Is the Med-Aesthetic Upstream Still Profitable Amid Rising Supply and Intensifying Competition?

For years, the upstream sector of the medical aesthetics industry has been widely recognized as holding a dominant position within the entire value chain, with high profit margins and substantial returns serving as its defining characteristics.

From the business performance of publicly listed companies, the labels of high profitability and high returns are well substantiated. For instance, in fiscal year 2021, three upstream medical aesthetics enterprises—Bloomage Biotech, Imeik, and Haohai Biological Technology—achieved substantial revenue growth of 88%, 104.13%, and 53%, respectively, while their net profits increased by 21.13%, 117.81%, and 53.1%, respectively.

Such robust profitability naturally attracted significant investor interest, culminating in a surge of financing activities in 2021, during which 23 upstream medical aesthetics companies secured funding.

It is not just capital that is focusing upstream; an increasing number of entrepreneurs are also shifting their targets to the upstream sector. Even some companies originally focused on the mid- and downstream segments of the medical aesthetics industry have begun to explore the upstream market.

Amid the market’s rapid expansion, certain industry challenges are gradually coming to light. For instance, the upstream segment of the medical aesthetics industry, which has long enjoyed high profit margins, may see this advantage erode as competition intensifies with the influx of entrepreneurs and capital. Furthermore, on the whole, China’s upstream medical aesthetics sector still faces technical and manufacturing barriers.

Moreover, over the past two years, “profitability challenges” have remained a persistent label for downstream enterprises in the medical aesthetics industry. Under the impact of the pandemic, these downstream players have generally faced operational difficulties, leading to a decline in demand for their products, which has, in turn, adversely affected the development of upstream enterprises to a certain extent.

So, amid these disruptive changes, is the upstream segment of the medical aesthetics industry still as promising as once imagined? What are the real challenges it faces today? And how should companies respond to these challenges? To address these questions, VCBeat has engaged in discussions with industry experts and investors to seek answers.

The Gold Mine Behind Beauty

A market valued at hundreds of billions, with an industry penetration rate of less than 5% and a compound annual growth rate exceeding 10%, these figures all reflect the rapid development of the current medical aesthetics market.

With the rise of the “beauty economy” and improvements in socioeconomic standards, medical aesthetic services have long since transitioned from a niche market to mass consumer consumption.

Within the entire medical aesthetics industry chain, downstream medical aesthetics institutions actually account for more than half of the total output value. However, constrained by high customer acquisition costs and operational expenses, their profitability is less favorable than commonly perceived. In contrast, upstream manufacturers hold the most advantageous position in the industry chain.

According to data from the Suning Finance Research Institute, upstream enterprises in the medical aesthetics industry chain, such as raw material manufacturers and injectable product manufacturers, have an average gross profit margin of 90% and an average net profit margin of 30%. In contrast, mid- and downstream enterprises, including medical aesthetics institutions and platforms, have average gross profit margins of 50% and 60%, respectively, with both achieving an average net profit margin of only 10%, significantly lower than that of upstream enterprises.

From this perspective, it is not difficult to understand why the upstream segment of the medical aesthetics industry has garnered such significant attention. Of course, the near “explosive” growth witnessed in the upstream sector over the past two years is certainly not attributable solely to the factor of high profit margins.

According to Wang Xinliang, a partner at Mingfeng Capital, in addition to strong profitability, the increasingly robust talent ecosystem, numerous market success stories across its product portfolio, and mature market expansion strategies are all key drivers behind the current prosperity of the upstream medical aesthetics industry.

Furthermore, compared to mid- and downstream players in the industry, upstream medical aesthetics companies face higher entry barriers due to factors such as substantial R&D investment and stringent requirements for product performance. This implies that companies that are first to market with exclusive innovative products can maintain a unique advantage and capture a significant market share for a considerable period. Taking Allergan’s botulinum toxin product, BOTOX®, as an example, it was launched in 2002 and captured 86% of the global botulinum toxin market by 2005. Although its market share has declined somewhat with the emergence of competitors, data from GBI Research shows that BOTOX® still held a 74% share of the global botulinum toxin market in 2018.

Amid multiple influences, the upstream market of the medical aesthetics industry has become increasingly prosperous, but this has been accompanied by intensifying competition in the upstream sector.

“The Intensifying Competition in the Upstream Medical Aesthetics Sector”

When it comes to the upstream sector of the medical aesthetics industry, hyaluronic acid is clearly an indispensable presence.

In the medical field, it is difficult to find another niche sector as prosperous in the capital market as hyaluronic acid. Due to the gross profit margin of medical aesthetic hyaluronic acid injection products reaching as high as 90%, hyaluronic acid is also referred to as the "Moutai" of the medical aesthetics industry.

On one hand, thanks to the years of development in the hyaluronic acid industry, its production processes, output, and costs are well-suited to meet the growing demand for medical aesthetic services.

On the other hand, the rise of domestic medical aesthetics consumption and the rapid development of the non-surgical market, to which hyaluronic acid injections belong, have also provided a sufficiently large market space for the application of hyaluronic acid.

In the face of this massive market, domestic companies have also been actively entering the medical aesthetics hyaluronic acid market by launching hyaluronic acid injection products. Statistics show that approximately 60 hyaluronic acid-based dermal fillers have been approved in the Chinese market, indicating intense competition.

Another star product in the upstream segment of the medical aesthetics industry, “botulinum toxin,” has also seen intensifying competition in recent years.

In June 2020, Ipsen’s Dysport received marketing authorization in the United Kingdom, becoming the third botulinum toxin type A product approved for clinical use, following Lanzhou Institute of Biological Products’ Hengli and Allergan’s BOTOX.

On October 26, 2020, Beijing Sihuan Pharmaceutical Holdings Group Co., Ltd. announced that “Botulinum Toxin Type A for Injection (Letybo),” exclusively distributed by the company and manufactured by the South Korean biopharmaceutical company Hugel, was officially approved for marketing by the National Medical Products Administration on October 21, 2020, becoming the fourth botulinum toxin type A product approved for launch in China.

Since then, the domestic botulinum toxin market has entered a four-player competitive landscape. The annual report data from Sihuan Pharmaceutical also offers a glimpse into the strong profitability of botulinum toxin products.

In March this year, Sihuan Pharmaceutical released its 2021 business report. During the reporting period, the revenue and segment operating profit of Sihuan Pharmaceutical’s medical aesthetics business were approximately RMB 399 million and RMB 250 million, respectively, representing year-on-year increases of 1,383.3% and 971.1%, and accounting for 12.1% of the Group’s total revenue. This achievement was primarily driven by the performance contribution from the launch and sales of Letybo.

Significant market profitability has naturally attracted an increasing number of companies to invest heavily in this sector.

Competitive Landscape of the Domestic Botulinum Toxin Market (Partial)

It is evident that although botulinum toxin products are subject to stringent approval procedures, with only four products currently marketed in China, domestic companies are clearly unwilling to relinquish this lucrative opportunity. Consequently, competition for the Chinese botulinum toxin market is poised to intensify significantly.

Not only is competition intensifying among established staples in the medical aesthetics sector, such as hyaluronic acid and botulinum toxin, but even regenerative injectable products—a category that only received domestic approval last year—appear to be trending toward heightened market rivalry.

In 2021, the concept of regenerative medical aesthetics rapidly gained momentum. Huadong Medicine’s Ellansé (commonly known as “Girl Needle”), Sinopharm Aikang’s AestheFill (commonly known as “Baby Face Needle”), and Imeik’s Ru Bai Angel (also categorized as a “Baby Face Needle”) were successively approved in China. Additionally, Jinbo Bio’s “Recombinant Humanized Type III Collagen Lyophilized Fiber” received market approval. These products involve regenerative materials such as PLLA (poly-L-lactic acid), PCL (polycaprolactone microspheres), and collagen.

Revenue data also offers a glimpse into the market potential of regenerative injectable products. In 2021, Sinclair Aesthetics (the operating entity for Huadong Medicine’s domestic medical aesthetics business, responsible for the promotion and sales of Ellansé, known as “Girl’s Needle,” in China) reported operating revenue of RMB 185 million. In the first quarter of 2022, this figure reached RMB 157 million. This means that within just six months of its launch, Ellansé (“Girl’s Needle”) achieved sales totaling RMB 342 million.

Domestic companies are also intensifying their efforts in this emerging market, with players such as Yuanxiang Bio’s Aiti’en mADM (also known as “Coral Needle”), Xihong Bio, and Sihuan Pharmaceutical continuously entering the space. Although this niche segment is still in its early stages and the competitive landscape remains somewhat undefined, it is undeniable that the market battle for regenerative injectable products has already begun.

Unlike raw material manufacturing, the research and development of domestic medical aesthetic devices is largely centered on the theme of “domestic substitution,” a trend driven by the long-standing dominance of imported products in the medical aesthetic device market.

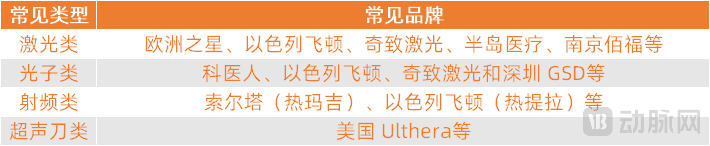

Taking popular photoelectric devices in the medical aesthetics equipment sector as an example, data from LeadLeo Research Institute shows that China’s market size for photoelectric medical aesthetics reached RMB 21.501 billion in 2019, contracted to RMB 19.172 billion in 2020 due to the impact of the pandemic, and is projected to grow to RMB 50.159 billion by 2025, with a compound annual growth rate (CAGR) of 13.43% from 2021 to 2025. Within this multi-billion-yuan market, numerous European, American, and South Korean brands hold dominant positions.

Competitive Landscape of the Domestic Market for Photoelectric Medical Aesthetic Devices

Competitive Landscape of the Domestic Market for Photoelectric Medical Aesthetic Devices

As a popular procedure in the medical aesthetics sector, this field has naturally attracted numerous companies to establish their presence.

For instance, in February 2021, Haohai Biological Technology entered into equity investment and product licensing agreements with Ouhuaimeike and the U.S.-based Eirion, thereby initiating its strategic layout in the field of energy-based medical aesthetic products. In March this year, Meiyankongjian, a subsidiary of Sihuan Pharmaceutical, executed an equity transfer agreement and a capital increase agreement with Shenzhen Yimei Medical. Through equity acquisition and capital injection, Sihuan Pharmaceutical invested in Shenzhen Yimei, marking its formal entry into the market for energy-based medical aesthetic devices.

Confronting the Issue of Increased Supply

It is evident that competition in the domestic market, whether in injectable products or medical devices, is intensifying. The ensuing question is: how long will this trend persist?

Regarding this issue, Wang Xinliang believes that years of promotional and marketing practices for cosmetics and medical aesthetic products have made China’s market strategies highly sophisticated. A large number of enterprises are sufficiently confident in entering this field, akin to how companies remain willing to invest in creating the 101st shampoo brand despite the presence of 100 existing brands in the market.

Furthermore, intensifying competition and shrinking profit margins downstream have created an urgent demand among distributors and institutions for innovative products and distinctive offerings, thereby further driving market prosperity. In the short term, there are no signs that these influencing factors will abate; therefore, the upstream segment of the medical aesthetics industry is expected to remain highly active for a considerable period to come.

The industry is booming, with significant capital inflows, presenting an undeniable opportunity for companies operating within this sector. However, some perspectives suggest that the absolute advantage once held by upstream players in the medical aesthetics supply chain has gradually diminished due to intensifying competition. The proliferation of product categories has also made it increasingly difficult for certain products to remain preferred choices for downstream medical aesthetics institutions.

Will the upstream segment of the medical aesthetics industry lose its inherent advantages in the near future? Does it still possess sufficiently distinct value to attract capital and innovators? Furthermore, will the contraction in downstream demand caused by the pandemic have a significant impact on the upstream sector?

To answer these questions, we need to conduct an analysis from the following perspectives.

First, the market potential is enormous, and competition remains in a blue ocean.

Compared with countries boasting well-developed medical aesthetics industries, such as Japan, South Korea, Europe, the United States, and Brazil, China’s market penetration rate of less than 5% reveals a significant gap. Given the industry’s compound annual growth rate (CAGR) exceeding 10%, China’s medical aesthetics market still holds immense potential for development and expansion.

Furthermore, although the number of products in various market segments continues to grow, the variety of medical aesthetic products in China pales in comparison to that of countries with more developed medical aesthetics industries. For instance, regarding hyaluronic acid and botulinum toxin mentioned above, China currently has approximately 60 approved hyaluronic acid injectable products and four approved botulinum toxin products. In contrast, South Korea’s hyaluronic acid sector alone boasts over 100 manufacturers, with more than ten botulinum toxin manufacturers having received regulatory approval.

From this perspective, the level of competition in the upstream segment of China’s medical aesthetics industry has not yet reached a state that can be described as a “red ocean.”

Jia Yangchun, founder of Nanjing Baifu, shares this view, noting that China’s upstream medical aesthetics sector remains largely a blue ocean with substantial room for growth. Both raw materials and equipment R&D face significant technical and process-related barriers, and given the medical nature of these products, market entry is subject to rigorous review processes and lengthy approval cycles. Consequently, although many companies are entering the upstream medical aesthetics space, intense competition is not expected to surge dramatically in the short term.

Second, high barriers create competitive advantages.

Compared with midstream and downstream enterprises and institutions, the upstream segment of the medical aesthetics industry is characterized not only by high profit margins but also by high entry barriers, namely significant technological barriers.

This also means that the lucrative upstream segment of the medical aesthetics industry is not easily accessible. Coupled with the stringent review processes and prolonged approval cycles mentioned earlier, companies that have already successfully entered the market are afforded ample time to leverage their “first-mover advantage,” and thus will not face significant disruption from new entrants in the short term.

Therefore, for new entrants to successfully capture a share of the market, they must deeply explore user needs, dare to pursue globally leading innovations, or leverage first-mover disadvantages by implementing incremental innovations to create higher-quality products.

Third, sustained demand growth is driving upstream development.

Over the past two years, the profitability of downstream medical aesthetics institutions has become increasingly challenging due to the impact of the pandemic. Although upstream players have consistently held a dominant position across the entire medical aesthetics industry chain, the decline in downstream demand has also adversely affected the business operations of upstream enterprises.

To adapt to the impact of the pandemic, some upstream enterprises have made corresponding changes, such as making targeted adjustments to their sales channels. However, in Wang Xinliang’s view, the pandemic’s current impact on the upstream industry does not yet amount to a structural change.

Meanwhile, thanks to the continuous growth in the user base, rising demand for medical aesthetics, and the high repurchase rate of certain aesthetic procedures, the upstream sector of the medical aesthetics industry has not been significantly impacted by the pandemic; some upstream companies have even achieved relatively strong growth rates during this period.

A senior industry veteran with over a decade of experience in the upstream medical aesthetics sector expressed agreement with this view, stating, “The impact of the pandemic on the upstream medical aesthetics industry was actually relatively short-lived. On one hand, companies adjusted their expansion strategies in response to market conditions to align with market development; on the other hand, consumer demand for medical aesthetic procedures has grown increasingly strong. Moreover, as certain medical aesthetic treatments are inherently high-frequency services, they foster strong customer stickiness.”

Final Remarks

It is evident that neither the influx of new market entrants nor the impact of the pandemic has thus far exerted a disruptive influence on the upstream segment of the medical aesthetics industry; however, this does not imply that upstream players can rest easy.

Although the upstream sector of China’s medical aesthetics industry is showing promising growth, it remains constrained by multiple factors, with insufficient technological breakthroughs being the most pressing challenge.

Taking hyaluronic acid as an example, although China is the world’s largest producer of hyaluronic acid raw materials and domestically produced products account for half of the approximately 60 approved hyaluronic acid injectable products, there is still a gap compared with international peers in the high-end segment. This is because the production of hyaluronic acid requires not only expertise in biofermentation technologies—such as strain selection, fermentation formulation, and process control—but also mastery of materials science and synthetic chemistry related to cross-linking, necessitating continuous iteration and accumulation of expertise.

This issue is not only prevalent in raw material production but also equally pronounced in equipment research and development.

In Jia Yangchun’s view, China’s domestic medical aesthetics equipment market remains in a relatively early and low-end stage. The high-end segment is still dominated by imported brands, with few teams possessing independent R&D and innovative capabilities. Moreover, the industry is characterized by significant heterogeneity; the prevalence of counterfeit and gray-market products not only undermines consumer interests but also impedes the healthy development of the sector.

It can be said that as niche sectors become increasingly crowded, companies with less distinct competitive advantages—such as those with inferior product strength—will quickly hit their growth ceilings and struggle to expand further. These companies will gradually lose their edge in both their collaborations and competitions with channels and institutions, as well as in the battle for end consumers.

Furthermore, when positioning themselves in the upstream segment of the medical aesthetics industry, some companies use mature overseas markets as benchmarks. However, it is important to note that Chinese medical aesthetics consumers differ from their overseas counterparts in terms of age structure, demand preferences, and level of education and acceptance regarding products.

Taking hyaluronic acid and botulinum toxin as examples, the International Society of Aesthetic Plastic Surgery (ISAPS) released its annual global survey on cosmetic procedures. In international markets, the top five non-surgical cosmetic treatments in 2019 were botulinum toxin, hyaluronic acid, hair removal, non-surgical fat reduction, and intense pulsed light (IPL) skin rejuvenation. However, in the Chinese market, hyaluronic acid ranks as the leading non-surgical medical aesthetic procedure.

“We anticipate that, as regulatory compliance strengthens across China’s entire medical aesthetics industry, the Chinese market will develop a product portfolio distinct from that of overseas markets,” said Wang Xinliang. Therefore, companies and investors need to more precisely grasp shifts in the market’s consumption structure.

At the same time, enterprises should also pay attention to the impact from the external environment, such as the continuous prosperity of light medical beauty projects and the ongoing penetration into lower-tier cities. Based on market changes and user needs, they should launch innovative products to seize first-mover advantages, or continuously refine their products for incremental innovation.

In summary, the upstream segment of the medical aesthetics industry remains a field rife with new breakthroughs and possibilities. We look forward to the emergence of more promising sectors within the broader upstream medical aesthetics market.