Shanghai Medbank Health Technology Co., Ltd. announced the completion of its Series B financing round totaling RMB 1 billion, following a strategic investment received from China Life Reinsurance Company Limited in March 2020. Medbank Health has garnered support from platform shareholders across medical e-commerce, health insurance, and internet sectors, creating multi-sector synergy. In October of the same year, Beijing Yuanxin Huibao Technology Co., Ltd. underwent industrial and commercial registration changes after securing investment from Tencent, thereby opening up greater possibilities for future technological empowerment and user reach.

Refine Product Division of Labor

“In modern society, risk factors have become more complex. Product innovation should be tailored to the specific scenario-based needs of segmented populations to maximize the fulfillment of individuals’ personalized and differentiated health protection demands. By actively leveraging new technologies such as the internet, cloud computing, and big data, service offerings can be innovated to comprehensively enhance customers’ experience and sense of gain,” analyzed Professor Zhu Minglai, Director of the Center for Health Economics and Medical Security Research at Nankai University.

Within the health insurance industry chain, the roles of insurers, insurance intermediaries, technology companies, third-party administrators (TPAs), pharmaceutical e-commerce platforms, chronic disease management organizations, pharmaceutical companies, and physical examination centers are becoming increasingly specialized each year, with service offerings further extended. Collaboration among these industry players has grown closer across key stages, including product design, customer engagement, sales and operations, underwriting and claims processing, and medical services. Meanwhile, service-oriented entities such as technology companies and TPAs are steadily expanding, leading to a year-on-year increase in the granularity of labor division within the health insurance sector.

In the future, health insurance will gradually seek integration with fields such as biopharmaceuticals, pharmaceutical e-commerce, chronic disease management platforms, physical examination centers, and wearable devices. As the industry achieves deep convergence at the foundational level, the division of labor in its superstructure will become increasingly clear.

Final Remarks

The essence of insurance lies in regulating supply through mutual assistance. To achieve rational, efficient, and high-quality supply regulation, technology is an indispensable core element.

Insurtech is the fundamental driver of supply-side adjustment in health insurance. Only through technological empowerment by big data, cloud computing, and artificial intelligence can the health insurance industry achieve better future development and safeguard the health of more consumers.

Special thanks to the following industry experts for their strong support of this report (listed in no particular order):

Zhang LehuiOperating Partner, Changling Capital

Zhang QingfengCEO, Beijing Aixuan Information Technology Co., Ltd.

Feng HaoVice President, Kangfu Smart Pharmacy & Kangfu Health, Shanghai Magnesium Health Technology Co., Ltd.

Wan XiaolongShanghai Medbanks Health Technology Co., Ltd. – CMO, Medbanks Health

Xu BingyuFounder & CEO, Huamei Haolian Medical Technology (Beijing) Co., Ltd.

Wang QianBeijing Jinguan Technology Co., Ltd.

Sun WenjingBeijing Miaoyijia Health Technology Group Co., Ltd.

The above content is part of the report. You can scan the mini-program code to get the full text for free:

This report is part of the series of reports for the 6th Future Healthcare 100 Conference by VCBeat. The conference will be held from June 14 to 16, 2022, at the Shishan International Convention Center in Suzhou, Jiangsu Province, where the report will be released on-site.