After Raising Billions, Health Insurance Sector Faces Major Challenges: Where to Next?

Bright Health

Healthcare Platform Provider

UnitedHealth Group

Health Insurance and Health Information Technology Service Provider

Oscar Health

Online Medical Insurance Service Company

The Health Insurance Industry Is Approaching a Critical Turning Point.

Since the second half of last year, some leading companies in the health insurance industry have been facing significant challenges.According to multiple industry insiders who spoke to VCBeat, the “workforce restructuring and business adjustments” at the relevant companies are proceeding in an orderly manner.

For a time, the question of how health insurance companies should develop in the future has sparked wave after wave of discussion within the industry.It is worth noting that health insurance has been a highly sought-after “darling” of capital in recent years.: Since 2020 alone, there have been over 40 financing deals in China’s primary health insurance market, with total funding amounting to tens of billions of RMB. A host of prominent investors and corporations, including Sequoia Capital, Matrix Partners, BlueRun Ventures, Northern Light Venture Capital, IDG Capital, and Tencent, have appeared on the list of investors.

(Frequency of Investment and Financing in the Health Insurance and Insurtech Sectors, as of April. Image source: VCBeat)

Behind the heavy investments lies investors’ high expectations for the health insurance sector. “As a payer, one holds a pivotal position in the healthcare industry and serves as a key variable in determining whether a business model can be effectively constructed. Health insurance represents a payer segment with enormous growth potential,” Wang Wei (a pseudonym), Deputy General Manager of the Product Development Department at an insurance group, told VCBeat. “In recent years, driven by policy support and technological advancements, health insurance is ushering in significant opportunities for structural transformation. Those who seize this opportunity may grow into giants with market capitalizations reaching billions, tens of billions, or even hundreds of billions. This is the core logic behind the substantial influx of capital into this industry.”

After securing substantial funding, health insurance-related companies advanced aggressively, continuously hiring and expanding their business operations, achieving notable results in the short term. However, on the other hand, the recent challenges faced by some leading enterprises indicate that the industry has encountered treacherous waters and turbulent currents.

“At the beginning of last year, when the market was booming, the health insurance technology company I worked for was hiring aggressively. It was also during that period that I transitioned from the traditional medical device sector to innovate in payment solutions. However, after several rounds of adjustments to the new business line, its objectives remained unclear, leaving us uncertain about our direction. This led to continuous cash burn by the company without any noticeable business traction. Consequently, due to operational pressures, the company began implementing successive rounds of layoffs starting early this year,” said an anonymous professional in the health insurance technology industry, speaking to VCBeat.

A number of primary market investors and industry professionals have also consistently stated that the general direction for health insurance is sound, but issues such as an overly narrow industry strategy, tight cash flow, overheated concepts, and inflated valuations have already become apparent and urgently need to be addressed.

Where Is the Health Insurance Industry Headed Amid Current Challenges?

Health insurance is not an emerging sector; it is even slightly traditional, having rarely made waves in the capital markets before.

So why have investment institutions shown such high enthusiasm for this sector in recent years, pouring tens of billions of yuan into it? The core lies inThe market growth rate and capacity of the domestic health insurance sector are entering an acceleration phase.

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the original premium income for health insurance business reached RMB 817.3 billion in 2020, a year-on-year increase of 15.7%, with a growth rate significantly higher than that of other types of insurance. Notably, the annualized growth rate of health insurance over the past five years reached 31.4%, doubling the market size, and it is estimated to have surpassed the RMB 1 trillion mark in 2021.

Simply put, the health insurance sector is a vast and deep market: with original premium income exceeding one trillion yuan and an annualized growth rate of over 30%, the overall market potential is highly attractive. Furthermore, judging from the industry’s evolutionary trajectory abroad, this sector has the capacity to produce giant enterprises.

Consequently, in the face of the trillion-yuan blue ocean of health insurance, numerous health insurtech companies have been established, and fundraising has accelerated. Trends in primary market investments reveal that the health insurtech industry has broadly undergone three waves of development.

·The first wave, spanning from 2014 to 2017, saw the rise of channel-innovation pioneers represented by companies such as Huize Insurance and Shuidi; these enterprises have since gone public and secured core positions in the field.

· The second wave, spanning from 2017 to 2020, was characterized by builders of closed-loop pharmaceutical insurance ecosystems, represented by companies such as Yuanxin, Sipay, and Magnesium Health. These enterprises have enhanced medical efficiency by increasing investment in healthcare services, and they are now on the eve of going public.

· The third wave, spanning from 2020 to the present, features service providers focused on middle- and back-office operations, represented by companies such as Baoxian Jike (Insurance Geek) and Haorensheng Technology. These firms primarily engage in group insurance, risk control, actuarial pricing, and operational optimization. Most of these enterprises are currently at Series A to Series C funding stages and are in a phase of rapid growth.

In terms of the chronological order of the waves,Health insurance technology companies primarily address three core issues: first, channel innovation; second, expansion of service capabilities; and third, enhancing overall efficiency for insurance companies.

“Leveraging internet technology and traffic to drive growth in health insurance sales makes it easier to establish a closed-loop business model,” Liu Xing (a pseudonym), an investor in the primary market, told VCBeat. Health insurance is a business model that relies on scale; therefore, companies innovating in distribution channels can rapidly expand their volume with capital support, thereby increasing revenue and valuation. Once leading firms solidify their positions, the competitive landscape rarely undergoes significant changes. “This is why companies focusing on channel innovation tend to rise first.”

As companies pioneering channel innovation gradually mature, the sector is shifting from a growth-driven market to a saturated one, intensifying competitive pressures. In this context, investment institutions have turned their focus to health insurance technology firms that are expanding their service offerings.

Specifically, service expansion refers to the strategy by which health insurance technology companies link resources across the pharmaceutical, healthcare, and insurance sectors to help insurers undertake the service components of health insurance, including medical care and health management. The core of this model lies in resource integration and enhancing the implementation capability of health insurance products. A representative example of this model overseas is UnitedHealth Group, which currently has a market capitalization exceeding RMB 3 trillion.

“Service expansion aligns more closely with product logic, meaning it helps insurers refine their health insurance product portfolios, thereby leveraging high-frequency services to drive the sales of low-frequency insurance products and enhance user experience,” said Liu Xing. For instance, electronic claims settlement and online communication enable insurers to deliver faster services, while establishing offline pharmacies can improve patients’ medication purchasing experience.

As channel innovation and service expansion give rise to industry leaders, investment firms are increasingly betting on companies that enhance the overall operational efficiency of insurers in areas such as risk control, underwriting, and claims settlement, thereby delivering value through refined operations.Thus, the rise of three waves has driven the rapid development of the health insurance industry.

According to VCBeat, there are currently no fewer than 10 health insurance technology companies in the primary market with annual revenues exceeding RMB 100 million, with some even achieving a 100% year-on-year business growth rate, underscoring the sustained enthusiasm within the industry.

Riding the tailwinds, the health insurance industry has been taking off continuously and should have proceeded according to its predetermined narrative. So why is it facing significant challenges this time, and where exactly does the crisis stem from?

Since the beginning of this year, leading health insurance technology companies in the primary market have undergone workforce optimization to reduce expenses and maintain normal operations. Additionally, some health insurance technology companies already listed in the secondary market are seeking new monetization models.

“Behind the financial crises or business adjustments of some companies lies a common problem prevalent across the entire industry: Health insurance products in China are currently highly homogenized, with on-offer health insurance coverage and eligible insured populations being strikingly similar, lacking sufficient differentiation, and the technological attributes embodied by health insurtech remain weak.“Liu Xing, an investor in the primary market, stated, ‘The essence of health insurance technology lies in applying technology to the health insurance sector; however, it is currently difficult for technology to significantly enhance cost-containment capabilities and health management standards. On the other hand, insurers’ demands remain focused on increasing insurance sales volume. Therefore, whether a solution can bring in more customers will determine whether insurers decide to pay for it.’”

Therefore, among the three waves of rapid development in health insurance technology, channel innovation and service expansion were the first to gain momentum, with the underlying logic being to achieve customer acquisition and enhance customer stickiness.Based on this, the core competitiveness of health insurance technology companies currently still lies in their customer acquisition capabilities and the construction of medical service networks.

“It is evident that companies pursuing channel innovation are currently faring relatively well, yet they face significant traffic pressure and low competitive barriers, with their success hinging on first-mover advantage. The business model of service expansion is asset-heavy, requiring financing to get operations off the ground; while this raises the entry threshold, the current integration between insurance and services remains weak, with leading enterprises still relying primarily on pharmaceutical sales to drive revenue. B2B companies aiming to improve insurers’ efficiency are confronted with challenges such as high customization demands, limited average transaction values, and poor replicability, resulting in relatively small revenue scales,” said investor Liu Xing.

In specific cases, channel innovation is exemplified by Huize Insurance, whose sales expenses from 2018 to 2021 were RMB 94 million, RMB 164 million, RMB 230 million, and RMB 350 million, respectively, showing a year-on-year increase. This trend highlights its anxiety over acquiring traffic-based customers. Waterdrop Inc., meanwhile, is exploring more monetization avenues. Early this year, Waterdrop Crowd-funding introduced a 3% service fee to cover reasonable operating costs and ensure the platform’s sustainable operation, sparking widespread online debate.

Health insurance technology companies that are deeply rooted in service expansion also face significant challenges. For instance, a certain health insurance tech firm recently underwent workforce restructuring; despite years of efforts in the health management services sector, its gross profit margins have remained persistently low. According to insiders,The asset-heavy model and low gross margins have kept the company in a state of continuous loss, with annual deficits reaching hundreds of millions. Consequently, it has had to rely on continuous fundraising in the primary market to sustain its growth. When financing channels are blocked, the company becomes vulnerable to financial crises.

“Most domestic health insurance technology companies are benchmarking themselves against foreign counterparts such as UnitedHealth Group and Kaiser Permanente, but there are significant differences between the insurance systems in China and the United States. Under the broad coverage of national basic medical insurance, private health insurance is not yet a necessity, and market acceptance remains relatively low.” In the view of investor Liu Xing, high-quality medical resources are concentrated in public hospitals, where service providers hold greater bargaining power. Cooperation agreements are typically non-exclusive, leading to severe product homogenization. This also makes the value of current health insurance distribution channels far exceed that of the products themselves.Therefore, many health insurtech companies currently offering health management services are essentially still helping insurers sell more policies, resulting in intense hyper-competition. The value of technological innovation has yet to be fully realized.”

In response to this, Zhong Chongming, a researcher in the health insurance sector, suggests that as they move forward, health insurtech companies should, first, ensure that technological innovation is closely aligned with current business needs, as deviations from practical realities will render such efforts unsustainable; and second, while the so-called “cash burn” associated with technological innovation may be phased and flexible, it must not disregard considerations related to business tracks and financial performance evaluations.

As indicated above, the current health insurance industry suffers from severe homogenization, with many companies still relying on “cash burn” to drive growth, thereby posing hidden risks to their sustainable development. How, then, can this impasse be broken? Answers may be found by looking to the relatively mature health insurance industries abroad.

The first thing to realize is that,Just as is the case domestically, innovators in the overseas health insurance sector have also encountered treacherous shoals and turbulent currents.

For instance, Oscar Health, a health insurance technology company favored by Google. The company aims to transform the health insurance industry through digital technology, much like Uber revolutionized the taxi industry. This is reflected in its use of digital tools to streamline user decision-making processes, enable remote health management, and reduce medical costs.However, from its founding to its IPO last year, Oscar Health accumulated losses exceeding $1 billion.

This is because Oscar Health primarily focuses on individual insurance and online operations, exposing it to higher adverse selection risks than traditional health insurers, which has kept its loss ratio persistently high. To curb losses, Oscar Health has taken two main measures: raising premiums and halving the number of in-network provider partners. Nevertheless, its loss ratio and operational losses remain above the industry average, leading to low customer retention rates and stagnant growth.

To this end, Oscar Health has made substantial investments in technological innovation within the insurance sector and built the world’s first full-stack technology platform, which stands as its most significant technical highlight. Specifically, this full-stack technology platform integrates data science with end-to-end control over user experience. Through backend systems, it enables functions such as automated collection of user data and real-time intervention in users’ health behaviors. The platform covers a broad range of healthcare scenarios, including data collection from users and providers, claims management, billing and benefits administration, as well as user behavior research and intervention.

In a nutshell, Oscar Health leverages digital technologies to provide users with remote medical services and proactively engages in medical care and health management, thereby expanding the functional scope of health insurers beyond the passive role of mere claims payers traditionally assumed by such companies.

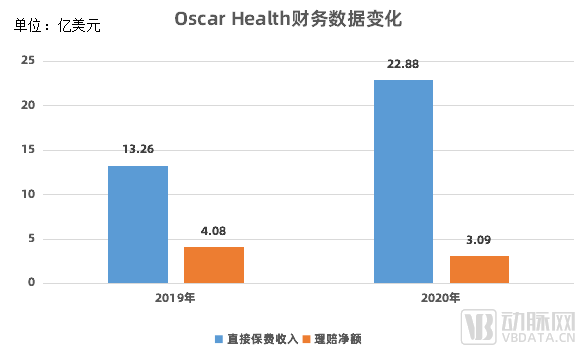

The benefits of technological integration are evident. According to Oscar Health’s financial reports, the company’s net claims amounted to RMB 408 million and RMB 309 million in 2019 and 2020, respectively, representing 30.77% and 13.51% of its direct premiums. This demonstrates that Oscar Health’s cost-control capabilities have become increasingly prominent, validating its business model and technological prowess.

Another example is Bright Health, known as the “mini UnitedHealth,” which primarily promotes two types of health insurance products: Medicare Advantage (a Medicare plan for seniors) and IFP (Individual and Family Plans for self-employed individuals).

In the product design of its Individual and Family Plans (IFP), Bright Health primarily offers three tiers—Bronze, Silver, and Gold—to cater to different population segments, with monthly premiums and reimbursement limits increasing progressively across these tiers. In this model, Bright Health leverages both its extensive healthcare service resources and its base of health insurance subscribers, with the core strategy being the construction of a closed-loop ecosystem integrating pharmaceuticals, healthcare services, and insurance.

Health insurance is a business that relies on scale. The challenge facing Bright Health is how to more efficiently acquire service resources to precisely match user needs, as this ultimately determines whether Bright Health can better control costs.

In response, Bright Health has established a high-performance information technology system to empower its healthcare service platform, connecting insurance customers with medical resources. Additionally, Bright Health launched the MOIS EMR (Electronic Medical Record) system to improve patient care experiences and enhance provider efficiency. MOIS is highly customizable and features robust functionalities that help healthcare institutions manage all operations, from daily clinic workflows to patient management.

Meanwhile, Bright Health launched myhealthkey, an electronic personal health record (PHR) web application that enables patients to stay informed and engaged in their healthcare. Additionally, by leveraging big data models to integrate healthcare services with insurance offerings, Bright Health provides users with high-quality medical care while tailoring the most suitable insurance plans to their individual health profiles, thereby achieving a highly personalized approach.These measures have largely addressed the long-standing pain point of ineffective interventions in health management.

As can be seen from the above, the key words for the growth of foreign health insurance unicorns are focusing on preventive medicine and data analysis technology.“As technology-driven enterprises, most domestic health insurance companies currently allocate too small a proportion of their revenue to R&D investment. This means that these firms still primarily operate with a traffic-oriented mindset, focusing on business model playbooks, resulting in minimal differentiation among them. Only by enhancing their technological capabilities—thereby enabling customer acquisition for insurers while reducing costs and improving efficiency—can they achieve more substantial profits,” said an industry insider. “It is also crucial not to overlook the fact that the acquisition and application of medical data remain significant challenges for the industry today.”

Nevertheless, development always follows a spiral upward trajectory. For the health insurance industry, it is precisely through the continuous breakthroughs of wave after wave of innovative forces that it has gradually achieved today’s accomplishments.

As enterprises explore more methods and problem-solving approaches, the industry is bound to usher in a new wave of growth.