How Sports Rehabilitation Is Poised to Become the Next Aesthetic Medicine and Dental Care Market

In recent years, the Chinese government has encouraged the public to engage in various sports activities. According to projections by the General Administration of Sport of China, the number of people regularly participating in physical exercise is expected to exceed 630 million by 2035. Given that the incidence rate of sports injuries among athletes and active individuals is approximately 10%–20%, it is estimated that around 100 million people will require rehabilitation treatment for sports injuries in the future.

Sports rehabilitation was initially developed to serve athletes. With rising economic standards and heightened health awareness, the use of targeted exercise interventions to accelerate functional recovery has not only gained recognition within the sports community but is also increasingly favored by postoperative patients, individuals with sports injuries, and those suffering from chronic pain.

According to data from the China Health and Health Statistical Yearbook, China’s rehabilitation medical services market is on the verge of reaching a scale of RMB 100 billion. Consequently, many people liken sports rehabilitation to the next frontier in the medical aesthetics and dental care sectors. However, compared with these two mature markets, sports rehabilitation remains in its infancy. VCBeat has interviewed numerous industry insiders to explore how sports rehabilitation can evolve into the next major growth sector akin to medical aesthetics and dental care.

The development of medical aesthetics and dentistry is inseparable from their inherent characteristics. Compared with traditional serious medical services, medical aesthetics and dentistry exhibit stronger attributes of consumer healthcare. Although both fall under the umbrella of “medical care,” there are distinctions between them. First, their purposes differ: simply put, serious medical care aims to treat diseases, while consumer healthcare seeks to enhance quality of life. In other words, the criterion for evaluating consumer healthcare products and services is whether they genuinely improve consumers’ quality of life.

Second, practitioners in consumer healthcare also come from the field of conventional medicine. The majority of physicians working in consumer healthcare previously practiced conventional medicine, acquiring clinical experience in disease treatment before transitioning to consumer-oriented services. Their professional background ensures expertise and is one of the key factors that motivate consumers to purchase these services.

Comparison Between Consumer Healthcare Services and Serious Medical Services

Third, consumer healthcare permits no errors. Consumer healthcare is not a rigid demand; rather, it exists in dependence on other essential needs, such as those related to social interaction, psychological well-being, and service quality. Consequently, it tolerates few mistakes. Therefore, consumer healthcare must involve conservative and cautious medical practices, striving to avoid unsatisfactory outcomes. In addition to sound regulations, professional competence, and ethical standards for practitioners, safety remains the paramount element in the design of consumer healthcare products and services.

Fourth is the market-oriented approach. Given its consumer-centric nature, payments are primarily out-of-pocket, granting consumers absolute choice. Therefore, such products and services are better suited for operation by private institutions that are closely aligned with the market. It is precisely this market-driven operation of private institutions, which closely responds to consumer demands, that has fueled the rapid development of the medical aesthetics and dental care sectors in recent years.

We can also explore how to approach sports rehabilitation from these perspectives.

Essentially, sports rehabilitation, like medical aesthetics and dentistry, aims to improve quality of life; the difference lies in the level of public awareness.

A typical example is that if a person feels their teeth are unattractive and affect their work and daily life, they will immediately think of seeing a dentist, with the only difference being the choice between public and private medical institutions.

Among office workers in first- and second-tier cities, lumbar disc herniation has become an occupational disease due to prolonged desk work. However, only a small fraction of affected patients are aware that they can seek pain relief through sports rehabilitation institutions.

Their condition typically follows one of two paths: either they delay treatment while symptoms are mild, seeking massage therapy and physical rehabilitation only when the pain becomes unbearable; or they wait until the condition worsens and undergo surgery, yet face a high risk of recurrence due to their postoperative living and working environments.

In fact, chronic low back pain, represented by lumbar disc herniation, is often caused by long-term poor posture and the inability to activate or weakness of the muscle groups responsible for maintaining stability.

By opting for sports rehabilitation, one can address the root cause of postural misalignment by correcting muscle strength imbalances. Through manual therapy and instrumental interventions to relax soft tissues, combined with active exercises to strengthen weakened muscles, a physiologically sound muscular balance can be re-established, thereby alleviating pain.

However, this pathway remains unknown to many.

Sun Xiaoyi, co-founder of UP Clinic, explained to VCBeat: “Looking at the development trajectory of community healthcare abroad, a ‘3+1’ model has emerged, comprising three pillars—dentistry, rehabilitation, and general practice—plus pharmacy services. In China, dentistry is already well-developed, general practice is rapidly expanding, and the pharmacy sector is obviously mature; the only shortcoming lies in rehabilitation. This, however, indirectly underscores that the demand for rehabilitation services is genuine.”

Exercise rehabilitation remains a poorly understood concept among the general public. Image source: APTA (American Physical Therapy Association)

“Sports rehabilitation currently falls within the scope of sports on the rise and healthcare moving downstream,” Zhang Ting, co-founder of Qingrun Health, told VCBeat.

It is precisely because sports rehabilitation lies at the intersection of multiple disciplines that public awareness of it remains at a very rudimentary stage. “In the United States, individuals experiencing pain naturally turn to the various rehabilitation facilities widespread throughout their communities. In contrast, people in China tend to endure such discomfort in silence, only seeking hospital care when absolutely necessary,” said an industry insider with overseas study experience, in an interview with VCBeat.

“The ambiguity of the concept is also an obstacle to its promotion. Sports rehabilitation is benchmarked against physical therapy abroad, which actually includes not only exercise but also manual therapy, physical agent modalities, and other approaches. However, current sports rehabilitation emphasizes exercise alone, thereby downplaying its comprehensive nature and raising the barrier to public understanding,” Zhao Qingyi, CEO of Fudong Musculoskeletal, told VCBeat.

Of course, the situation has changed in recent years. Taking mature orthopedic surgeries as an example, influenced by the traditional belief that “it takes 100 days for injuries to tendons and bones to heal,” many patients did not undergo postoperative rehabilitation, which prevented normal functional recovery and adversely affected their quality of life. In recent years, with social progress, physicians have begun to educate patients on the importance of postoperative rehabilitation, thereby gradually fostering awareness and understanding of rehabilitation among patients.

Cognition requires time to settle and events to drive it.

Not long ago, riding the wave of enthusiasm for the Beijing Winter Olympics, the topic “The End of the Ski Slope Is the Orthopedics Department” brought sports medicine and rehabilitation to the attention of hundreds of millions of ordinary people, elevating industry visibility to a new height. Many industry insiders remarked, “One Winter Olympics is worth several years of market education.”

Just as the aesthetic economy promoted by medical aesthetics and dentistry ultimately focuses on self- and social recognition, fulfilling psychological and physiological needs to enhance quality of life, people’s perception of exercise has also evolved. It is no longer viewed as a physical pastime for the “strong but simple-minded,” but has been elevated to the level of a healthy lifestyle philosophy.

Exercise has also evolved from an optional activity into a trendy lifestyle, with people willing to pay for every aspect of it.

Particularly in first-tier megacities, regular exercise has become a socially recognized lifestyle. People derive physiological and psychological satisfaction from physical activity, regarding it as an essential component for enhancing quality of life. In addressing the adverse consequence of sports injuries, the public is gradually shifting from the previous approach of rest and abstinence from exercise to proactively seeking treatment to ensure continued participation in physical activities.

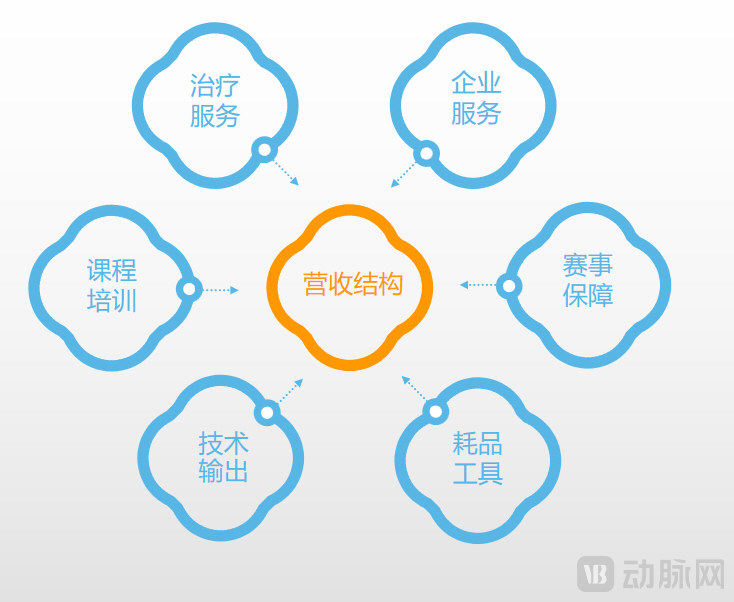

From the perspective of sports rehabilitation institutions, in order to meet growing demand, more service offerings have been developed beyond postoperative rehabilitation and sports injury care. These include chronic pain rehabilitation for the neck, shoulders, waist, and legs among office workers; scoliosis management for adolescents; and specialized services for sports enthusiasts, such as physical conditioning support for marathon runners.

Overall, public awareness of sports rehabilitation has been increasing year by year, and the concept of rehabilitation is gradually gaining acceptance. Many gyms and wellness centers have targeted this market, launching sports rehabilitation services one after another. However, due to limitations in professional expertise, many of these institutions fail to deliver the outcomes expected by consumers.

The phenomenon of bad money driving out good has emerged during the industry’s initial acceleration phase, indirectly reflecting the sector’s high level of interest. The general public is still in a transitional state between awareness and unawareness; industry chaos risks alienating users who have been painstakingly educated—a critical issue that practitioners must address.

Whether in medical aesthetics or dentistry, there is no significant shortage of physicians. Although the business layouts of private institutions and public hospitals differ, practitioners in both sectors emerge from the same training system, which distinguishes them from the sports rehabilitation field.

Although many procedures in medical aesthetics and dentistry are low-risk, consumers place significant importance on whether practitioners hold valid professional licenses. The availability of talent also determines the pace of industry development; beyond standardized technical systems, operational strategies, and management methods, the supply of qualified personnel is a critical factor in the rapid expansion of institutions.

In sports rehabilitation, a service package requires the involvement of at least two roles: physicians and physical therapists. Physicians determine whether patients require rehabilitative therapy; if so, physical therapists take over to conduct assessments, design rehabilitation plans, and implement them. This structure exists because physical therapists do not have prescription privileges.

For sports rehabilitation institutions, the shortage of physicians is relatively easy to address, given the well-established training systems and the large pool of available talent. In contrast, the issue concerning rehabilitation therapists is more complex.

Currently, the mainstream training of sports rehabilitation professionals in China is divided into two tracks: Sports Rehabilitation offered by physical education universities, and Rehabilitation Therapeutics within the medical school system. According to data from the China Higher Education Student Information and Career Center (CHESICC), 79 higher education institutions offer programs in Sports Rehabilitation, while 178 offer programs in Rehabilitation Therapeutics. With thousands of students graduating each year, why does this remain an issue? This must be examined from the perspective of healthcare institutions.

The products and services offered by sports rehabilitation institutions differ significantly from those in the medical aesthetics and dental sectors. In medical aesthetics and dentistry, offerings are centered around high-value consumables, with various products and services designed accordingly, and customers primarily pay for these consumables. In contrast, the products and services provided by sports rehabilitation institutions aim to restore functional capacity, with the core value lying in the expertise and philosophy of physical therapists. Customers are essentially paying for the therapist’s treatment plan or therapeutic system.

Most services offered by sports rehabilitation institutions require manual implementation.

The reality is that graduates from both sports universities and medical schools fail to meet the demands of sports rehabilitation institutions. For single-site rehabilitation clinics, building a team from scratch takes nearly three years. However, due to staff turnover, these clinics can only maintain team integrity after this period, with their talent pool insufficient to support expansion needs.

From the user’s perspective, the ultimate goal is to fulfill psychological and physiological needs while enhancing quality of life. In medical aesthetics and dentistry, in addition to selecting practitioners with core technical expertise and operational proficiency, the materials used are also a significant factor in customers’ decision-making. In contrast, sports rehabilitation is essentially a purchase of rehabilitative techniques, where the key selection criteria are the practitioner or the brand system.

Previously, VCBeat noted in its article “The Rapidly Growing Sports Rehabilitation Niche: Annual Salaries of 600,000 Yuan Still Fail to Attract Talent” that many institutions have adopted self-training programs to address staffing shortages. For instance, UP Clinic established the UP Research Institute, hiring more than 40 full-time Chinese and foreign experts to train newly graduated recruits using its own resources. By replicating the clinical environments of rehabilitation centers in advanced Western countries, the institute rapidly enhances their technical skills to meet employment requirements. During the pandemic, graduates who had planned to pursue further studies abroad, as well as international students whose master’s or doctoral programs overseas were interrupted due to the pandemic, could choose to work at UP Clinic, thereby simulating the working environment of overseas rehabilitation institutions.

However, small and medium-sized institutions, particularly those operating as single-location practices, face an awkward dilemma. While they can provide training, their scale is limited. After a period of employment, trainees often realize they can operate independently, leading them to establish their own practices and take a significant portion of the client base with them. Since smaller institutions have not yet built sufficient brand equity to retain clients, their efforts in staff development inadvertently undermine their own competitiveness.

Certainly, many industry professionals have already taken steps to change the status quo. For instance, Qingrun Academy, in collaboration with United Family Healthcare (Beijing United Family Rehabilitation Hospital), the Chinese Association of Rehabilitation Medicine, the China Non-Public Medical Institutions Association, and the Royal Dutch Society for Physical Therapy, has jointly launched the “Standardized Training Program for Rehabilitation Therapists.” Through a curriculum lasting two to six months, the program enables graduates to smoothly transition from their role as students to that of professionals in the workplace.

Average Transaction Value of Sports Rehabilitation Institutions

From an operational perspective, a people-centric business model faces a challenge: the number of clients each rehabilitation therapist can serve daily is limited. Each session typically lasts one hour, capping a therapist’s daily capacity at 8–10 client groups. Over a month, this translates to a maximum of approximately 180 client groups. With an average revenue per visit ranging from RMB 600 to RMB 1,200, the revenue generated per therapist is relatively lower compared to sectors such as medical aesthetics and dentistry.

The limited talent pool and service models cap the per-capita revenue of sports rehabilitation institutions; however, free from the constraints of high-value consumables, overall costs remain controllable. Although single-store revenue scales lag behind those in medical aesthetics and dentistry, sports rehabilitation boasts higher profit margins.

Like consumer healthcare services such as medical aesthetics and dentistry, sports rehabilitation currently places particular emphasis on safety. While medical aesthetics and dentistry may involve invasive treatment options, sports rehabilitation entirely avoids safety concerns at the product design level.

Taking Ranran Sports Rehabilitation as an example, the business is divided into three main sectors: sports rehabilitation, physical maintenance, and physical conditioning. These sectors target pain relief and functional recovery; muscle care and injury prevention; and strength training and physique enhancement, respectively. The exercise intensity gradually increases from low to high, aiming to minimize the risk of old injuries recurring.

This distinction is based on a product system designed to meet customers’ needs at different stages. For example, a retired woman who undergoes postoperative rehabilitation and achieves functional recovery may feel fully satisfied. At most, impressed by the excellent service and outstanding rehabilitation outcomes, she might purchase an additional maintenance package, which would enable her to meet everyday living requirements such as going downstairs to buy groceries or taking her dog for a walk.

Sports Rehabilitation Institutions Design Services with Safety in Mind

For young sports enthusiasts, functional recovery is the most fundamental need. They may also want to understand the causes of their sports injuries, how to prevent them, whether insufficient muscle strength is a contributing factor, and whether they require sport-specific conditioning training. These services can effectively extend customer lifetime value and increase institutional revenue.

Based on customer feedback, particularly from younger clients, there is a reluctance to undergo training within medical institutions, as they perceive healthcare solely as a means for treating illness. Their selection of follow-up programs is not driven by therapeutic needs but rather viewed as an investment in themselves. From this perspective, such choices have the potential to translate into long-term, recurring consumption.

Under the premise of safety, the restoration of functional capacity, improvement in quality of life, and return to sports represent the immediate demands of young people for sports rehabilitation at the current stage.

There is still room for consumer healthcare to make more attempts centered on safety. Taking hyaluronic acid in medical aesthetics as an example, it is a product with high safety that requires repeated consumption, and its duration lasts between six months to one year. In other words, if users choose hyaluronic acid, repeat purchases are highly likely.

In contrast, while the sports rehabilitation industry ensures safety—with some institutions even introducing aquatic rehabilitation therapy—no single product or service has driven large-scale repeat purchases. Institutions must therefore delve deeper into the productization of their technical offerings, establishing standardized treatment protocols for specific conditions such as postoperative rehabilitation after anterior cruciate ligament (ACL) reconstruction, adolescent idiopathic scoliosis, biomechanical assessment and correction, and postpartum body shaping.

These standardized products not only expand the user base and increase revenue, but also enable rapid replication of the business model, while deepening customers’ recognition of the institution’s brand. Institutions can leverage this to build patient communities and strengthen operational efforts to maintain customer relationships, which is essential for establishing a sustainable long-term brand image.

Unlike serious medical care, which leans toward passive marketing and relies primarily on word-of-mouth, consumer healthcare is market-oriented and requires proactive marketing efforts.

As foreign countries have been leading China by many years in the rehabilitation industry, the revenue structures of overseas rehabilitation institutions have become a model for many domestic counterparts to emulate.

In terms of customer acquisition channels, institutions currently rely primarily on referrals and word-of-mouth. While referrals represent a relatively mature approach, they serve only as a foundation; sustainable growth depends on leveraging word-of-mouth. By enhancing consumer experience, building brand reputation, and cultivating a loyal customer base—thereby increasing the rate of patient referrals—institutions can further improve the stability of their customer acquisition.

Primary Customer Acquisition Channels for Sports Rehabilitation Institutions

Diversification of customer acquisition channels is a crucial guarantee for sustainable development. Many institutions are also exploring new media operations in an effort to achieve channel diversification. In addition, some star rehabilitation therapists are building their personal brands on new media platforms. For instance, the account “Sports Rehabilitation with Lao Sun” has amassed over 2.6 million followers on Douyin (TikTok’s Chinese version), establishing a solid foundation for both traffic generation and monetization.

However, unlike the direct and precise user acquisition models of medical aesthetics O2O platforms, the sports rehabilitation industry is still in its nascent stage, relying heavily on general-purpose platforms such as Dianping, Zhihu, and Weibo. These platforms exhibit relatively low conversion rates and limited effectiveness in driving conversions.

Furthermore, a unique business model is also a critical factor in institutional operations. For instance, UP Clinic has segmented its services into two divisions—“UP Clinic” and “UP Stretch”—based on the distinction between clinical medical care and consumer-oriented medical care. Services involving clinical medical care, such as surgery, postoperative rehabilitation, and conservative treatment, are offered under UP Clinic. Meanwhile, consumer-oriented services, including sports injury rehabilitation, posture correction, and athletic performance enhancement, are provided through UP Stretch.

The benefits of this approach include alleviating outpatient congestion and providing customers with more cost-effective services. According to Sun Xiaoyi, co-founder of UP Clinic, “The return on investment period for stretching services is very short; the first clinic even achieved break-even in its first month. The brand is rapidly upgrading its model, exploring optimal product offerings, staffing configurations, pricing structures, and career advancement pathways for such small-scale clinics.”

Thanks to this single-store model, UP Clinic has achieved rapid expansion. It currently operates eight locations in Shanghai, strategically situated in prime commercial districts known for lifestyle services and fitness, such as Raffles City Changning and Taikoo Li. The company plans to continue expanding its stretching clinic network in the future.

The establishment of UP Clinic’s stretching model holds positive significance for the development of the sports rehabilitation industry. Although sports rehabilitation falls under consumer healthcare, it is fundamentally a medical institution, subject to lengthy approval processes and requiring relatively substantial investment. In sports rehabilitation, certain consumer-oriented services represent a new business format; whether operational and management standards can be established for these services forms the basis for their rapid expansion. The creation of such standards is a challenge that all sports rehabilitation institutions must address.

Only after standardization is established can the issue of scalability be addressed.

Currently, the largest sports rehabilitation institutions in China number only around ten, with most being local businesses and very few operating across regions. In contrast, foreign rehabilitation companies already have enterprises with hundreds of locations. In the coming years, as the influence of the sports rehabilitation industry expands and public awareness increases, the number of chain sports rehabilitation institutions is expected to rise further.

Meanwhile, small yet exquisite single-store outlets and small-scale chains are also a significant driving force behind industry development.

For these small yet exquisite practitioners, the ability to implement refined, consumer-centric operations is a true test of managerial acumen. For instance, some institutions adopt a user-oriented approach by dividing the treatment process into several stages, with clearly defined outcomes for each. Patients pay on a stage-by-stage basis, only proceeding to payment for the next phase after achieving the rehabilitation goals of the current one.

“Sports rehabilitation is not inexpensive. For many first-time clients, it is difficult to commit upfront to a multi-month program requiring payment for dozens of sessions at once. We address user concerns by demonstrating phased progress; once the rehabilitation goals are achieved, these clients become our most effective advocates,” said the head of Reboot Heart Power Sports Rehabilitation, a Nanjing-based institution, in an interview with VCBeat.

Furthermore, companies like Fudong Musculoskeletal have pioneered the application of digital therapeutics in sports medicine, addressing accessibility issues during rehabilitation. The integration of digital therapeutics into rehabilitation not only enables patients to access high-quality rehabilitation services regardless of their location but also effectively alleviates the shortage of rehabilitation therapists in China.

The recurring waves of the pandemic have disrupted the development pace of many sports rehabilitation institutions. The integration of digital therapeutics has overcome spatial and personnel constraints by leveraging intelligent wearable rehabilitation devices that connect patient-facing apps with physician-side management backends. This interconnectivity among devices, patients, and institutions enables integrated, precision rehabilitation delivery.

In addition, Ranran Sports Rehabilitation has partnered with Beijing Sport University to establish a Sports Rehabilitation Research Center. While cultivating talent, the center also exports its standardized protocols to help outsiders quickly enter the industry.

It is precisely due to the continuous exploration by these practitioners in operations and management that sports rehabilitation institutions have achieved steady development in recent years.

An analysis of sports rehabilitation institutions from the perspective of consumer healthcare clearly reveals that, unlike the mature medical aesthetics and dental industries, sports rehabilitation remains in its early stages of development despite its significant potential. Many challenges still need to be addressed.

First, in terms of talent, this was the least lacking segment in consumer healthcare services in the past, but has become a bottleneck hindering the rapid expansion of the sports rehabilitation industry. Private institutions have assumed the training responsibilities that should ideally be borne by universities. Encouragingly, many young people from the new generation are choosing to enter the sports rehabilitation field out of genuine interest and passion. With the future development of the industry, the influx of a large number of high-quality technical professionals will surely elevate the overall caliber of technical talent in sports rehabilitation rapidly.

Next is scaled operations. The development path of any consumer healthcare project inevitably relies on scaled operations. Contrary to the external narrative touting sports rehabilitation as the next trillion-yuan market poised for explosive growth akin to dentistry and medical aesthetics, multiple industry insiders told VCBeat, “At this stage, we must curb impetuousness and take each step steadily. Blind expansion will only harm the industry.”

A prevailing view is that the explosive growth in the medical aesthetics and dental sectors stems from years of accumulation. This accumulation encompasses both industry-specific factors—ranging from talent and technology to the entire industrial chain—and the gradual enhancement of public awareness, which serves as a prerequisite for such rapid expansion. Although the sports rehabilitation sector holds significant potential and also falls under the category of consumer healthcare, it remains in its introductory stage. Therefore, expecting explosive growth at this juncture would be unrealistic.

Regarding the development of the industry, Sun Xiaoyi stated, “At this stage, institutions should focus on strengthening their internal capabilities, improving their own standardization, enhancing peer exchanges, and establishing industry standards. With these preparations in place, coupled with increased public awareness, sports rehabilitation will enter a period of rapid development.”