Early-Stage Healthcare Investment Cools Down: Rational Correction or Awaiting the Next Breakout?

Much like the weather in May, with its intermittent rain and occasional cold gusts, early-stage investment in the healthcare sector has finally stabilized after a period of intense heat.

Review of Early-Stage Healthcare Financing in May 2022

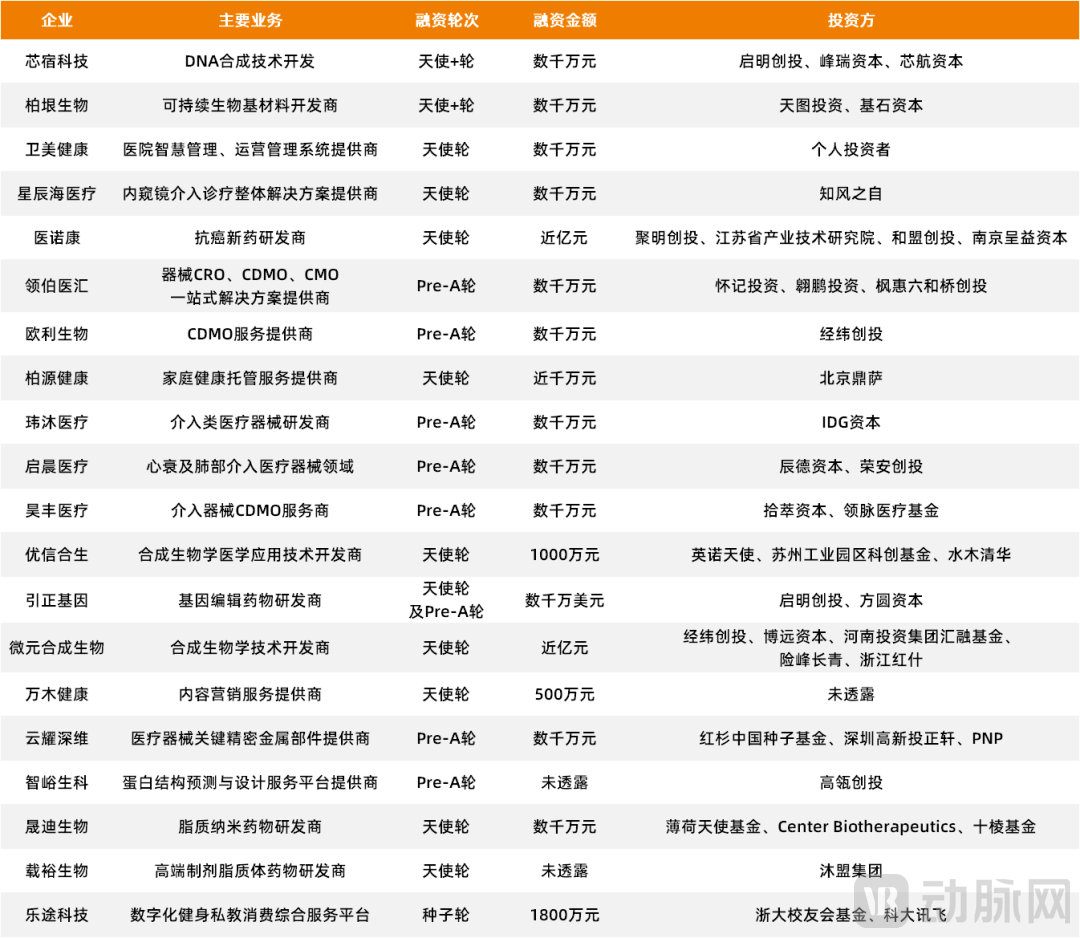

According to incomplete statistics from VCBeat’s Orange Data Bureau, a total of in China’s healthcare sector in May20 Early-Stage (Seed, Angel, and Pre-A) Investment and Financing Events, Total Financing AmountOver RMB 500 million. Compared with April, both key metrics declined; the number of financing events decreased by 25% year-on-year, while the total financing amount,Year-on-year decrease of 200%.

Therefore, investment institutions are choosing to "tighten their belts" at present,Has investment in early-stage healthcare projects returned to rationality? Or are we quietly awaiting the next wave of IPOs breaking their issue price?

Two Major Trends: High Proportion of Scientist Entrepreneurs, “Hard Tech” Remains Mainstream

Data always tells the truth. A further analysis of early-stage financing data for May reveals two key insights:

First, this is reflected in the founders, with an increasing proportion of scientists starting businesses.

According to statistics from VBInsight, among the 20 healthcare companies that completed early-stage financing in May,Over 80% of founders have a scientific background, and most of them graduated from top-tier domestic or international research institutions.

For example, having completed an angel round of financing worth nearly RMB 100 millionYinuokang, its core management team collectively possesses decades of successful experience in drug R&D, and key leaders have previously spearheaded PROTAC and molecular glue projects at U.S. innovative drug companies, advancing related candidates into clinical trials.

For example,Xinsu Technology, which has completed tens of millions of yuan in Angel+ round financing, its core teamHailing from prestigious institutions such as the Massachusetts Institute of Technology, UC Berkeley, Washington University in St. Louis, Tsinghua University, Peking University, Fudan University, and Nanjing University, they possess extensive research experience and industry expertise in biotechnology, integrated circuits, MEMS, and microfluidics.

This also aligns with the fundamental principles of entrepreneurship in the current healthcare sector. On one hand, research institutions have vigorously encouraged scientists to launch startups in recent years and created a favorable environment for them, prompting a wave of scientists to step out of their laboratories. On the other hand, as the healthcare industry increasingly extends into high-tech domains, today’s startups require greater “hard” technological capabilities than in the past, thereby raising the bar for founders.

Second, this is reflected in specialized sectors, where medical devices and biopharmaceuticals are equally prominent, while synthetic biology and CDMOs have emerged as hotspots for early-stage investment.

According to statistics from VCBeat’s Orange Fruit Bureau, among the 20 healthcare companies that completed early-stage financing in May,“Hard-tech” enterprises account for as high as 80%.Among them, the number of medical device companies and biopharmaceutical companies is the same, with 8 companies each.

Upon further analysis, among these 16 “hard-tech” companies,Synthetic Biology and CDMOThese sectors have become the focus of early-stage investment, with three companies each, accounting for a combined total of 37.5%.

Let’s start with synthetic biology. Wei Yuan Synthetic Biology, which completed an angel round of financing of nearly RMB 100 million in May, is a biomanufacturing company based on synthetic biology technology. It is committed to producing various compounds using low-carbon, energy-efficient, and sustainable methods for applications in pharmaceuticals, daily chemicals, agriculture, food, feed, and materials.

Let’s talk about CDMOs.Completed a tens-of-millions-yuan Pre-A financing round in MayOuli Biotech, is a CDMO service provider focused on nucleic acid therapeutics, dedicated to providing global pharmaceutical companies with "one-stop" CDMO services including nucleic acid drug discovery, laboratory R&D, process and analytical development, CMC services, API manufacturing, and drug registration.

It is evident from the investment fervor in niche sectors that the intersection of hard technology and substantial demand remains a “strategic battleground.” This area is not only a focal point for entrepreneurial efforts by a new generation of scientist-founders but also a key investment target for early-stage investors.

Taking synthetic biology as an example. As one of the most lucrative healthcare sectors over the past year, synthetic biology has garnered undeniable attention in the primary market. According to incomplete statistics from the investment community,At least 26 companies secured financing in 2021., including Bluepha, Changjin Biotech, and Boyin Biotech.

And the investment lineup behind it is exceptionally strong, including bothSequoia, Hillhouse, CDH Investments, Matrix Partners China, Qiming Venture Partnerssuch as well-known VC/PE firms, as well as internet giantsByteDance, in addition, a large number of VC/PE firms are queuing up to enter the market.

Certainly, there are good reasons why synthetic biology has garnered such strong favor from investment institutions. From a holistic perspective, synthetic biology is a multidisciplinary field with vast potential applications in biomanufacturing, cell and gene therapy, food and consumer goods, fine chemicals, and modern agriculture. As one of the foundational technology platforms in the industry, it holds significant market potential.

Furthermore, from the perspective of specialized sub-sectors, biomanufacturing, cell and gene therapy, and alternative proteins are all segments with exceptionally high growth ceilings. Among these prominent sectors, synthetic biology is already gaining momentum, currently in a phase of rapid technological advancement and accelerating application commercialization. Consequently, a large number of startup projects are transitioning from the laboratory to the marketplace. How to identify high-quality ventures with genuine market viability from this pool has become a new challenge for investors.

Multiple Key Metrics Decline: Why Is Early-Stage Healthcare Financing “Cooling Down”?

In contrast to the fervor of April, the keyword for the early-stage healthcare investment market in May was “cold.”

On the one hand, in terms of volume, both the number of financing deals and the number of participating investment banks have declined.First, regarding the number of financing deals: a total of 20 early-stage financing rounds were completed in May, representing a 25% year-on-year decline. Second, concerning investor participation: across these 20 early-stage financing deals in May, a total of 39 investment firms participated, a decrease of 32 from April and an 82% drop compared to the same period last year. In addition to the significant decline in deal volume, enthusiasm among top-tier investment firms has also sharply waned.

On the other hand, in terms of investment amount, both the total sum and the “unit price” have shown a sharp decline.First, regarding total financing: the total amount of early-stage healthcare financing in May was only RMB 500 million, a significant drop from over RMB 1.5 billion in April, representing a 200% year-on-year decrease. Second, concerning “average deal size”: early-stage financing amounts in May remained relatively stable, with 80% concentrated in the range of tens of millions of yuan. There were only two deals exceeding RMB 100 million, marking a notable decline compared to the seven such early-stage deals recorded in April.

So, why has the early-stage healthcare market begun to cool down?

There is, of course, a reason for this.First, from the perspective of the broader environment, affected by the pandemic, overall economic activity has remained subdued, with both primary and secondary markets currently in a state of contraction. As a result, investment institutions are exercising greater caution in making investments compared to the past. In addition, core regions such as Shanghai and Beijing have been under prolonged lockdowns, making many procedures that require in-person delivery difficult to complete in the short term and forcing delays.

Secondly, from the perspective of investment logic,Unlike the initial “frenzy” for early-stage projects, after a period of consolidation, many investment institutions have gradually cooled down, benchmarking against the market and developing a new set of early-stage investment logics. On the other hand, the evaluation criteria used by investment institutions for early-stage projects are becoming increasingly refined and rationalized, with full consideration given to their risk profiles and return rates.

Finally, from the perspective of the project itselfOn the one hand, constrained by various factors, there are very few startups that possess cutting-edge technologies and original innovation. On the other hand, from the perspective of scientists, having long operated within the closed environment of academic institutions, they lack expertise in commercial domains such as corporate operations management and resource expansion, and find it difficult to master these core competencies in a short period. This has, to some extent, delayed the market entry of early-stage projects.

From fervor to tranquility, this is the fundamental development pattern for the vast majority of things; the early-stage medical investment sector is no exception. Although the cooling observed in May was merely transient and does not signal the arrival of an industry inflection point, a return to rationality and prudence is an inevitable trend.

Therefore, for scientists embarking on entrepreneurial ventures, the top priority is always to develop projects that are truly innovative and meet market demands. In addition, scientists should also strive to enhance their core competencies in corporate operations and management. Meanwhile, for investment institutions crowded into the early-stage healthcare sector, it is essential to not only continuously improve their ability to identify promising early-stage projects but also strengthen their post-investment support services for these ventures.

Only in this way can one gain a first-mover advantage in the early-stage healthcare investment arena, which is full of opportunities and challenges.