Synthetic Biology Professor Couple Earns $120M Net Profit in a Year Selling Medical-Grade Face Masks

Giant Biogene

Skin Care Product R&D Developer

The Boundless Possibilities of Medical Dressings, Redefined by Giant Biogene’sIPOThe relighting of the registration application sparked a wave of market excitement.

Having weathered a turbulent cycle of breakout popularity, viral fame, product shortages, public skepticism, regulatory crackdowns, and cooling demand, medical dressings continue to demonstrate robust vitality. In early May, Giant Biogene, holding two blockbuster medical-grade skincare brands, “Comfy” and “Collgene,” filed its prospectus with the Hong Kong Stock Exchange, embarking on a new journey into the capital markets. As a company pioneering the novel concept of producing collagen products through recombinant synthetic biology methods, it is the third medical dressing manufacturer to pursue an initial public offering (IPO).

Previously, Chuanger Biology and FuErJia Technology, each leveraging their top-five-selling medical dressing brands—Chuangfukang, Chuangermei, and FuErJia—launched IPO bids on the STAR Market of the Shanghai Stock Exchange in June 2020 and the ChiNext Board of the Shenzhen Stock Exchange in September 2021, respectively. After a series of setbacks, these two leaders in the medical dressing sector shifted their listings to the Beijing Stock Exchange several months ago, updated their financial data, and restarted their IPO processes. Now, with the entry of Giant Biogene, it appears all but certain that one company will finally go public in China’s booming domestic medical dressing industry.

Amid the chaos wrought by new entrants, the skepticism of onlookers, and the solitary courage of those who hold their ground, the industry continues to strive—within an increasingly clear regulatory framework and a more rational understanding of demand—to provide tools that may effectively serve people’s desire for beauty.

Medical dressings first appeared on the social media platform Xiaohongshu (Little Red Book) under the name “medical aesthetic masks,” instantly capturing the attention of young women. At that time, propelled by a single review article that garnered over 10,000 likes and nearly 1,000 comments, medical dressings rapidly gained popularity on Xiaohongshu, with their buzz quickly spreading to WeChat Moments and highly active short-video platforms such as Douyin and Kuaishou. According to previous statistics, there were more than 20,000 posts related to “medical aesthetic masks” on Xiaohongshu alone, with nearly 100 products available for sale. Hailed as “the true love of budget-conscious girls” and “the nemesis of long-standing acne,” these products dominated Xiaohongshu’s trending topics for an extended period.

When medical dressings first surged in popularity, products from mainstream brands were frequently sold out. On WeChat Moments, micro-merchants were “pressured” by customers to secure supplies of medical dressings. “This is indeed a rare, phenomenon-level product,” one micro-merchant remarked. Customers’ enthusiasm was evident in their bulk purchases—buying by the box—and a high repurchase rate exceeding 80%, demonstrating their devotion to the product and overshadowing the Japanese and South Korean beauty brands that had initially educated Chinese consumers about facial masks.

Subsequently, the most popular live-streaming influencers and traffic-driving celebrities began promoting medical dressings, pushing their popularity to its peak with high praise such as “comparable to major brands.” The presence of Qianxun Holding, under a former top-tier internet celebrity, in the shareholder list of Giant Biogene stands as a testament to that era when medical dressings were embraced by the general public. At that time, first-tier brands such as Chuangermei, Fu’erjia, and Kefumei became scarce commodities, with their circulating prices soaring accordingly. According to the recollection of a micro-business agent, the procurement price for the Fu’erjia brand she represented rose from approximately RMB 900 per box to over RMB 1,600 per box, while transaction volumes still doubled.

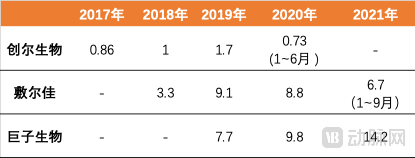

Based on the revenue data disclosed in subsequent prospectus filings, leading medical dressing companies entered a golden period of performance growth starting in 2017. From 2018 to 2019, the revenue generated by FuErJia’s series of medical dressing products increased from RMB 330 million to RMB 910 million, more than doubling. Meanwhile, Trauer Bio maintained consecutive annual growth in sales of its medical dressing product series from 2017 to 2019. Giant Biogene’s publicly disclosed revenue data begins in 2019; during this period, the sales revenue contributed solely by its two products, Comfy and Collgene, grew from RMB 770 million to RMB 1.42 billion, representing a compound annual growth rate (CAGR) of 35.7%.

Revenue Data of Leading Medical Dressing Companies (2017–2021) (Source: Prospectuses)

The immense wealth-creating potential of blockbuster products has emboldened leading brands to scale up and strengthen their market positions. As early as June 2020, Trauer Biotech filed an application with the Shanghai Stock Exchange (SSE) for a listing on the STAR Market, and its IPO was approved by the end of that year. The product-side hype duly translated into capital market enthusiasm. In April 2021, shares of Harbin Sanlian Pharmaceutical, which manufactured products under contract for Fu’erjia, rose for more than ten consecutive trading days, accumulating a gain of over 260%. In September of the same year, Fu’erjia submitted its prospectus to the Shenzhen Stock Exchange (SZSE) for a listing on the ChiNext Board, and the filing was accepted. From phenomenon-level hit products to a cluster of publicly listed companies, the fervor surrounding medical dressings has surged wave after wave.

However, like all emerging sectors that initially raced forward blindly, the medical dressing industry, despite its rapid advancement, is fraught with hidden concerns.

First, there is false advertising. In a previous report, VCBeat noted that an examination of nearly 100 products revealed that the majority of facial masks claiming to be “medical-device registered” were filed as Class I medical devices, while those filed as Class II or Class III clinical medical devices were exceedingly rare. The remainder were primarily cosmetics registered under the “cosmetic” designation, with many engaging in deceptive practices by misrepresenting their true nature. Second, there is exaggerated promotion. Medical dressings that have obtained “medical-device registration” often aggressively market benefits such as hydration, moisturization, skin whitening, and acne treatment. This constitutes an overstatement of the product’s performance, exceeding the capabilities recognized during the qualification process.

Consequently, regulators launched a stringent crackdown, causing the medical dressing market to cool down abruptly. In June 2021, eight ministries and commissions, including the National Health Commission, the Cyberspace Administration of China, and the Ministry of Public Security, issued the “Special Rectification Work Plan for Cracking Down on Illegal Medical Aesthetic Services.” In November, the State Administration for Market Regulation released the “Law Enforcement Guidelines for Medical Aesthetic Advertising.” Subsequently, the Ministry of Public Security published an article on its official website stating that it would further intensify efforts to combat illegal and criminal activities in the medical aesthetics sector, such as the manufacturing and sale of counterfeit products, unlicensed practice, dissemination of false advertising, and fraud involving “medical aesthetic loans.” On December 31, the National Medical Products Administration issued an announcement on the Catalogue of Class I Medical Devices, removing products such as “medical cold compress patches” and “cold compress gels” from the Class I medical device list, thereby forcing more than 2,000 related registered products to be taken off the market.

Under a collapsing nest, the IPO journeys of Chuanger Biotechnology and FuErJia Technology appeared markedly ill-timed. During the registration filing stage, Chuanger Biotechnology encountered repeated setbacks; its listing review was suspended twice—once in late March 2021 and again in September—due to expired financial documents, ultimately leading it to pivot to the Beijing Stock Exchange in early 2022. Meanwhile, FuErJia Technology’s prospectus also lapsed without any new progress. At that time, investors deemed medical dressings, alongside the various beauty concepts that had gained traction in recent years, unworthy of investment.

Is the concept of medical dressings truly a pseudo-proposition? The answer is no.

In the capital markets, Voolga and Chuang'er Bio have made a comeback, while Giant Biogene is accelerating its push toward an IPO. At the end of 2021, Giant Biogene completed its first external financing in more than 20 years since its establishment. In addition to Hillhouse Capital (holding a 4% stake) and CPE Yuanfeng (holding a 4.33% stake), which made decisive significant investments, this financing round attracted a strong lineup of prominent institutions, including Legend Capital, Greenwoods Asset Management, CDH Investments, and CICC Capital. According to industry rumors, Giant Biogene’s brief appearance in the private equity market sparked fierce competition among investment firms, driving its valuation in that round to nearly RMB 20 billion amid scarce availability of shares.

In January 2022, shortly after voluntarily withdrawing its IPO application for the STAR Market the previous month, Chuanger Biotechnology announced the filing of tutoring records for its public offering and listing on the Beijing Stock Exchange, shifting its focus to a new capital market. In the same month, Fu'erjia updated its financial data, with its IPO status showing a resumption of review. Listed companies specializing in medical dressings are poised to emerge.

From a product market perspective, the pursuit of beauty among women in China represents an inexhaustible gold mine. In earlier years, people spared no expense to have overseas proxies purchase widely touted skincare rarities, or traveled abroad simply because they heard that treatments like sheep placenta injections and skin boosters could lock in youth. Therefore, when medical dressings with transparent costs and clear functions emerged, consumers found them hard to resist, particularly patients troubled by skin conditions such as acne and dermatitis. The previous surge in popularity of medical dressings has validated this trend. In recent years, there has been a sharp increase in the number of individuals requiring skin repair after undergoing minimally invasive aesthetic procedures such as laser therapy, microneedling, and chemical peels. Even without recommendations from friends, most people have used medical dressings in accordance with medical advice.

It can be said that the market demand for medical dressings is highly certain, and the investment logic is as solid as a rock. The real question lies in whether there are high-quality products available on the market.

The primary criterion for a high-quality product is regulatory compliance, which serves as a critical lifeline; indeed, most medical dressing manufacturers fail due to non-compliance. In China, registration for Class II medical devices takes 0.8 to 2 years, while Class III registration requires more than 2 years. During this period, applicants must submit clinical trial reports. After submitting the registration application, the technical review process involves convening expert advisory meetings, engaging external experts for review or conducting joint evaluations with drug approval authorities, and performing quality management system inspections. For Class III registration applications, clinical trials must first be approved by the National Medical Products Administration (NMPA). This approval entails a comprehensive analysis of institutional equipment, qualified personnel, the risk level of the medical device, and a benefit-risk assessment report of the clinical trial protocol.

For leading enterprises, meeting this first criterion is not difficult. After the previous round of industry consolidation, products with only Class I filings were eliminated from this market, which exceeds RMB 20 billion, leaving only a few participants holding Class II and Class III registered products to enter the final competitive stage. VCBeat’s research found that the main medical device-numbered products sold by Voolga, Trauer Bio, and Giant Biogene hold Class II or Class III registration credentials. For example, according to its prospectus, Voolga’s revenue is derived from the sales of medical device dressings and functional skincare products, with its product portfolio dominated by Class II medical devices (accounting for 55.54% of sales in 2020), supplemented by functional skincare products.

This means that qualified medical dressing manufacturers must possess strong R&D capabilities and be willing to invest heavily in research and development, which is why leading companies continue to place significant bets on R&D. Previously, one of the most criticized aspects of Fu'erjia was its insufficient R&D efforts; it had only two R&D personnel, whose salaries were lower than those of sales staff. During the reporting period, its R&D expenditures were RMB 307,800, RMB 603,900, RMB 1.4797 million, and RMB 132,000, respectively, accounting for an extremely low proportion of its revenue.

According to the 2021 semi-annual report, Trauer Biotech recorded revenue of RMB 110 million and a net profit of RMB 21.227 million, representing a year-on-year decline of 45.1%. Meanwhile, R&D expenses increased significantly. Trauer Biotech explained that the decline in net profit was highly correlated with the increase in R&D investment during the same period. Giant Biogene, which has just submitted its prospectus, regards rapid updates and iterations to enrich its product portfolio as its core competitiveness. According to the prospectus, Giant Biogene has an R&D team of 84 members, 43 of whom hold master’s degrees or higher, accounting for 51.2% of the R&D staff. Over years of accumulation, Giant Biogene has also built a proprietary synthetic biology technology platform for the design and development of recombinant collagen, rare ginsenosides, and other bioactive ingredients. The company holds 75 patents and patent applications.

In the final competitive arena, industry giants must compete not only on product certifications but also by exerting greater effort in maintaining high standards and strict requirements throughout production and sales processes. The logic of the medical dressing market is one of higher-dimensional competition overpowering lower-dimensional players; this superior strategic positioning must be reflected in all aspects related to the product. For medical dressings, success depends on certifications in the short term, product quality in the medium term, and service excellence in the long term.

In the production phase, medical dressings face higher technical requirements. First, there are personnel requirements: according to regulations, the person in charge of a medical dressing manufacturing enterprise must have at least an associate degree or higher. The requirements for managers are even stricter; in addition to educational qualifications, they must hold a junior-level or higher professional technical title and have more than three years of work experience in quality management, production, or technical management. Second, there are facility requirements: the production workshop must be non-sterile and produce non-implantable products, while the microbiology laboratory must meet Class 10,000 cleanliness standards and be equipped with two independent compressed air systems. These stringent requirements impose rigorous conditions on the production environment of manufacturing enterprises. Ordinary cosmetics manufacturers would clearly find it difficult to meet such conditions.

In the sales phase, medical dressings are subject to stricter regulatory constraints. According to regulations, manufacturers of medical dressings may only engage in advertising after obtaining approval numbers for medical device advertisements. Entities providing internet drug information services must employ at least two personnel with professional expertise in pharmaceuticals and medical devices, and they must pass review and approval by regulatory authorities before selling medical dressings online. How to operate consumer-grade aesthetic medicine bestsellers under the stringent requirements applicable to medical-grade products is a mandatory course that industry giants must pass.

Although all three companies are vying for a spot in the final round, leveraging bioactive substances to appeal to consumers’ desire for beauty, Giant Biogene deliberately or inadvertently downplayed the cosmetic value of collagen and sodium hyaluronate in its prospectus—labels closely associated with Chuanger Biology and FuErJia. Instead, Giant Biogene chose to brand itself with synthetic biology, arguably the hottest concept at present and the prevailing trend in the development of raw materials for this type of medical dressing. This strategic positioning undoubtedly enhances Giant Biogene’s competitive edge.

Synthetic biology processes and robust online marketing capabilities are driving Giant Biogene’s rapid growth.

Among Giant Biogene’s core products, collagen is the most critical bioactive ingredient. Since the 1980s, renowned beauty brands such as Sisley and Helena Rubinstein have begun incorporating collagen into cosmetics, launching pure collagen formulations and collagen-enriched skincare serums, facial masks, cleansers, and creams. These efforts have firmly established collagen’s well-known benefits for moisturizing, anti-aging, and skin brightening in consumers’ minds.

Currently, collagen is primarily obtained through two methods: extraction from animal or human tissues and production via genetic engineering, with the latter referring to the synthetic biology approach adopted by Giant Biogene. Although animal-derived collagen remains the mainstream option, it has significant drawbacks.

Xenogeneic and allogeneic collagen carry risks of viral contamination and immunogenicity. Furthermore, their high structural rigidity at the biological level makes them prone to molecular chain breakage during processing, thereby disrupting the triple-helix conformation essential for collagen’s biological function. Undoubtedly, the rigid characteristics of animal-derived collagen increase the complexity of manufacturing processes. In addition, the vast majority of animal-derived collagen is water-insoluble, making it difficult to completely remove solvents used during processing, which in turn leads to cytotoxicity upon use.

Giant Biogene employs synthetic biology technology using Escherichia coli as a chassis. By performing specific enzymatic cleavage and ligation on human collagen genes, the company introduces and expresses these genes to produce collagen, thereby circumventing, to a certain extent, the aforementioned drawbacks of animal-derived collagen. For synthetic biology approaches, enhancing and stabilizing the production capacity of chassis cells represents a key technical bottleneck and constitutes Giant Biogene’s process advantage. According to its prospectus, Giant Biogene has an annual recombinant collagen production capacity of 10,880 kilograms, making it one of the companies with the largest recombinant collagen production capacity globally. Furthermore, the purity of Giant Biogene’s recombinant collagen reaches as high as 99.9%, consistently meeting industry standards for medical-grade materials, and its capacity utilization rate has been rapidly increasing since 2021.

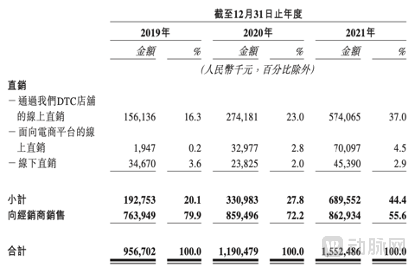

Beyond its innovative production processes, Giant Biogene has also intensified its efforts in online direct sales and distribution channels. In recent years, shifting channel-building focus from offline to online has become nearly an industry-wide consensus. For instance, FuErJia’s revenue share from online channels grew from 11.85% in 2018 to 29.08% in 2020. Meanwhile, ChuangEr Bio’s online-to-offline revenue ratio shifted dramatically from 61.01% online and 38.99% offline in 2017 to 41.21% online and 58.79% offline in 2019, directly reversing its previous emphasis.

The prospectus reveals that Giant Biogene has made substantial investments in building online marketing channels, which have driven significant revenue growth. In terms of expenditure, the company spent RMB 64.523 million, RMB 124 million, and RMB 306 million on online marketing from 2019 to 2021, primarily covering platform marketing fees, platform service fees, and costs associated with collaborations with new media key opinion leaders (KOLs). On the revenue front, Giant Biogene’s online income rose from RMB 192 million in 2019 to RMB 689 million in 2021, representing a 3.58-fold increase. Notably, online direct sales revenue through e-commerce platforms surged more than 30-fold, climbing from RMB 1.947 million to RMB 70.097 million.

Giant Biogene Revenue Data (Source: Prospectus)

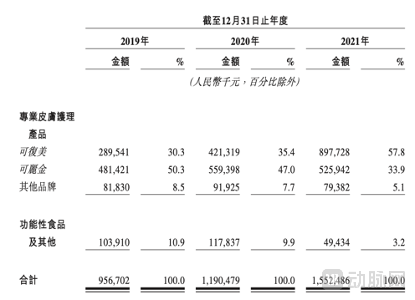

By integrating the sales data for Comfy (Ke Fu Mei) and Collgene (Ke Li Jin) provided by Giant Biogene, we can even infer that it was precisely the company’s sustained efforts in online channels that turned Comfy into a blockbuster medical dressing. According to Magic Mirror data, from 2019 to 2021, Comfy’s sales ranking across all categories rapidly jumped from 10th place to the top three. During this period, Comfy’s sales revenue increased by RMB 608 million. In the same timeframe, Giant Biogene’s online channel sales grew by RMB 486 million, while its offline channel sales increased by RMB 109 million. This suggests that the strong sales performance of Comfy was largely driven by its online channels.

Giant Biogene Revenue Data (Source: Prospectus)

More importantly, Giant Biogene’s online channels are predominantly direct-to-consumer, which, together with its proprietary manufacturing processes, constitute the infrastructure built through operational accumulation that supports future growth. In this sense, Giant Biogene has already secured the foothold needed to enter the capital markets.

So, can we conclude that medical dressings have entered a fast lane of development? Perhaps it is not that simple; the issue lies in the slowing sales growth. According to the prospectus of Trauer Bio, its revenue has already shown negative growth. Meanwhile, Giant Biogene, despite its rapid growth, faces the risk of declining return on investment. According to the prospectus, from 2020 to 2021, Giant Biogene’s online marketing expenditures increased from RMB 124 million to RMB 306 million, a rise of 146.7%, whereas during the same period, its online revenue grew from RMB 307 million to RMB 644 million, an increase of 109.7%. The growth in expenditure did not translate into commensurate revenue growth. Of course, this reflects only short-term changes in revenue.

We are more inclined to believe that the medical dressing sector, characterized by clearer regulations and more concentrated competition, possesses strong growth momentum and will give rise to multiple publicly listed companies.