Bausch+Lomb Completes Largest U.S. Healthcare IPO of the Year, Focusing on Ophthalmic Innovation

Bausch+Lomb

Eye Health Product Provider

On the evening of May 6, 2022 (Beijing Time), eye health company Bausch+Lomb successfully completed a dual listing on the New York Stock Exchange and the Toronto Stock Exchange under the unified ticker symbol BLCO, marking the largest healthcare IPO in the U.S. stock market this year. Amid recent turbulence in the U.S. stock market, many companies considering public offerings have been waiting for an opportune moment. As such, Bausch+Lomb’s listing has been closely watched as a bellwether for the IPO market. However, the company’s final offering price was set at $18 per share, raising $630 million, which fell short of market expectations. On May 6, Bausch+Lomb opened at $18.50 on the NYSE, up 2.78%, implying a total market capitalization of $6.3 billion.

Founded in 1853, Bausch+Lomb is widely recognized by the general public for selling contact lenses, lens care products, and other eye care items. However, positioning itself as a medical company, the group also offers hospital-based products such as ophthalmic pharmaceuticals and surgical medical devices, ranking second globally in scale, just after Alcon.

In terms of operations, Bausch+Lomb’s annual revenue has long remained in the $3–4 billion range, with profits hovering around $1 billion. The company’s overall fundamentals are sound; while it lacks sustained upward growth, it is self-sustaining. With a strong foothold in the ophthalmology sector, which holds considerable consumer potential, even slow development generates substantial revenue.

So, why is such a stable industry leader pursuing an IPO?

From a small optical shop to today’s multinational giant, Bausch+Lomb’s growth trajectory has always kept pace with the advancement of optics.

Bausch + Lomb was founded in 1853 and is one of the longest-operating companies in the United States. Its earliest product was the monocle. By 1903, Bausch + Lomb had already established product lines including eyeglasses, microscopes, photographic lenses, and telescopes, and even held patents for camera shutters. The first satellite image of the Moon was captured using a camera lens manufactured by Bausch + Lomb. Additionally, prior to World War II, Bausch + Lomb designed a pair of sunglasses specifically for U.S. pilots, which were widely adopted by the U.S. military; this brand was Ray-Ban. After the war, the iconic image of American pilots wearing Ray-Ban sunglasses left a deep impression on people around the world, propelling the brand to fame and into the fashion industry. However, Bausch + Lomb sold Ray-Ban in 1999, but that is a story for another time.

Domestic consumers are most familiar with Bausch+Lomb for its contact lenses. In 1965, Bausch+Lomb acquired the patent for hydrogel contact lenses invented by two Czech scientists. In 1971, the company received FDA approval and launched a new type of contact lens made from Poly-HEMA material, which is the globally renowned “Soflens” contact lens brand that remains popular to this day.

In the 1990s, Bausch+Lomb successively acquired precision manufacturing companies such as Storz Ophthalmic and Chiron Vision, structuring its business into four divisions: consumer health, contact lenses, pharmaceuticals, and surgery. Although there have been minor adjustments since then, its overall R&D efforts have consistently revolved around these four core areas.

Bausch+Lomb was taken private in 2007 after being acquired by the private equity firm Warburg Pincus. However, the company’s operational performance has not shown significant improvement since then, and it has also faced a series of product quality issues.

In 2013, Valeant, Canada’s largest pharmaceutical company (renamed Bausch Health in 2018), acquired Bausch & Lomb for $8.7 billion, marking the year’s largest acquisition. Under the agreement, approximately $4.5 billion was paid to an investor group led by Warburg Pincus, while the remaining $4.2 billion was used to repay Bausch & Lomb’s debt. Following the transaction, Bausch Health became one of the world’s largest contact lens manufacturers. Bausch & Lomb retained its original name and operated as a subsidiary of Bausch Health, serving as its most significant and stable source of cash flow.

However, Valeant’s peak did not last long. In late 2015, Valeant became embroiled in controversy over its pricing strategies and its use of specialty pharmacies to distribute drugs, prompting an investigation by the U.S. Congress that ultimately led to the ouster of CEO J. Michael Pearson. This high-profile scandal dethroned Valeant, leaving it with numerous accounting issues and massive debt. Amid pessimistic expectations, Wall Street investors sold off Valeant’s stock, causing its share price to plummet.

Bausch Health’s self-rescue efforts have continued to the present. In August 2020, Joseph Papa, CEO of Bausch Health, stated in a press release: “We have divested approximately $4 billion in non-core assets, repaid more than $8 billion in debt, and resolved many legacy legal issues. We believe now is the right time to begin the spin-off process.” Bausch+Lomb was one of the core assets he referenced. Immediately upon completion of the spin-off, Bausch+Lomb filed for an initial public offering on the New York Stock Exchange.

Over the past decade, Bausch+Lomb has maintained stable operations, whether through acquisitions, spin-offs, or its current independent listing. While the official reasons for the spin-off and listing have not been disclosed, VCBeat speculates that by separating from Bausch Health, which is burdened with debt, Bausch+Lomb may gain greater financial resources and operational autonomy, thereby enabling more diversified development strategies. For Bausch Health, divesting high-quality assets makes it easier to manage its remaining assets, accelerating its transition from a generic drug manufacturer to an innovative pharmaceutical company.

Bausch+Lomb’s prospectus provided a brief overview of the company using a series of figures: the company employs approximately 12,000 people, operates in around 90 countries and regions, serves a potential customer base of over 1 billion individuals, boasts brand awareness exceeding 70%, and offers more than 400 product varieties.

Bausch+Lomb typically categorizes its products into three major segments: Vision Care, Ophthalmic Pharmaceuticals, and Surgical. Vision Care is a pure B2C business, surgical medical devices are generally sold to healthcare institutions, and ophthalmic pharmaceuticals are divided into over-the-counter (OTC) and prescription drugs, each with distinct distribution channels.

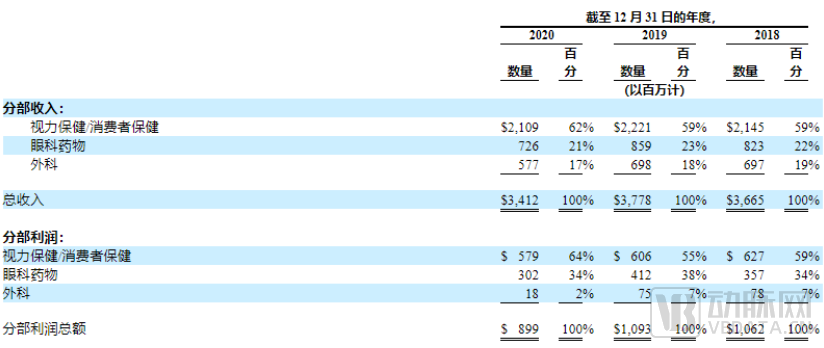

Financial Data Disclosed in Bausch+Lomb's Prospectus

Financial Data Disclosed in Bausch+Lomb's Prospectus

Vision care is Bausch+Lomb’s primary source of revenue and profit. Operational data for 2020 shows that the company’s vision care business generated $2.11 billion in annual revenue, accounting for 62% of total revenue, and $580 million in profit, representing 64% of total profit.

Among these, contact lenses and their care products, OTC eye drops, and ocular vitamins are Bausch+Lomb’s primary profit drivers. Particularly notable is its contact lens business, which combines therapeutic and medical-aesthetic attributes. Bausch+Lomb boasts the industry’s most extensive product portfolio, including daily disposable soft contact lenses; multifocal, toric, and multifocal toric soft contact lenses; and colored contact lenses. It holds the number-one sales position in key markets such as China, as well as in several emerging markets, including Thailand and India.

Following closely is Bausch+Lomb’s pharmaceutical business, which accounts for 21% of total revenue and is dedicated to postoperative care and the treatment of various ocular conditions, such as glaucoma, ocular inflammation, ocular hypertension, dry eye disease, and retinal diseases. Its four major ophthalmic pharmaceutical brands are VYZULTA, Lotemax, Prolensa, and BEPREVE.

Notably, Bausch+Lomb’s innovative drug R&D pipeline is closely centered around its ophthalmic business. Latanoprostene bunod, which has already been launched, is a prostaglandin analog used to lower intraocular pressure in patients with open-angle glaucoma or ocular hypertension. Besifloxacin hydrochloride, a widely recognized N-1 cyclopropyl 8-chloro fluoroquinolone antibacterial agent, inhibits Gram-positive and Gram-negative bacteria by suppressing bacterial DNA gyrase and topoisomerase IV. Loteprednol etabonate is an ophthalmic corticosteroid indicated for the treatment of steroid-responsive inflammatory conditions of the eyelids, bulbar conjunctiva, cornea, and anterior segment of the globe, such as allergic conjunctivitis, rosacea keratitis, and selected infectious conjunctivitis.

Currently, Bausch+Lomb has five products in Phase IV clinical trials, two in Phase III, and three in Phase II globally, covering indications such as red eye and astigmatism. Its R&D focus will remain primarily on over-the-counter (OTC) drugs in the near future.

Surgery is currently the business segment of Bausch+Lomb that contributes the least to revenue, generates the lowest profits, and carries relatively higher risks. Its standard product portfolio includes ophthalmic surgical instruments and equipment, phacoemulsification devices, and intraocular lenses; the VICTUS femtosecond laser, commonly used in cataract surgery, falls within this business segment.

Despite its extensive product lines, Bausch+Lomb’s competitiveness is not protected by high barriers.

In 2020, amid the sweeping COVID-19 pandemic, Bausch+Lomb’s operating revenue declined by 17.75%, and its profits fell by 9.69%. Behind this performance were two key factors: on one hand, the closure of brick-and-mortar stores and reduced consumer spending due to stay-at-home measures prompted by the pandemic; on the other hand, Bausch+Lomb failed to launch any blockbuster products during this period.

Reviewing the prospectus data, Bausch+Lomb’s R&D expenses from 2018 to 2020 were $221 million, $258 million, and $253 million, respectively, accounting for 6.0%, 6.8%, and 7.4% of total revenue. Product-related R&D spending was even lower, at $196 million, $234 million, and $236 million, representing 5.3%, 6.2%, and 6.8% of total revenue, respectively. For a medical giant with a market capitalization of $6.3 billion, such levels of R&D investment are insufficient to sustain its competitive edge.

Further Analysis of Core Products in Bausch+Lomb’s Product Portfolio.

In recent years, colored contact lenses have demonstrated strong consumer appeal due to their aesthetic enhancement properties, boasting exceptionally high repurchase rates and becoming a favored target for capital investment. As of February 2022, China alone was home to more than 1,800 companies operating in the colored contact lens sector.

The influx of a vast number of companies has inevitably diluted Bausch+Lomb’s contact lens business, yet challenges also bring opportunities. This is particularly true for colored contact lenses, a niche segment heavily reliant on marketing. The rise of domestic e-commerce and live-streaming commerce has not only paved the way for smaller brands to survive but also created space for leading enterprises to reach a broader user base more rapidly.

During the prospectus blackout period from 2021 to 2022, Bausch+Lomb leveraged its official flagship store on Tmall to conduct multiple live-streaming sessions, accelerating user reach through channel innovation. Meanwhile, it launched co-branded colored contact lenses with top-tier IPs such as Chinese National Geography, positioning the century-old brand within the fashion circle of Generation Z.

Furthermore, Bausch+Lomb serves as the exclusive distributor in China for Thermage, a device developed by its sister company, Solta Medical. According to data from the “2021 White Paper on the Aesthetic Medical Device Industry” released by Yidu Data, the fifth-generation Thermage alone generated $142 million (RMB 923 million) in revenue across East and Southeast Asia, a success to which Bausch+Lomb’s strategic contributions in the Chinese market significantly contributed.

Thus, it appears thatBausch+Lomb’s performance in the consumer market no longer resembles that of a medical device company; instead, it has transformed into a medical aesthetics company.Shifting strategic tracks could significantly benefit its development. With the medical aesthetics industry currently at its peak growth, driven by a compound annual growth rate (CAGR) of 20%-30%, Bausch+Lomb is poised to leverage this momentum to break through the $4 billion revenue barrier.

Revisiting the Segment on Intraocular Lenses. Bausch+Lomb, together with Alcon, Johnson & Johnson, and Zeiss, controls 80% of China’s intraocular lens (IOL) market. However, the IOLs under Bausch+Lomb that have obtained NMPA certification include eight categories: Intraocular Lens, Akreos AO Micro Incision Lens, SofPort Intraocular Lens, SofPort Intraocular Lens, One-Piece Hydrophobic Intraocular Lens, Intraocular Lens, Acrylic Intraocular Lenses, One-Piece Hydrophobic Intraocular Lens, and Preloaded Acrylic Intraocular Lenses with Injector. All of these products hold only “National Medical Device Import Registration” certificates, indicating that none are manufactured domestically in China. Amid the surging trend of domestic substitution in the Chinese market, all of Bausch+Lomb’s IOL products face potential policy-related risks.

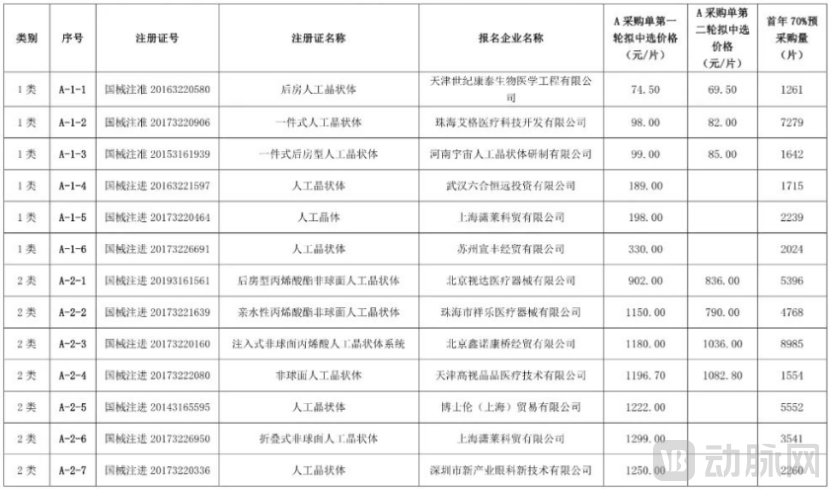

Furthermore, the introduction of volume-based procurement has further squeezed the profit margins of Bausch+Lomb’s intraocular lens-related business. In March 2021, Bausch+Lomb won bids in the volume-based procurement organized by the Guangdong Pharmaceutical Exchange Center, reducing the unit price of intraocular lenses, which previously ranged from RMB 3,000 to RMB 10,000, to approximately RMB 1,000, representing a maximum price reduction of 90%. As China is a “key market” for Bausch+Lomb, the expansion of centralized procurement from Guangzhou to a nationwide scale will pose a significant test to the company’s profitability, a challenge that has not yet been reflected in Bausch+Lomb’s prospectus.

Public Notice of the Proposed Winning Bidders for the Alliance Region’s Volume-Based Procurement of Intraocular Lens Medical Consumables in 2021 (Procurement Package A)

Public Notice of the Proposed Winning Bidders for the Alliance Region’s Volume-Based Procurement of Intraocular Lens Medical Consumables in 2021 (Procurement Package A)

Overall, constrained by policy, market dynamics, and other multifaceted factors, Bausch+Lomb’s core competitiveness is increasingly shifting toward the consumer segment, with a rising proportion of related business activities. While there is currently no data to substantiate the merits or drawbacks of this strategic shift in focus, fundamentals in the medical aesthetics market suggest a promising outlook for Bausch+Lomb.

Since the prospectus does not disclose the actual use of the funds raised, we cannot determine whether Bausch+Lomb’s newly raised capital was used by its parent company, Bausch & Lomb Incorporated, to repay debt or retained for its own use to address the numerous issues under the current structure.

Compared with Alcon, the industry leader with a comprehensive ophthalmic product portfolio, Bausch+Lomb’s product system, although diverse, still has significant gaps and does not cover highly promising medical devices such as OCT. To break through its current limitations, Bausch+Lomb needs capital and greater autonomy to better align its strategies with market demands and strengthen its core competitiveness.

If post-listing developments follow the latter scenario, the spun-off Bausch+Lomb will be able to break free from past constraints and focus more intently on addressing business challenges. Judging by its stock price, the market is highly confident in Bausch+Lomb’s future.

Whether it can break through the limitations and move to the next stage remains to be proven by time.