Can Huiminbao, the Three-Year Phenomenon Covering 140 Million People, Sustain Its Momentum?

MediTrust Health

Innovative Inclusive Health Medical Service and Security Platform

360Health

A Healthcare Company

Since its surge in popularity in 2020, the nationwide “Huimin Bao” supplementary medical insurance schemes have accumulated a total of 140 million enrollments.

This figure would be an exceptionally outstanding achievement for any health insurance product in China.After all, in the current era of rapid development in the health insurance industry, no other product has demonstrated such swift market expansion capabilities: nearly 100 insurance companies have participated, covering more than 200 cities, with total gross written premiums reaching approximately RMB 14 billion.

Not only that, but Huiminbao is also reshaping the entire healthcare industry, attracting numerous health insurance technology platforms and pharmaceutical companies to join. Furthermore, by virtue of its extensive coverage, Huiminbao holds unparalleled advantages in both data accumulation and customer acquisition channel reach. It is well known that within the health insurance industry, data and customer acquisition are two critical priorities for every insurer.

(Chart by VCBeat)

(Chart by VCBeat)

However, the sustainability of Huiminbao still faces challenges.In terms of enrollment rates, there is currently significant variation across cities. The highest rates exceed 80%, while first-year enrollment in some regions ranges from 1% to 15%, with certain areas falling below 5%. Notably, apart from cities with higher economic development levels, most Huiminbao (inclusive supplementary medical insurance) schemes have limited enrollment rates.

“After experiencing a period of explosive growth akin to ‘adding oil to a raging fire,’ the market dividends for Huiminbao insurance have been rapidly depleted.” Yang Zhenguo, an industry practitioner in the health insurance sector, told VCBeat.Currently, the exploration of Huiminbao (city-specific supplemental medical insurance) across various regions remains largely a bottom-up process of imitation or follow-the-leader dynamics. Loss ratios and subsequent policy adjustments remain to be observed, and some emerging issues are unlikely to have short-term solutions.

How Have “Huiminbao” Plans Performed Over the Past Three Years of Surging Popularity? What Are the Industry Stakeholders’ Strategies, and What Direction Will Their Evolution Take in the Future? In response to these questions, VCBeat has analyzed publicly available data and conducted interviews with industry experts to provide insights into the Huiminbao landscape.

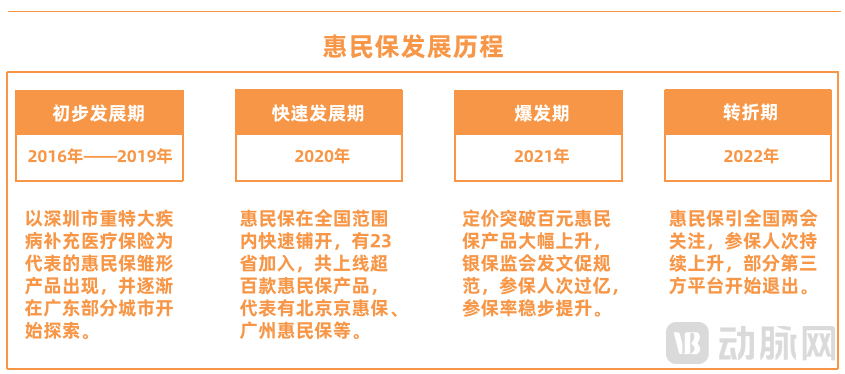

The rapid advancement of Huiminbao (inclusive supplementary medical insurance) is attributable to its product features of “low premiums and high coverage limits,” coupled with government endorsement and the joint promotion by insurers and third-party enterprises, making it a veritable viral sensation.

Taking “Zibo Qihui Bao” as an example, enrollment for this inclusive commercial health insurance plan concluded on December 6, 2021. The number of insured individuals exceeded 1.58 million, marking a year-on-year increase, with an enrollment rate reaching 37.4%.

“As long as individuals have social insurance, they can purchase this coverage for just tens to hundreds of yuan, regardless of their health status. With sum insured amounts reaching up to millions of yuan and government endorsement, these are the reasons why Huiminbao has gained widespread popularity.“Zhang Xinyao, a senior executive at an insurance company, told VCBeat, ‘Huiminbao can be described as the first truly universal health insurance product. In contrast, the previously popular critical illness insurance and million-yuan medical insurance policies primarily covered healthy individuals, failing to effectively stimulate demand for commercial health insurance among the general public.’”

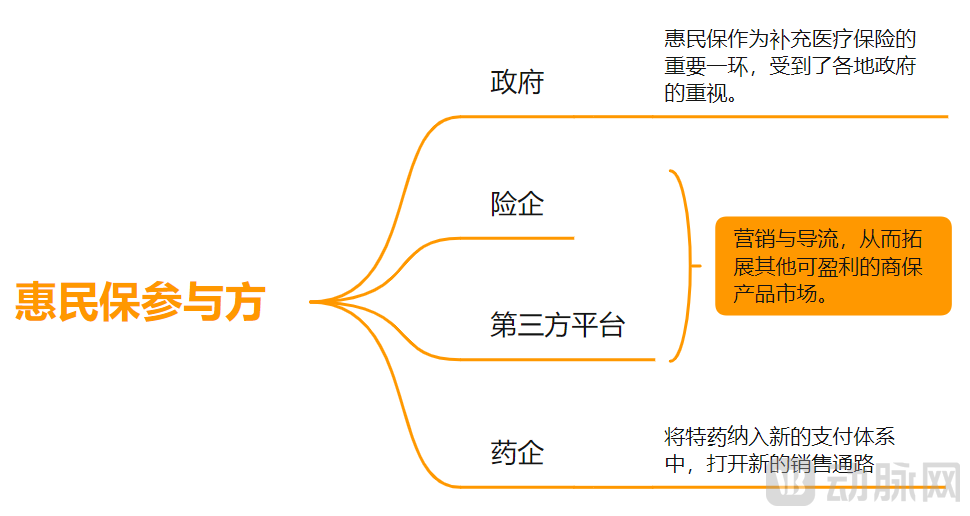

For insurance companies and third-party enterprises, the primary objective of actively participating in Huiminbao (city-specific supplemental medical insurance) is customer acquisition. “Compared to generating profits, they place greater emphasis on achieving secondary conversion sales,” stated Zhang Xinyao. He noted that promoting Huiminbao enables low-cost customer acquisition, broader business coverage, market education, and the accumulation of operational data.

Therefore, for both insurance companies and third parties, as long as Huiminbao breaks even or incurs only minor profits or losses, it falls within an acceptable range. The core objective remains strategic: to leverage Huiminbao for marketing and customer acquisition, thereby expanding the market for other potentially profitable commercial insurance products.

(Considerations of Various Stakeholders in Huiminbao; Graphic by VCBeat)

(Considerations of Various Stakeholders in Huiminbao; Graphic by VCBeat)

Despite “not making a profit,” can such low-priced Huiminbao really deliver on its promise of covering critical illnesses?

“The design of the product is key to whether Huiminbao can effectively provide coverage for serious illnesses, andThe loss ratio after actual operation is the core evaluation metric.“Zhang Xinyao stated.

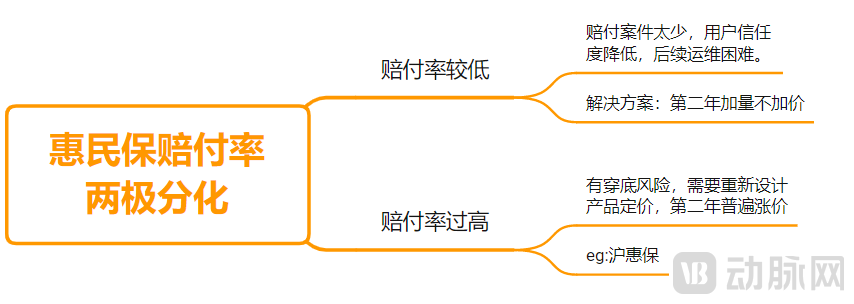

A search of publicly available data reveals that many Huiminbao (city-specific supplemental medical insurance) plans have low loss ratios. For instance, a Huiminbao plan launched in a central Chinese city reported 550,000 enrollees. With a premium of RMB 69 per person, total premium income amounted to approximately RMB 38 million. As of September 30 last year, cumulative claim payments totaled RMB 8.1717 million, resulting in a loss ratio of approximately 22%.

“In some cases, Huiminbao insurance plans have processed only dozens of claims, with total payouts amounting to just over one million yuan and loss ratios below 10%; in certain regions, Huiminbao products have even disappeared from the market,” said an industry insider who requested anonymity. “Many Huiminbao plans face similar issues of inadequate claim payouts, which directly undermines consumer trust in these products.”

Meanwhile, some Huiminbao plans are under pressure due to high claim payouts. For instance, Shanghai’s Huhuibao has paid out a cumulative RMB 524 million in claims from July last year to February this year, accounting for 61% of its RMB 850 million in premiums. Notably, Huhuibao still has four months left in its claim period before the next policy year begins.

“Some local healthcare security administrations require a minimum loss ratio of 80% for city-specific supplemental medical insurance (Huiminbao), with the remaining 20% covering various expenses such as marketing and operations. This means that Hu Hui Bao has only about 20% of its premiums available for claims; exceeding this threshold would result in a deficit, turning the program into a loss-making venture,” said the aforementioned source. “Had it not been for the Shanghai outbreak, this would have become a highly probable scenario.”

In some regions, claim payouts are insufficient, while others face the risk of fund depletion, resulting in a polarized loss ratio for Huiminbao insurance.In response, Zhang Xinyao stated that the industry and medical insurance authorities are also gradually adjusting the design of related products to optimize loss ratios.

Taking a Huiminbao (city-specific supplementary medical insurance) product in a western region of China as an example, it initially offered only coverage for out-of-pocket expenses within the national drug catalog and special drug coverage. In its first year, the loss ratio for special drugs was below 30%, and the loss ratio for in-catalog coverage was also under 50%. In response to this situation, the product has been adjusted this year with enhanced benefits while keeping the premium unchanged, effectively offering “more coverage at no additional cost.”

According to VCBeat, several “Huimin Bao” (inclusive commercial health insurance) products launched this year have adopted a strategy of “enhancing coverage without raising premiums.” These improvements primarily involve further optimization of eligibility criteria, deductibles, and coverage responsibilities, while addressing gaps in protection for critical and rare diseases and expanding the list of covered specialty drugs. Some Huimin Bao plans have also piloted additional health services, including internet-based medical offerings such as remote consultations and home nursing care.

For Huiminbao products with high loss ratios, repricing needs to be considered. “When institutions first launched Huiminbao, they lacked clear insights into the profile of insured customers, making risk control challenging and necessitating a gradual learning process. However, data from the previous year often provides important references for pricing products in the following year, thereby enabling continuous optimization of the overall product,” said Zhang Xinyao.

According to the 2022 edition of “Hu Hui Bao,” for which enrollment opened today (May 25), the annual premium has increased from RMB 115 last year to RMB 129, representing a 12% rise.

(Graphic by VCBeat)

(Graphic by VCBeat)

It is evident that, amidst both successes and concerns, Huiminbao continues to undergo iterative development.As Huiminbao continues to evolve, many industry experts agree that the landscape among various stakeholders will undergo significant changes.: Some institutions secured the desired channel and user resources, while others gained nothing from the process and departed in disappointment.

“The market has repeatedly proven that after any viral product triggers agitation and frenzy, it will eventually return to rationality and normalcy,” said Zhang Xinyao.

The multiple stakeholders of Huiminbao, including the government, insurance companies, third-party health insurance technology providers or service providers, and pharmaceutical companies, are key to its rapid launch and sustained operation.

But as a commercial health insurance product, why do local governments endorse Hui Min Bao?

This is because in March 2020, the State Council issued the “Opinions on Deepening the Reform of the Healthcare Security System,” which stated that by the end of 2030, China will have established a healthcare security system with basic medical insurance as the mainstay, medical assistance as the safety net, and coordinated development of supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid.As an important component of supplementary medical insurance, inclusive “Huiminbao” schemes have garnered significant attention from local governments across China.

“Currently, commercial health insurance products on the market lack the scale necessary for effective risk pooling, and their high enrollment thresholds and premiums have limited their role in providing multi-tiered coverage. Therefore, the emergence of Huimin Bao is viewed favorably by the government,” said Yang Zhenguo, a professional in the health insurance industry.

In terms of operations, local governments and healthcare security administrations typically provide supportive services such as policy recommendations, data sharing, and public communication and education, with some also offering follow-up guidance. For instance, the Healthcare Security Administration of an eastern province is closely monitoring the claims experience of local Huimin Bao (city-specific supplementary medical insurance) programs across its prefecture-level cities, has conducted multiple surveys on project claims, and is poised to issue relevant guidance documents to standardize the ongoing operation and maintenance of Huimin Bao.

“While the level of government support varies across regions, there is now a broad industry consensus that during the initial promotional phase, governments should take a more proactive role in publicity efforts such as encouraging enrollment; however, once Huiminbao (inclusive commercial health insurance) products are launched into the market, insurers should be granted greater operational autonomy,” stated Zhang Xinyao.

Let's take another look at insurance companies and third-party platform companies.For insurance companies, the commissions from low-priced Huiminbao (inclusive health insurance) products are relatively meager, making it difficult to incentivize sales agents. Therefore, third-party platforms need to provide multi-dimensional empowerment in areas such as distribution channels, services, and even risk control.

“Huiminbao insurance schemes particularly test the overall operational capabilities of third-party platforms. After all, within a co-insurance consortium that often comprises more than ten members, coordinating the sales pace among consortium partners, enhancing offline marketing efficiency, and reducing the sales difficulty for agents are all significant challenges,” an industry expert involved in the design of multiple Huiminbao products told VCBeat.

Overall, third-party platform companies must not only attract traffic but also effectively manage its operational conversion, provide technical expertise and integration support, and continuously iterate on their products and strategies.

“At the end of the day, this is ultimately a tough and labor-intensive business. Third-party platform companies are willing to engage in it not only to acquire customer numbers and some data, but also to boost transaction volumes and brand awareness, thereby laying the groundwork for financing and initial public offerings,” said an industry insider who requested anonymity. “In the past two years, competition among third-party platforms in the Huiminbao (city-specific supplemental medical insurance) sector was intense, with price wars even breaking out in certain regions. After this fierce rivalry, the industry has cooled down, and many companies have chosen to exit.”

To date, Nuanwa Technology, Ping An Medical Insurance Technology, and 360 Health have all withdrawn from the Huiminbao market. “The circumstances surrounding each company’s exit vary,” said the aforementioned industry insider.

First, some companies have adjusted their strategies and no longer engage in insurance-related businesses. For instance, Ping An Medical Technology, which pioneered the Shenzhen Huiminbao (inclusive health insurance) business, has exited the Huiminbao sector amid its current strategic transformation.

Second, some companies suffer from poor overall operational performance and fail to generate profits. Huiminbao is inherently a volume-driven business, where the enrollment rate often determines the financial capacity for subsequent third-party platform operations and maintenance. If a company lacks sufficient overall operational capability, the ultimate outcome will be incurring losses while merely gaining superficial publicity.

Beyond the entry and exit of third-party platforms, pharmaceutical companies’ enthusiasm is also gradually being ignited.Based on implementation progress across various regions, Huiminbao (city-specific supplemental medical insurance) is gradually expanding its coverage to include more specialty drugs. Taking Beijing Puhui Bao as an example, in addition to covering 25 specialty drugs, it has, for the first time, expanded its formulary to include 75 overseas-specific drugs prescribed by designated medical institutions in the Boao Lecheng International Medical Tourism Pilot Zone in Hainan. Patients become eligible for reimbursement once their out-of-pocket expenses reach a deductible threshold of RMB 20,000.

“Many local Huiminbao plans have included specialty drugs in their coverage, giving pharmaceutical companies that have faced payment pressures in recent years a taste of success,” said Yang Zhenguo, an industry practitioner in the health insurance sector. He noted that after being listed in the Huiminbao specialty drug directories, pharmaceutical companies have opened up new sales channels and deepened their collaboration with health insurers.

In summary,After three years of explosive growth, Huiminbao, as a novel model for commercial insurance collaboration, has successfully aligned government bodies, insurers, health insurance technology firms, pharmaceutical companies, and other stakeholders, establishing a complete collaborative ecosystem.As for whether continuous operation and maintenance can be sustained in the future, it depends on the level of collaboration among all parties and their own capabilities.

As population aging deepens, a gap persists between the existing basic medical security system and commercial health insurance, making it difficult for low-income and elderly populations to mitigate health risks through individual means.Huiminbao, as a form of supplementary medical insurance, will serve as a bridge connecting basic medical insurance and commercial health insurance.

“Huiminbao represents the first collaboration between basic medical insurance and commercial health insurance, potentially propelling health insurance to a new level,” said Zhang Xinyao. He noted that supporting the development of inclusive medical insurance products not only alleviates the burden on basic medical insurance but also paves the way for commercial health insurance.

It is worth noting that although the health insurance sector has experienced rapid growth in recent years, with its premium volume surpassing RMB 800 billion in 2020 to become the third-largest insurance category after life and auto insurance, its claim payouts amounted to less than RMB 300 billion. This figure accounts for less than 5% of the total national health expenditure, which exceeded RMB 7 trillion for the year, indicating a limited role in providing supplementary coverage."Hui Min Bao" has undoubtedly opened up new prospects for the further popularization of health insurance.

“Huiminbao can acquire a large pool of potential customers at a low cost, presenting insurers with an excellent opportunity for market education and customer acquisition. Such data and channels are essential for the secondary or multiple conversions of health insurance products,” said Zhang Xinyao.

In this process, in what direction will Huiminbao evolve? According to many industry insiders,First, the sector is becoming increasingly standardized under policy support, which requires national and local healthcare security administrations to refine supportive policies., such as clarifying the access rights and procedural standards for using foundational data in the development of Huiminbao (inclusive commercial health insurance), and establishing a collaborative mechanism for credit-based supervision.

Second, as Huimin Bao continues to develop in depth, the long-touted commercial narrative of “pharmaceuticals, healthcare, and insurance” will accelerate its implementation.Thanks to the exploration of Huiminbao (city-specific supplemental medical insurance), collaboration between the pharmaceutical and insurance industries will become closer, with both sides enhancing mutual understanding and identifying more best practices and methodologies.

Third, the "Huimin Bao" pioneered a risk-sharing coinsurance model, setting a precedent for the insurance industry to underwrite policies through collective industry efforts., which will enable future industry co-insurance pools to pilot initiatives such as volume-based procurement of commercial insurance formularies in the promotion of health insurance, thereby fostering the practical application of more innovative products.

Looking back on the rapid expansion of Huimin Bao over the past three years, it is evident that this trend reflects new breakthroughs and possibilities in the health insurance market. Although the road ahead may still face many difficulties and challenges, with careful cultivation and guidance from all participating parties, the health insurance industry will gradually move towards a virtuous cycle, thereby building a new ecosystem for medical security.

(At the interviewees' request, Yang Zhenguo and Zhang Xinyao are pseudonyms.)