Behind the Frenzied Fundraising and Sky-High Valuations: The Intensifying 'Involution' Among Medical Entrepreneurs

Arch Capital Group

A company responsible for insurance and reinsurance business

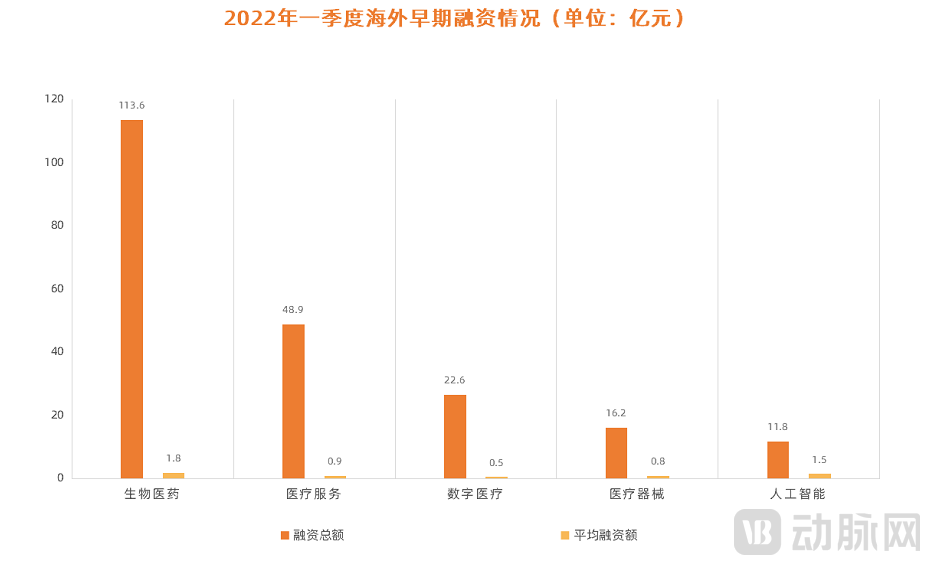

“Medical projects are becoming increasingly expensive,” is the common sentiment among many investors today. Although the persistent pandemic has made economic conditions and fundraising more difficult, the valuations of medical projects have instead risen. Taking overseas early-stage financing in the first quarter of 2022 as an example,196 Companies Have Raised a Cumulative Total of RMB 21.7 Billion in Financing, with an average financing amount of over RMB 100 million per enterprise—something unimaginable just a few years ago.

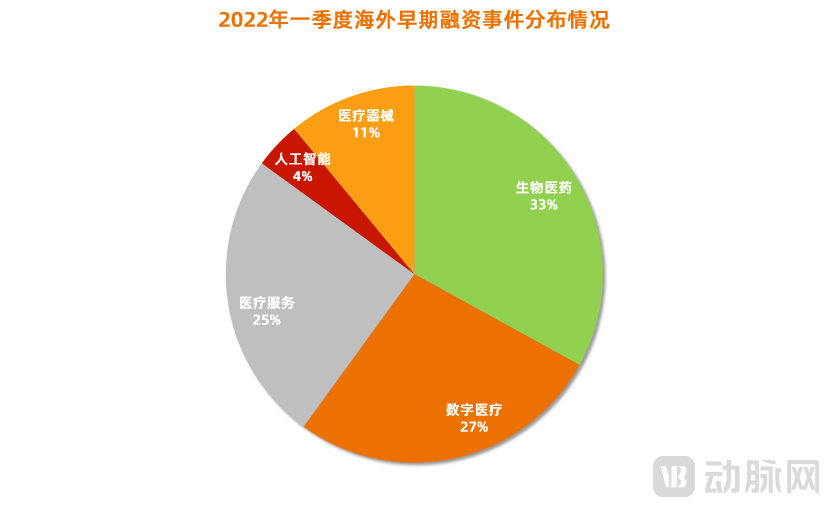

This phenomenon has emerged partly due to a process of eliminating the false and retaining the true, and also because the importance of healthcare has been highlighted against the backdrop of the global pandemic. Judging from early-stage overseas financing in the first quarter,Biopharmaceuticals hold an absolute lead in terms of financing amount, number of financing events, and average financing size.。

Q1 2022 Overseas Early-Stage Healthcare Project Financing Overview, Data Source: VCBeat

From these projects, it is evident that most have strengthened their core competencies. From initial concept-driven investment to the rigorous selection process during the capital winter,Capital places greater emphasis on the practical problems a project can solve, as well as the team’s capabilities and R&D strength.—Under this requirement, startups are forced into fierce internal competition. This necessitates that entrepreneurs adjust their mindset before entering the market—“Who do you want to be, what problems do you aim to solve, and where do your strengths lie?”. Entrepreneurs are becoming more rational by accurately positioning themselves and thinking things through before entering the market.

such as the company with the highest financing amount in the first quarterCellino, this technology company specializing in the scaled manufacturing of stem cells was founded in 2017 by three young scientists who graduated from Harvard University. Cellino integrates IT and optics to address cost and efficiency challenges in the manufacturing process of cell therapies. The company’s next-generation manufacturing platform leverages artificial intelligence (AI) and laser technology to automate cell therapy production, thereby reducing expenses and overcoming scalability limitations. This pioneering approach has the potential to reduce production costs by an order of magnitude and expand patient access to cell therapies.

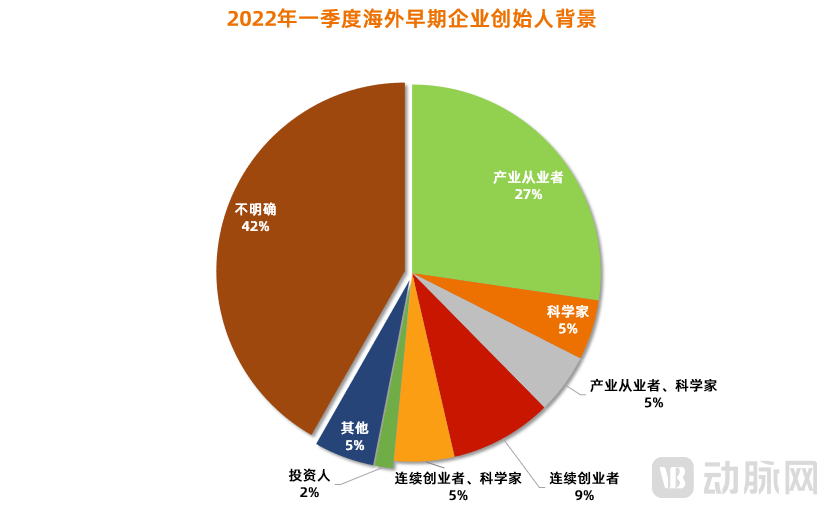

An analysis of the backgrounds of early-stage teams that have secured financing reveals that investors are raising their expectations for founders. Among these 196 funded companies, more than 50% of the founding teams have industry backgrounds, with the majority being senior executives from large enterprises who possess at least 10 years of experience and management expertise in the healthcare sector. Furthermore, 36% of these founders are serial entrepreneurs, some of whom even have prior successful exits and IPO experience.

Moreover, clinicians are increasingly entering the entrepreneurial arena, with their presence being more common in specialized fields such as mental health and dentistry. The majority of these individuals possess over a decade of experience as clinicians, nurses, or licensed pharmacists. Leveraging this professional expertise, they employ digitalization, artificial intelligence, and healthcare informatics to address challenges encountered in frontline medical settings.

Background of Teams That Secured Financing in Q1 2022; Data Sourced from Artery Orange and Public Records

In addition,Some Investors Have Also Entered the Entrepreneurial Arena, accounting for 10% of founding teams with industrial backgrounds. They favor technology-driven sectors such as biopharmaceuticals and medical devices. This preference is influenced both by their inherent investment logic and by their observations across the entire healthcare industry; they are more inclined toward “hardcore” tracks that address unmet medical needs, which have been relatively hot in recent years.Cell therapy, immunotherapy, high-value medical consumables, and mRNA vaccinesThey have more options.

In Q1 2022 financing, the project teams had backgrounds with investors; data sourced from Artery Orange and public information.

On the other hand, scientist entrepreneurship has also become a trend. Among these 196 companies, 32 have core teams originating from research institutes. Similar to investor-entrepreneurs, scientists also show a stronger preference for technology-driven sectors. For instance, 64-x and Gameto, co-founded by Professor George Church, known as the “godfather of genetics,” are referred to as“The Most Profitable Scientist”NextRNA Therapeutics, founded by Robert Langer, and Quris, an AI-driven drug discovery company co-founded by Langer and Nobel laureate Aaron Ciechanover.

Among them, Harvard University, the Massachusetts Institute of Technology (MIT), and Stanford University are the main forces. Scientists at MIT and Harvard focus more on the fields of biomedicine, medical devices, and artificial intelligence. There are six projects from Harvard University and five from MIT. Scientists from these two top universities are also keen on forming strong alliances, and the companies they co-found are sure to receive significant attention from capital investors.

Stanford University’s projects are exclusively concentrated in the biomedical sector. Coincidentally, the scientists behind all three initiatives chose to co-found their ventures with serial entrepreneurs from the industry.

Q1 2022 Financing: Companies Co-founded by Scientists. Data sourced from VCBeat and public information.

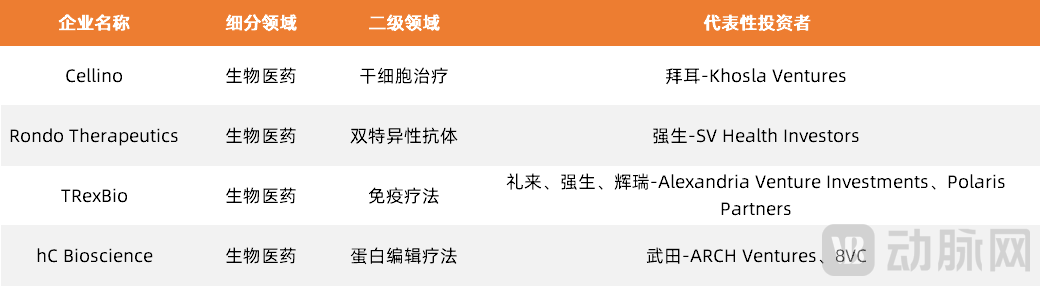

Of course, a select few companies have assembled all “three key elements of hyper-competition.” Their teams not only include industry veterans with many years of experience but also bring together serial entrepreneurs, investors, and scientists. Such startups can be regarded as the “kings of cutthroat competition,” and they remain concentrated in the biopharmaceutical and high-value medical device sectors, where substantial financing rounds and backing from star investors are the norm. Among them, RNAimmune, founded by Chinese scientist Dr. Shen Dong, announced in March that it had secured financing equivalent to approximately RMB 170.1 million, making it the best-funded company among these “king-of-the-hill” contenders.

Q1 2022 Financing: Startups That Have Assembled the “Three Elements of Involution”; Data Sourced from VCBeat and Public Information

Cross-boundary integration refers to the transition from entities of one attribute into the operations of another. Fusion, analogous to its physical counterpart, denotes melting or blending into a unified whole.

The emergence of a new class of instrumental technologies inevitably triggers large-scale cross-industry collaboration and integration within the healthcare sector. Examples include the evolution from the internet to internet healthcare, from information technology to bioinformatics analysis, from artificial intelligence (AI) to AI-assisted imaging diagnosis and AI-driven drug discovery, and from digital technologies to digital health. This convergence of new technologies with healthcare will also spark a new wave of healthcare financing.

In today’s early-stage investment landscape, the advantages of AI-driven drug discovery and digital health are becoming increasingly prominent. In overseas early-stage financing during the first quarter,A total of 10 AI-concept companies secured funding, primarily focusing on drug development, insurance payment, and care services.Among them, four AI-driven drug R&D companies raised nearly 700 million yuan in financing. Three of these companies were established in 2017 and 2018, a period that marked the peak of integration between artificial intelligence and healthcare. Meanwhile, Protai, founded in 2021, quickly secured funding by leveraging its significant advantages in proteomics and an end-to-end AI platform for drug discovery.

On the other hand, the cross-sector integration of artificial intelligence is also evident in its empowerment of the healthcare services sector. The availability of robust computing power has brought new solutions to tasks involving complex and granular calculations. A case in point is Tint, an AI-driven insurance payments company. Matheus Riolfi, the company’s co-founder, believes that insurance plays a crucial role in driving economic innovation. Leveraging artificial intelligence, the company aims to reshape the insurance landscape by embedding diverse products and services into insurance offerings. In February 2022, Tint secured $25 million in Series A financing, with investors including QED Investors, Nyca, Deciens, Y Combinator, and Webb Investment Network.

Digital technology is also empowering medical services. In the first quarter of 2022, a total of 50 digital health companies secured financing. These companies were highly concentrated, with the majority focusing on mental health, health management, and wearable devices.

During the COVID-19 pandemic, various forms of telemedicine have been on the rise, and the reality has undoubtedly forced a significant increase in patients' demand for digital technologies. Since approving the first prescription digital therapeutic in 2017, the U.S. Food and Drug Administration (FDA) finally saw an explosion in approvals in 2020, with seven products gaining FDA approval within half a year.

The pursuit of physical health has given rise to multi-billion-dollar markets in medical devices, gene therapy, and antibody development. However, mental health deserves equal attention. The National Alliance on Mental Illness (NAMI) in the United States describes depression as the “leading cause of disability worldwide” and a “major contributor to the global burden of disease.” In April 2016, the World Health Organization (WHO) released a report stating that depression and anxiety disorders cost the global economy approximately $1 trillion annually. According to NAMI data, this figure reaches as high as $193 billion in the United States alone.

Since 2000, the establishment of digital mental health companies has experienced two peaks, in 2012 and 2015 respectively, while the peak for initial financing occurred in 2015. In fact, some companies that later became industry benchmarks often secured their first round of financing within one year of establishment. For example, Lyra Health was founded in 2015 and completed its first round of financing in the same year; Quartet was founded in 2014 and secured financing the following year; Talkspace was founded in 2012 and obtained financing the next year; Calm was also founded in 2012 and raised funds the following year. Of course, there were exceptions, such as Akili Interactive Labs, which was founded in 2011 but did not secure financing until 2015.

Another reason for the rising popularity of digital mental health solutions is related to the social environment. High-profile suicides driven by mental health issues have sparked public discourse, while also exposing a lack of adequate mental health resources. Most digital mental health companies are concentrated in regions with high prevalence rates of mental disorders, such as the United States and the United Kingdom, where professional medical resources are severely strained. In the U.S., for example, patients seeking help from CBT therapists must first schedule an appointment, with the earliest available slots often being three weeks away. Digital CBT effectively utilizes the fragmented time of both doctors and patients, enabling timely access to care.

The selection of application scenarios reflects the high degree of specialization among overseas digital mental health companies, particularly those in the United States. Some products can even replace mental health professionals, rather than merely assisting in diagnosis and treatment. Based on their core business models, digital behavioral health companies offer services such as expert opinions, value-added services, and support networks. Among these, value-added services exemplify how innovative technologies are disrupting healthcare, a transformation currently being implemented by several U.S. digital mental health companies. For instance, Pear Therapeutics’ digital therapeutics have received FDA approval, while Akili Interactive Labs’ video game-based therapy is preparing to submit an application for FDA clearance. These products do not require professional guidance during use.

Secondly, health management is also a key application scenario in digital healthcare. This can be primarily divided into two categories: one involves out-of-hospital interventions for patients with conditions such as diabetes, kidney disease, and cancer; the other focuses on proactive health management for healthy populations, including disease prevention, nutrition, and physical fitness. The first category requires robust out-of-hospital intervention, a process that heavily relies on patient adherence and self-management capabilities. In this context, digital therapeutics serve to replace manual interventions by managing postoperative rehabilitation and side effects, while also providing support for physicians’ subsequent treatment decisions.

According to VCBeat’s “White Paper on Digital Therapeutics in China 2.0,” digital therapeutics are not limited by disease types but do have certain constraints regarding diagnostic and treatment processes and intervention methods, as they can only digitize a portion of services to replace manual interventions. Therefore, they are more suitable for indications that require long-term management, involve multiple interventions, have clear clinical guidelines, and are characterized by low patient adherence and self-management capabilities.

In addition to startups,Industry Giants Are Also “Competing Fiercely”On one hand, they pursue innovation through in-house R&D; on the other, corporate venture investment is also a common approach. Not only venture capital firms but also industry giants are witnessing the growth of innovative companies as corporate investors. For these large enterprises, when facing declining innovation capabilities and needing to acquire new information and ideas from external sources, initiating venture capital investments is a viable option. Such investments are typically related to the company’s existing business, closely aligned with its current strategy, complementary to its corporate strategy, or aimed at exploring potential business models.

Meanwhile, there is a cohort of investment firms in the venture capital community that specialize in early-stage discovery. These firms excel at entering when technological achievements are just emerging, strategically positioning themselves to seize first-mover advantages. To some extent, these institutions serve as trendsetters in investment. When these two types of investors converge on a project, it signifies dual endorsement from both the investment community and the industry. In the first quarter, four financing rounds involved participation from both industry giants and early-stage venture capital firms, with these companies being heavily concentrated in the biopharmaceutical sector.

Projects jointly participated in by pharmaceutical giants and prominent early-stage venture capital firms; data sourced from VCBeat.

Of course, the “involution” in healthcare venture capital is actually a long-term state. Giants are scrambling to get ahead in business development (BD), investments, and product filings; investment firms often quickly follow suit once they identify emerging investment trends. After undergoing the rigorous selection process of the capital winter, entrepreneurs have also joined the fray.

We often lament the toll that “involution” takes on our mindset and the drain it places on our sense of self. Yet, from the perspectives of entrepreneurship and venture capital, positive involution is not necessarily undesirable. For the market and patients, it signals enhancements in innovation and product performance. For investors, beyond the improvement in founders’ qualities and technological innovation, what is even more valuable is the deep reflection entrepreneurs engage in before entering the market. For entrepreneurs, while the outward appearance of “ramping up competition” may seem like added pressure, internally it encourages a more prudent and rational approach, prompting them to carefully consider their foundational strategies and objectives. Planning thoroughly before taking action may well prove to be a beneficial practice.