2022 Cancer Early Screening Industry Report: Four Business Models Accelerate to Capture a RMB 150 Billion Blue Ocean Market

China faces a severe cancer burden, with approximately 10,000 new diagnoses daily. Seventy percent of patients are initially diagnosed at intermediate or advanced stages, resulting in poor prognosis and low survival rates. Among the national policies for cancer prevention and control, early cancer screening has garnered increasing attention and high expectations.

Early Cancer Screening refers to the screening for early-stage cancers and precancerous lesions in target populations who appear healthy and have not yet exhibited obvious abnormal symptoms. Early screening holds promise for reducing cancer incidence and mortality rates, thereby improving patients' quality of life.

Currently, the main commercialization pathways for tumor early screening products based on genetic technology include ToH, ToB (health checkup centers), ToG, and ToC. Most companies have adopted differentiated strategies leveraging their respective strengths. As they continue to expand market coverage and seek innovative promotional approaches, enterprises have already identified some of the key success factors for each commercialization pathway.

To clarify the commercialization progress of current gene-based early cancer screening products and to identify the key success factors across various commercialization pathways, VCBeat has produced this report by leveraging policy insights and conducting multi-dimensional analyses of industry data. The research involved surveys of two research institutes, ten innovative enterprises, and five investment firms, as well as interviews with 19 experts, company founders, and investors. We have drawn the following conclusions:

Multi-Channel Market Education Drives Early Screening Products to Gradually Demonstrate Their Role in Optimizing Clinical Resource Allocationutilized actualForce。The process by which companies promote their products to hospital-based clinicians, end-users (C-side), and business clients such as health examination institutions (B-side) also serves as the most powerful form of market education. As companies advance their marketization efforts and market education deepens, end-users’ awareness of early screening has gradually strengthened, while hospital-based clinicians’ acceptance of early screening products has steadily increased. This trend helps direct clinical resources toward high-risk populations who truly need early screening.

A New Landscape Will Emerge Amidst a Flourishing Array of Scenario-Specific Early Screening ProductsUnique early cancer screening products are defined by distinct combinations of performance characteristics, pricing, clinical utility, and sampling procedures. Following a period of rapid, diversified growth, products tailored to the specific needs of various settings—including tertiary hospitals, health examination centers, primary care institutions, and home use—will be the first to establish successful commercialization pathways.

Commercialization of Early Screening Products Requires Strengthening Both Internal Capabilities and External Strategies。For tumor early screening products based on genetic technology, compliance is the foundation of their commercialization. In the process of commercial implementation, it is necessary to enhance the product's own strength by improving product performance, enhancing clinical guidance significance, and increasing cost-effectiveness. At the same time, measures such as improving market education, entering authoritative guidelines and consensus, and solving payment issues are needed to perfect the industrial ecosystem.

Currently, the industry has revealed a clear path for enhancing product competitiveness, with steady improvements achieved through a virtuous cycle. Furthermore, governments, enterprises, medical experts, basic medical insurance, and commercial insurance continue to collaborate in strengthening the industrial ecosystem.

Dual Drivers of Policy and Technology: Early Cancer Screening Carries a ¥150 Billion Market

>>>>

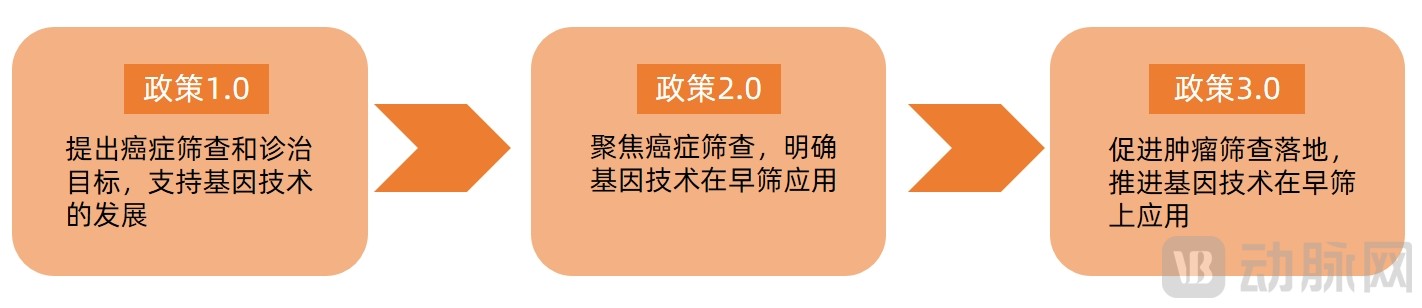

Three Stages in the Evolution of Early Screening Policies: From Focus to Implementation

Evolution of Early Cancer Screening Policies: Emphasizing Cancer Screening and Advancing Genetic Technologies.Specifically, in the field of cancer prevention and control, national objectives have progressively shifted from nationwide cancer screening and early diagnosis and treatment to targeted screening for high-incidence regions and high-prevalence cancer types, and further to localized implementation of tumor screening programs. In terms of technological advancement, the country continues to promote the application of genomic technologies in early cancer screening.

Overview of Early Cancer Screening Policies

Source: Arterial Orange Database, produced by VCBeat.

Based on the above policies and analysis, the evolution of policies can be divided into three stages.

In the first phase, the nation established goals for cancer screening and early diagnosis and treatment, while providing technical support for the development of genetic technologies. In the second phase, the focus shifted to screening for specific cancer types and in high-incidence regions, clarifying the application of genetic technologies in screening. In the third phase, the nation began implementing tumor screening across various regions, while simultaneously advancing the practical application of genetic technologies in early tumor screening.

Evolution of Early Cancer Screening Policies

Source: VCBeat, produced by VCBeat.

New Advances in Liquid Biopsy Technology Offer Potential for Further Cost Reduction

Screening methods are becoming increasingly diverse, with multiple technical pathways offering complementary advantages.Clinically, early tumor screening primarily relies on imaging and endoscopy. Liquid biopsy, in contrast, is an in vitro diagnostic technique that analyzes body fluids representative of the patient’s disease site—such as blood, saliva, sweat, feces, urine, and secretions. Currently, common assays include circulating tumor cells (CTCs), circulating tumor DNA (ctDNA), and tumor-derived exosomes.

Comparison between Traditional and Emerging Early Screening Source:: VCBeat, produced by VCBeat.

Source:: VCBeat, produced by VCBeat.

We can see that new discoveries have been made in both underlying technology platforms and biomarkers.。

For example, HIFI-prof technology from Herui Gene is based on the NGS platform and employs whole-genome sequencing, MeCap, and other series of detection techniques along with corresponding analytical algorithms for blood cfDNA. It builds early warning and prediction models for multi-omics, multi-dimensional low-frequency variants, including tumor early driver gene mutations, structural variations, and epigenetic alterations, achieving dual excellence in performance by ensuring both "accurate detection" and "precise computation."

Furthermore, He Rui Gene’s PCR-free WGS library preparation effectively reduces data redundancy and sequencing volume, thereby lowering the costs associated with whole-genome sequencing.。

In terms of biomarkers, Mei’ao Bio has developed a red blood cell-based liquid biopsy platform, discovering that from the same volume of peripheral whole blood, tumor-derived long DNA fragments can be extracted from abundant red blood cells with longer in vivo survival periods, yielding 50–100 times higher content than cfDNA.

Meanwhile, based on Mei’ao Bio’s long-term research, red blood cell-derived nucleic acids exhibit high content, longer fragment lengths, fewer loci in biomarker panels, and higher sensitivity. This positions the company to achieve equivalent or superior detection performance with fewer biomarkers, thereby reducing commercialization costs.

Early Screening Market Sees Steady Growth, with Scale Expected to Exceed RMB 150 Billion in Three Years

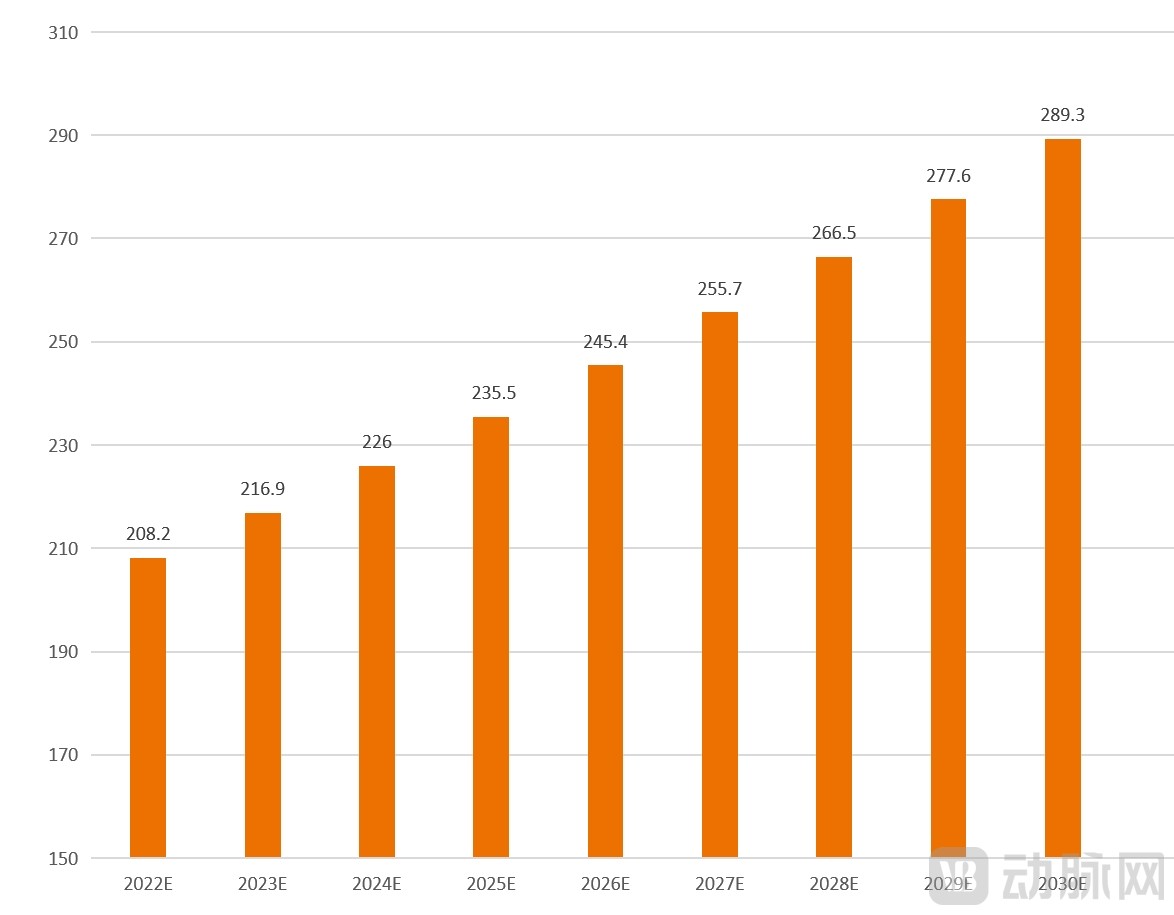

China’s tumor early screening market holds immense potential.In China, annual medical expenditures for malignant tumors exceed RMB 220 billion, representing a significant financial burden on households and the national basic medical insurance fund. According to a report by Frost & Sullivan, cancer treatment costs in China are projected to rise to USD 351.7 billion in 2023 and further increase to USD 592 billion by 2030.

According to Burning Rock Biotech’s prospectus, the market size of cancer early screening in China is projected to grow from $18.4 billion in 2019 to $28.9 billion in 2030.By 2025, the market size is expected to exceed $23.6 billion (approximately RMB 150 billion).。

Market Size of China's Early Cancer Screening Industry (USD Billion), 2022–2030

Source: Burning Rock Biotech Prospectus, prepared by VCBeat

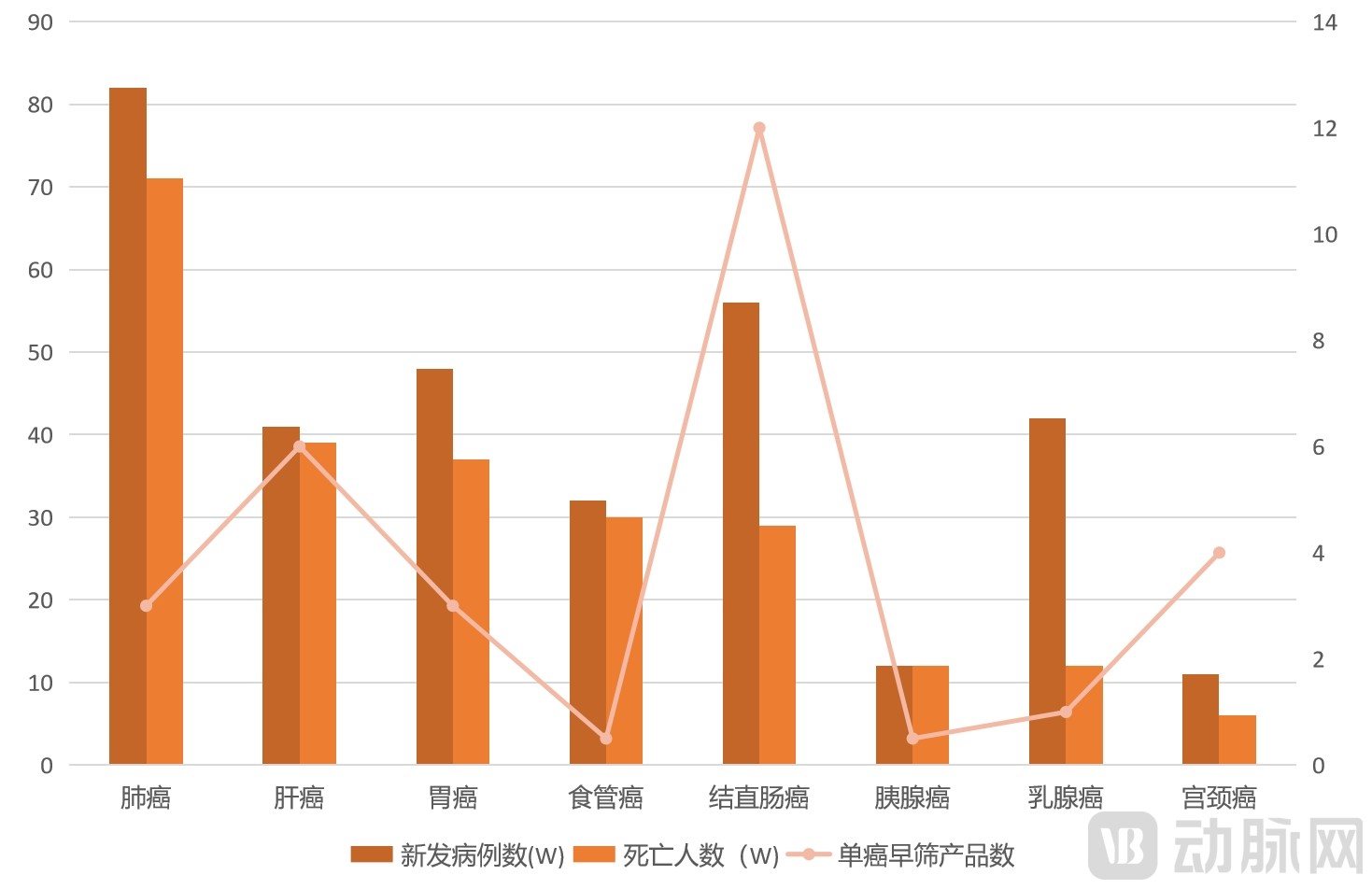

Single-cancer products cover a wide range of cancer types, with the largest number of products available for early screening of colorectal cancers.

Among early screening products based on genetic technologies, those targeting colorectal cancer are the most numerous, followed by liver cancer and cervical cancer. In contrast, there are relatively few corresponding early screening products for high-incidence cancers such as lung cancer and esophageal cancer.

Comparison of Product Counts Across Cancer Types

Data sources: WHO, Arterial Orange Database; produced by VCBeat.

Comparison and Analysis of the Top 10 Cancers by Incidence and the Number of Associated Early Screening Products (Limited to Commercialized Products)According to incomplete statistics, compared with other cancer types, there are fewer early screening products based on gene technology for high-incidence cancers such as lung cancer and esophageal cancer. In the field of lung cancer early screening, the mature application of AI technology may be one of the contributing factors.

Prospective Study Data Continues to Be Released, Product Performance Strongly Validated

Obtaining the Class III medical device certification for early screening from the National Medical Products Administration (NMPA) represents the highest endorsement of a product’s performance, largely due to the stringent requirements imposed on prospective registrational clinical trials during the approval process.

In September 2018, New Horizon Health launched “Clear-C,” China’s first prospective, large-scale, multicenter registration clinical trial for early cancer screening. Conducted under the supervision and guidance of the National Medical Products Administration (NMPA), the trial spanned 16 months, enrolling a total of 5,881 participants, with 4,758 cases ultimately included in the statistical analysis.

Ultimately, Colotect® secured China’s first approval for cancer early screening, backed by clinical trial data demonstrating a 95.5% sensitivity for colorectal cancer detection, a 99.6% negative predictive value for colorectal cancer, and a 63.5% sensitivity for advanced adenomas.

Furthermore, Genetron Health and the National Cancer Center launched the multicenter prospective study “HCCscreen™ Investigational Study.” As of February 2021, the study had completed follow-up for 1,615 patients positive for hepatitis B surface antigen (HBsAg). The blood-based HCCscreen™ test for early detection of hepatocellular carcinoma achieved a sensitivity of 88% and a specificity of 93%, outperforming ultrasound combined with alpha-fetoprotein (AFP) testing.

Genetron Health’s liver cancer early screening model, M2P-HCC, developed based on the findings of this study, has gained expert recognition.

In the single-cancer early screening market, an increasing number of prospective study results have been released. While companies have validated the performance of their respective products, they have collectively bolstered market confidence in early screening solutions, thereby encouraging more enterprises to accelerate the advancement of their prospective studies.

The Growing Number of Pan-Cancer Companies Is Set to Become the New Favorite in the High-End Market

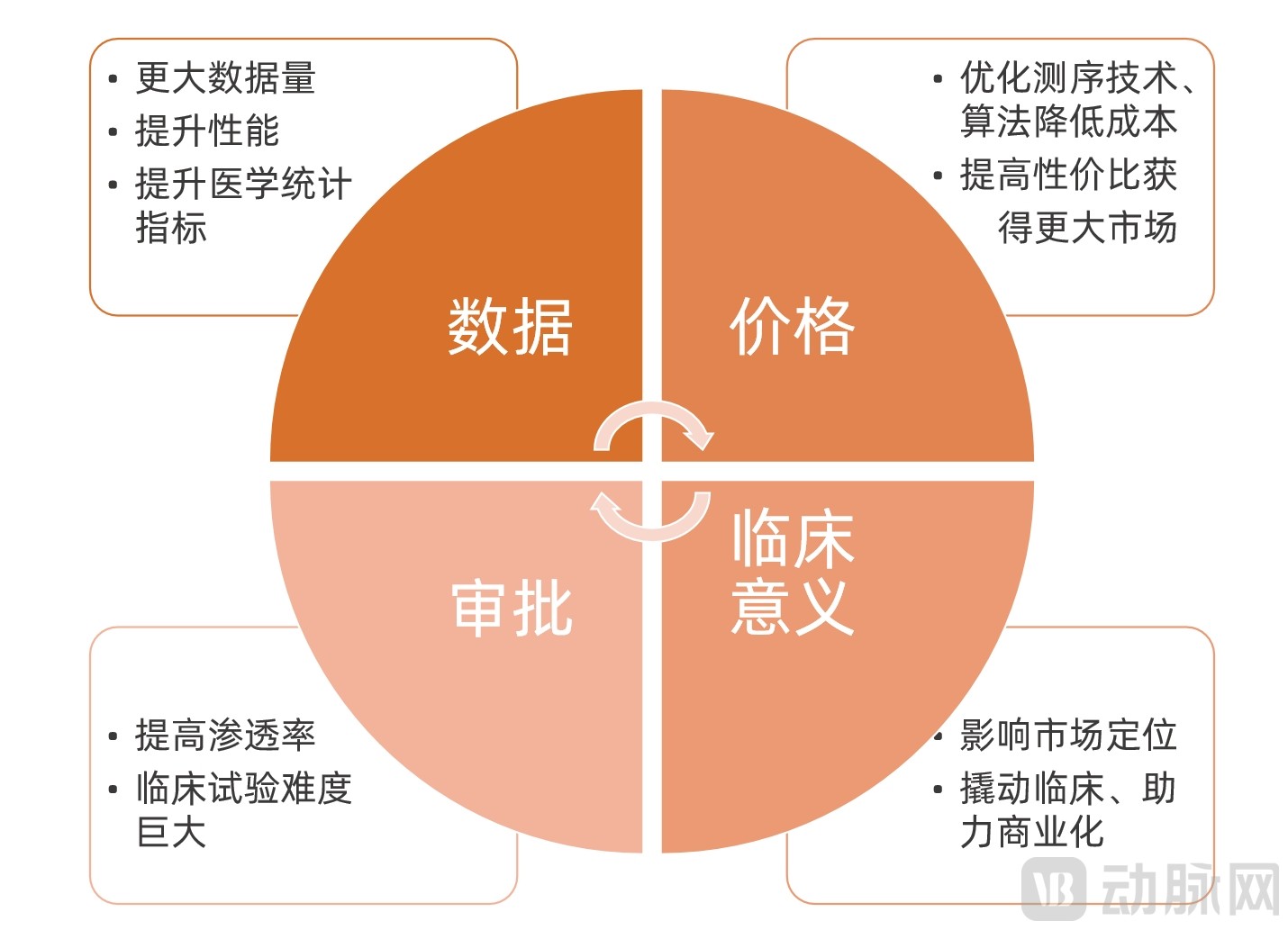

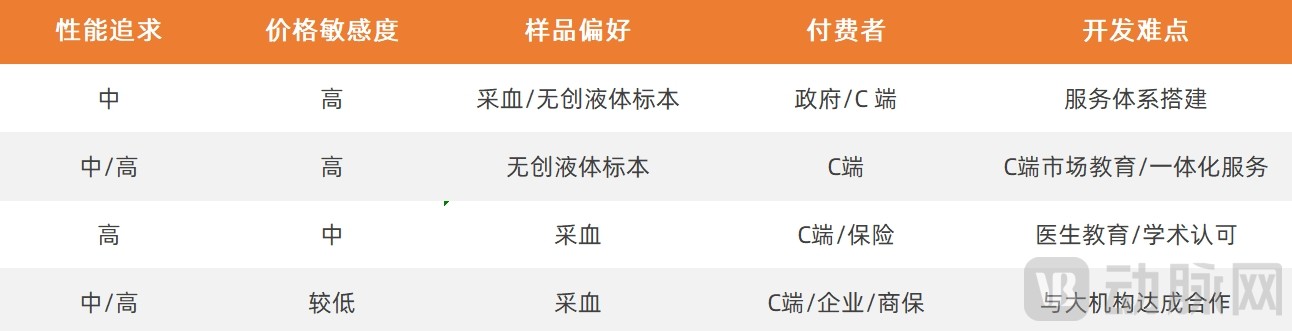

Data, pricing, approval, and clinical significance are key elements for product commercialization.As nearly everyone constitutes the target population, pan-cancer early screening products hold immense market potential. These products require larger datasets, necessitating that companies invest more time and capital to acquire sufficient data for continuously improving medical statistical metrics and enhancing product performance.

Commercialization Elements of Pan-Cancer Early Screening Products

Source: VCBeat, produced by VBInsight

Pan-cancer early screening may become the new favorite in the high-end market.Pan-cancer early screening products are typically priced several times higher than single-cancer tests, which is a major factor limiting their adoption. However, for high-net-worth individuals who are less price-sensitive and seek to screen for multiple cancer types using a minimal sample volume (typically blood), pan-cancer early screening products may represent a preferable option. Although these products come at a premium, they offer the convenience of obtaining multi-cancer screening results without regard to medical statistical metrics.

Single-cancer and pan-cancer products may not be a simple matter of “either/or,” but rather differentiated offerings tailored to consumers’ varying needs and purchasing power.

Early Screening Facilitates Rational Utilization of Clinical Resources, with Grassroots Levels Harboring a Vast Market

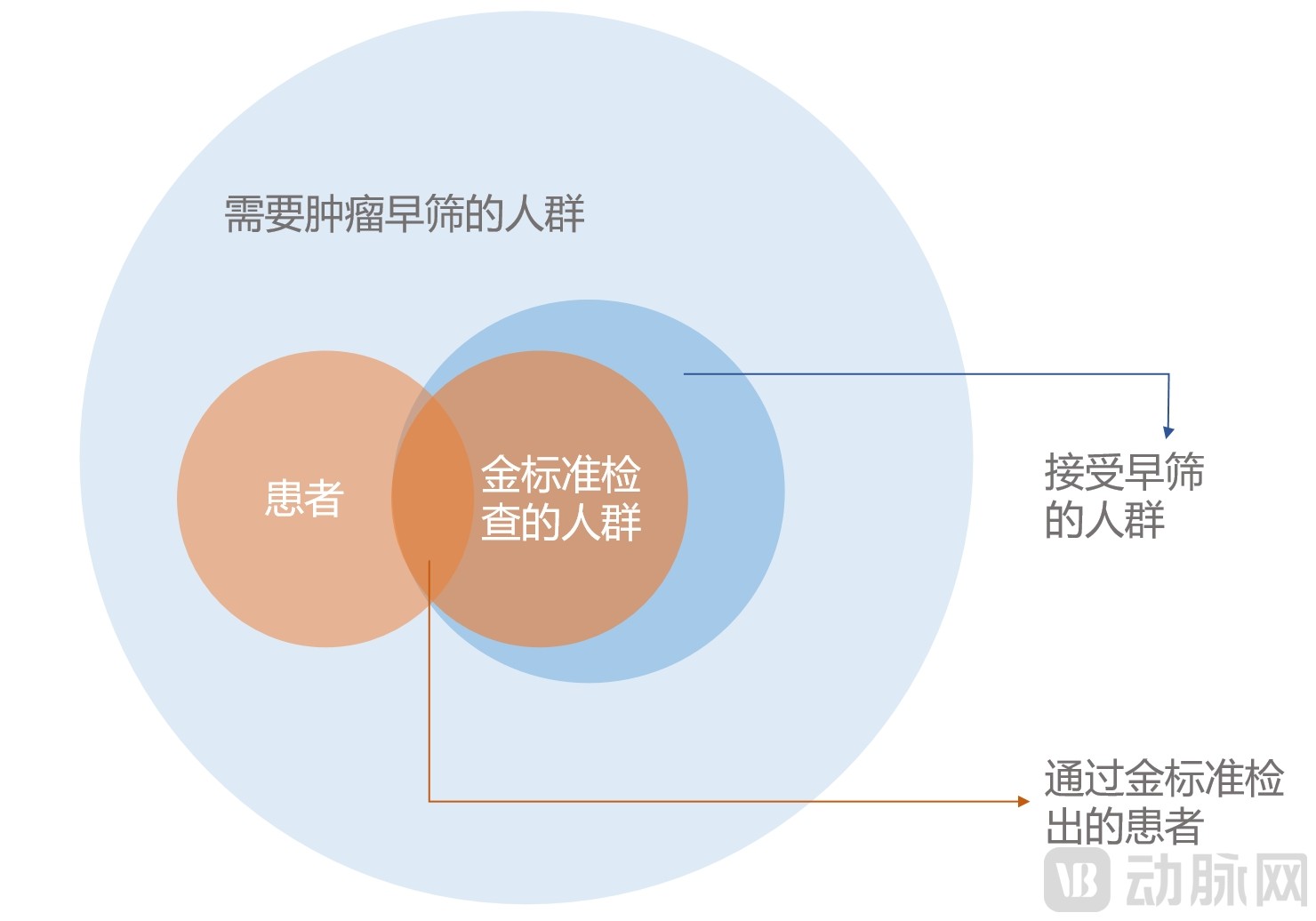

Clinical Significance of Early Screening Products: Facilitating Rational Resource Allocation.Traditional cancer screening tests are in short supply, while demand for early detection products is clear. Rather than replacing existing clinical diagnostic technologies for early cancer detection, the more significant value of early cancer screening in clinical practice lies in facilitating a more rational allocation and utilization of healthcare resources.

Supply and Demand in the Traditional Market for Early Cancer Screening

Source: VCBeat, prepared by VBInsight

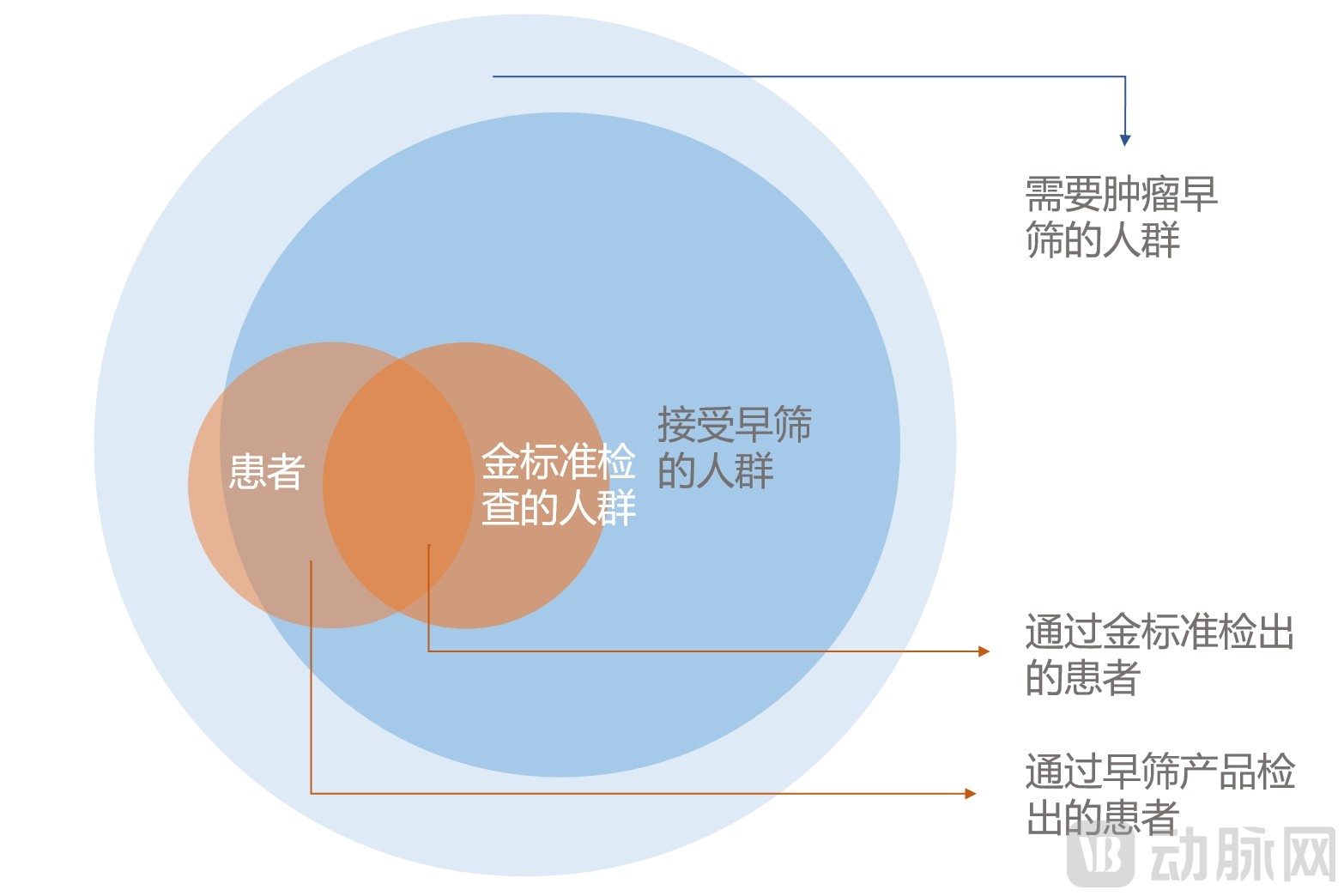

Early screening products serve three primary functions in facilitating the rational allocation of medical resources: first, they help meet the demand for early screening by reaching a broader population in need of cancer screening; second, they improve the detection rate of gold-standard diagnostics; and third, they provide patients and clinicians with more options during the diagnostic process.

Market Demand and Supply for Early Cancer Screening Driven by Screening Products

Source: VCBeat, produced by VBInsight

LDTs Unleash Their Beachhead Potential: Accelerating Market Education and Building Clinical Confidence

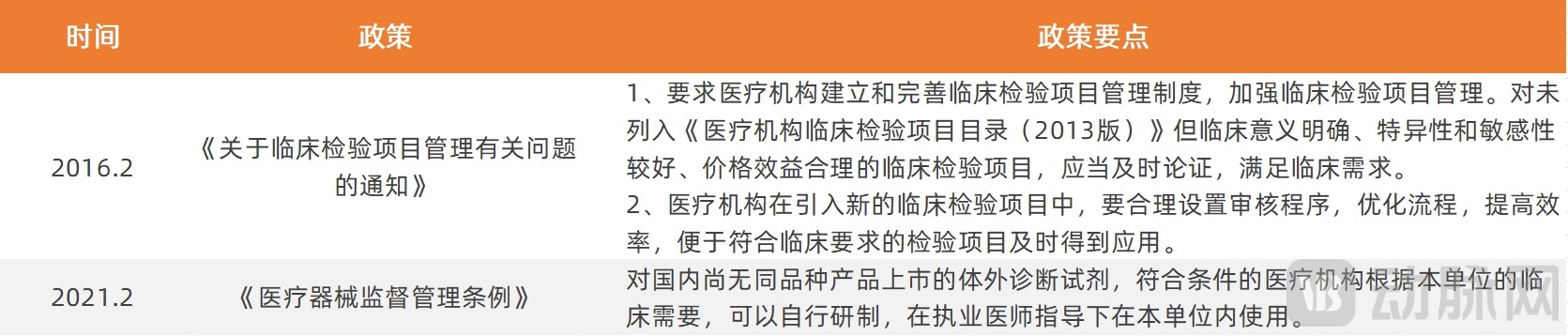

LDTs are subject to regulatory requirements at the policy level for the first time.On March 18, 2021, the National Medical Products Administration (NMPA) website released the revised Regulations on the Supervision and Administration of Medical Devices, requiring that laboratory-developed tests (LDTs) be used only under the following three conditions:

1. No in vitro diagnostic reagents of the same variety are currently marketed in China.

2. In-house Development and Use within Medical Institutions

3. Use under the guidance of a licensed physician

Regulatory Policies Related to LDTs

Source: National Medical Products Administration, Arterial Orange Database; prepared by VCBeat.

Optimizing product performance and accelerating market promotion are both indispensable.Prior to obtaining regulatory certification, early market deployment enables companies to generate revenue and alleviate financial pressure. More importantly, it facilitates the accumulation of real-world data, which can be used to validate and optimize technical models, enhance product performance, and ensure superior and reliable medical statistical metrics.

At this stage, racing to secure clinical applications and advancing technological R&D are equally important; neither can be dispensed with.

Expanding clinical coverage, cultivating physicians’ habits, and building clinical confidence are crucial.During the LDT phase, products with comparable cost-effectiveness must strive to capture greater market share, where clinical trust and physician endorsement are paramount. In hospitals, the interpretation of early screening results necessitates the involvement of clinicians, ensuring that report interpretations align more closely with physicians’ diagnostic and treatment practices.

Clinical Competitiveness Analysis Model for Early Screening Products

Source: VCBeat, prepared by VBInsight

IVD Gains First-Mover Advantage: Primary Care Is the Hidden Blue Ocean on the Healthcare Side

IVD Model: Reducing Marginal Costs and Facilitating Academic Promotion。In addition to continuing the LDT sales and service model, post-certification products have expanded their sales channels, allowing for direct sale as test kits to hospitals or clinical laboratories with appropriate testing qualifications. This new sales approach reduces costs associated with sample transportation, laboratory operations, and labor, thereby lowering marginal costs and enabling more agile responses to rapidly expanding market coverage.

Furthermore, products that have obtained NMPA medical device registration certificates will also benefit from academic promotion as a powerful tool in clinical settings. If the results of early screening products fail to gain clinical recognition, users will need to undergo traditional examinations regardless of the screening outcome. This would significantly diminish market demand for such products and hinder the development of the early screening market. Therefore, IVD products that effectively leverage academic promotion will further secure a first-mover advantage.

IVD Services for Primary Care: A Potential Blue Ocean in the Healthcare Sector.Due to limited diagnostic resources and clinical experience, primary care physicians often lack the infrastructure required for gold-standard early cancer screening methods, such as gastrointestinal endoscopy and CT scans. User-friendly early screening products make it feasible to conduct cancer screening in remote, grassroots healthcare settings.

Furthermore, the “grid-based” division of labor among primary healthcare institutions covers nearly all residents, maintaining clear and comprehensive health records that enable easy identification of individuals within the age groups recommended by guidelines for early cancer screening. With the support of appropriate software, it would be feasible to effectively notify and educate residents to complete early screening at the frequencies recommended by the guidelines.

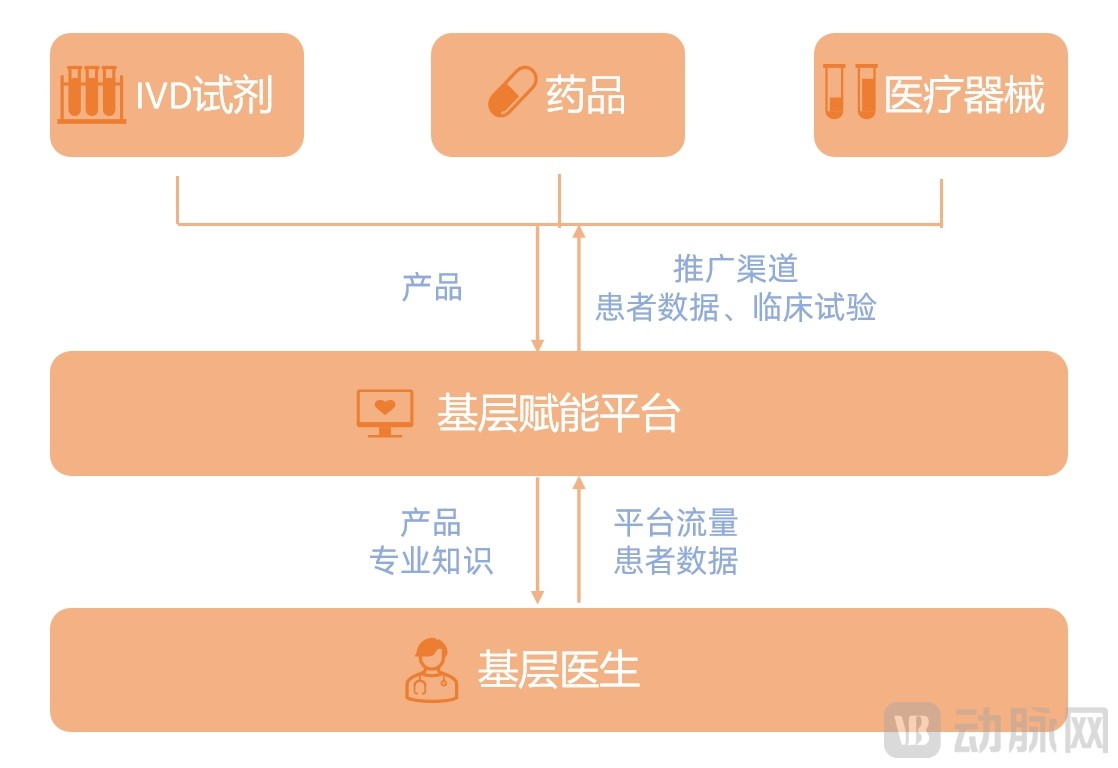

In fact, some enterprises have already initiated their deployment at the primary care level. Platform companies specializing in facilitating the reach of pharmaceuticals and medical devices to grassroots healthcare providers have provided significant support for the adoption of early cancer screening products in primary medical institutions.

Business Operation Model of Grassroots Empowerment Platform Companies

Source: VCBeat, produced by VBInsight

Early cancer screening is a specialized health examination program, with screening methods working in synergy.

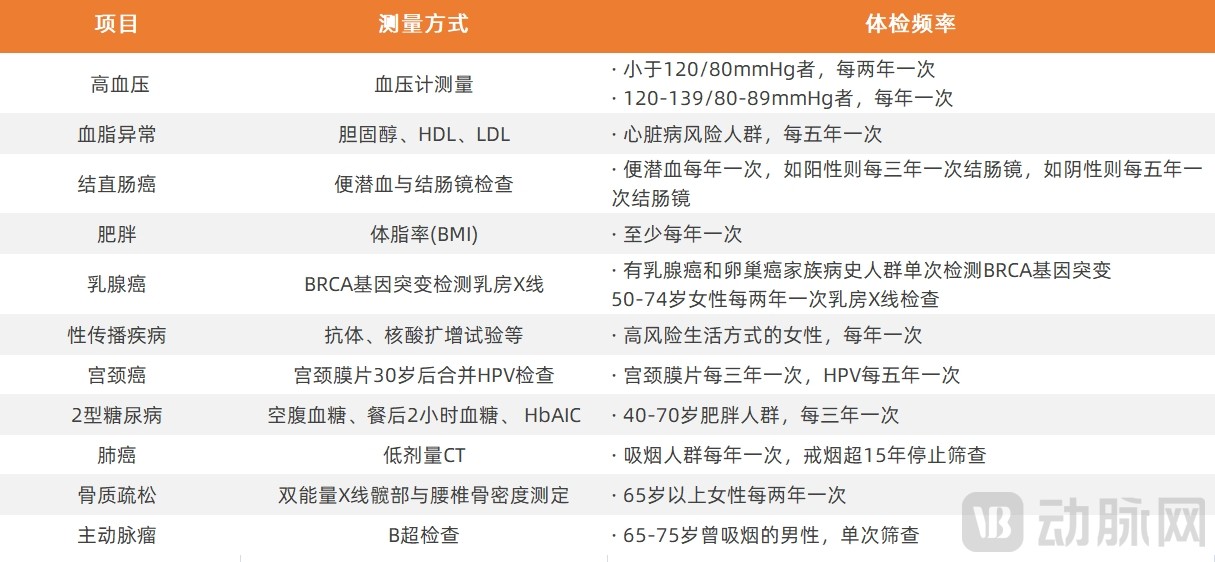

Domestic demand for health checkups continues to grow, with early screening companies actively expanding their presence. A “1+X” framework is adopted in designing checkup packages, where cancer early screening serves as the “X” specialized component, effectively complementing the basic “1” package.The U.S. Preventive Services Task Force (USPSTF), an authoritative body for issuing preventive medicine guidelines, recommends health screening items including hypertension, dyslipidemia, colorectal cancer, obesity, breast cancer, sexually transmitted diseases, cervical cancer, diabetes, lung cancer, osteoporosis, and aortic aneurysm, constituting a “1+X” comprehensive examination. Regarding specific screening methods, imaging, endoscopy, and genetic testing are jointly employed for early cancer detection.

Physical Examination Items Recommended by the U.S. Preventive Services Task Force

Source: VCBeat, prepared by VBInsight.

The Development of Early Cancer Screening in the Physical Examination Industry Shows a Trend of Integration

Overall, the core resources associated with early cancer screening projects in health checkup centers include upstream screening reagents/services, screening detection equipment, post-examination physician diagnostic and treatment services, insurance coverage at the payment stage, and data and technical services throughout the entire process. The current layout of early cancer screening in existing health checkup centers also relies on the integration of these resources.

Core Resources for Early Cancer Screening in Physical Examination

Source: VCBeat, produced by VBInsight

Integrate resources to build a “screening-diagnosis-treatment” service loop.Ping An Health (Check-up) Center is a key member of the Ping An Healthcare Ecosystem. Leveraging advanced diagnostic equipment and a team of authoritative medical experts, it has established a closed-loop medical service model encompassing “screening, diagnosis, and treatment.” In terms of equipment, the company has made significant investments to introduce state-of-the-art technologies such as 256-slice low-dose spiral CT scanners and 3.0T magnetic resonance imaging (MRI) systems.

Currently, in the field of early cancer screening and diagnosis, Ping An Health (Testing) Center has established a cancer prevention concept by customizing differentiated tumor marker panels—18 items for women and 15 items for men. Various precision imaging examinations have played a significant role in promoting early screening for specific cancers, including lung cancer, lymphoma, and gastric cancer.

Early-Stage Screening Companies and Health Checkup Centers Must Collaborate to Implement Early-Stage Screening Programs

Price advantage is a key factor for early screening companies to penetrate the health checkup market.Compared with entering the clinical side of hospitals, the threshold for early screening products or services to enter physical examination centers is relatively low. Product differentiation is one aspect; on the other hand, price advantage is an important factor for early screening companies to open up the physical examination market.

Value-Added Services Facilitate the Promotion of Early Screening Products in the Physical Examination Market.If early screening companies offer corresponding insurance as a value-added service with their products—for example, providing a certain payout if a positive diagnosis is confirmed within one year after an initial negative result, or partnering with health examination centers to reimburse imaging and endoscopic examinations,Therefore, such value-added services can, to a certain extent, alleviate customers’ concerns about payment and enhance the product’s appeal, particularly among non-high-net-worth individuals within high-incidence populations who are more price-sensitive.

Diagnostic services at health examination centers facilitate the upgrade of early screening product offerings.If health checkup centers can address patients’ subsequent diagnosis and treatment needs, thereby alleviating their concerns about medical care, they will be more attractive to potential customers.

Central and local governments are continuously increasing their financial investment in early cancer screening programs.

The early cancer screening program has received government support in terms of both policy and funding.According to data from the official website of the National Health Commission, in 2018, the central government allocated more than RMB 280 million in subsidies for early diagnosis and treatment of cancer. By the end of 2018, the cumulative investment from the central government had reached nearly RMB 1.87 billion. At the local level, Shanghai and Tianjin have included colorectal cancer screening in their public welfare programs.

Selected Oncology Projects and Achievements Funded by the Central Government Since 2005

Source: VCBeat Orange Database, produced by VCBeat.

Under policy support, the 5-year survival rate for malignant tumors has increased by nearly 10%.At a press conference held by the National Health Commission in June 2018, He Jie, an academician of the Chinese Academy of Sciences and Director of the National Cancer Center, announced that the current five-year survival rate for malignant tumors had risen from 30.9% a decade earlier to 40.5%, representing an increase of nearly 10 percentage points. This indicates that the overall effectiveness of early screening in recent years has been considerable.

Genetic Testing Technologies Demonstrate Higher Adherence at the Primary Care Level

The grassroots level is the weak link in the four-tier cancer prevention and control system.Within China’s four-tier cancer prevention and control system—national, provincial, municipal, and county levels—the grassroots level remains the weakest link in early tumor screening efforts.

Dilemmas in Early Cancer Screening at the Primary Care Level

Source: Kunyuan Bio, VCBeat.

Public health initiatives for early cancer screening based on genetic testing have demonstrated higher compliance at the grassroots level.From the perspective of early cancer screening methods, traditional approaches such as endoscopy and medical imaging remain the mainstream modalities for implementation, both in hospital clinical settings and in health examination centers. With the application of genetic testing technologies in early cancer screening, the convenience of performing preliminary screening through a simple blood draw has led to higher compliance among high-risk populations.

Public welfare initiatives hold strategic significance for enterprises, laying the foundation for the promotion of early screening programs.For early screening companies, public welfare projects can not only promote product adoption and validate the feasibility of their offerings but also secure certain government subsidies.Currently, public welfare projects hold strategic significance for early screening companies.

Developing Livelihood Projects Requires Joint Efforts from All Parties

For Different Regions, Cancer Type Selection Is Fundamental. Climates in Different Regions, Differences in lifestyle and dietary habits are correlated with the incidence of specific cancer types, which exhibit regional characteristics. Selecting appropriate regions and cancer types is fundamental to developing public welfare projects.

High-Incidence Regions for Various Cancer Types

Source: 2018 Annual Report of China Cancer Registry, prepared by VCBeat.

Livelihood projects are a process of multi-party collaboration and joint participation.Livelihood projects require coordinated efforts from all parties,In decision-making for public welfare projects, entities such as the National Health Commission and the Centers for Disease Control and Prevention play a supportive role, with the key determinant being the willingness of local governments. During implementation, efforts should begin with regular public reminders and health management services provided by medical institutions, adopting a point-to-area approach to gradually expand coverage. Coupled with top-down mobilization and supervision by grassroots cadres, this strategy aims to achieve proactive nationwide participation in cancer screening, early diagnosis, and early treatment.

In livelihood projects, the power of innovative enterprises is crucial.On one hand, it possesses cutting-edge early cancer screening technologies; on the other, it has established a service system capable of handling the scale required for public welfare initiatives. Key components—including logistics systems, standardized medical laboratory testing protocols, early screening technical training, science popularization platform development, after-sales services, and report interpretation—must all align with the operational scale demanded by such public health programs.Only in this way can the “hardware” and “software” conditions for cancer prevention and control as a public welfare initiative be ensured.

In the short term, compete for early market share through differentiated services.

A positive service experience is key to retaining users and driving traffic in the consumer market.Currently, end-user customers who purchase the product directly fall primarily into two categories: one consists of repeat buyers who first used the product upon recommendation from professional clinical institutions and were satisfied with their service experience; the other comprises those who purchased and used the product based on recommendations from friends or family members who had positive experiences.Among these, the crucial product factor is to provide a good user experience.。

Therefore, a comprehensive service process and superior user experience are increasingly critical for capturing the consumer (C-end) market. In response, companies are not only continuously optimizing their core product service workflows but also introducing various value-added services to provide patients with enhanced experiences and greater assurance.

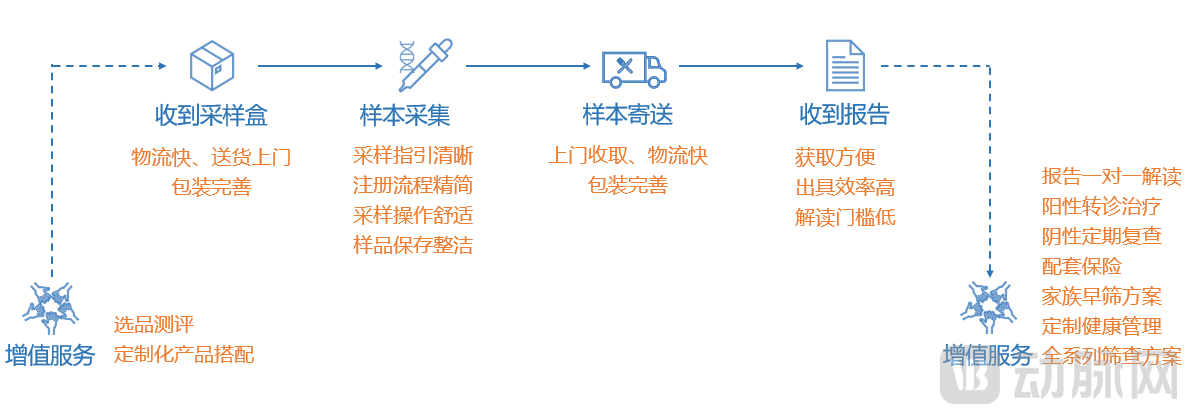

Service Chain for Early Screening Products: Pre-, During, and Post-Use

Source: VCBeat, prepared by VBInsight

As illustrated in the chart, the traditional product service process involves users receiving a sampling kit, completing registration and sample collection according to the instructions, and mailing the samples back to the laboratory, followed by a waiting period for the report. Each stage of this process offers ample room for service enhancement. In addition to vertical optimization of core product services, a series of value-added services have been horizontally extended to the pre- and post-service phases.

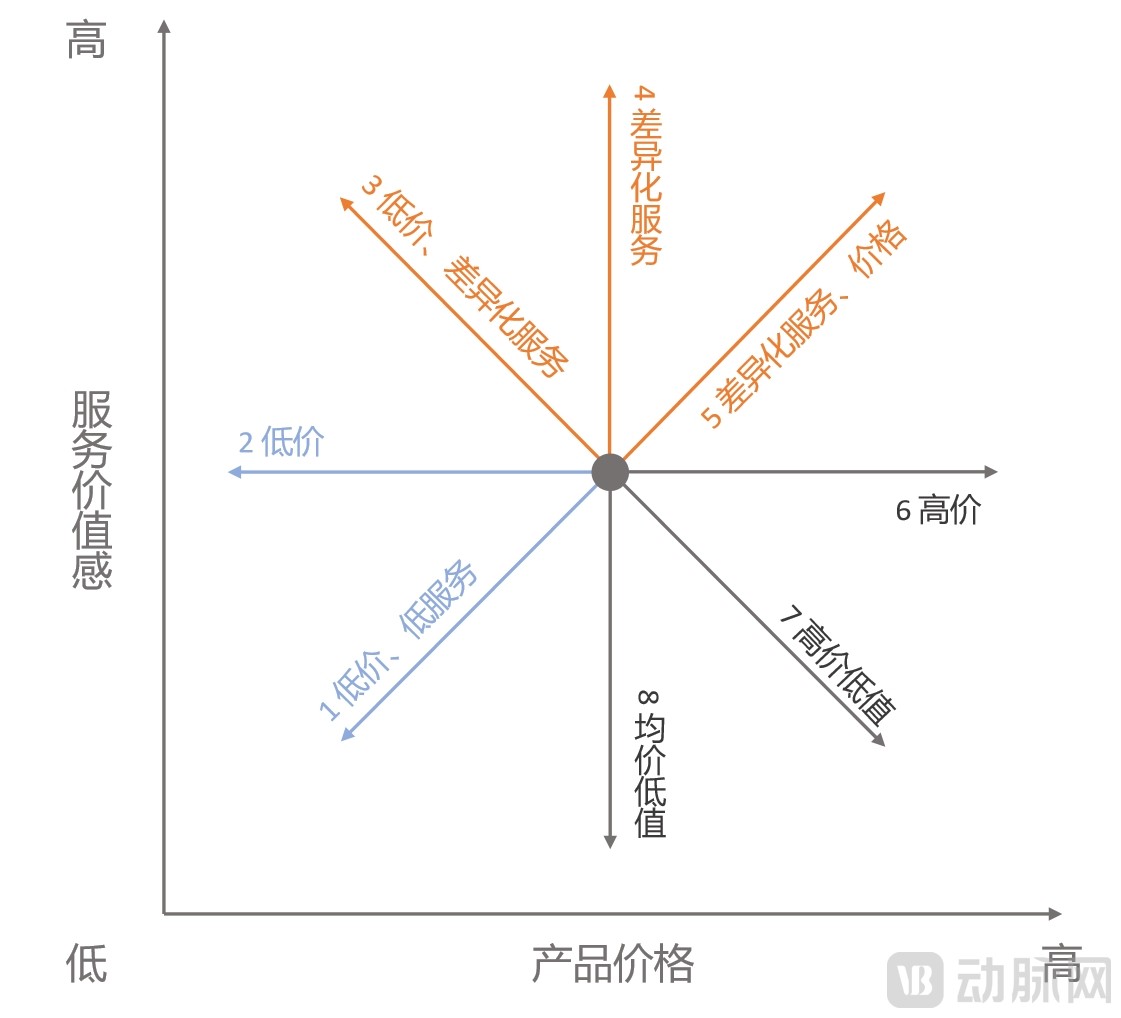

Deeply understand consumer needs to precisely create differentiated services.Adopting low pricing, even at the expense of certain services, to capture a segment of the market that is highly price-sensitive may serve as a short-term survival strategy; however, companies must ultimately join the ranks of competitors differentiating through service offerings. To gain greater competitiveness in this realm of differentiated services,It is crucial to gain a deep understanding of consumer (C-end) needs, accurately assess the urgency of these needs, and match them with corresponding value-added services.。

The Competitive Strategy Clock for Early Screening Products

Source: VCBeat, prepared by VBInsight

Long-term performance, capturing the consumer market with real-world data

NMPA approval and expert endorsement are a powerful booster for the consumer market.C-end users are less sensitive to medical statistical indicators than clinical professionals, but more sensitive to whether the product has obtained national approval and whether it is recognized and recommended by clinical experts.

Compared with the effort required to educate end-users on how to distinguish between retrospective and prospective trials, and to differentiate the sensitivity and specificity of data products from various sources,The “yes-or-no” advantage of obtaining national approval or receiving expert recommendations is more effective for B2C consumers.

Certification brings the C-end market while providing better regulation and development for consumers.In fact, the regulatory approval of early screening products not only brings trust and reliability to consumers but also creates a safer and more standardized market environment for early screening from multiple dimensions.

A New Landscape Will Emerge Amidst a Flourishing Array of Early Screening Products Tailored to Specific Scenarios

Different scenarios impose varying expectations and demands on early screening products.The early-stage cancer screening sector has experienced a period of rapid, diversified growth. Moving forward, companies with core competitive advantages will outpace the market’s growth rate, expand rapidly, and gradually distinguish themselves.

Currently, although enterprises employ largely similar promotion models and channels, the inherent differences in products—from technology to user experience—combined with disparities in resource availability among companies, are leading to increasingly divergent outcomes across channels for products within the same sector. In the future, differentiated leading products are likely to emerge in various settings, including home care, tertiary hospitals, primary healthcare institutions, and health examination centers.

Expectations and Requirements for Early Screening Products Across Different Scenarios

Source: VCBeat, prepared by VBInsight

Product + Corporate Differentiation Advantages Enable Products to Shine in Their Respective Scenarios.Invisible yet powerful market forces will increasingly drive product differentiation among enterprises. In the future, products with strong penetration into lower-tier markets and a high cost-performance ratio are expected to thrive at the grassroots level, while those that leverage expert educational resources and boast a complete service industry chain may win favor among end consumers.

Meanwhile, products with high academic research value and significant clinical relevance will demonstrate stronger competitiveness in tertiary hospitals, while those with average performance and pricing may achieve greater penetration in health checkup centers.

Market Education Improves, Early Screening Products Gradually Demonstrate Their Ability to Optimize Clinical Resource Utilization

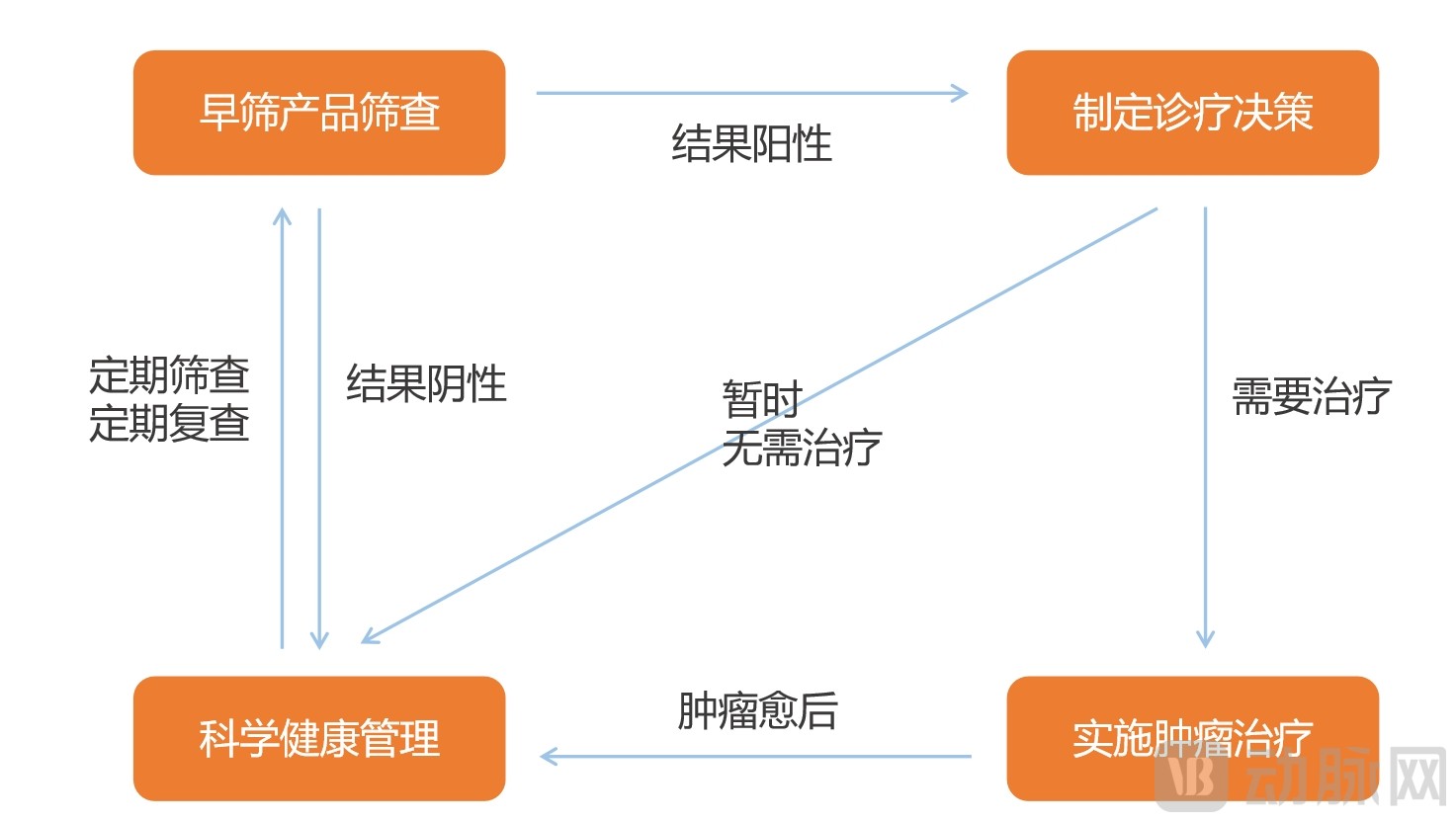

Early cancer screening is increasingly playing a role in triaging healthy individuals and patients, significantly optimizing the utilization of medical resources.For tumors, over a long period in the past, the needs of asymptomatic individuals undergoing routine check-ups, those concerned about developing the disease, symptomatic high-risk groups, and patients urgently requiring diagnosis were all borne by clinical medical resources.

Limited medical resources are overwhelmed, making it difficult to allocate them according to actual needs. Tiered diagnosis and treatment has been a long-standing focus of healthcare system reforms, and early screening products in the field of oncology can make effective contributions to this effort, helping to ensure more rational utilization of clinical resources.

The Triage Effect of Early Screening Products on the Population

Source: VCBeat, produced by VBInsight.

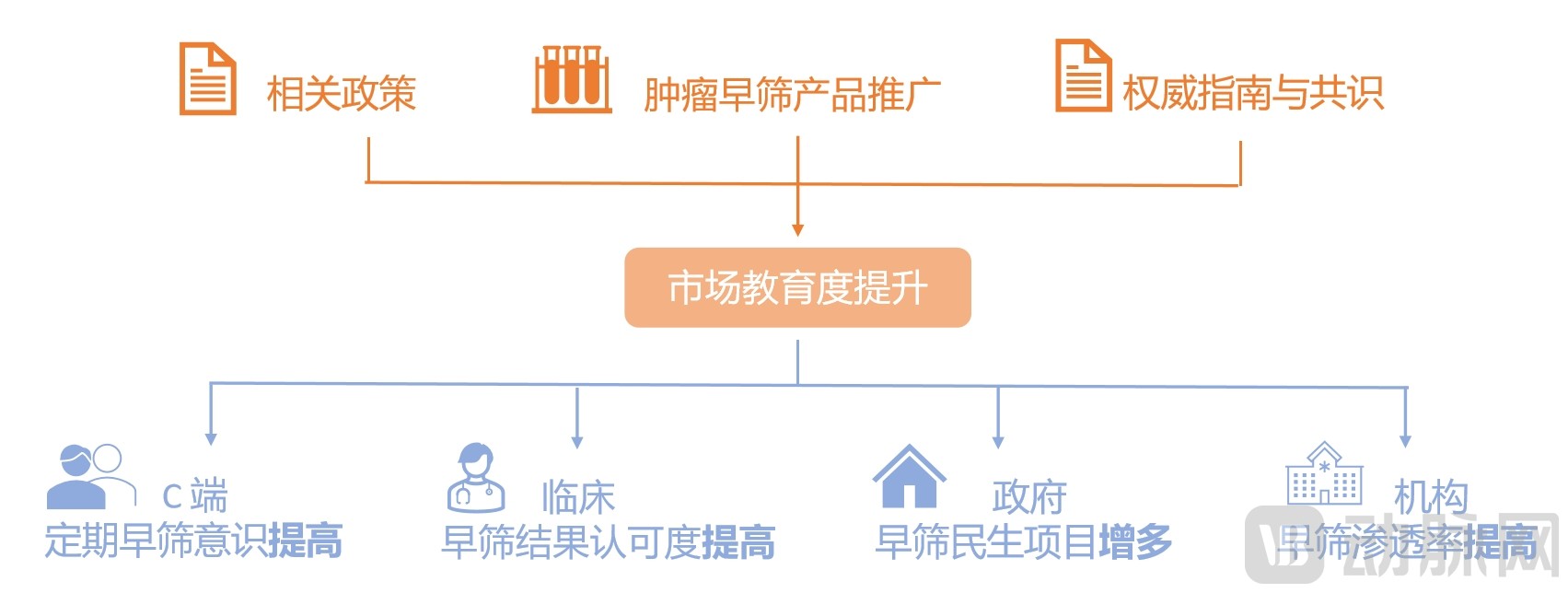

Product promotion is an effective process of market education.In the aforementioned triage system, concerted efforts and consensus among all market participants are required. There remains significant room for improvement in market education, where policy measures and product promotion serve as effective educational avenues. These initiatives provide substantial support for achieving organic coordination across all stages, ultimately optimizing the utilization of medical resources.

Marketization Process Enhances Market Education Levels

Source: VCBeat, produced by VBInsight

Product Commercialization Requires “Internal and External Excellence”

Enhancing one's own capabilities and improving the industrial ecosystem are both indispensable.The core of gene-based early cancer screening products is rigorous medicine, meeting the screening needs of high-risk populations while expanding into the potential consumer-grade C-end market.

This inevitably means that, from R&D to commercialization, the product must not only strengthen its own competitiveness by improving performance, enhancing clinical guidance value, and increasing cost-effectiveness, but also mature the industry ecosystem through measures such as advancing market education, gaining inclusion in authoritative guidelines and consensus statements, and addressing reimbursement challenges.

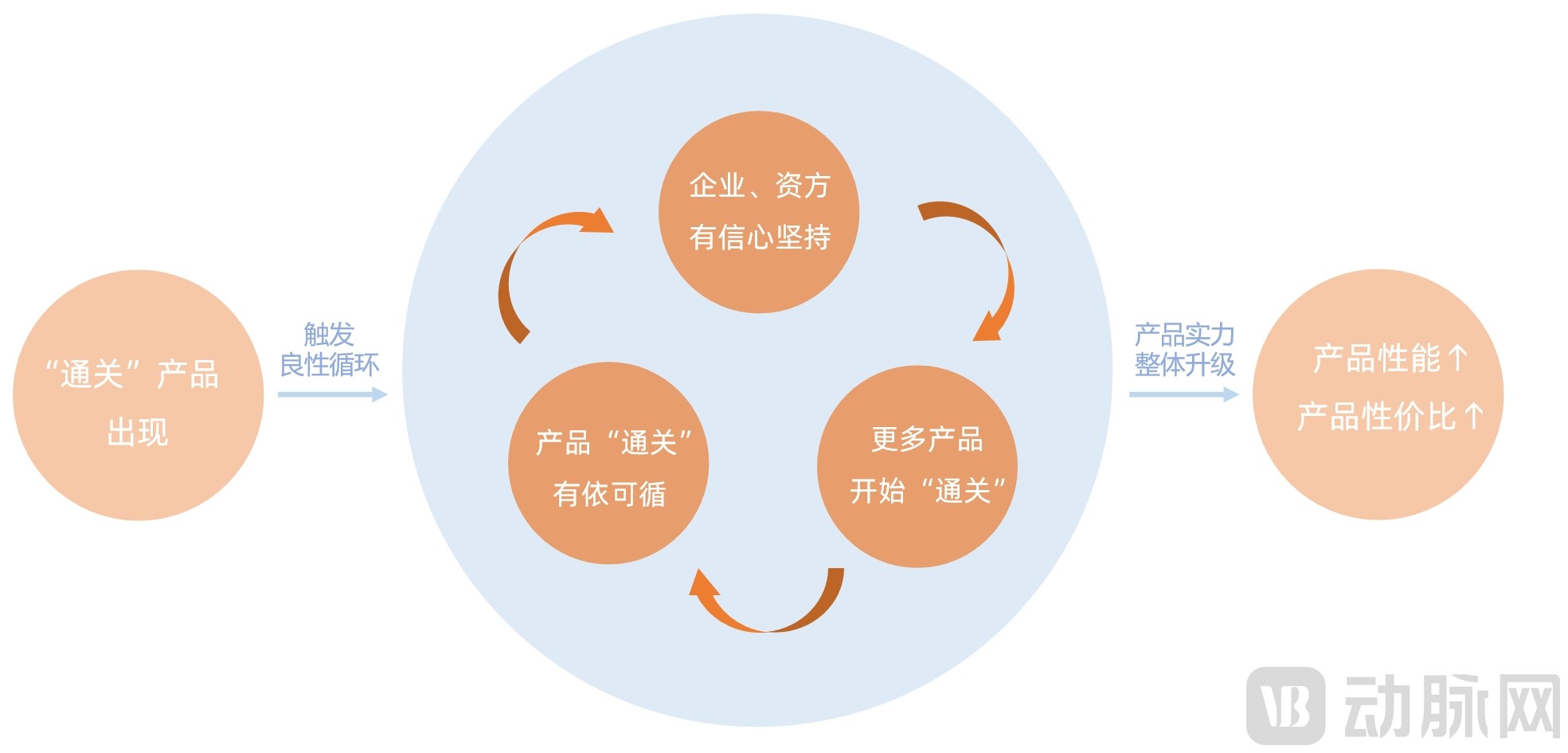

Product strength is steadily improving, with a clear upgrade path emerging.After several years of rapid development, the capabilities of gene-based early cancer screening products have steadily improved. The sector has also seen its first products successfully achieve regulatory approval, clarifying the pathway for product capability enhancement.

This has triggered a virtuous cycle of enhanced product capabilities. A clear upgrade path boosts confidence among companies and investors still “on the journey,” while providing a well-defined framework for strengthening product capabilities, thereby facilitating the emergence of more products that successfully “pass the test.” Within this virtuous cycle, the pathway for product upgrades will become increasingly clear, ultimately promising to reduce capital and time expenditures while enhancing product cost-effectiveness, all while ensuring continuous improvement in product strength.

Currently, the prices of most gene-based tumor early screening products are on par with or higher than those of the clinical “gold standard.” As these products continuously improve through the aforementioned virtuous cycle and their cost-effectiveness increases to the point where their prices fall below that of the “gold standard,” their commercialization process will accelerate significantly.

The Virtuous Cycle of Steadily Enhancing the Intrinsic Strength of Early Cancer Screening Products

Source: VCBeat, prepared by VBInsight.

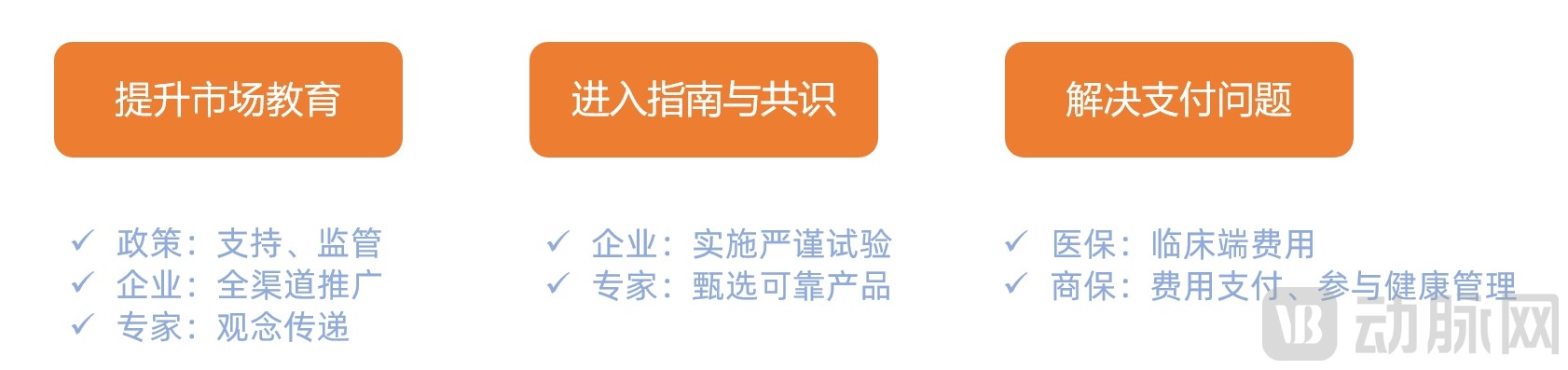

Perfecting the industrial ecosystem requires collaborative efforts from all sectors.At this point, products with reliable performance and high cost-effectiveness still cannot be guaranteed to achievesuccessful commercial implementation. To truly enable laboratory research findings to reach end users, support cancer prevention and control, reduce incidence rates, and improve survival rates, collaborative efforts across all sectors are needed to gradually enhance the industrial ecosystem:Enhance market education, gain inclusion in authoritative guidelines and consensus statements, and address reimbursement challenges.

Pathways to Creating a Business-Friendly Environment for the Commercialization of Early Cancer Screening Products

Source: VCBeat, produced by VBInsight

Currently, some early screening products have been included in guidelines and consensus statements, collaborations with commercial insurance are already underway, and policies are showing increased support and regulatory efforts. In the future, through the collaborative efforts of the government, enterprises, medical experts, public health insurance, and commercial insurance, gene-based cancer early screening products will surely see a more robust industrial ecosystem. With both internal improvements and external advancements in the commercialization process, the market prospects for early screening products are promising.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows. Scan the QR code to access the mini-program and read the full report for free.

1.1 Three Stages in the Evolution of Early Screening Policies: From Focus to Implementation

1.2 New Explorations in Liquid Biopsy Technologies Offer Potential for Further Cost Reduction

2.2 The Growing Number of Pan-Cancer Companies May Become the New Favorite in the High-End Market

3.1 Clinical Significance of Early Screening Products: Facilitating Rational Allocation of Resources

3.2 LDTs Unlock Beachhead Potential: Accelerating Market Education and Building Clinical Confidence

3.3 IVD Gains First-Mover Advantage; Primary Care Is a Hidden Blue Ocean in the Healthcare Sector

4.1 Early Cancer Screening as a Specialized Health Checkup Item with Synergistic Screening Methods

Chapter 5: Livelihood Projects Are a Powerful Tool for Early Market Expansion by Enterprises

5.1 Central and Local Governments Continuously Increase Funding for Early Cancer Screening Programs

5.2 Genetic Testing Technologies Demonstrate Higher Adherence at the Primary Care Level

5.3 Developing Livelihood Projects Requires Joint Efforts from All Parties

Chapter 6: Leveraging Service and Performance to Capture the Consumer Market

6.2 Focus on Long-Term Performance to Capture the Consumer Market with Real-World Data

7.3 Commercialization of Early Screening Products Requires “Internal and External Excellence”

This report is part of the series for the 6th Future Healthcare Top 100 Conference by VCBeat. The conference will be held online from June 14 to 18, during which the report will be presented and released. Below is the QR code for downloading the full text of the report.

Special Thanks (in order of interviews):

Mr. Kang Jian, Director of Brand and Content at Yunqueyi; Mr. Sun Tong, Vice President of Meinian Onehealth Healthcare Group; Mr. Zhu Yeqing, CEO of New Horizon Health; Mr. Zhang Jiangli, CEO of Genetron Health; Mr. Zhu Weiyan, Founder of Meiao Bio; Ping An Health (Testing) Center; Genetronics; HelixGene; and BGI Genomics for their strong support in the preparation of this report.