Digital and AI Health White Paper Released: Core Driver of Future Industry Growth and Catalyst for Competitive Landscape Transformation

Editor’s Note: This article is from China Renaissance Capital. Authors: Li Rui, Zhang Yizhou, Yi Chuanqi, Hu Binyu, Hu Tianmou. Republished with permission by VCBeat.

Core Viewpoints

1. Digitalization will become the core driver of future growth in the healthcare industry, leading a new round of changes in the competitive landscape. Driven by a combination of factors—including policy support, technological iteration, market evolution, and the normalization of pandemic control measures—the healthcare industry is embracing digital technologies as never before, comprehensively advancing into the era of “digital governance.” Digital technologies are reshaping, or are poised to reshape, the healthcare industry. Over the past year, primary market transaction activity in the digital health sector has increased significantly, the number of companies filing for IPOs has surged, and initial public offerings have achieved remarkable growth.

2. Regulatory policies are accelerating the supply-side reform of healthcare into a critical phase, compelling the entire industry chain—upstream and downstream—to reduce costs, improve efficiency, and ensure strict legal and regulatory compliance. Key stakeholders, including pharmaceutical companies, hospitals, and insurers, must respond promptly and proactively to meet these regulatory demands. These demands range from implementing end-to-end digital traceability for pharmaceutical products targeting drug manufacturers, to advancing hospital informatization reforms led by the full coverage of electronic medical records (EMR) in Grade III hospitals, and encouraging the development of commercial health insurance as the primary secondary payment platform amid increasingly constrained basic medical insurance payments.

3. Cutting-edge technologies are flourishing and emerging in rapid succession, injecting a continuous stream of new momentum into the industry.

(1) AI-driven drug discovery in China is currently in the validation phase, having rapidly transitioned from the start-up stage to the growth stage, with future efforts gradually shifting toward the mid-to-late stages.

(2) Medical robots have reached a critical juncture for clinical validation, with surgical and rehabilitation robots gaining the highest industry recognition; commercial breakthroughs that further increase installation rates and utilization rates are highly anticipated.

(3) Extended Reality (XR) is gaining momentum and will gradually be applied to various scenarios, including disease treatment, clinical assistance, rehabilitation training, medical education and training, and medical nursing, thereby delivering unprecedented user experiences and innovative diagnostic and therapeutic pathways;

(4) The nascent emergence of digital twins is poised to drive commercialization in healthcare, with initial adoption occurring on both the pharmaceutical enterprise and patient sides—particularly in applications such as digital drug trial models, precision medicine, and health monitoring and management.

(5) As digital therapeutics (DTx) gradually mature, DTx companies that exhibit the “three haves and three highs”—namely, clear indications and mechanistic rationale, robust evidence-based medical support, and identified payers, coupled with a large patient base, high growth rates, and strong willingness to pay—will continue to attract capital attention. This is particularly evident in fields such as ophthalmology and mental health. The first-mover advantage of leading enterprises will enable them to rapidly widen their gap with competitors.

4. Frequent instances of IPOs breaking issue price and valuation inversions in the secondary market for healthcare have signaled a shift toward greater market rationality going forward.

First is the rational analysis of demand, specifically determining whether a sector represents genuine or pseudo-demand, assessing the rigidity of such demand, and evaluating whether the market size and growth ceiling are sufficiently large;

Second, a rational assessment of commercialization: whether the business model is theoretically viable and practically executable by the team, and whether stakeholders are genuinely willing to pay, along with the magnitude and sustainability of their willingness to pay;

Third, rational reflection on regulation: whether today’s logic will remain valid tomorrow, whether current policies will continue to apply in the future, and, against the backdrop of medical insurance cost containment and “vacating the cage to change the bird” (i.e., phasing out low-value services to make room for high-value innovations), what pathways offer sustainable long-term development.

5. Key Sectors Under Capital Spotlight and Worth Anticipating in 2022:

● Supply Side: AI-driven drug R&D, smart pharmaceutical enterprises, smart hospitals, and digital drug companions

● Demand Side: Myopia prevention and control in adolescents, adolescent mental health, smart rehabilitation for the elderly, early screening for lung cancer and Alzheimer’s disease, women’s health, and emerging sectors combining consumer services with healthcare

● Payer Side: Healthcare IT and health insurance technology companies, differentiated innovative commercial insurance products

I. What Major Changes Occurred in 2021

In 2021, driven by a confluence of factors—including policy support, technological iteration, market evolution, and the normalization of pandemic control—the healthcare industry is embracing digital technologies with unprecedented momentum, comprehensively advancing into an era of “digital governance.” Digital technologies are reshaping, or poised to reshape, the healthcare and medical industry. Never before has innovation, exemplified by digital technology, garnered such widespread attention, emphasis, and participation across the entire healthcare sector. Stakeholders throughout the industry appear to have tacitly reached a consensus: digitalization will become the primary driver of industrial scale growth and serve as a watershed moment in the new round of global industrial competition.

Due to its high compliance requirements and low level of digitalization, the healthcare industry has become one of the most important scenarios for the practical application of digital technologies. The industry itself is undergoing structural changes as its digital maturity increases. The enormous industrial value embedded in this transformation has successfully reignited capital interest in digital health.

(I) Digital Healthcare Seizes a Transaction Boom, Facilitating the Transition from Old to New Growth Drivers in the Industry

1. Looking back at the past year, 2021 marked the starting point of the capitalization upcycle for digital health.

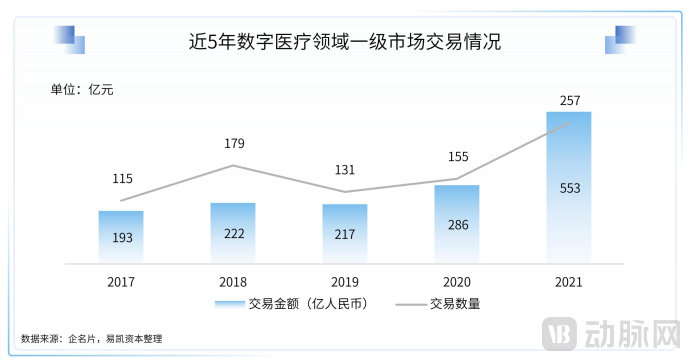

(1) Significant Surge in Primary Market Transaction Activity in the Digital Health Sector in 2021

Based on market transaction data from the past five years, the average transaction amount in 2021 nearly doubled compared to the preceding four-year average. In 2021, China’s digital health sector recorded 257 financing deals, with a total funding amount of RMB 55.3 billion, representing year-on-year increases of 66% and 93%, respectively. The average size per financing round was approximately RMB 200 million.

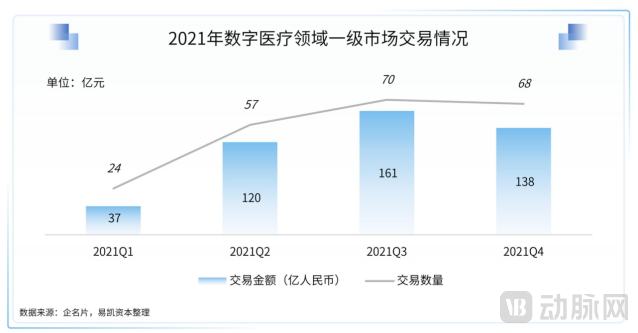

Quarterly, based on the timing of public relations announcements for financing events, the primary market for digital health has maintained strong momentum since the second quarter of 2021, with several large-scale financing deals occurring.

On the one hand, amid the pandemic, the contactless nature of remote digital healthcare and its system automation continued to play a significant role in addressing strained medical resources and avoiding crowd gatherings. This rapidly educated the user base, allowing the market to recognize the convenience and efficiency brought by healthcare digitization, thereby sustaining its utility in the post-pandemic era. On the other hand, the first wave of internet healthcare companies capitalized on the dividends of this market shift. After four to five years of development, by 2021 they had entered the mid-to-late stages, with their businesses nearing maturity. Naturally attracting strong investor interest, they drove the overall financing pace across the digital healthcare sector. Meanwhile, as some financing activities were delayed due to the pandemic, certain deals initially planned for 2020 were completed in 2021, indirectly contributing to the overall growth in financing that year. Finally, benefiting from the continuous development and upgrading of digital infrastructure—such as 5G, smartphones, medical data, and AI—the digital healthcare sector has entered a fast lane of accelerated growth, garnering increasing market attention and laying the foundation for its explosive expansion.

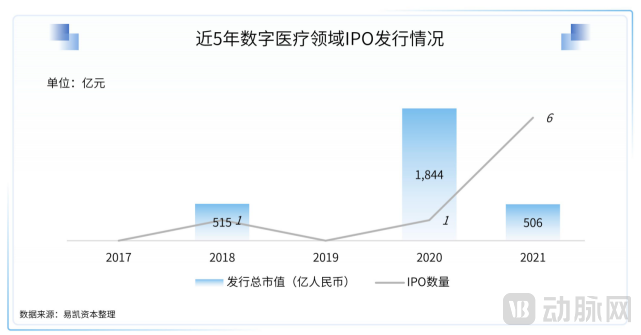

(2) Digital Health Sector Sees Leap in IPO Issuances in 2021

In 2021, six companies went public through initial public offerings (IPOs), with a combined issuance market capitalization reaching RMB 50.6 billion. The roster of IPOs in the digital health sector shifted from companies incubated by large platforms to independently market-oriented enterprises. This marks a validated pathway from the primary market to IPOs in the digital health sector, indicating on one hand that some companies in this field have matured and gained public recognition, and on the other hand providing venture capital funds with more certain expectations for market exit routes.

In terms of stock price performance, influenced by the overall cycle of the secondary market, the digital healthcare sector saw varying degrees of correction in the four companies listed on the Hong Kong Stock Exchange as of December 31, 2021, while the one company listed on the A-share market demonstrated a counter-trend rise. This situation will also have a certain impact on future IPO planning for companies.

3) In 2021, the number of IPO filings in the digital health sector experienced an explosive surge

In addition to the six companies that successfully went public, the number of digital health firms filing for initial public offerings (IPOs) in 2021 far exceeded the total from all previous years combined. A total of 12 companies submitted IPO filings, with 10 choosing the Hong Kong Stock Exchange, one opting for the U.S. stock market, and one listing on the STAR Market of China’s A-shares. This trend indicates that the first wave of companies in the digital health sector is gradually maturing and actively pursuing IPOs.

2. Digital Healthcare Is Gradually Evolving from “Internet + Healthcare” to “Healthcare Digitalization”

Most companies in China’s digital healthcare sector remain in the early to mid-stages, with the overall industry continuously maturing. While the competitive landscape in certain segments has gradually become clear, leading-tier companies are taking the lead in pursuing initial public offerings (IPOs). The year-on-year increase in the proportion of projects at Series D to Pre-IPO stages further underscores that the digital healthcare sector has transitioned from early-stage exploration onto a fast track toward maturity.

In the field of digital health, a cohort of companies founded and rapidly growing around 2015 became the first wave of digital health firms integrating the internet with healthcare. Typified by pharmaceutical e-commerce, these companies were the earliest to reap the dividends brought about by market shifts, while also sharing common characteristics:Leveraging internet technology as its foundation to enhance the efficiency of out-of-hospital processes, with the business model ultimately monetizing through “pharmaceuticals.”, achieving rapid growth in commercial revenue and subsequently going public or filing for IPOs within a few years. As pioneers of digital health, this wave of companies successfully brought the sector into the public spotlight and ignited an investment boom in the digital health field.

Since around 2019, market understanding of the first wave of digital health has continuously evolved. Further catalyzed by the subsequent pandemic, the second wave of digital health companies has garnered significant capital appreciation, gradually shifting toward “healthcare digitalization.” Typical representatives include AI-based medical imaging and departmental/clinical digitalization. These companies have moved away from the aggressive, high-profile “Internet Plus” approach, instead focusing more on the core essence of healthcare.Digitalization enhances the efficiency of in-hospital diagnosis and treatment processes. Payers are shifting their focus toward pharmaceutical companies or hospitals, while monetization models can be realized through services, software, or specific products.. Some of these companies have reached the mid-stage of development, beginning to demonstrate potential and trends in the scale of commercial revenue, and have become the backbone of the current digital health sector.

Over the past two years, numerous companies have continued to emerge in the market, further solidifying the essence of “medical digitalization.” Digital therapeutics (DTx), as a typical representative, delves deeper into the core of healthcare through digital means, supplementing or replacing traditional medical approaches to diversify treatment options and bring hope for symptom relief to patients. These companies are still in the early stages of development, and we look forward to their future progress.

(II) The Pandemic Has Catalyzed a Fundamental Transformation in the Digital Healthcare Industry

Digital healthcare has played a significant role in various scenarios to effectively support the prevention and control of the COVID-19 pandemic. An era represented by digital healthcare has quietly arrived with the normalization of the epidemic. The COVID-19 outbreak has greatly accelerated the development of digital healthcare within a short period and, to some extent, reshaped the regional landscape of the pharmaceutical and health industries.

1. Internet Healthcare

Over the past few years, relentless exploration within the industry has led to a flourishing of internet healthcare models, giving rise to diverse business formats such as digital health, health consulting, and pharmaceutical e-commerce. However, many of these services have remained on the periphery of core medical care. The first golden era of Chinese internet healthcare briefly faded from the spotlight of capital markets following the IPOs of numerous pharmaceutical e-commerce companies. Spurred by the pandemic, the internet healthcare sector has experienced a resurgence in investor interest, emerging as a valuable asset capable of addressing practical challenges in medical consultation and treatment. Influenced by COVID-19, the government has encouraged residents to seek online medical consultations to reduce physical gatherings. In 2021, user bases across all segments of internet healthcare platforms expanded, with the total number of users increasing by approximately 15 million. Among these, appointment and consultation platforms saw the largest absolute growth in users, adding around 5.7 million, while pharmaceutical e-commerce platforms recorded the highest growth rate at 38.5%.

However, digital healthcare still faces significant challenges. The ultimate indicator of qualitative transformation in service models and quality lies in how to integrate underlying digital capabilities with institutional innovation, streamline health insurance payment mechanisms, establish a closed-loop system for “pharmaceuticals and medical services,” and achieve synergistic coordination among these three elements within the institutional framework.

2. Hospital Digitalization

Amid the pandemic, digital transformation has profoundly impacted hospital service systems, with traditional film-based imaging diagnostics upgraded to digital films. During the COVID-19 outbreak, AI healthcare companies have developed an “AI + CT” model for medical imaging diagnosis. This approach helps reduce misdiagnoses and missed diagnoses, assists primary healthcare institutions in identifying infected individuals, serves as an effective tool for determining clinical cases of COVID-19, and buys critical time for the rapid isolation, diagnosis, and treatment of patients. AI-assisted imaging diagnosis is currently the most mature application area in AI healthcare and is poised for significant growth under the new normal of pandemic control.

3. Telemedicine

5G remote transmission technology has broken through the spatial limitations of medical resources and doctor-patient interactions, facilitating more efficient communication and exchange among healthcare providers. Currently, hospitals in Wuhan are interconnected via 5G technology, with the West Campus of Wuhan Union Hospital successfully establishing connections with Beijing Chaoyang Hospital and Beijing Friendship Hospital. In addition to remote consultations between Beijing and Hubei Province, regions such as Sichuan, Chongqing, Zhejiang, and Jiangsu have also leveraged 5G-enabled diagnostics and treatment during the pandemic, achieving comprehensive, barrier-free remote mobile consultations. The deployment of 5G network coverage in hospitals will be prioritized, accelerating innovative applications of 5G across a broader range of medical scenarios.

(3) Regulatory Policy Guidance to Promote Supply-Side Reform in Healthcare

2021 was a year of dramatic shifts in the policy landscape. The government introduced robust policies to strengthen industry regulation, targeting the primary payers in the digital healthcare sector: hospitals, pharmaceutical companies, and insurers. These policies were fundamentally guided by compliance and legality. Initiatives such as the full-process digital traceability of pharmaceuticals for drug manufacturers, and hospital informatization reforms led by the comprehensive coverage of electronic medical records (EMR) in all tertiary hospitals, established a compliance-driven foundation for digital transformation across the industry. Beyond compliance requirements, and in response to increasingly constrained basic medical insurance payments, regulatory policies have fully encouraged the development of a secondary payment platform dominated by commercial health insurance, designed to complement basic medical insurance effectively.

The development of industries related to digital healthcare is closely intertwined with policy; in certain sectors, policy serves as the core driver propelling industrial growth. For pharmaceutical companies, policies such as volume-based procurement and the consistency evaluation of generic drugs have fundamentally altered their profit models. Consequently, rather than increasing investment in sales and marketing, the paramount priority—akin to a corporate lifeline—has become controlling R&D, production, and manufacturing costs, while significantly enhancing efficiency in critical operations to ensure survival in a highly competitive market. For hospitals, the central theme in the second phase of healthcare informatization reform is how to meet the demands of this wave of change while leveraging digital tools to improve both management standards and clinical care quality.

1. Pharmaceutical Companies: The "Major Test" of Informatization Is Imminent; Regulatory Drivers Are Propelling All Types of Pharmaceutical Enterprises Fully into the "Era of Digital Governance"

Following the implementation of the Drug Administration Law of the People’s Republic of China and the Vaccine Administration Law of the People’s Republic of China, the National Medical Products Administration (NMPA) revised the Appendix on Biological Products in accordance with Article 310 of the Good Manufacturing Practice for Drugs (2010 Revision). This appendix was issued on April 23, 2020, as a supporting document to the Good Manufacturing Practice for Drugs (2010 Revision), and came into effect on July 1, 2020. With regard to Article 59 of the Appendix, enterprises that use information systems with real-time data acquisition for record-keeping were granted a transition period due to the time required for IT infrastructure development; they were required to meet the relevant requirements by July 1, 2022. For pharmaceutical companies specializing in biological products, 2021 marked the inaugural year for building such information systems, with the major assessment of IT infrastructure readiness approaching rapidly in July 2022.

The release of this revised appendix has imposed new requirements on the informatization of Chinese pharmaceutical enterprises, while also presenting fresh challenges and opportunities for China’s biologics industry, represented by vaccines. Prior to 2021, regulatory policies primarily focused on the drug distribution sector, yielding initial results in overseeing sales and procurement activities. As supervision over the distribution channel continues to improve, regulatory attention has increasingly shifted toward R&D traceability and production safety within pharmaceutical companies.

With the advent of the era of digitalized production, first, the primary medium for production records will change. Production lines and systems will need not only to collect real-time data through information technology but also to archive such data in electronic form, thereby creating reliable electronic batch records. Second, production informatization poses greater challenges to the management of manufacturing processes. In the past, due to the lagging level of informatization in pharmaceutical enterprises, real-time recording of production processes relied mainly on manual transcription, which raised concerns regarding data credibility, data security, and compliance, thus significantly affecting the quality of pharmaceutical production. This issue will be improved or even resolved with the application of continuous monitoring technologies, thereby prompting enterprises to continuously enhance their process management capabilities. Finally, production informatization challenges the quality management of pharmaceutical enterprises. New informatization systems and electronic record requirements will change the way quality events are communicated in production and testing operations: whereas previously communication relied solely on the transfer of paper records and verbal exchanges, there is now the business flow push functionality of informatization systems. To address this, enterprises need to establish new pathways for managing and handling quality events and ensure effective interaction of quality event data across multiple informatization systems, thereby guaranteeing timely recording and resolution of quality events during vaccine production and testing.

As the “top performers” in their sector, biological products will be the first to face the challenges of information technology (IT) infrastructure development. We believe that with the continuous improvement of regulatory mechanisms, production digitalization will become an imperative for pharmaceutical companies across more product categories. However, “Rome was not built in a day.” For manufacturing departments, particularly those in vaccine companies, implementing and testing new systems or upgrading existing systems, processes, and control measures, as well as coordinating relationships among functional departments such as quality assurance, quality control laboratories, and information technology, will entail a substantial workload. Meanwhile, for regulatory bodies overseeing quality compliance, strengthening the regulatory framework will also facilitate the standardized upgrading of the industry.

2. Hospitals: From Individual Products to Comprehensive Data Interconnectivity, Policy Guidance Drives the Construction of Fully Smart Hospitals

Since the official launch of the Hospital Smart Service Grading Assessment in August 2019, the National Health Commission has required hospitals across 31 provinces and municipalities to submit assessment data in phases. Hospitals in various regions have responded actively by advancing the development of smart hospital services. Furthermore, on September 17, 2021, the Bureau of Medical Administration and Hospital Management under the National Health Commission issued the Notice on Conducting the 2021 Hospital Smart Service Grading Assessment and Smart Management Self-Assessment. The Notice stated that it would comprehensively assess secondary-level and above hospitals that utilize information systems to deliver smart services and implement smart management, and assign grades for both hospital smart services and smart management.

In recent years, the National Health Commission of China has continuously refined its evaluation system for smart hospitals, with the core objective of guiding and directing medical institutions to comprehensively transition from informatization to intelligent upgrading. The national evaluation framework for “smart hospitals” comprises three major components: first, an assessment of the level of clinical informatization in hospitals, represented by the Electronic Medical Record (EMR) System Analysis and Evaluation Standards, which establishes a graded classification of EMR system application levels (revised in December 2018); this evaluation system covers all clinical information systems within hospitals. Second, a graded evaluation of patient services, namely the Hospital Smart Service Graded Assessment Standard System (released in March 2019). Third, a graded classification of smart hospital management, which evaluates and grades the level of managerial informatization in hospitals (draft released in August 2019). From the continuous evolution of these policies, it is evident that the smart hospital evaluation system has been refined into a three-pronged assessment and grading framework targeting smart services, smart medical care, and smart management. In fact, the rating results are directly linked to the performance appraisal of public hospitals, thereby compelling hospitals to place genuine emphasis on informatization development.

Currently, the information systems in most hospitals have entered a replacement phase, and traditional standalone IT modules will face significant challenges due to business upgrades. Furthermore, how hospitals leverage innovative digital tools to provide smart services to patients will become a critical pathway for their transition from informatization to intelligentization.

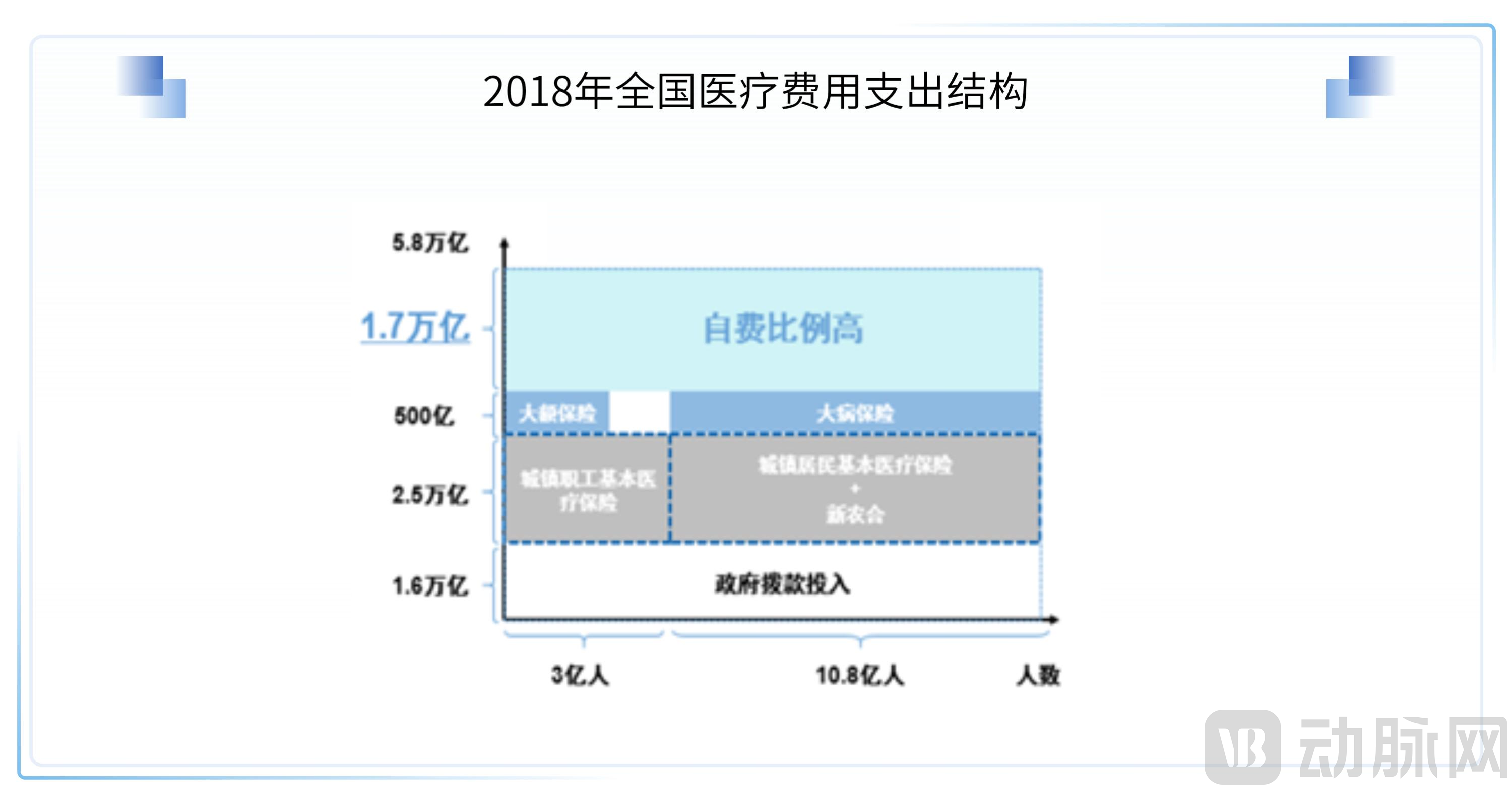

3. Payment: The CBIRC vigorously promotes industrial innovation and exploration; the next phase of health insurance still awaits a breakthrough following the era of million-yuan medical insurance

On January 16, 2022, the China Banking and Insurance Regulatory Commission (CBIRC) issued the “Report on Issues and Recommendations for the Development of Commercial Health Insurance in China” to life and health insurance companies. The Report pointed out that commercial health insurance has played a positive role in supporting the Healthy China initiative, facilitating the construction of a multi-tiered medical security system, and promoting the development of the health industry. However, it also acknowledged that China’s commercial health insurance sector remains in its early stages of development, with significant shortcomings in product supply and claims services. Major issues include inadequate risk protection capabilities, low levels of specialized operational expertise, and elevated business risks.

Since 2015, when a wave of insurers led by ZhongAn and Taikang rushed to launch innovative million-yuan medical insurance products, the health insurance industry has experienced six years of ups and downs. As the coverage of these policies reached a certain scale, their growth momentum has begun to wane, revealing signs of “waning stamina.” This trend is driven by multiple internal and external factors, including sluggish insurance consumption amid the pandemic, competition from city-specific supplementary medical insurance (Huiminbao), and product homogenization. Furthermore, due to the relatively extensive management practices of some market participants, issues such as misleading marketing, distorted product design, and unreasonable coverage terms have become increasingly prominent, leading to strict regulatory rectification and standardization.

The health insurance sector, encompassing policy and regulations, major insurers, and social medical resources, presents a complex commercial and social challenge. Designing relevant products and aligning supporting services constitute significant difficulties. The Report indicates that, in terms of risk coverage, commercial health insurance products suffer from severe homogenization. There is limited supply of mid-to-high-end medical services, and the coverage of certain popular products overlaps substantially with that of basic medical insurance, failing to provide an effective supplement. From an operational perspective, the level of specialized management in commercial health insurance remains low, with insufficient integration with health management and inadequate synergy with the broader health industry.

In January 2021, the China Banking and Insurance Regulatory Commission (CBIRC) issued the Notice on Regulating Issues Related to Short-Term Health Insurance Business. The Notice, comprising 13 articles, standardizes the operational and management practices of short-term health insurance from aspects including product design, renewal, sales, claims settlement, and discontinuation. It explicitly stipulates that short-term health insurance policies shall not guarantee renewability, strictly prohibits marketing short-term health insurance as long-term health insurance, requires insurance companies to disclose the overall loss ratio of their short-term health insurance business every six months, and strictly forbids the arbitrary discontinuation of short-term health insurance products.

In fact, since the implementation of new regulations on short-term health insurance, many insurance institutions have begun to explore and launch long-term versions of million-yuan medical insurance products. This move aims to establish differentiated competition with Huimin Bao (city-specific supplemental medical insurance) by highlighting the advantages and capabilities of long-term coverage. Notably, in addition to optimizing renewal terms, many million-yuan medical insurance policies are focusing on differentiated offerings in terms of coverage responsibilities, starting to address the healthcare protection needs of the mid-to-high-end market. In the future, to further enhance product competitiveness, insurers will continue to upgrade and innovate in value-added services, such as providing green channels for medical treatment, advance payment for medical expenses, and assistance in securing appointments with specialist physicians.

In the long term, the implementation of insurance products for non-standard and pre-existing condition populations will serve as a significant source of incremental growth and supplementation for the health insurance market. Data service companies that predict mortality and morbidity risks for specific populations, and based on these predictions provide product pricing for insurers and reinsurers, while also delivering risk control systems and refining risk management rules for these special groups, will become a key pillar of growth.

(IV) The Impact of Frontier Technologies on the Industry

1. Continuous Advancement of AI in Drug Discovery and Development

As an emerging interdisciplinary field that has gained prominence over the past three years, AI-driven drug discovery has attracted rapid capital deployment and significant attention against the backdrop of robust global growth in innovative pharmaceuticals. Global R&D investment in new drugs continues to grow steadily, with an annual growth rate projected to remain at 4%–5% over the next five years. In China, policy measures such as centralized volume-based procurement and national reimbursement negotiations have prompted pharmaceutical companies to accelerate their transition toward innovative drugs. Consequently, the proportion of Class 1 new drug applications has risen substantially, while leading pharmaceutical enterprises continue to increase their marginal investments in new drug R&D.

From 2018 to 2021, according to incomplete statistics, there were approximately 54 financing events in the AI-driven drug R&D sector across China, involving 190 participating institutions (including venture capital firms, funds, and industrial capital), with a total cumulative financing amount of nearly RMB 13 billion. The years 2020 and 2021 marked a significant turning point for China’s AI drug discovery industry, witnessing a doubling in both the number of financed projects and the overall financing volume. During this period, most AI drug development companies successfully transitioned rapidly from the startup stage to the growth stage, amid surging investor interest.

In terms of business models, China's AI-driven drug discovery industry remains in the validation phase, primarily encompassing:

1) AI-SaaS providers primarily offering software platform services: Delivering state-of-the-art computational software tools and leveraging extensive collaborations to accumulate larger datasets for algorithm iteration.;

2) AI-Biotech companies primarily focused on developing internal R&D pipelines: These companies mainly leverage AI to advance their proprietary pipelines, thereby accelerating the validation of their algorithmic platforms, and periodically license out maturing pipeline assets.;

3) AI-CRO companies that provide outsourcing services to pharmaceutical companies, CROs, and other drug R&D firms: They collaborate with numerous external enterprises to jointly advance pipeline development, charging fees and sharing revenues based on milestones, thereby sharing the risks of drug failure while enjoying the benefits of successful drug launches.。

In terms of financing, capital in the industry is highly concentrated. In 2020, XtalPi secured over $300 million in funding, accounting for 70% of the total financing in China’s AI-driven drug discovery sector that year. In 2021, XtalPi completed its Series D round, raising $400 million—approximately 60% of the total AI drug R&D financing for the year—and achieving a valuation exceeding RMB 13 billion, thereby solidifying its status as a domestic industry unicorn. Other AI drug R&D companies, such as StarPharm and WisdomRock, have also successfully completed their Series B+ financing rounds. The rapid fundraising by leading companies has fueled capital enthusiasm and driven industry upgrades, prompting the emergence of more AI drug discovery startups within this niche segment. Currently, the sector remains in its early stages of development, with momentum expected to gradually shift toward the mid-to-late stages in the future.

2. Medical Robots Reach a Critical Juncture for Clinical Validation

In 2018, there were over 100 financing deals in the medical robotics sector alone, making it a hot spot for capital investment since then and maintaining its popularity to this day. From prototypes and concept machines at that time to varying clinical progress four years later, we have observed that many medical robotics companies (especially those focused on surgical robots) failed to reach a satisfactory stage of development. Many companies faced issues such as product instability and unsatisfactory clinical trial results. How to finalize concepts and truly manufacture stable medical robotic products that meet clinical needs remains a challenging question. The technical challenges of integrating hardware and software behind surgical robots test every startup team, while the vast gap between promising prospects and practical difficulties tests every investor and investment institution involved.

From the perspective of industry investment and financing, the investment enthusiasm in China's medical robotics sector showed a trend of first increasing and then decreasing from 2019 to 2022. Investment activity was relatively high in 2018, while it cooled down somewhat in 2022.

Medical robots widely recognized by the majority remain concentrated in surgical and rehabilitation robotics. Due to their direct involvement in surgical procedures, surgical robots demand exceptionally high levels of accuracy and precision, making them the most challenging category to manufacture. They are typically applied in orthopedic, abdominal, and other surgeries, helping to reduce postoperative pain and enhance operational precision. These medical robots can simulate surgical procedures and replace healthcare professionals in performing tasks that may cause harm to the human body. With advantages such as minimal error, high safety, and absence of physiological fatigue, they help reduce labor costs, assist healthcare workers, provide precise surgical services, and shorten postoperative recovery time.

Although the development prospects of medical robots are generally viewed favorably, and systemic investment opportunities in the medical robot industry are widely considered promising by capital markets, the contradiction between installation rates and utilization rates persists across the sector. Underutilization remains a significant challenge facing the entire medical robotics industry.

Although medical robotics face numerous challenges, some companies have successfully navigated these difficulties to establish leading positions in the industry. These enterprises have finalized their product designs, achieved satisfactory interim results from clinical trials, and garnered substantial support from industry experts. As healthcare reforms deepen and the pandemic induces profound industry transformations, medical robots remain essential tools for hospitals in the post-pandemic era. The implementation of volume-based procurement (VBP) policies has exceeded expectations; with high-value consumables for major conditions such as orthopedics and cardiovascular diseases included in VBP programs, the traditional hospital revenue model reliant on consumable sales will be fundamentally reshaped. Consequently, the proportions of drug and consumable revenues will decline significantly, creating an urgent need for hospitals to identify new revenue centers. Innovative medical services enabled by innovative medical devices, led by robotic systems, have continuously enhanced their efficacy and functionality through clinical accumulation in recent years. From the listing of Tinavi Medical Technologies to the spin-off of MicroPort MedBot, the capital market has demonstrated ample confidence and support for China’s medical technology innovations.

We believe that innovative medical services, represented by medical robots, will become the core hallmark and revenue center for hospitals. The adoption of innovative products will increasingly differentiate hospitals from one another. Patients are also more inclined to seek care at medical institutions equipped with innovative service capabilities. As pricing items for innovative medical services continue to be established, the procurement of innovative medical devices will significantly stimulate innovation within China’s medical device industry, driving its gradual transition from catch-up growth to global leadership in innovation.

3. Extended Reality Is Gaining Momentum

Video immersive technologies such as VR (Virtual Reality), AR (Augmented Reality), and MR (Mixed Reality) are collectively referred to as Extended Reality, or “XR.” XR is poised to further transform medicine.

Among these technologies, VR is the most mature, having been applied across various aspects of healthcare with remarkable success. Over the past few decades, scientists have gradually discovered the therapeutic effects of VR in ophthalmology and neuropsychiatry. As a significant complement to traditional pharmaceuticals, medical devices, and surgical procedures, VR has been increasingly utilized in disease treatment and clinical assistance scenarios. AR technology overlays virtual information onto real-world environments; for instance, by projecting holographic organs onto anatomical models to aid navigation, it provides clinicians with “X-ray vision” during clinical surgeries. MR technology offers surgeons the convenience of directly viewing patients’ computed tomography (CT) and magnetic resonance imaging (MRI) scans in 3D format. This helps surgeons identify specific anatomical structures relevant to the planned procedure, thereby facilitating more effective surgical outcomes. Additionally, smart glasses can record simulated surgeries and provide trainees with real-time vital signs data.

Currently, the application of XR in medical scenarios in China is still in its early stages. At present, the market penetration rate of XR remains significantly lower than that of other electronic devices. User education and market acceptance require long-term cultivation, while the technological maturity of the upstream and downstream supply chains and pricing factors are also key determinants influencing the large-scale adoption of XR.

We believe that XR will gradually permeate all aspects of the healthcare sector, delivering unprecedented user experiences and innovative diagnostic and therapeutic pathways. Based on value orientation and commercial feasibility across various scenarios, this integration can be broadly categorized into three tiers.The preferred approach is (1) XR+ disease treatment, such as vision impairment therapy (amblyopia, strabismus, myopia, presbyopia, etc.) and neuropsychiatric/mental health applications (autism spectrum disorder, attention deficit, Alzheimer's disease, depression, anxiety, etc.).Second is (2) XR + Clinical Assistance, such as sedation and analgesia (replacing the use of fentanyl/midazolam in scenarios like cancer pain, labor pain, surgical pain, and post-traumatic stress disorder) and surgical visualization systems (providing anatomical structures and intraoperative navigation). Then comes (3) XR + Rehabilitation Training, including 3D simulated limb training, cognitive function training, fitness scenarios & datafication, and virtual coaches;(4) XR+ Medical Education and Training, including panoramic video instruction and surgical simulation training; (5) XR+ Medical Nursing, such as urinary catheterization simulation, postoperative stoma care simulation for breast and colorectal cancer, perioperative pressure ulcer management, and cardiopulmonary resuscitation (CPR) simulation.

4. Early Signs of Digital Twins Emerge

Digital Twin is a virtual entity created digitally to represent a physical entity. It is a technological approach that leverages historical data, real-time data, and algorithmic models to simulate, validate, predict, and control the entire lifecycle of the physical entity.

Digital twins have been applied in multiple fields due to their characteristics such as interoperability, scalability, real-time capability, fidelity, and closed-loop functionality. The primary application demands for digital twins in the healthcare sector are:

1) For government: Enhance the coverage and efficiency of urban diagnosis and treatment, and promote the rational allocation of urban medical resources through intelligent technologies such as mobile monitoring, mobile clinics, wireless remote consultations, smart prescriptions, and cloud storage of medical information;

2) For pharmaceutical companies: Digital simulation of “virtual patients” may shorten the time required for new drugs to progress from the design phase to general availability and improve success rates;

3) Patient-Oriented: By leveraging patient health records, medical history, medication history, and monitoring data from smart wearable devices, a “medical digital twin” can be established for each patient in the cloud. Supported by technologies such as biochips, augmented analytics, edge computing, and artificial intelligence, this digital twin simulates human physiological processes to enable predictive analysis of individual health status and precise medical diagnosis.

Of course, digital twins still face numerous challenges in practical applications. The first challenge lies in data and security: for instance, ensuring consistency in multi-dimensional, multi-scale data acquisition; the inability to guarantee the stability and accuracy of data transmission; and deficiencies in processing efficiency and secure storage capabilities for massive datasets. The second challenge pertains to business models: such as insufficient application value, poor compatibility, and unclear profitability models. Additionally, there are challenges in the integration and interoperability of multiple systems: including data ambiguity, unclear data correlations, the need for improved data availability and quality, difficulties in fusing multi-source heterogeneous data, lack of uniformity in communication interface protocols and related data standards, and imperfect mechanisms for data sharing and openness.

We believe that the applications of digital twins with significant commercial potential in the healthcare sector will first be realized on the pharmaceutical company side and the patient side.

1) Digital Drug Trial Models: “Digital twins” of human organs and systems are becoming increasingly realistic, providing the theoretical and technical foundation for pharmaceutical companies to explore disease mechanisms and conduct drug trials through digital drug trial models, thereby avoiding costly human or animal studies. Initiatives such as the U.S. “Living Heart” project and the EU’s “NeuroTwin” project have introduced new paradigms and scenarios for drug development. In the future, a growing number of open-source digital drug trial models will be developed, optimized, and utilized, potentially replacing animal or human trials altogether.

2) Precision Medicine: Leveraging medical digital twins, physicians can collect and analyze patients’ health big data—including genetic information, lifestyle habits, family medical history, and clinical records—to develop personalized and targeted treatment plans and medications, thereby achieving precise diagnosis and therapy.

3) Health Monitoring and Management: In the realm of personal health monitoring and management, digital twins enable a clearer understanding of physiological changes and provide timely warnings for diseases or behavioral anomalies (such as stroke or abnormal postures indicative of falls in the elderly).

5. Digital Therapeutics (DTx) Gradually Maturing

Digital therapeutics offer a novel therapeutic option beyond existing conventional pharmacological treatments, non-pharmacological interventions (such as surgery, radiation therapy, and physical therapy), and psychological and behavioral therapies. As software applications (Apps), digital therapeutics (DTx) primarily treat diseases by modifying patients’ lifestyles and behaviors, exerting effects equivalent or similar to those of conventional medications in disease treatment and prevention. They can also be used in combination with other drugs or medical devices to enhance therapeutic efficacy. DTx not only serves as a complement to traditional treatments but also pioneers an entirely new therapeutic modality. Therefore, DTx can be regarded as “digital drugs,” which are essentially special “medicines” subject to stringent regulation comparable to that for conventional pharmaceuticals and medical devices, albeit delivered in the form of software applications. A defining feature of DTx is that its clinical safety and efficacy are substantiated by clinical evidence, and it has obtained certification and approval from regulatory authorities.

2021 marked the breakout of the “digital therapeutics” (DTx) concept. According to publicly available data, 59 DTx projects in China completed 127 transactions in 2021, with participation from 180 investment institutions and cumulative financing nearing RMB 4.3 billion. Financing activity was skewed toward early-stage investments, gradually gaining momentum in mid- to late-stage rounds. Based on relevant forecasts, the industry maintains a positive outlook on the future of DTx, with the overall market size expected to grow at a robust rate.

In certain sectors, where access to medical services is extremely limited and the breadth and depth of payer coverage are both weak, therapeutic digital therapeutics have been able to attract a substantial base of self-paying users. The purely essential self-pay segments primarily target the elderly and children, who demonstrate strong willingness and motivation to pay. Psychiatry, ophthalmology, and broader mental health are currently the key areas being explored for digital therapeutics. Digital therapeutics companies with core product pipelines focused on autism, Alzheimer’s disease, and pediatric strabismus and amblyopia received significant capital investment in 2021.

Of course, digital health has its inherent limitations. Self-paying users often exhibit high churn rates and low adherence, which may impose a ceiling on the addressable revenue scale for digital therapeutics (DTx) companies. In this context, leveraging new payers to expand revenue and achieving a comprehensive B2B2C transformation will be the primary direction for future exploration. Currently, China’s commercial insurance market remains relatively underdeveloped, and the standard medical insurance market has initially entered a "red ocean" stage of intense competition. Consequently, all health management and intervention-related services will become important customer acquisition tools for insurance capital, a trend that will substantially drive the development of digital therapeutics in the medium to long term. Furthermore, pharmaceutical companies are likely the most interested stakeholders in digital therapeutics. It is entirely possible for pharma companies to incorporate DTx services as adjunctive treatment plans for patients. However, whether pharmaceutical companies have sufficient profit margins to afford such procurement is difficult to generalize against the backdrop of centralized volume-based procurement.

We believe that digital therapeutics must satisfy three key characteristics to have the opportunity to develop a relatively mature and stable business model.First, digital therapeutics (DTx) target conditions for which there are no effective specific pharmacological treatments; thus, DTx will serve as a critical component of diagnostic and therapeutic regimens. Second, there must be an appropriate payer structure for the conditions addressed by DTx, with out-of-pocket payment driven by essential medical needs currently serving as the primary reimbursement mechanism. Third, DTx must demonstrate genuine clinical efficacy, validated through both clinical trials and real-world use cases. In 2022, the DTx sector—characterized by clear out-of-pocket payment models, proven efficacy, and validation—will continue to attract significant capital attention. Leading companies will rapidly widen their competitive advantage over peers through first-mover benefits while further refining their profitability models.

II. Key Transactions in the 2021 Market

(I) Major IPOs in the Digital Health Sector in 2021

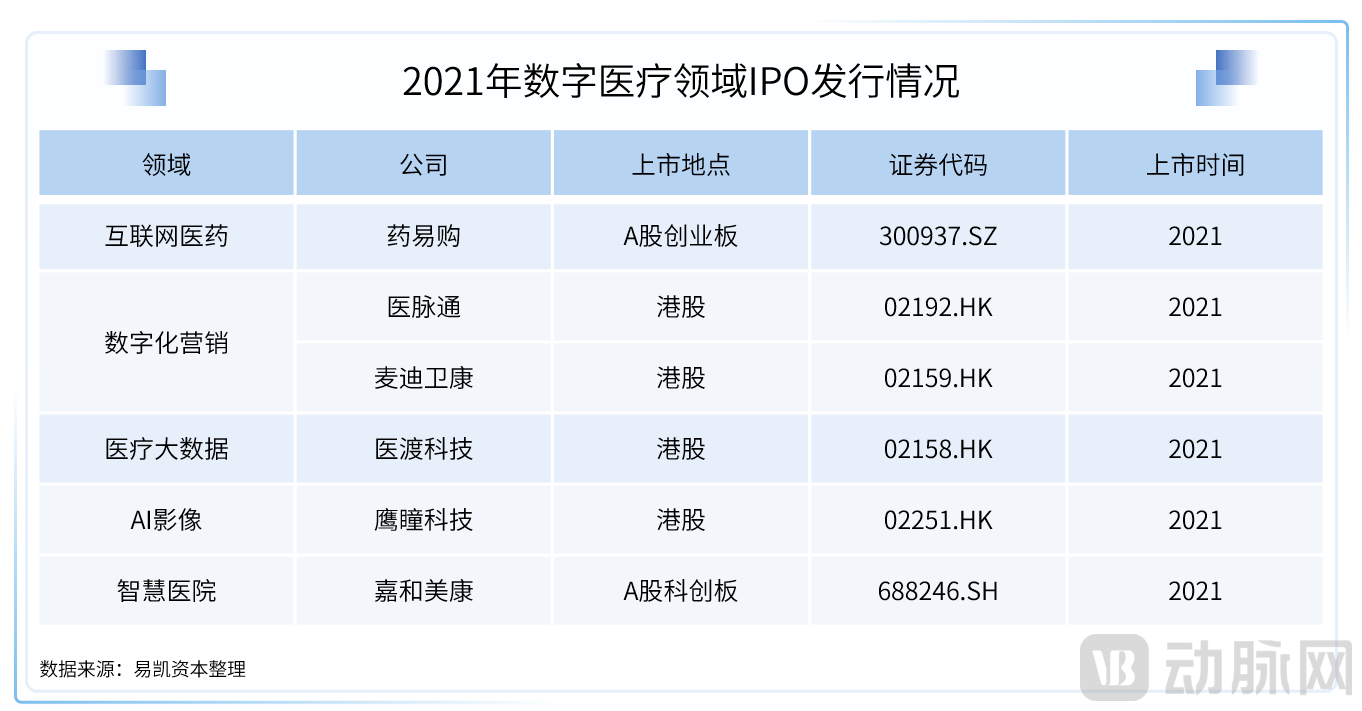

1. Medlive

Medlive Technology Co., Ltd. (Stock Code: 02192.HK) successfully listed on the Main Board of the Hong Kong stock market on July 15, 2021. The company offered 155 million shares at an issue price of HK$27.2 per share, raising net proceeds of approximately HK$4.001 billion.

Medlive is an internet-based physician platform company dedicated to precision education for doctors. While providing professional medical information and services to physicians, it also offers targeted promotional services for pharmaceuticals and medical devices to companies in these sectors. One of Medlive’s core platforms, the Medlive website, is among the largest physician platforms in China, serving over 2.4 million physician users with comprehensive resources including drug information, academic updates, and career development support.

The listing of Medlive marks the gradual maturation of industries related to pharmaceutical companies, which are emerging as core payers in the pharmaceutical sector. Amid the industry-wide push for cost reduction and efficiency enhancement, pharmaceutical companies, as core payers, demonstrate strong willingness and substantial capacity to pay across sales, clinical, and intelligent control domains. Consequently, business models targeting pharmaceutical companies are being increasingly validated and have gained support and recognition from the capital market.

Medlive’s successful listing has heightened capital market interest in the digitalization of pharmaceutical marketing. In 2021, multiple pharmaceutical companies’ digital marketing arms sequentially completed growth-stage financing, marking a new phase in their business development. Against the backdrop of cost reduction and efficiency enhancement in the pharmaceutical industry following healthcare reforms, coupled with shifts in collaborative models among pharmaceutical enterprises in the post-pandemic “new normal,” digital marketing has rapidly unleashed significant market opportunities and potential.

In the future, pharmaceutical company-funded industries will expand rapidly. With policy support, the intelligent transformation of pharmaceutical companies will extend to core areas such as production, R&D, and clinical trials, becoming a key investment hotspot.

2. Airdoc

Airdoc Technology Inc. (stock code: 02251.HK) successfully listed on the Hong Kong Stock Exchange on November 5, 2021, marking the debut of the “first AI medical imaging stock.” Airdoc’s IPO price was HK$75.1 per share, with net proceeds from the Hong Kong listing amounting to HK$1.566 billion, and its market capitalization exceeded HK$7 billion.

Airdoc is one of the first companies in China to provide solutions for early detection, auxiliary diagnosis, and health risk assessment based on AI-powered retinal image recognition. By leveraging retinal imaging, multimodal data analysis, and deep learning algorithms, Airdoc enables non-invasive, accurate, rapid, effective, and scalable detection and diagnosis of chronic diseases for healthcare institutions and general health providers.

Since 2015, thanks to advancements in digital imaging and acquisition equipment, the availability of standardized medical data has become increasingly robust. The core competitive barrier of the industry has gradually shifted from initial data acquisition to innovation in algorithms and platforms. Although AI-driven segments such as digital eye, digital heart, digital liver, and digital brain have been progressively established and refined, and AI healthcare has developed rapidly, commercial competition has intensified accordingly, while commercial implementation remains a persistent challenge for these companies.

Fierce competition has propelled the emerging AI medical imaging industry into a consolidation phase ahead of schedule. From the current perspective, policy support and regulatory approval remain the two key enablers for the commercialization of AI enterprises’ products. Compared with 2020, supportive policies for AI have been successively introduced, and preliminary progress has been made in exploring reimbursement items for AI-based medical imaging services across various provinces and municipalities.

We believe that the AI medical imaging sector will continue to refine its focus around three key areas: “how to bring AI to more patients,” “how to address payment challenges,” and “how to effectively solve clinical problems.” From screening to diagnosis, and from diagnosis to population-wide screening, medical AI will deliver its core value to a broader population. Meanwhile, the dual drivers of approval and regulation are accelerating the reshuffling and upgrading of the AI medical imaging landscape. Only companies with truly robust products and viable business models will emerge as the ultimate leaders.

3. Yidu Tech

Yidu Tech (Stock Code: 02158.HK) successfully listed on the Hong Kong Stock Exchange on January 15, 2021. The global offering comprised approximately 156 million shares, with the offer price set at HK$26.3 per share, raising net proceeds of HK$3.9 billion. On its listing debut, Yidu Tech’s total market capitalization exceeded HK$58 billion, attracting significant attention from the capital markets.

Yidu Tech’s core product is its namesake platform, “Yidu Cloud,” which primarily provides healthcare solutions based on big data and artificial intelligence (AI) technologies to key stakeholders in the healthcare industry. The company delivers services to and collaborates with these major participants, including hospitals, pharmaceutical, biotechnology, and medical device companies, research institutions, insurance providers, physicians and patients, as well as regulatory authorities and policymakers.

As a next-generation provider of medical big data technology and artificial intelligence solutions, Yidu Tech has continuously iterated and upgraded its business model from the traditional single-sided approach serving hospitals and governments, expanding into digital CRO services for pharmaceutical companies and personal health management services. The success of this business transformation has garnered support from the capital market, while the innovative business segments have injected fresh growth momentum into Yidu Tech.

We believe that hospitals, medical communities, and medical alliances, as key stakeholders in the healthcare industry, urgently need to integrate and streamline their traditionally fragmented IT systems. The deep processing and analysis of large-scale, multi-source, heterogeneous medical data are critical, making the construction of next-generation digital intelligent cloud infrastructure a pivotal task. Against the backdrop of a promising long-term vision, the core challenge facing all stakeholders is how to systematically achieve the digital transformation of healthcare systems, represented by hospitals. On the path toward hospital digitalization, the era of traditional health IT vendors has come to an end, while competition among next-generation smart hospital product providers is just beginning. Product implementation and the development of flexible business models will become the focal points of competition in the hospital informatization market.

(II) Major Primary Market Transactions in the Digital Health Sector in 2021

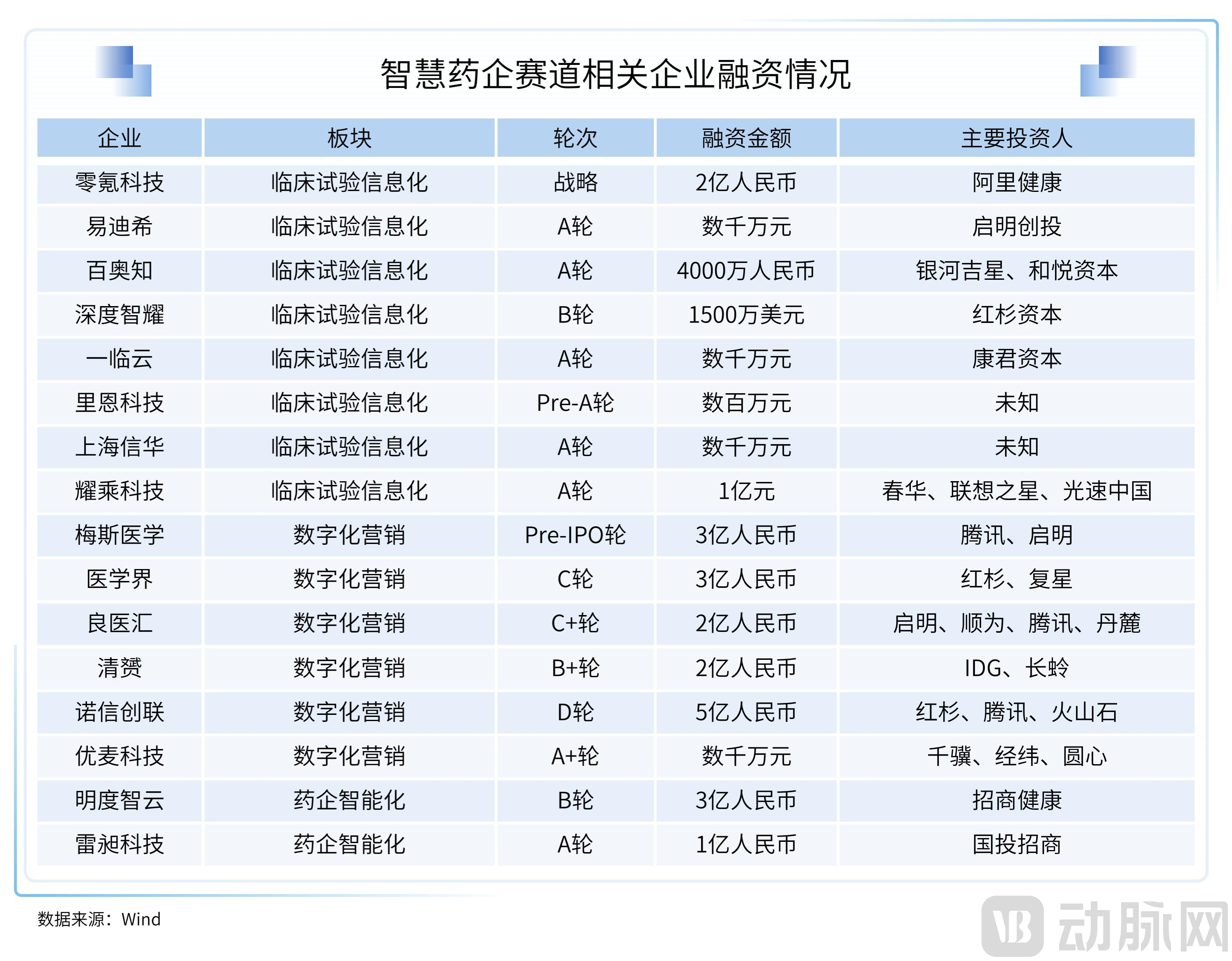

1. Yuanxin Technology

Yuanxin Technology is a comprehensive healthcare delivery platform focused on prescription drugs. Its current revenue is primarily driven by the sales of new and specialized drugs (i.e., innovative, highly complex, or high-diagnostic-and-treatment-demand medications), with a strategic presence in the pharmacy market adjacent to hospitals. This is complemented by the development of an online medical service platform to drive patient traffic to these hospital-adjacent pharmacies. The company has also made initial forays into the insurance business, positioning it as a key direction for future expansion. Under its umbrella, the internet healthcare brand Miaoshou Doctor operates as a nationwide professional online platform for follow-up consultations between doctors and patients, as well as a safe medication dispensing platform. By integrating segments such as Miaoshou Internet Hospital, the Miaoshou Doctor APP, DTP (Direct-to-Patient) chain pharmacies, and Yuanxin Huibao, the company leverages internet technology to create a closed-loop pharmaceutical service ecosystem encompassing “medical care, patients, pharmaceuticals, and insurance.”

Amid the broader trend of China’s healthcare reform to separate pharmaceutical prescribing from dispensing, Miaoshou Doctor, which had previously explored areas such as patient registration and consultations, was among the first companies to recognize the direction of healthcare policy changes and successfully establish a presence in the out-of-hospital pharmacy sector, pioneering China’s earliest DTP (Direct-to-Patient) pharmacy business model. The success of Yuanxin has truly broken new ground in integrating internet-based healthcare with pharmaceutical sales, establishing it as a viable and practical business model.

2. Mingdu Zhiyun

Mingdu Zhiyun is a high-tech enterprise dedicated to the comprehensive digital transformation of the life sciences sector. It provides pharmaceutical companies with full-lifecycle solutions spanning from R&D to production, helping them enhance R&D efficiency, ensure compliant and stable manufacturing, establish end-to-end traceability systems for smart pharmaceutical operations, and elevate their digitalization and intelligence capabilities, thereby contributing to the healthy development of the industry.

Mingdu Zhiyun is a leading vertical industrial internet platform in China, specifically tailored for the pharmaceutical manufacturing sector. Its forward-looking digital platforms for R&D, production, and logistics have become powerful tools accelerating the development of China’s pharmaceutical industry. Amidst the wave of healthcare reform and upgrading in China, Mingdu leverages its deep industry insights to assist Chinese pharmaceutical companies in gradually modernizing and upgrading their operations, thereby facilitating the comprehensive digital transformation of China’s pharmaceutical manufacturing sector.

3. Senyi Intelligence

Senyi Intelligence is a provider of comprehensive solutions for smart hospitals in China. The company specializes in delivering professional and efficient digital and intelligent infrastructure solutions for hospitals, including intelligent clinical research, disease management platforms, lean clinical management, data governance, data integration, and real-world studies.

Against the backdrop of the 14th Five-Year Plan, hospitals are rapidly transitioning from informatization to an era characterized by datafication and intelligence. The future high-quality development of public hospitals will undoubtedly center on information technology infrastructure, refined management, and more precise medical care, all of which require deep integration of artificial intelligence. Data is paramount; it serves as the core component of informatization initiatives. Data quality is critical to the research and application of key data models and artificial intelligence. A new wave of smart hospital service providers, led by Senyi Intelligence, is progressively enhancing the digital and intelligent capabilities of hospitals. In the future, these providers will better empower the high-quality development of public hospitals.

4. Fourier Intelligence

Fourier Intelligence is a high-tech enterprise that leverages its independently developed core rehabilitation robotics technology as a foundational platform to provide globally leading, comprehensive intelligent rehabilitation solutions for medical institutions and patients worldwide.

Intelligent rehabilitation is a critical solution to address the current shortages of resources and manpower in the rehabilitation sector, and it will serve as a core strategy for coping with an aging society in the future. As a pioneer in the rehabilitation robotics industry, Fourier Intelligence boasts a portfolio of rehabilitation robots that feature leading-edge technology, complementary functionalities, and interconnected data systems. Its successful financing round in 2021 has drawn significant capital attention to the field of intelligent rehabilitation robotics, laying a solid foundation for the development of China’s intelligent robotics enterprises. The advancement of intelligent rehabilitation will provide robust support for the implementation of the national tiered diagnosis and treatment system. In the future, home-based and community-based rehabilitation are poised to replace traditional rehabilitation models, extensively bringing rehabilitation services and concepts into every household.

5. Infervision

Infervision is an AI company specializing in AI-powered medical imaging interpretation, with comprehensive coverage of major diseases affecting multiple sites and organs, including the lungs, heart, brain, blood vessels, breasts, and bones and joints. It provides hospital clients with intelligent solutions spanning the entire healthcare workflow—screening, diagnosis, treatment, management, and research—with its products deployed in over 400 medical institutions across nearly 20 countries worldwide.

Infervision is among the first batch of AI medical imaging companies in China and has launched the country’s first FDA-cleared AI-assisted diagnostic product for lung diseases. The attention Infervision Medical has garnered in the capital market, along with its completion of Series D+ financing, undoubtedly represents a milestone in the AI diagnostics sector. However, the sector still broadly needs to address challenges related to business models and profitability. We believe that the AI medical imaging sector is entering the second half of its competitive landscape, where companies with genuine implementation capabilities and viable business models will still have opportunities to overtake their competitors.

6. Jianhai Technology

Jianhai Technology is a provider of cloud-based post-discharge follow-up services for patients. By deploying its cloud follow-up platform within hospitals, the company optimizes medical resources, assists physicians in managing patients outside the hospital setting, and supports pharmaceutical companies in delivering more precise and effective patient education and services.

Jianhai Technology specializes in the development and operational management of post-diagnosis disease management services. It is one of the few emerging modern enterprises in the industry capable of focusing on the post-hospital market to provide comprehensive, AI-driven whole-course disease management solutions. Post-diagnosis disease management and long-term care have always been critical components of case management. The Jianhai model has successfully transformed out-of-hospital patient management into a clinically effective, implementable, and sustainable business model. It addresses the multifaceted needs of patients, pharmaceutical companies, and hospitals, while enabling effective feedback of patient data. The company’s visionary mission—“Making Care a Potent Remedy”—has thus become a reality.

III. Key Investment Themes and Market Outlook for 2022

Reviewing the investment hotspots in the primary market and the overall performance of the secondary market in 2021, we believe that the keyword for investment this year is “rationality,” which encompasses several implications:

1. Rational reflection on needs analysis,Specifically, whether a sector represents genuine or pseudo-demand, the rigidity of such demand, and whether the market size and ceiling are sufficiently large;

Second, a rational approach to commercialization.Namely, whether the business model is theoretically viable and whether the team can practically execute it; whether stakeholders are genuinely willing to pay, as well as the magnitude and sustainability of their payments;

Third, rational reflection on regulation.Will today’s logic hold true tomorrow? Will current policies remain applicable in the future? Against the backdrop of healthcare cost containment and structural optimization (“swapping old for new”), what pathways offer sustainable long-term growth? In light of these fundamental considerations, we have conducted systematic analyses and in-depth comparisons to identify the most significant and promising investment themes and market forecasts for 2022, presented from the perspectives of supply, demand, and payment.

(I) Supply Side: The Trend of Domestic Substitution Persists, Digitalization Promotes Intensification, and Homogenization Drives Differentiation

1. AI Drug Discovery and Development: Enhancing Success Rates and Shortening Development Cycles

Currently, AI-driven drug discovery remains in its early stages, with varying degrees of penetration across all phases and aspects of the drug development process. It has seen extensive applications ranging from basic research to target identification, biochemical activity assessment, and clinical trials. Among these, target discovery and compound synthesis are the most representative areas and constitute the primary focus of artificial intelligence (AI) adoption in new drug development. Nevertheless, there is still significant room for improvement in current AI applications, requiring substantial breakthroughs both in methodologies and in their integration with the pharmaceutical industry.

Externally, with the 2015 reform of the drug review and approval system as a starting point, the state has encouraged the development of innovative drugs through various measures, including registration and approval, medical insurance reimbursement, market launch regulations, talent policies, and patent protection, thereby significantly compressing the value space for “me-too” innovative drugs and generics. Internally, the need for pharmaceutical companies to reduce costs and increase efficiency has become pronounced, with the low efficiency of traditional R&D driving both pharmaceutical enterprises and capital to rapidly embrace AI.

China’s AI-driven drug discovery sector has evolved from its nascent stage in 2014–2015, through a period of stagnation in 2016–2017, to the substantial boom witnessed in recent years. This trajectory reflects the industry’s gradual maturation, with an increasing number of companies establishing stable and sustainable business models through iterative exploration. In terms of specialized segments, most AI-powered drug R&D firms currently focus primarily on small molecules. However, as algorithmic models and R&D paradigms continue to innovate and evolve, AI applications are beginning to take hold in the fields of large molecules and RNA, attracting growing attention. Looking ahead, companies capable of truly breaking through the industry’s ceiling will need not only to achieve substantive progress in their operational development but also to adapt their business models in response to the dynamics of China’s drug R&D market. Only by doing so can they successfully overtake competitors on the curve and emerge as the next unicorns.

Candidate drugs developed through overseas AI-driven R&D have entered clinical trials. The public listings of AI computational drug discovery companies, represented by Schrödinger and Relay Therapeutics, along with the involvement of multiple multinational pharmaceutical companies and internet giants, have served as catalysts for the surging interest in this field. On the other hand, the pandemic has driven unprecedented attention from capital markets toward the biopharmaceutical industry. As a sector with immense market potential, AI-enabled drug discovery continues to attract significant investment.

Regarding the pace of financing, as more companies move past their startup and growth phases, overall funding in 2022 shifted toward later stages. However, due to the impact of XtalPi’s listing timeline and the valuations of AI-driven healthcare and pharmaceutical companies in the secondary market, capital will continue to pay attention to the sector. Nevertheless, the industry is becoming more rational, leading to a corresponding slowdown in the financing pace for AI drug discovery. This broader trend poses greater challenges to companies’ business progress and their ability to generate internal cash flow.

2. Smart Pharmaceutical Enterprises: Policy-Driven, in the Post-Pandemic Era, Pharmaceutical Companies Are Fully Embracing the “New Era of Digital Governance”

The digital economy occupies a pivotal position in national strategy, with digital innovation emerging as a new growth engine and driving force for the pharmaceutical industry. For a long time, Chinese pharmaceutical companies have lagged significantly in digital maturity. However, driven by the profound shifts in the industrial landscape brought about by the pandemic, coupled with the continuous implementation of digitalization policies, pharmaceutical enterprises are now comprehensively stepping into a new era of data governance, whether proactively or reactively.

Pharmaceutical companies are facing the most stringent digital regulatory environment in the post-pandemic era, with policies extending from distribution oversight upstream to core links such as production and R&D. In this era of strict regulation, pharmaceutical enterprises need digital tools to address compliance requirements and achieve comprehensive cost reduction and efficiency gains, thereby mitigating the significant impact on product sales caused by policies such as volume-based procurement and the consistency evaluation of generic drugs. In the post-pandemic era, pharmaceutical companies are confronted with the reconstruction and innovation of multi-party collaboration models, making digital tools a critical weapon for adapting to the new normal.

Digital transformation is an inevitable path for the survival and development of pharmaceutical companies. It significantly enhances their concurrent processing capabilities, enabling them to transition from a single-core era to a multi-core era. Digital innovation will become a new growth point and driver for the development of the pharmaceutical industry. In 2021, the digitalization and intelligentization of pharmaceutical companies developed rapidly. As a key link in China's pharmaceutical industry, the digital market driven by their own development needs has ushered in vigorous growth. Among these, digital marketing services, digital clinical services, and digital intelligent upgrades are the core tracks for smart pharmaceutical enterprises, with digitalization continuously driving the intelligent upgrade of the pharmaceutical manufacturing industry.

The three sectors with the strongest payment momentum in pharmaceutical companies, ranked by demand gradient, are marketing, clinical operations, and management. Among these, digital marketing and digital clinical trials have already undergone the first wave of development, with several leading enterprises emerging. With the most abundant funding available on the marketing and clinical trial sides, these areas will be the primary high-growth tracks. Furthermore, to meet the needs of refined management and enhance R&D and production efficiency, the production and R&D sectors will also become key areas of investment for pharmaceutical companies.

As the core payer, pharmaceutical companies’ strong payment capacity and willingness collectively determine that business models centered around them will exhibit greater feasibility and profitability. The commercial environment for industries where pharmaceutical companies serve as payers is more market-oriented compared to other B2B segments within the industry. Sub-sectors with pharmaceutical companies as the core payer are entering a phase of rapid growth and are expected to maintain high-speed expansion, given that the majority of demand remains unmet. Medlive’s successful listing in Hong Kong serves as a benchmark case for enterprises in this segment, thereby bolstering primary market investors’ confidence to strategically position themselves in the digitalization track targeting pharmaceutical companies.

We believe that the digital transformation of pharmaceutical companies will gradually shift from providing electronic tools to offering data middle-platform services. The core objective is to ensure the consistency and reusability of various types of data within pharmaceutical enterprises, thereby accumulating data assets and empowering their technological innovations in medical technology. Requirements for product suppliers in vertical sectors will become more diversified. In response to the distinct needs of pharmaceutical companies for data accumulation and application across different domains, specialized service providers will emerge to deliver targeted solutions. These suppliers will be required to possess strong professional expertise. Purely electronic tool systems will either be phased out or integrated by middle-platform providers, as the value delivered by standalone products will become extremely limited.

Meanwhile, there is a gradual transition from information governance to data application: As business operations deepen, service providers will increasingly leverage the data accumulated from their own operations and those of their clients to develop relevant applications, thereby feeding back into and empowering the pharmaceutical industry itself.

3. Smart Hospitals: At the Crossroads of Product Strength and Business Models

After more than two decades of health information system development, most hospitals operate multiple disparate systems that manage data and information across different dimensions, such as Hospital Information Systems (HIS), Picture Archiving and Communication Systems (PACS), Laboratory Information Systems (LIS), and Electronic Medical Record (EMR) systems. Against the backdrop of the 14th Five-Year Plan, hospitals are rapidly transitioning from informatization to a new era characterized by data-driven operations and intelligence, as traditional information systems increasingly fail to meet the growing demand for diversified, intelligent management and clinical care.

Smart hospitals also represent a market strongly driven by policy. Regulatory frameworks and assessment criteria for hospital informatization are gradually being refined, and the level of digital intelligence will become one of the key metrics for hospital accreditation in the future, creating an urgent and rigid demand for IT upgrades among hospitals. From a management perspective, hospitals currently face tight IT coupling caused by the parallel operation of multiple vendor systems, which leads to data fragmentation across various business modules, hindering interoperability and resulting in data silos. From a clinical care perspective, hospital clinical departments currently have limited data processing capabilities and lack data-driven applications that can effectively address critical clinical pain points.