Moutai Invests $2.7B While Youngor Retreats from $1.9B Hospital Venture: How Are Listed Companies Faring in Cross-Industry Hospital Projects?

In May, news about listed companies crossing over to build hospitals frequently appeared.

Youngor Group Co., Ltd., a listed men’s apparel company, initially announced its plan to exit the healthcare sector and donate hospital assets valued at RMB 1.36 billion to the local government. Just one week later, a dramatic reversal occurred: at a meeting attended by five supervisors of Youngor, a proposal to terminate the external donation was unanimously approved. The company stated that this decision resulted from its board of directors and management team having “listened to the opinions of a broad base of shareholders” following the previous announcement.

On the same day Youngor announced the withdrawal of its donation, 1,700 kilometers away, Guizhou Moutai Hospital officially commenced operations. Built by Kweichow Moutai Group in accordance with the standards for a Grade III Class A general hospital, the facility represents an investment of approximately RMB 1.9 billion. As a non-profit livelihood project, Moutai aims to address the reality that Renhuai City’s population of 720,000 previously lacked a single Grade III Class A hospital.

Youngor Struggles to Offload a Hot Potato: Can Moutai Hospital Successfully Operate a New Facility?

A decade ago, a wave of restructuring swept through state-owned enterprise (SOE) hospitals, leading to their divestiture from parent companies and transition into privately run medical institutions. Ten years on, hospitals self-built by listed companies as part of their strategic expansion into the health industry are being completed one after another. After experiencing a frenzy of hospital acquisitions and greenfield investments between 2014 and 2016, followed by a return to rationality in hospital investment during 2018, 2019, and throughout the pandemic era, how have these listed companies—with no prior healthcare background—fared in their cross-sector ventures into hospital construction?

The Story of Youngor’s Hospital Establishment

On May 17, Youngor Group Co., Ltd. issued an announcement stating that the company plans to exit the healthcare industry by donating Puji Hospital and related assets to the Ningbo Municipal People’s Government, and will seek authorization from the shareholders’ meeting for the management team to handle relevant matters. The announcement disclosed that the estimated value of the assets to be donated is RMB 1.36 billion (subject to final accounts), and the expected impact of this donation on the company’s net profit for 2022 is RMB 1.02 billion (subject to audited figures).

Regarding the reasons for the donation, Youngor provided three explanations in its announcement: first, the uncertainty of the domestic and international economic situation has increased in recent years; second, the national healthcare system reform is advancing in depth; third, the company lacks operational teams and experience in related industries. If it continues to invest in Puji Hospital and related assets, there may be a significant imbalance between input and output, which is not conducive to the company focusing its funds and energy on developing its core business.

Therefore, the company has decided to further focus on its core business by concentrating resources, capital, teams, and management efforts, while adjusting its existing industrial structure.

The donation announcement sent shockwaves through the market; under pressure from shareholders, the donation resolution was withdrawn seven days later.

As a men’s apparel company, why did Youngor Group Co., Ltd. diversify into the healthcare sector? When did it begin building hospitals? And why did this hospital ultimately become a “hot potato” that Youngor was stuck with?

The earliest strategic layout dates back to 2015.

On March 7, 2015, Youngor Group Co., Ltd. announced its plan to establish a health industry fund in Yinzhou District, Ningbo City, with RMB 1 billion of its own funds. “The fund will primarily make equity investments in enterprises within the broader health industry that are in their growth, expansion, or mature stages, possess promising industry development prospects, and hold significant value for mergers and acquisitions. It will also focus on private placement opportunities of high-quality listed companies, as well as investment opportunities arising from the restructuring and mixed-ownership reforms of large and medium-sized state-owned enterprises in the medical and healthcare sector.”

At that time, Youngor believed that “with the enhancement of China’s comprehensive national strength, the improvement of people’s living standards, and the in-depth advancement of national healthcare reforms, the medical and health industry will usher in broad development prospects and significant investment opportunities.” Youngor also placed high hopes on its layout in the health industry, aiming to “facilitate the transformation of the company’s investment business toward strategic and industrial investments, enhance profitability, and diversify revenue streams.”

By 2018, Youngor Group Co., Ltd. had acquired an 81,326-square-meter plot of land in Haishu District, west of Ningbo, for RMB 75.0964 million. For this medical and health care land parcel, Youngor intended to"Advancing the transformation of real estate business into emerging related industries such as wellness, elderly care, and health towns."。

Under the land grant conditions at the time, Youngor Group Co.,Ltd. was permitted to construct only a large-scale non-profit medical institution on the plot, which was required to meet the construction standards for a Grade 3A general hospital, with approximately 1,600 beds and a total investment of no less than RMB 1.7 billion. Regarding the project timeline, construction was to commence within six months from the date of land acquisition, with a construction period of 30 months, and the facility was to be completed and put into operation in one phase. In other words, barring any unforeseen circumstances, this Grade 3A hospital was expected to become operational by mid-2021; this facility later became Puji Hospital.

At that time, Youngor Group Co., Ltd. announced its plan to construct a large-scale comprehensive smart hospital meeting the standards of a Grade A Tertiary hospital, and to create a health town integrating medical care and elderly care. It also planned to establish Kanglv Holdings Co., Ltd. to centrally manage and operate assets in hotels, tourism, healthcare, and eldercare. Meanwhile, the Ningbo Puji Hospital project received approval from the Ningbo Municipal Health Commission and signed a comprehensive trusteeship agreement with the University of Chinese Academy of Sciences Ningbo Huamei Hospital (Ningbo No. 2 Hospital), with Phase I comprising 450 beds scheduled to be completed and put into operation in 2021.

At that time, local media viewed the outcome of this land auction as filling the gap in large-scale comprehensive medical services in the western urban area in the future.

Continuing the planning of this health-focused town integrating medical and elderly care services, on February 1, 2021, Youngor established Ningbo Youngor Health and Elderly Care Management Co., Ltd. with a registered capital of RMB 360 million. One month later, the company acquired a plot of land designated for other commercial and service purposes (specifically for elderly care institutions) in Jishigang Town, Haishu District, Ningbo, for a total price of RMB 324 million. This location is situated in the vicinity of the previously mentioned Puji Hospital.

For years, Youngor has emphasized its exploration of industrial transformation, with the expansion of its healthcare portfolio marking a significant step. However, in its 2021 annual report, this statement was revised to “optimize industrial layout and gradually exit the health industry.”

Then there was the recent incident in which a donated hospital withdrew its donation.

Land Acquisition and Hospital Construction: The Once-Booming Frenzy of Building Hospitals

In 2015, when Youngor began to lay out its health industry, it was the hottest time for hospital investment.

In December 2014, during an inspection of the Shiyue Town Health Center in Zhenjiang City, Jiangsu Province, General Secretary Xi Jinping put forward the assertion that “without universal health, there can be no comprehensive well-being.” In October 2015, the Fifth Plenary Session of the 18th Central Committee of the Communist Party of China proposed for the first time to advance the construction of a Healthy China, elevating “Healthy China” to a national strategy.

Subsequently, driven by macroeconomic policies, the strategic layout and development of the health industry have garnered significant attention. Capital from various sources has flocked in, while listed companies have seized the opportunity to diversify their operations through cross-sector expansion.

More specifically, as central state-owned enterprises (SOEs) continue to divest their social functions, a wave of restructuring has begun among SOE-affiliated hospitals. Over 3,000 existing enterprise-run hospitals are in urgent need of investment from social capital to be transformed into privately operated medical institutions.

Thus, 2014–2016 became the peak period for hospital investment, with acquisition and greenfield development being the only two approaches.

Dr. Zhuang Yiqiang, Director of the Guangzhou Ailibei Hospital Management Center, told VCBeat that acquisition and greenfield development are two entirely different approaches. “There are significant differences between the two. Building a hospital from scratch offers the advantage of full control over all aspects; however, it entails a long investment cycle and poses considerable challenges in recruiting suitable talent during the early stages. In contrast, acquisitions involve navigating numerous issues related to hospital restructuring and integration.”

Overall, listed companies primarily participate in hospital investments through investment and acquisition, “after all, the cycle for building from scratch is too long.”

However, building hospitals in-house involves another layer of market capitalization management logic for listed companies, beyond merely acquiring land. “The process of establishing a hospital takes time, and during this period, the stock prices of listed companies continue to rise even before the hospital is completed and operational. From the announcement of entry into the health industry, through land acquisition, commencement of construction, completion of building, to the hospital’s opening, positive news continuously helps shape favorable market expectations and boost share prices. Even if the hospital ultimately performs poorly, that outcome would not materialize until ten years later.”

Multiple interviewees believe that in the early years, most enterprises venturing into hospital construction across industries oversimplified the endeavor, assuming it was merely a matter of “securing a plot of land and erecting a building.”

A Non-Exhaustive Review of Hospital Investments

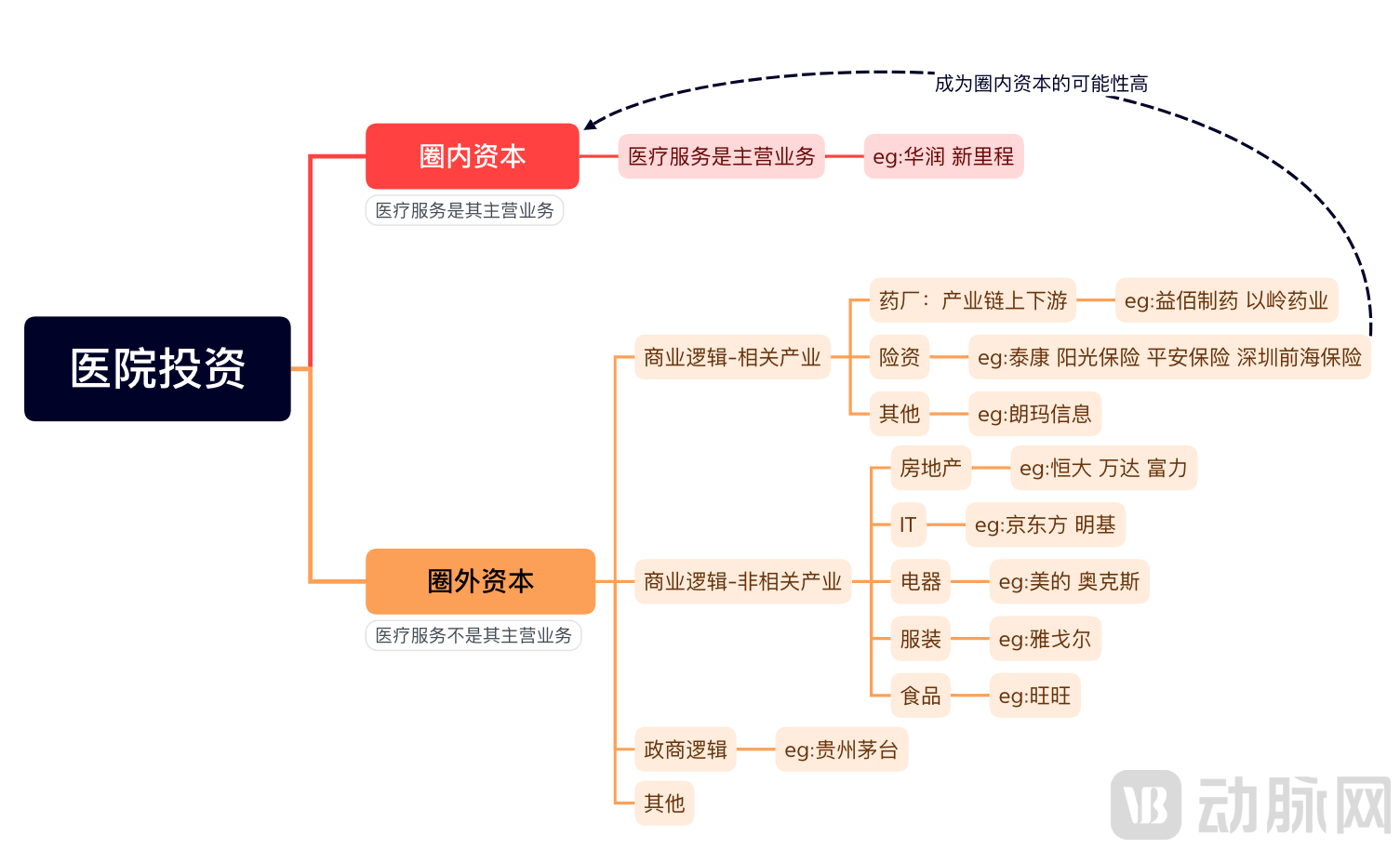

“Land acquisition and construction”-driven cross-sector hospital establishment by non-industry capital can be broadly categorized into the following types:

This includes entrants from both healthcare-related and non-healthcare-related industries.

The former primarily comprises pharmaceutical manufacturers and insurance capital, whose strategic objective is to integrate the upstream and downstream segments of the industrial chain.

For pharmaceutical companies, establishing their own hospitals can help collect clinical cases and facilitate drug research and development.Taking Yiling Pharmaceutical as an example, Wu Yiling acquired 26 mu of land in the Western Development Zone of Shijiazhuang in 1993, at the outset of his career development, to establish Yiling Hospital and Yiling Pharmaceutical. Notably, the hospital was completed and put into operation even before the pharmaceutical factory. According to the official website of Hebei Yiling Hospital, after more than two decades of development, the hospital has forged a successful path by leveraging innovations in Traditional Chinese Medicine (TCM) academic theory to drive departmental construction and specialized development. It is now a local Grade A tertiary general hospital integrating traditional Chinese and Western medicine.

The logic of insurance capital is to achieve the integration of healthcare and insurance.Among them, Taikang Healthcare and Sunshine Insurance have both established mature operational models.

According to its official website, Taikang Healthcare is committed to building a high-quality medical service brand characterized by the integration of healthcare and insurance, as well as the integration of medical care, elderly care, and rehabilitation, with an integrated approach to medical practice, education, and research. It has established five major medical centers across eastern, western, southern, northern, and central China, and has independently developed three specialized disciplines: rehabilitation, dentistry, and neurology. By promoting innovation in value-based healthcare, it provides patient-centered, holistic, end-to-end, and full-chain medical and health management services, thereby achieving a relatively comprehensive strategic layout.

In 2016, Sunshine Union Hospital, the first large tertiary general hospital in China invested by an insurance company, officially opened in Weifang, Shandong Province, marking the beginning of Sunshine Insurance Group’s strategic layout in the healthcare sector.

“The traditional healthcare industry operates on a model where patients are the primary payers, whereas integrating commercial health insurance into the payment system creates the possibility of forming a closed-loop ecosystem. Commercial insurers have an inherent incentive to control costs. When insurance companies operate healthcare facilities, acting as both the ‘payee’ and the ‘payer,’ their own cost-control imperatives naturally drive them to supervise hospital prescriptions and manage patient health, fostering an intrinsic motivation to assist patients with health management. This aligns with the mature Pharmacy Benefit Manager (PBM) system in the United States, a model that offers valuable lessons for China.” This was the rationale provided by Sunshine Insurance Group Corporation Limited at the inception of its hospital, explaining why insurance capital is well-suited for operating healthcare institutions.

“Sunshine Union Hospital is currently operating very well, ranking among the top three hospitals locally. It has more than 1,000 beds.”Zhuang Yiqiang also believes that insurance capital is the cross-industry capital most likely to become a player within the healthcare services sector.。

The scope of companies from unrelated industries is even broader. According to incomplete statistics by VCBeat, these include real estate firms, IT companies, appliance manufacturers, food enterprises, and others, all seeking to expand their industrial footprint and enter the broader health sector.

Judging from AUX, another Ningbo-based enterprise, its foray into the big health industry has yielded far better results than that of Youngor Group Co.,Ltd.

In 2002, Aux began actively exploring a distinctive path for private capital investment in healthcare. In 2006, it fully funded the establishment of Zhejiang University Mingzhou Hospital, which has since grown into one of the largest and highest-standard comprehensive private hospitals in Zhejiang Province.

“The future healthcare industry is the core strategy for Aux’s development,” emphasized Zheng Jianjiang, Chairman of Aux Group.

AUX Group’s listed subsidiary, Sanxing Electric, was renamed Sanxing Medical in 2015.

According to Zhuang Yiqiang’s observations, such enterprises typically adopt a conservative development strategy, lacking the ambition to build hospital chains; instead, they focus on establishing a single hospital locally to serve the community.

“Moutai’s hospital construction may follow this logic.” According to official disclosures from Moutai, once completed, the hospital will serve as a non-profit livelihood project, addressing the reality that “Renhuai City, with a population of 720,000, lacks even one Grade A tertiary hospital.”

According to hospital disclosures, Guizhou Moutai Hospital held a signing ceremony for a cooperation agreement with Zunyi Medical University, officially becoming the university’s directly affiliated hospital. On March 22, Guizhou Moutai Hospital also signed a cooperation agreement with the Affiliated Hospital of Zunyi Medical University to jointly promote the development of healthcare in Guizhou Province.

No shortage of enterprises with no relevance to the health sector speculatively entering the market.

Bubbles Squeeze Out, Hospital Investment Returns to Rationality

Jiang Xiaodong, a managing partner at Changling Capital, has long focused on the healthcare services sector and has invested in chain hospital brands such as Hygeia Hospital and Gushengtang. Based on his observations, over the past 5–10 years, hospitals established by non-healthcare enterprises through cross-industry diversification have rarely achieved success. Here, “success” refers to operational and developmental achievements of the healthcare institutions themselves, rather than financial returns realized by corporate investors from their hospital investments.

“The healthcare services market holds potential, but that doesn’t mean anyone can excel in it.” Jiang Xiaodong has noted a common misconception among investors: underestimating the conditions required to operate a hospital successfully. In his view, healthcare services differ significantly from sectors such as TMT (Technology, Media, and Telecom), where a single brilliant idea can yield a strong product that is then rapidly scaled up with capital. By contrast, healthcare services demand the consistent and meticulous execution of “a thousand detailed tasks.”

Jiang Xiaodong told VCBeat that Changling Capital believes investing in healthcare services is essentially investing in capabilities, and investing in capabilities is ultimately about investing in people. “At its core, healthcare services are not a matter of capital, location, or physical assets; they are fundamentally an issue of management and development, which boils down to the human factor.”

Among human factors, the importance of “visible” doctors is undeniable, whereas hospital administrators and operators, who are less known to the general public, often have their significance underestimated. “Entrepreneurship in healthcare services is better suited for experienced individuals.” In Jiang Xiaodong’s investment experience, being both “passionate and proficient” serves as an excellent hallmark for founding teams in healthcare services; such individuals are more likely to build hospitals that excel, scale up, and strengthen their market position.

Zhuang Yiqiang strongly agrees with this point: “Those crossing over from other industries do not understand healthcare; directly applying the business logic of other sectors to the healthcare industry is the most fatal mistake.”

“In fact, this is a capital-intensive industry characterized by long investment cycles and low but stable returns. Taking U.S. hospitals as an example, their average annual return on investment is approximately 5%. However, one advantage of the healthcare sector is its resilience to economic fluctuations; it can even be considered counter-cyclical. Some international analyses suggest that healthcare demand actually rises during economic downturns, with increases in conditions such as depression, as well as in incidents like suicides and violent altercations,” said Zhuang Yiqiang.

Yet, this consensus on the understanding of the healthcare services industry has only been reached in recent years. Prior to this, the medical industry was burdened with excessively high and unrealistic expectations.

The bursting of the bubble and the rational retreat of hospital investment began around 2019. As hospitals failed to generate expected returns, investors started divesting from previously acquired hospital assets.

What accelerated the cooling of this market was the ensuing pandemic. Private healthcare rarely featured in the mainstream narrative surrounding the “pandemic heroes” who rushed to the front lines. It is undeniable that the pandemic has once again widened the gap in public perception between public and private healthcare.

“Youngors” Dilemma: Sell Hospitals or Press On?

Consequently, enterprises that have already crossed over into hospital establishment find themselves in a dilemma: moving forward requires sustained professional investment amid low returns, while retreating means completely abandoning their prior strategic layout and investments. Zhuang Yiqiang analyzes that some companies still operating these hospitals may not necessarily remain optimistic about the sector; rather, they are able to persist simply because of their deep pockets.

“Youngor’s next step is either to sell off the asset or to press on despite the difficulties, which requires finding partners and custodians—namely, professional post-investment management services,” judged Zhuang Yiqiang.

From the perspective of overall revenue, healthcare service providers are not performing as poorly as commonly perceived. Zhuang Yiqiang told VCBeat that, according to statistics from Guangzhou Ai Li Bi, the average year-on-year growth in operating revenue for the top 50 listed healthcare service companies in 2021 was 35.4%. “In recent years, there have been multiple mergers and acquisitions in the listed healthcare services sector, including General Technology Group’s acquisition of Baoshihua Medical and New Milestone Healthcare’s acquisition of Hengkang Medical. The industry will undergo further consolidation, with a trend toward ‘the large getting larger and the small being acquired.’”

As for listed companies entering the hospital sector from other industries, Zhuang Yiqiang believes that they need to make a major decision next: whether to exit or strive to become established insiders in terms of capital. The so-called becoming established insiders in terms of capital means that medical services can become an important business segment or even the main business of the company. This requires more investment from enterprises to achieve integration across the upstream and downstream of the industrial chain, further consolidate resources within the industry, including collaborating with public hospitals and universities to develop discipline construction, and pursue differentiated development in accordance with national healthcare reform policies.

If a company decides to become “insider capital,” its subsequent priority should be to strengthen its post-investment management capabilities. In Zhuang Yiqiang’s view, Ping An Insurance’s takeover of Peking University International Hospital presents precisely this challenge—how to sustain operations.