How to Build a Nationally Leading Healthcare IT Enterprise: Strategies, Innovations, and Market Pathways

At the end of last year, Jiahe Meikang, after a 16-year marathon, finally secured its listing on the secondary market, injecting fresh blood into the long-dormant club of A-share medical informatics companies. It has been more than two years since Shanda Diwei, the previous medical IT enterprise to list on the STAR Market.

IPOs for Healthcare IT Companies Are a Well-Known Challenge. Whether traditional information system vendors or internet healthcare companies falling under the broader category of informatization, very few healthcare informatization enterprises have successfully completed IPOs on China’s A-share market despite its scale of tens of billions of yuan; to date, the total number stands at merely 15.In summary, some companies are unable to go public, some are indifferent to an IPO, and others have never even considered it.

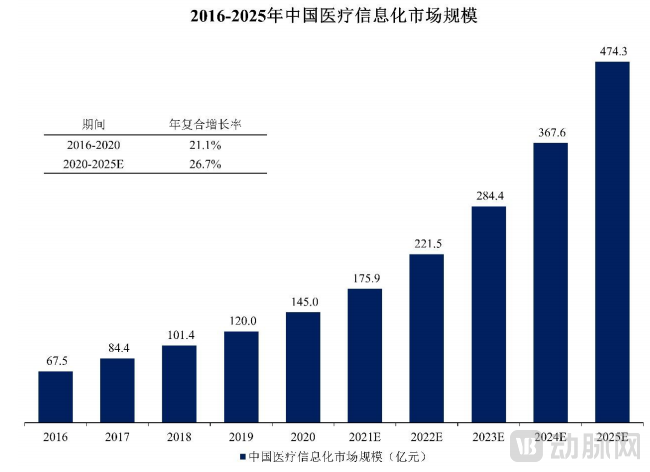

Market Size of China's Healthcare Informatics Industry (Data Source: Annual Reports of Jiahe Meikang, Frost & Sullivan)

However, the integration of technologies such as artificial intelligence and the Internet of Things has made it impossible for healthcare IT to advance in isolation. Following the injection of over RMB 10 billion in capital, the informatization industry—once distant from the secondary market—is gradually converging around shared objectives.

Yet, in the face of the entrenched market dominance held by pioneers, how should emerging medical IT companies strategically position their product portfolios to break through the encirclement and suppression, thereby becoming a force that reshapes the industry landscape?

An analysis of the demands for healthcare informatization reveals three key aspects. The first is the construction of medical IT infrastructure, primarily centered on Hospital Information Systems (HIS), Picture Archiving and Communication Systems (PACS), Clinical Information Systems (CIS), electronic medical records (EMR), and big data centers; this market segment features a stable competitive landscape. The second involves evaluation-driven development led by the National Health Commission, encompassing rating initiatives for EMR systems, interoperability standards, and smart hospitals; this area is characterized by substantial demand coupled with stringent requirements. The third pertains to department-specific implementations, such as intelligent waste management overseen by infection control offices and infusion solutions for hospital wards; these projects are typically decentralized, independent, and diverse, with a stronger emphasis on software.

Infrastructure and rating-related demands are dominating the overall development direction of healthcare IT today,Hospital projects centered on electronic medical records (EMR) and smart hospital accreditation, as well as public health initiatives focused on regional informatization, often command unit prices in the tens of millions, with some exceeding 100 million yuan.This market segment evaluates enterprises’ comprehensive business capabilities. The majority of the market is dominated by listed companies such as Neusoft Group, B-Soft, and Yilianzhong, as well as regional leaders like Chongqing Zhonglian and Nanjing Haitai.

The oligopolistic landscape has driven small and medium-sized healthcare IT enterprises to bypass the core markets dominated by industry leaders. However, the remaining market segments are either located in third- and fourth-tier cities or occupy a cost-center position within hospitals, receiving limited strategic attention. Furthermore, competition among smaller healthcare IT firms is often regionalized; for instance, it is challenging for a company from Province A to enter the hospital market in Province B, as it must both accurately assess local needs and establish distribution channels. Consequently, China’s healthcare IT industry remains highly fragmented, with small and medium-sized enterprises struggling to expand from regional players to national contenders.

The key to breaking the rules lies in establishing stable connections with hospitals across various regions.

Easier said than done. For small and medium-sized enterprises (SMEs), the establishment of cross-regional relationships relies on the combined effect of multiple factors, with limited effectiveness; however, the underlying logic can be simply summarized into two types:Technological Innovation, address hospitals' latent needs through innovative approaches;Product Innovation, closely following hospital construction policies and promptly launching products that help hospitals meet regulatory requirements. In practice, these two approaches often intersect and work in synergy.

Enterprises that focus on technological innovation are typically the new generation of medical IT companies. Backed by capital, their strategy is to address long-standing pain points in hospitals through technological breakthroughs,The emphasis is on the optimization and reconstruction of existing processes.Huimei Technology and Senyi Intelligence’s specialty-specific Clinical Decision Support Systems (CDSS) leverage intelligent processing capabilities to audit various scales, such as those for Venous Thromboembolism (VTE) risk and psychiatric assessment. Similarly, the auxiliary diagnostic solutions provided by Infervision and Deepwise Medical can also be regarded as part of the informatics domain, enhancing examination efficiency.

Theoretically, an innovative product that meets market needs can gradually gain acceptance over time; however, in practice,For companies to market their products across China, the key lies in leveraging promotional communication to bridge the information asymmetry between hospitals and enterprises, thereby enabling hospitals to recognize the value of the products.Just like Huoshu Technology, which printed its logo on Nongfu Spring bottles at the 2020 CHINC conference, such efficient marketing is eye-catching. Yet it also prompts a sigh: the marketing phase often takes longer and costs more than R&D.

Pursuing a second path for breakthrough requires less capital, relying primarily on R&D personnel’s understanding of specific scenarios and their ability to precisely navigate policy landscapes. On this path, enterprises are often driven by department-level transformations led by policy changes or demand-side shifts led by consumers (C-end). They provide specialized, targeted solutions addressing the specific needs of particular medical scenarios, thereby securing a dominant voice before the market scale in these niche segments matures.The emphasis is on seizing the market by pioneering product development during the response vacuum period triggered by policy-driven structural reforms in hospitals.

For instance, the vigorous promotion of Diagnosis-Related Groups (DRG) has rendered the existing staffing and hardware/software configurations in many medical records departments inadequate to meet the demands of the new policy. In response, numerous small and medium-sized healthcare IT companies have quickly stepped in to fill this gap, leveraging technologies such as artificial intelligence and big data to develop intelligent systems for medical record quality control and data reporting.

Moreover, in recent years, changes in policies and patient demands for various hospital departments have gradually translated into shifts in the relative status of these departments. Emerging specialties are raising requirements for the comprehensive capabilities of information systems, thereby giving rise to a fragmented yet vast specialized healthcare IT market.Seizing the vacuum period of departmental status transition, these medical IT sectors, rarely ventured into by capital, are leaping from regional-level enterprises to national-level enterprises.

Despite conceptual differences between the two approaches, in practice, both parties consistently focus their entry points on core policies such as the high-quality development of public hospitals and the performance evaluation of tertiary public hospitals. By addressing specific needs, they develop specialized informatics solutions. This article uses three scenarios—medical records departments, emergency centers, and day surgery centers—as examples to illustrate this approach.

The Medical Records Department at the Eye of the Storm

“The biggest change in the Medical Records Department is that we are being criticized by the hospital president with increasing frequency.”

Across hospitals in China, the status of medical records departments varies significantly. In some Grade A tertiary hospitals in Beijing, the Medical Records Department is a first-level department, holding equal standing with the Medical Affairs Office. However, in many other regions, it does not constitute an independent department and is instead designated as a “Medical Records Room.” It was only with the introduction of numerous hospital development policies that its status began to gradually change.

For instance, among the 55 indicators outlined in the “Operational Manual for Performance Assessment of National Tertiary Public Hospitals (2022 Edition),” seven are directly derived from the front page of medical records, requiring the Medical Records Department to curate surgery-related medical record data with high quality.

The reform of medical insurance payment methods based on Diagnosis-Related Groups (DRG) and Big Data Diagnosis-Intervention Packet (DIP) is a more critical factor reshaping the status of medical records departments. As DRG/DIP shifts hospitals’ revenue sources toward medical quality and control of resource consumption, medical records serve as the most direct vehicle for reflecting these aspects. Once considered of little value yet difficult to discard, medical records departments are now assuming new roles within hospitals driven by these policy changes.

Yisheng Intelligence is one of many startups focusing on AI-driven medical record quality control. Zhou Yutong, its CEO, told VCBeat: “The changing role of the medical records department stems from shifts in healthcare revenue structures. Whether for health insurance reimbursement, hospital accreditation, or performance evaluation, various policy inspections all hinge on medical records as a critical entry point, requiring hospitals’ status to be assessed through this lens.” This means that,Medical records were once merely a cost center for hospitals, but now hold the potential to recoup financial losses.

However, administrative changes always lag behind policy changes. “When hospital directors suddenly realize that medical records are impacting every aspect of their work, their first reaction is invariably to approach the head of the Medical Records Department and ask, ‘Why has your department failed to effectively manage the quality of medical records?’”

The Medical Records Department naturally faces its own challenges, with the most critical issue being a shortage of personnel. Medical records quality control specialists require dual knowledge reserves and mindsets in both clinical medicine and coding, along with extensive practical experience. According to Zhou Yutong, if one follows the traditional logic of medical talent development—first educating individuals, then having them obtain certification, and finally allowing them to work with credentials—this process would take at least 10 years. “At the current stage, not many hospitals in any given province are likely to have a sufficient number of certified medical records quality control specialists on staff.”

By targeting this niche, companies such as Huimei Technology, Yunzhisheng, and Yisheng Intelligent have begun to leverage AI and big data tools for medical record quality control. Meanwhile, firms like Huoshu Technology and Aideng Technology have directly entered the healthcare IT market through DRG-focused solutions. After all, whether from a cost or talent perspective, hospitals across China can only rely on technological support to raise the performance of their medical records departments from low levels to passing standards in the short term.

“2021 Healthcare Artificial Intelligence Industry Report” compiled all tender and bidding data related to healthcare AI in 2021, with quality control (QC) and clinical decision support system (CDSS) AI products accounting for the largest shares at 29% and 28%, respectively. The majority of these projects were associated with medical record quality control, sufficiently demonstrating hospitals’ recognition of this emerging technology.

Taking data provided by Yisheng Intelligent as an example, a large comprehensive tertiary Grade A hospital saw its monthly medical insurance surplus increase from RMB 39 million to RMB 125 million—an improvement of nearly RMB 80 million—after implementing the Yisheng Intelligent Medical Record Quality Control System under the DRG payment method.

"Obviously, starting from the urgent needs of the Medical Records Department, the ultimate goal is not merely to serve that department."Accurate medical record data will ultimately provide significant support for hospital management and operations. Therefore, companies specializing in medical record quality control are striving to expand their business offerings. At present, they already have a base of loyal hospital clients supporting them.

From Emergency Department to Emergency Center

For the general public, “emergency care” is a familiar term. However, within the hospital system, most emergency departments are defined merely as “pass-through” units: patients transit through them rather than staying for extended care. Consequently, emergency departments have long occupied a peripheral yet intermediary position—important, but undervalued.

There are two models for the establishment of emergency departments. One is the hospital-based emergency department, which coordinates resources and processes across various departments to stabilize patients’ vital signs in the shortest possible time, thereby gaining valuable time for subsequent specialized treatment. The other is the “hospital-within-a-hospital” model, which has its own internal medicine, surgery, and other common clinical departments, enabling it to cover the entire process of diagnosis and treatment for emergency patients.

"Judging by the trends in emergency department construction, more hospitals are willing to build it into a center rather than a mere passageway."

From an economic perspective, in the broader context of DRG implementation, the emergency department’s temporary exclusion from DRG payment systems enables hospitals to maintain profitability under traditional models. From the standpoint of patient needs, streamlining emergency care processes to facilitate earlier access to comprehensive treatment will more effectively save patients’ lives.

To date, the development of emergency centers has transcended mere disciplinary construction, evolving toward a systematic framework. This system encompasses pre-hospital care, coordination and treatment within the hospital’s emergency department, and post-discharge follow-up, all of which fall under the comprehensive responsibility of the emergency center.

The transition from a “department” to a “center” signifies the emergence of new healthcare IT requirements. In the era of smart healthcare, the operational scope of emergency centers will no longer be confined by geography; supported by 5G technology, emergency care commences the moment a patient boards an ambulance.

Therefore, the medical information system for the emergency department should not be confined within the department itself. In the pre-hospital emergency care phase, the system needs to connect every ambulance via the Internet, monitor the deployment status of each medical staff member, and acquire real-time patient data. This allows documentation and chief complaint records, which were previously completed only after arrival at the hospital, to be entered in advance; additionally, electrocardiogram (ECG) and blood pressure assessments are conducted beforehand, enabling patients to proceed directly to the ward for treatment without delay upon hospital admission.

Another challenge lies in the informatization system for emergency departments within hospitals. Under the “hospital-within-a-hospital” model, developers of emergency care information systems must thoroughly understand the operational workflows of each subspecialty department and the interaction mechanisms among different departments. It is essential to integrate the Hospital Information System (HIS), Picture Archiving and Communication System (PACS), and Clinical Information System (CIS) of the emergency center. This not only tests vendors’ capabilities in building individual medical IT systems, but also requires them to develop multimodal systems that support collaborative workflows across multiple departments, posing significant challenges for developers.

The development of independent emergency medical services (EMS) information systems in China began around 2016. To date, only a limited number of companies have entered this field. Notable players with strong performance include Changhong Smart Health, Jiuyi Information, and Meditech Technology. Most providers are capable of building only standalone pre-hospital emergency systems or isolated (partial) in-hospital emergency systems. Few enterprises have successfully integrated both components into a unified system that serves the entire emergency center.

Jiuyi Information is one of the few companies currently capable of developing a comprehensive emergency care system that covers pre-hospital, in-hospital, and post-discharge phases. Ran Kairui, its Chairman, once stated in an interview with VCBeat: “Emergency centers have moved from a peripheral role in the past to the central focus today. Their structure has become increasingly complex, making it difficult for most enterprises to build complete systems that meet hospital needs. In our view, pre-hospital and in-hospital stages do not constitute the entirety of emergency care informatization. We have also incorporated follow-up care into our system to help emergency departments establish a complete diagnosis-and-treatment closed loop, which will fundamentally transform the value system of emergency centers.”

From the perspective of bidding data,Currently, hospitals tend to procure emergency care information systems in a fragmented manner, with few opting for comprehensive solutions. Most purchases consist of standalone pre-hospital emergency care systems or independent remote emergency centers, with investments ranging from RMB 5 million to RMB 10 million.With the further development of emergency centers, both modular and integrated solutions will capture a larger market share.

Day surgery is a long-standing concept in China, first appearing at Wuhan Children's Hospital in 2001. However, it was not until 2015 that policies formally required tertiary hospitals to initiate pilot programs. In 2019, the proportion of day surgeries among elective procedures was incorporated into the performance evaluation system for public tertiary hospitals. By 2021, the initiative for high-quality development of public hospitals explicitly called for vigorous promotion of day surgery and an increase in its proportion. Research data indicate that after implementing day surgery, hospitals experienced a 37%–55% reduction in average pharmaceutical costs per case and a 20%–40% decrease in average hospitalization costs per admission. The introduction of Enhanced Recovery After Surgery (ERAS) protocols, advancements in medical technology, insufficient hospital bed resources, and growing patient demand for surgical procedures have all spurred the rapid development of day surgery in China. Compared with conventional approaches, day surgery has demonstrated reduced rates of complications and nosocomial infections, along with optimized treatment and nursing practices.

In 2014, 28 hospitals under the Shanghai Shenkang Hospital Development Center had already implemented day surgery programs, with an annual volume of 73,100 cases. Following implementation, the average length of stay decreased by 1.85–4.36 days, and the average cost per hospitalization dropped by 15%–60%. In 2018, Renji Hospital, affiliated with Shanghai Jiao Tong University School of Medicine, performed 35,411 day surgeries, accounting for 40.5% of the hospital’s total surgical volume during the same period, with level III and IV procedures comprising 50.2% of these cases. In the same year, West China Hospital of Sichuan University reported 24,960 day surgeries, representing 25.11% of its total surgical volume, with level III and IV procedures accounting for 60.1%. However, the adoption of day surgery in China remains limited. As of the end of 2018, only 1,340 hospitals offered day surgery services, and the volume of day surgeries accounted for less than 10% of the total surgical volume nationwide.

An Analysis of Day Surgery Implementation Models in Chinese Hospitals: Early adopters such as West China Hospital, Xiangya Hospital, Renji Hospital, and the Second Affiliated Hospital of Zhejiang University School of Medicine have established independent day surgery centers. However, most Grade 3A hospitals still conduct day surgeries within the respective clinical departments, with many institutions adopting a hybrid model combining both approaches.

Beijing Day Surgery Medical Technology Co., Ltd., a subsidiary of Huibin Technology, was among the first enterprises to develop management information systems for day surgery centers. In its “Proposal for the Development of Day Surgery Projects,” the company stated that the development of day surgery should be approached from a hospital-wide perspective, with a dedicated management structure established. It recommended forming a Hospital Day Surgery Development Leadership Group, led by the Hospital President and overseen by the Vice President in charge of clinical operations. The Medical Affairs Department (or Division) would manage medical quality, with participation from the Department of Anesthesiology, the Nursing Department, and various clinical specialties. This group would comprehensively assess the readiness of each specialty, initiate services with highly mature procedures, establish day wards or specialized day surgery centers, streamline management processes, and gradually expand day surgery services.

As a relatively new entity,The design of the Day Surgery Center Information System primarily addresses three key requirements: first, the fundamental storage and exchange of patient diagnosis and treatment information; second, the digitization of previously offline workflows to enable online access to outpatient reports, specialty assessments, and anesthesia evaluations, as well as online surgical scheduling, thereby ensuring that day surgeries can truly be completed within a single day; and third, post-discharge patient follow-up, which is both the most critical and the most lacking feature in day surgery centers, and remains an area rarely addressed by major listed healthcare IT companies.

“As patients’ hospital stays shorten, with reduced time for postoperative care and rehabilitation, many leave the hospital immediately after surgery and often feel at a loss. Consequently, postoperative follow-up, rehabilitation guidance, return visits, nutritional support, and psychological interventions have become increasingly important. Moreover, cancer patients requiring periodic chemotherapy are increasingly managed in day-care chemotherapy wards in many hospitals. Monitoring adverse reactions after patients return home following chemotherapy is also a key direction for the future development of day-care medical services.“Zhang Jian, Executive Vice President of Beijing Daycare Medical Technology, stated.

“Therefore, to develop day surgery centers, it is necessary to address these issues by effectively managing patients, educating them on postoperative care and how to handle adverse reactions, improving follow-up efficiency, ensuring continuity of follow-up treatment, and accelerating postoperative recovery. Under our current healthcare system, relying solely on manual labor is insufficient to handle such a substantial workload; thus, assistance through medical information technology (IT) solutions is required.”

In terms of the market, listed companies such as Donghua Medical and Winning Health have relevant product offerings, but these are mostly limited to surgical appointment scheduling, with average transaction values under RMB 1 million, failing to meet the numerous professional requirements mentioned above. Furthermore, statistics from March 31, 2021, to March 30, 2022, show only nine targets identified through full-text search, indicating significant market potential.

To date, day-case surgeries account for approximately 13% of elective surgeries in China. Driven by supportive policies, this figure is poised to continue rising. Consequently, for startups, information systems for day-case care and postoperative rehabilitation represent a promising avenue with the potential to achieve leapfrog development.

Surging Demand: The Intelligent Transformation of the Intensive Care Unit

Unlike the three examples mentioned above, major changes in ICUs were driven by the ravages of COVID-19. Although there has been no independent policy support for their development in recent years, various policies introduced during the pandemic have imposed indirect requirements on ICUs. After all, the 2%–8% ratio of ICU beds to total hospital beds mandated 12 years ago in the Guidelines for the Construction and Management of Critical Care Medicine Departments (Trial) was only 1.73% in 2015, according to data cited in Guan Xiangdong’s book Forty Years of Critical Care Medicine in China.

Just as the expansion of ICU bed capacity is gaining momentum, so too is the intelligent transformation of ICUs. An ICU physician at Chengdu Third People’s Hospital told VCBeat, “Theoretically, the ICU should be the most highly informatized department among all medical specialties. It requires close teamwork and information exchange among physicians, continuous 24-hour monitoring of all patients’ vital signs, and accurate recording of all monitoring data to meet the high demand for data in clinical decision-making by different physicians. Furthermore, the ICU needs an integrated platform to aggregate various types of data and enable regional collaboration.”

Executing such tasks is no easy feat; it requires healthcare IT companies to possess robust IT solution capabilities, a solid grasp of medical logic and clinical thinking, and the involvement of engineers in clinical workflows to gradually address various detailed issues through long-term practice. Taking sepsis, one of the most critical conditions in the ICU, as an example, assessing a patient’s risk and stage of sepsis demands experienced clinicians who can integrate multiple factors, including the patient’s medical history, length of hospital stay, and physiological parameters. Purely IT-focused professionals are ill-equipped to deliver solutions that meet actual clinical needs.

Therefore, the most critical yet scarcest of the three key elements is IT talent equipped with ICU-style logical thinking. To secure such talent, one must either recruit physicians with an ICU background to transition into IT, or have medical IT professionals gain several years of hands-on experience within ICUs. Consequently, enterprises capable of providing comprehensive intelligent solutions for ICUs are extremely rare. Among startups, Sichuan Zhicall Technology, which has collaborated with West China Hospital for eight years, stands out as a leader and previously pioneered the new model of Enhanced-ICU (remote intensive care). Among publicly listed companies, Neusoft Group is relatively more advanced.

Given the relative complexity of intelligent solutions for intensive care units (ICUs) and the high threshold for entrepreneurial experience, this market remains a blue ocean. Furthermore, data from the National Health Commission’s “2019 National Medical Services and Medical Quality and Safety Report” shows that the proportion of ICU beds to total hospital beds rose from 1.9% in 2014 to 2.2% in 2018, representing a 16.4% increase. With this substantial growth in bed capacity, corresponding medical equipment and healthcare informatization are also poised to maintain rapid growth.

First movers will reap the short-term benefits of market expansion, but they must also accelerate the intelligent transformation of their businesses to brace for the impending industry shakeout.

The above four examples correspond to the three stages of medical IT innovation (specialty informatization) driven by departmental transformation: the Day Surgery Center is in the exploration stage, the Emergency Department and ICU are in the implementation stage, and medical record quality control has reached the maturity stage. Of course, these four examples are not exhaustive; nearly all innovation scenarios share similar characteristics, including:

1. Shifts in Departmental Status Under Policy Guidance: Medical IT companies invariably flock to mainstream hospital departments, resulting in largely homogeneous product architectures and content, where innovation fails to deliver value commensurate with the innovation itself. It is only when the status of a department changes that new demands emerge in scenarios previously underserved by medical IT solutions.

2. The Vacuum of Lacking Integrated Informatics Solutions: Even in a slow-moving sector like healthcare informatics, capital injection still seeks to accelerate growth, aiming to expand from regional markets to the national level as rapidly as possible. Consequently, when strategizing their market presence, companies often target niches lacking integrated informatics solutions, thereby developing products that can compete with, or even surpass, those of publicly listed companies.

3. Substantial Economic Value: The economic value of all selected scenarios must be evaluated, meaning that the hospital’s revenue-generating capacity should be enhanced, either directly or indirectly, upon procurement of the corresponding products.

Theoretically, the aforementioned scenarios and their corresponding medical IT products have the potential to help hospitals increase revenue. However, whether this can be achieved in practice, and whether these solutions can expand from regional markets to a national scale across China, remains uncertain. Further empirical evidence is needed to provide a more definitive answer.

Most importantly, latecomers must persuade the actual owners of hospitals, rather than department managers, that while solving problems is important, it is even more critical to identify effective payers.

However, the overarching trend toward specialized digitalization in healthcare is already set. Driven by policy and market demand, the emergence of several more national-level medical IT enterprises in China before 2025 may be merely a matter of time.