Sequoia Dominates Early-Stage Healthcare Investments as 71 Firms Split Over RMB 1.5 Billion in April

HemaCell

Cell Therapy Drug Developer

During the recently concluded May Day holiday,Everyone may be inOn the bed where one rests, at the dining table where one eats, or even on the way to get a nucleic acid test, only Orange Bureau,Have always kept a close watch on early-stage healthcare projects.。

Data sourced from VBInsight.

Data sourced from VBInsight.

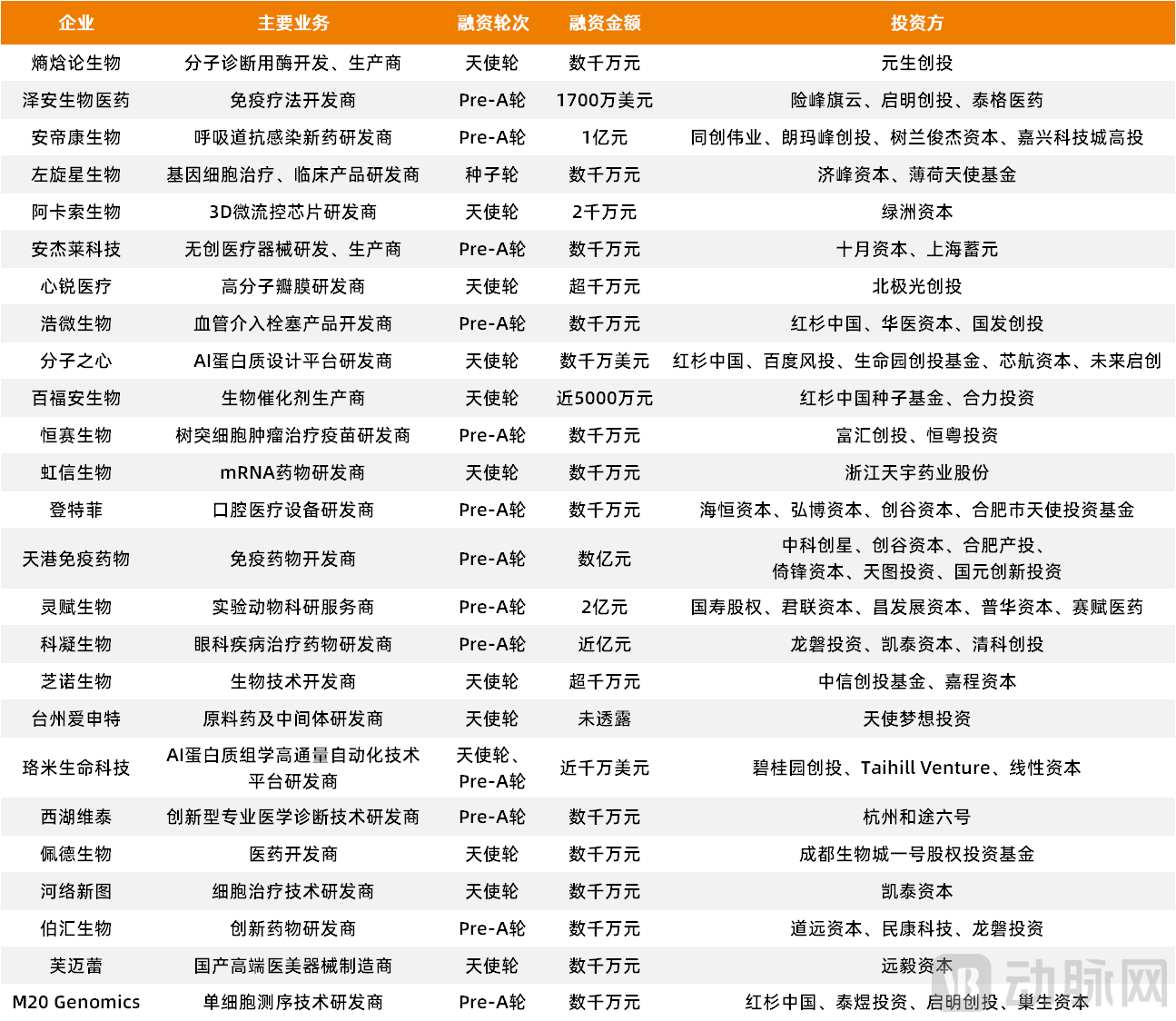

According to VCBeat, a total of 25 early-stage investment and financing transactions occurred in China’s healthcare sector in April, with the total funding amount exceeding RMB 1.5 billion.

It is evident that, despite the impact of the pandemic, venture capitalists (VCs) have not become complacent; instead, competition in early-stage healthcare investments has intensified beyond previous levels. What lies behind this trend? And what insights can be drawn from the early-stage financing data in April?

Multiple Key Metrics Rise, Making the Intersection of Hard Tech and Critical Demand a “Strategic Battleground”

Although “Your Lie in April,” data always tells the truth, and the early-stage healthcare sector’s boom is well-founded.

First, in terms of volume, there were 25 early-stage investment and financing transactions in April, representing a year-on-year increase of 39%. Second, in terms of amount, the total early-stage financing exceeded RMB 1.5 billion in April, a year-on-year increase of 15.4%. Finally, regarding the number of investment institutions, 71 firms, including Sequoia, participated in early-stage investments in April, an increase of 21 from the previous month.

Further analysis of these data reveals two key insights:

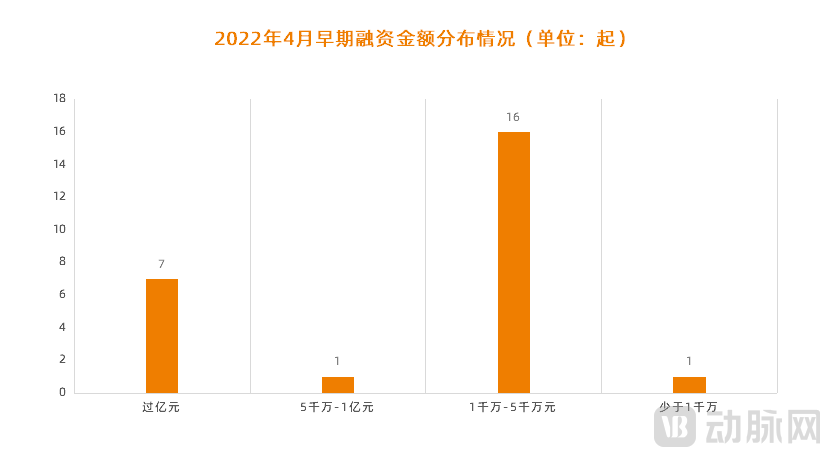

First, in terms of amount, the “unit price” for early-stage financing has risen significantly, with deals exceeding RMB 100 million accounting for nearly 30%.

Data sourced from VBInsight.

According to statistics from Artery Orange, among the 25 companies that completed early-stage financing in April, seven raised over RMB 100 million each, accounting for 28% of the total. Among them, Lingfu Bio, a research service provider for laboratory animals, emerged as the “most fund-attractive” startup, securing over RMB 200 million in its Pre-A round.

There is a reason why early-stage financing is “expensive.”

On the one hand, from the perspective of the early-stage investment market. Currently, an increasing number of investment institutions are beginning to focus their attention on the early-stage healthcare sector,

“The number of ‘investors’ has increased significantly compared to the past, but the number of ‘investees,’ i.e., startups, has not grown proportionally.”

Consequently, “scrambling for scientists’ projects at the gates of research institutions and universities” has become the norm for current investors. In such a market environment characterized by “demand outstripping supply,” the “unit price” of early-stage investments is inevitably set to rise.

From another perspective, that of startup development: Since most startups at this stage are rooted in “hard tech,” and market competition is becoming increasingly fierce, the initial capital investment required for startups is quite substantial.

These funds are primarily allocated across two dimensions: first, R&D, specifically to accelerate the advancement of its own product pipeline; and second, team building, namely recruiting core personnel suited to the company’s development needs.

Second, in terms of specialized sectors, biopharmaceuticals remain the “protagonist,” with oncology and cardiovascular diseases emerging as “early hotspots.”

A seasoned early-stage investor once told VCBeat’s Orange Bureau in an interview that when investing in early-stage ventures, the top priority is selecting the right sector, as this represents a company’s “longest plank.” Only after that do investors evaluate its technology, and finally, the founder. Therefore, for startups, choosing a sector with substantial market size is particularly crucial.

According to VCBeat’s Orange Data, all 25 companies that secured early-stage financing in April were “hard-tech” enterprises, exclusively from the two subsectors of biopharmaceuticals and medical devices. Among them, 18 were biopharmaceutical companies (72%), and 7 were medical device companies (28%).

Further analysis reveals that over 35% of these 25 companies are focused on niche areas with significant unmet clinical needs, such as oncology and cardiovascular diseases.

Let’s start with oncology. Tiangang Immunotherapeutics, which completed a Pre-A financing round worth hundreds of millions of RMB in April, is a high-tech company focused on the development of source-innovative immunotherapeutic drugs. The company has filed 11 invention patents, and multiple product candidates have completed early-stage research and development, poised to enter a rapid growth phase leading to regulatory approval and commercial launch.

Turning to cardiovascular health, Xinrui Medical, which completed an angel financing round of over RMB 10 million in April, is a company engaged in the research and development of polymer heart valves. Centered on novel polymer heart valves, the company has built a comprehensive solution for valvular heart disease.

It is evident that the intersection of hard technology and substantial demand has not only become a focal point for a new generation of scientist-entrepreneurs, but also a key investment target for early-stage investors.

Sequoia “Takes the Lead”: Four Early-Stage Funding Rounds Completed in April—Where Did the Money Go?

“Investing early” has long become a consensus among investment firms.

According to statistics from Artery Orange, a total of 71 investment institutions participated in the 25 early-stage financing deals that took place in April. Among them, Sequoia Capital completed four early-stage financings, Qiming Venture Partners completed two, and the remaining 69 institutions each completed one.

Data sourced from VBInsight

In fact, Sequoia Capital’s strong performance was not limited to April; throughout 2022, it demonstrated keen insight and robust execution in early-stage healthcare investments. Statistics show that as of April 30, Sequoia had completed nine early-stage financing deals in 2022, making it the most active investor among all venture capital firms.

So, what early-stage investment logic of Sequoia can be discerned from this?

First, look to scientists as role models. According to statistics, among the nine companies that completed early-stage financing with Sequoia this year, all founders have scientific backgrounds and graduated from top-tier domestic or international research universities.

This also aligns with the fundamental principles of entrepreneurship in the current healthcare sector. On one hand, an increasing number of scientists are transitioning from laboratories to the entrepreneurial arena; on the other hand, the healthcare industry is gradually extending into high-tech domains, thereby imposing higher requirements on founders.

Second, aligning with hard technology. According to statistics, all nine companies that completed early-stage financing with Sequoia this year are from the biopharmaceutical and medical device sectors, including seven biopharmaceutical companies and two medical device companies. Notably, these startups are all targeting frontier technological fields.

Taking Baifuan Biology as an example, it is a startup focused on synthetic biology, possessing a comprehensive synthetic biology technology platform, an advanced enzyme engineering platform, and enzyme-based green process development technologies. In addition, there is HemaCell, China’s first platelet regeneration company, which holds unique technologies for stem cell reprogramming, editing, and differentiation.

Third, align with core clinical needs. According to statistics, more than 90% of the nine companies that secured early-stage financing from Sequoia this year are focused on niche areas with significant unmet clinical needs.

Taking Xinhua Biologics as an example, it primarily focuses on niche areas with significant unmet medical needs, such as the application of AI in cancer immunotherapy. In addition, Haowei Microbiology specializes in “TACE interventional therapy,” which has demonstrated promising application prospects in the treatment of hypervascular malignant tumors—including lung cancer, renal cell carcinoma, and breast cancer—as well as in conditions such as uterine fibroids, benign prostatic hyperplasia, and arthritis.

In fact, for investment institutions, “investing early” is no easy task, as to some extent, “early-stage investment” is tantamount to co-founding a startup alongside the founders.

Therefore, like founders, investors face highly specific and thorny pain points in the early stages. The first challenge is how to accurately access early-stage resources; the second is how to comprehensively screen early-stage projects; the third is how to engage in “effective communication” with early-stage entrepreneurs; and the last is how to provide post-investment services to startups. Each of these steps is critically important.

As one of China’s top investment firms, Sequoia began making strategic moves in early-stage investing as early as 2018. In that year, it pioneered the establishment of Sequoia China Seed Fund, and over the past three years, it has connected with more than 13,000 entrepreneurs, invested in over 170 early-stage companies, many of which have progressed to the growth stage, with several becoming unicorns valued at over $1 billion.

This is only the beginning; in the future, Sequoia’s exploration and practice in the early-stage sector will unlock even greater possibilities.

Overseas Early-Stage Funding Exceeds $120,000 in April, with Diversification Trends Across Sectors

Enthusiasm for the early-stage medical sector is high in China, and even more so overseas.

Data sourced from VBInsight Industry Think Tank

Data sourced from VBInsight Industry Think Tank

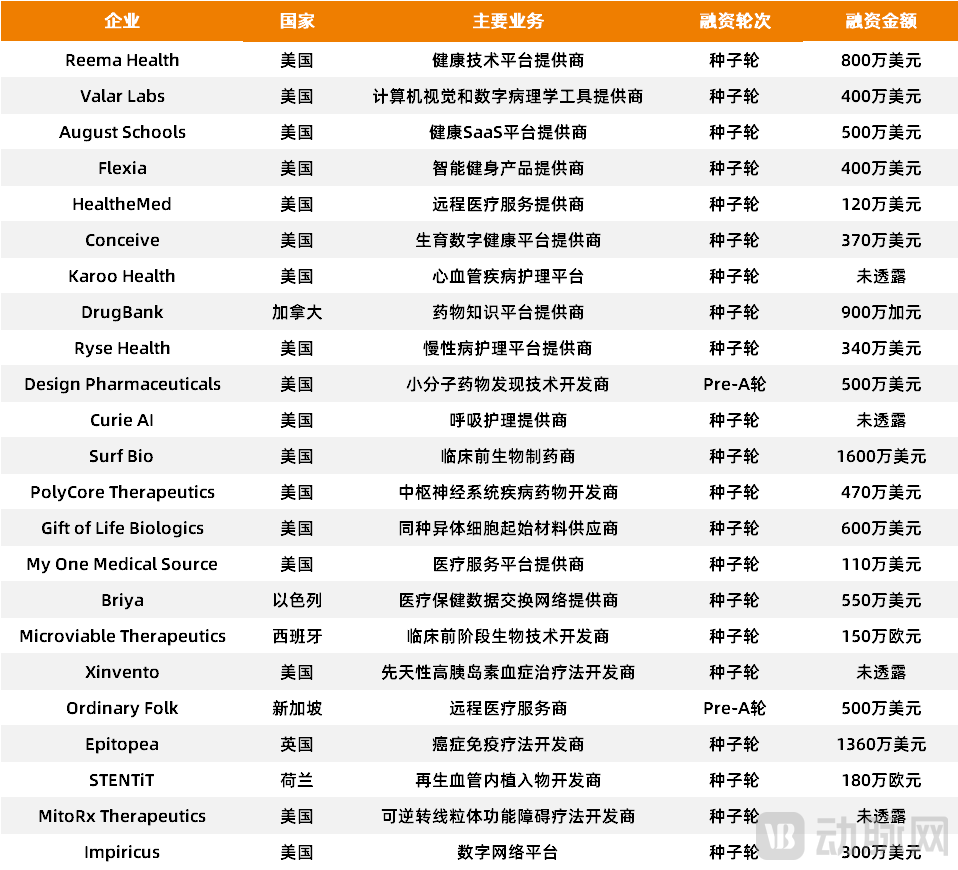

According to incomplete statistics from VCBeat, a total of 23 early-stage financing and investment deals occurred in the overseas healthcare sector in April, with total funding exceeding $1.2 billion.

Unlike China’s early-stage investment market, which focuses exclusively on biopharmaceuticals and medical devices, overseas early-stage financing is more diversified, with digital health as the primary focus, accounting for 56.5%.

Taking Ordinary Folk as an example, it is a telemedicine service provider. Currently, Ordinary Folk primarily operates two major platforms: the Noah platform, which is dedicated to providing men with diagnostic and treatment services for sexual health, mental health, hair care, and weight management; and the Zoey platform, which focuses on helping women address issues related to sexual health, mental health, and fertility. It is reported that the existence of the Noah and Zoey platforms effectively alleviates a series of pain points associated with offline medical visits, such as difficulties in making appointments and long waiting queues. Furthermore, these platforms enable individuals to more conveniently seek online consultations for sensitive conditions or complex diseases that are often difficult to discuss openly.

Additionally, there is Ryse Health, a startup that provides care services for patients with diabetes. It is reported that Ryse Health’s platform includes a continuous glucose monitor (CGM) and a customized application, primarily used for synthesizing data, supporting self-management, and facilitating communication between users and their care teams.

In addition, there are several new startups in the digital health sector, including Conceive, a provider of fertility digital health platforms; Flexia, a provider of smart fitness products; and DrugBank, a provider of drug knowledge platforms.

It is evident from this that both entrepreneurs and investors overseas are continuously striving toward better healthcare services. This trend is fundamentally linked to the structure of overseas healthcare systems and market demands.