The Rising Value of Chinese-Origin Molecules in Global Markets

GSK

Pharmaceutical R&D Manufacturer

Hansoh Pharma

Pharmaceutical Research, Production, and Sales

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Kailera Therapeutics

Developer of Obesity and Related Disease Therapies

Amino Observation - Original Production by the Innovative Drug Team

Author | Shawei Sha

The high quality of China's innovative drug BD assets is being repeatedly validated.

On April 14, GSK confirmed in a related disclosure at the SGO conference that it would advance the ADC project licensed from Hansoh Pharma into Phase III clinical development and designate it as a priority asset.

On April 16, Kailera Therapeutics, a partner of Hengrui Pharma, successfully listed on NASDAQ in the United States.

Even earlier, domestically produced PD-1/VEGF molecules went overseas consecutively and became the next-generation IO pipelines that BioNTech, BMS, Pfizer, AbbVie, and other MNCs heavily invested in and prioritized, with multiple global multi-center Phase III clinical trials rapidly launched across various fields.

The successive landing of significant milestones is also telling the market that the BD value of domestically produced molecules continues to rise.

/ 01 /

From Early Exploration to Later Mainstay

In the past few years, market discussions about China's innovative drug BD assets have mostly focused on quantity and speed. Molecules with genuine global competitiveness that are held long-term by multinational corporations (MNCs) and advanced to later-stage development are limited. It is not uncommon for early-stage collaboration projects to be terminated due to data not meeting expectations or strategic adjustments.

For a long time, Chinese-produced molecular exports have consistently been associated with two labels: large volume but low quality, and high return rates.

According to statistics, from 2020 to 2025, the "return rate" of licensed-out domestically innovative drugs is approximately 40%. This means a significant portion of licensed projects not only failed to complete all milestones but were even terminated in the early stages.

BMS Executives Stated at the JPM Conference, "The Interesting Aspect of China's Innovative Drugs is That We Are Able to Test More Projects in the Early Development Stage, Thereby Obtaining Clinical Proof of Concept More Efficiently to See What Works and What Doesn't." This Indicates That, in the Eyes of MNCs, China's Innovative Drugs Serve More as Tools for Exploring Early-Stage R&D.

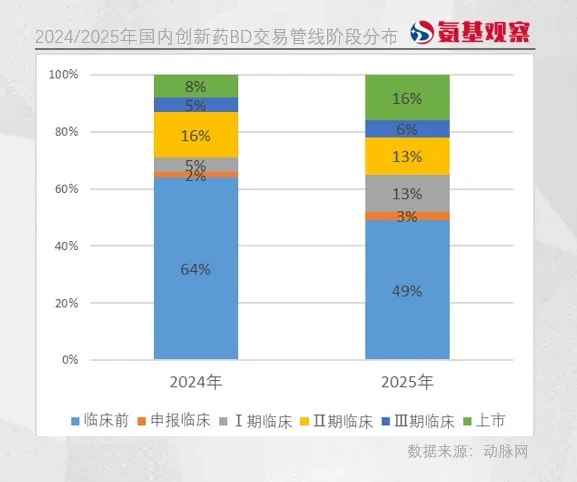

In 2025, this pattern is being completely broken, and more and more evidence shows that the status of China's innovative drug BD assets is changing.

据统计,By 2025, nearly half of China's BD assets will be advanced to Phase II and later stages by MNCs, transforming from peripheral supplements to become a core force in global R&D.

The two ADC projects authorized by GSK from Hansoh Pharma are representative examples. At the SGO meeting, GSK announced that a global Phase III clinical trial for B7H3 ADC HS-20093 in recurrent extensive-stage small cell lung cancer has been initiated. Meanwhile, a global Phase II clinical trial for osteosarcoma is ongoing, and if progress is smooth, a global Phase III clinical trial for osteosarcoma will be launched.

Another B7H4 ADC, mo-rez, is also regarded by GSK as a "priority asset," with plans to initiate five pivotal global Phase III clinical trials in 2026 for first-line maintenance treatment of primary ovarian cancer, second-line endometrial cancer, platinum-sensitive ovarian cancer, ovarian cancer without homologous recombination deficiency, and mismatch repair-proficient endometrial cancer.

This is undoubtedly a phased, milestone achievement in the ADC overseas boom of the past few years. Of course, it's not just ADCs—amidst global competition for emerging targets and mechanisms, China's innovative drug BD assets have also begun to take a dominant position.

Typical examples include PD-(L)1/VEGF bispecific antibodies, regarded as the next generation of IO therapies. Innovative drugs from China are globally leading in both quantity and progress.

Data shows that more than half of the PD-1/VEGF bispecific antibodies under development globally come from Chinese companies. Representative projects include AK112, SSGJ-707, RC148, IBI324, and BNT327, among others. These products have gradually been acquired by various multinational corporations (MNCs), with both upfront payments and total collaboration values showing an upward trend.

Moreover, as mentioned earlier, these assets have become the oncology pipelines that MNCs such as BioNTech, BMS, Pfizer, and AbbVie are heavily investing in and prioritizing, with multiple global multi-center Phase III clinical trials rapidly launched across various fields.

At the same time, MNC's emphasis on Chinese assets is also reflected in the evolution of cooperation models, extending from single project introductions to platform collaborations, and further to NewCo transactions for deep binding.

For example, Gilead's acquisition of Ouro Mmedicines, Connexia's overseas NewCo, for a down payment of $1.675 billion and up to $500 million in milestone payments, is essentially a forward-looking layout of its two self-immune pipelines with BIC potential. Recently, Hengrui Pharma’s NewCo, Kailera Therapeutics, successfully landed on NASDAQ, which once again verifies from the capital level that the global attractiveness of China's BD assets is increasing.

At any time, cold hard cash is the most convincing. According to incomplete statistics, in the past six months, nearly 20 milestones in China's innovative drug overseas BD have been triggered, with a total payment amount exceeding 1.5 billion US dollars. Among them, up to 18 cases were triggered by pipeline progress, accounting for more than 95%.

China's innovative drug BD assets are gaining comprehensive recognition.

/ 02 /

Let Clinical Data Speak

The rise in global status of China's innovative drugs is underpinned by an increasing number of overseas molecules, which have proven themselves with outstanding clinical data.

GSK Plans to Launch Five Phase III Trials of B7H4 ADC Mo-rez Covering the Full Course of Ovarian and Endometrial Cancers, Reflecting Strong Confidence in Mo-rez. GSK Spokesperson Abdullah Told the Media: "GSK Made This Decision Based on Two Independent Datasets from BEHOLD-1, Which Consistently Showed Favorable Efficacy and Safety Profiles."

Specifically, in the platinum-resistant ovarian cancer cohort, the ORR of the highest dose group of mo-rez reached 62% among 34 patients, and in endometrial cancer patients, the ORR of the highest dose was 67%. More than half of these patients had already undergone two or more treatment methods, belonging to a refractory population, with a conventional five-year survival rate of only 20-30% for such patients.

Also placed at strategic priority due to outstanding clinical data is Duality Biologics' B7H3 ADC DB-1311.

In 2023, DualityBio granted DB-1311 and DB-1303 to BioNTech for an upfront payment of $170 million and milestone payments of $1.5 billion. At the time of the deal, DB-1311 was still in the preclinical stage, and BioNTech had not made clear clinical plans for this molecule.

At this year's JPM conference, BioNTech highlighted DB-1311 (BNT324) in its presentation on ADC strategy and announced plans to actively initiate a pivotal Phase III clinical trial for its first-line treatment of mCRPC, due to the drug’s impressive efficacy data from Phase I/II trials in mCRPC.

Data show that DB-1311 achieved an ORR of 42.3% (52/73) and a DCR of 90.4% in heavily pretreated mCRPC patients, being recognized by BioNTech as a BIC. In addition, BioNTech also highlighted the drug's potential for pan-cancer treatment and has initiated a Phase II clinical trial of DB-1311 as monotherapy or in combination with BNT327 for advanced metastatic solid tumors.

In non-oncology fields, China's innovative drugs in autoimmune and metabolic sectors have also shown outstanding performance.

On March 23, Gilead made a significant acquisition of Ouro Medicines. The core asset, BCMAxCD3 bispecific antibody CM336, originated from Connaught Medical, whose outstanding clinical performance in the autoimmune field was the key attraction for Gilead.

In clinical studies involving patients with autoimmune hemolytic anemia, CM336 demonstrated excellent efficacy in patients who failed CD19 CAR-T therapy, with complete depletion of peripheral CD19-positive B cells lasting 3-6 months. In the indication of primary immune thrombocytopenia, CM336 also performed remarkably well, achieving complete and sustained depletion of peripheral B cells for over 5 months, without the occurrence of common side effects such as CRS or ICANS associated with immunotherapy.

In the metabolic field, Kailera Therapeutics stated in its prospectus that its GIP/GLP-1 agonist Ribupatide demonstrates "superior" clinical efficacy compared to Zepbound.

Phase III clinical results of Ribupatide for the treatment of obesity showed that 44.4% of patients in the 6mg dose group achieved more than 20% weight loss in 48 weeks, while Phase III clinical results of Zepbound showed that its highest dose (15mg group) achieved a 20.9% weight reduction in 72 weeks. In terms of both dosage and weight loss speed, Ribupatide demonstrated superior efficacy.

In addition, Kailera Therapeutics has two small-molecule assets for weight loss, also sourced from Hengrui Pharma. These molecules produced in China helped Kailera Therapeutics complete its US IPO worth $625 million, marking an important milestone in the capitalization of a NewCo platform for innovative Chinese drugs overseas.

It can be seen that an increasing number of Chinese innovative drug assets entering the global system through BD are making great strides forward with competitive clinical data.

/ 03 /

Not by chance, but by necessity

The closed-loop of NewCo, with an increasing number of molecules going overseas advancing to later-stage clinical trials abroad, the achievement of these milestones is not occasional but inevitable.

The core lies in the maturity of China's innovative drug development system, from talent to technology and regulation. With active participation from all parties, the domestic innovation ecosystem has gradually been established and reached initial maturity. It can be said that over the past decade, the influx of capital, policy support, and the rise and fall of countless pharmaceutical companies have intertwined, ultimately providing Chinese innovative pharmaceutical enterprises with an opportunity to take a seat at the table today —

From Trial-and-Error to Global Leadership: China’s Innovative Drugs Transition from Low-Cost Followers to BIC/FIC Pioneers, Taking Center Stage in Global Pharmaceutical Innovation.

McKinsey analysts stated: "China's current macro environment as a whole has created or nurtured an innovation-friendly atmosphere. This is reflected in various aspects, from a well-established regulatory framework to policies that encourage the development of industrial parks. Of course, China also boasts a vast talent pool, particularly in STEM (Science, Technology, Engineering, and Mathematics) fields."

It is precisely under the support of this systematic capability that the proportion of high-quality molecules in China's innovative drug supply continues to increase. This change is directly reflected in the BD market.

In the first quarter of 2026, the total amount of China's innovative drug BD broke through 60 billion US dollars, setting a new historical record. Among them, the proportion of platform-based cooperation and long-term binding models has increased significantly, indicating that MNCs' recognition of the quality of Chinese assets has turned into trust.

Once trust is established, the cooperative relationship shifts from one-time business development (BD) to deep binding involving multiple projects and platforms. Examples of this trend include Simcere Pharma's collaboration with BI on an AI-based peptide discovery platform, Insilico Medicine's partnership with Eli Lilly in the field of AI-driven target discovery, as well as Innovent Biologics' collaboration with Eli Lilly covering multiple early-stage pipelines in immunology and oncology.

This trust has further opened up cooperation in the new technology track. In this round of BD deals, small nucleic acid drugs such as siRNA and microRNA have become hot directions. MNCs' recognition and bet on China's capabilities in cutting-edge technology fields are continuing to strengthen.

Moreover, the weak position of China's innovative drugs in the global industrial chain is also changing.

According to data shared by the biopharmaceutical intelligence firm Evaluate with FierceBiotech, the average upfront value (including upfront payments and near-term achievable milestone payments) of China's innovative drug outbound BD has surged from US$52 million in 2022 to US$172 million so far in 2026, skyrocketing over 230% in just three years.

The upward trend continues. As of now, the average upfront payment value of disclosed outbound licensing deals for 2026 is 22% higher than the full-year average for 2025.

The wave of Chinese innovative drugs going global continues to surge. Perhaps it won't be long before we no longer see the so-called criticism of "selling green seedlings."

PS: Welcome to scan the QR code below to add Amino Jun's WeChat for communication.