China's TAVR Triad: Surging Revenues, Pipeline Expansion, and Anticipated Inclusion of Devices in National医保

MicroPort CardioFlow

A Provider of High-End Interventional Medical Devices in the Cardiac Valve Field, Engaged in R&D, Manufacturing, Sales, and Related Technical Consulting Services

Venus Medtech

Artificial Heart Valve System Device Developer

Peijia Medical

Developer of Cardiac and Cerebrovascular Interventional Medical Devices

Heart valve is a star sector in the medical industry.

The aortic valve is the primary battleground for competition among heart valve manufacturers. In the TAVR (Transcatheter Aortic Valve Replacement) sector alone, three listed companies have emerged: Venus Medtech, Peijia Medical, and MicroPort CardioFlow. Amidst the red-ocean trend in the aortic valve market, these three companies doubled their annual revenues in 2021, driven by sales of TAVR products.

Annual Revenue of the Top Three TAVR Players Source: 2021 Annual Reports of the Three Companies

Contrary to their continuously growing revenues, the stock prices of the three TAVR giants have fallen below their IPO prices. In early 2021, TAVR companies were still favored by investors, and MicroPort CardioFlow went public amid this favorable trend. However, the performance of these leading enterprises has cast a chill over the TAVR market.

Has the TAVR market met expectations? Beyond TAVR, what other high-potential segments in the heart valve field are worth exploring? By analyzing the 2021 annual reports of the three major players, we attempt to uncover some clues.

Unlike many high-end medical device products, the domestic TAVR market in China is led by locally manufactured brands, with imported brands only entering the Chinese market in 2020. In June 2020, Edwards Lifesciences’ third-generation TAVR product, the Sapien 3 valve system, was approved for marketing, becoming the first imported TAVR system approved in China.

China's TAVR market remains in its introductory phase. Both patient acceptance of high-cost valve therapies and physicians' acquisition of TAVR procedural skills require a transitional period. Furthermore, the limited number of hospitals and clinicians qualified to perform TAVR procedures across China means the market is still gradually taking shape.

2021 marked the inaugural year for the approval of TAVR products in China, with multiple domestically produced TAVR devices receiving approval from the National Medical Products Administration (NMPA), thereby driving profitability in the cardiac valve segments of these enterprises. Currently, there are no approved domestic products for mitral or tricuspid valve replacement/repair in China; therefore, the revenue of domestic companies is primarily derived from their TAVR businesses. Meanwhile, Chinese valve manufacturers have sequentially obtained overseas certifications and entered the European Union market. However, promotion and sales in overseas markets were temporarily slowed by the pandemic, so the primary revenue source for these enterprises remains the domestic market.

Venus Medtech Maintains Its Lead, Capturing Nearly 70% Market Share in Terminal Procedure Volume

As a leader in the TAVR field, Venus Medtech’s TAVR product, VenusA-Valve, received marketing approval from the NMPA in April 2017, becoming the first TAVR product approved for commercialization by the NMPA in China. Meanwhile, the upgraded version, VenusA-Plus, obtained NMPA marketing approval in November 2020 as China’s first approved retrievable TAVR product and began commercialization in early 2021.

Venus Medtech reported total revenue of approximately RMB 415 million in 2021, representing a year-on-year increase of 50.6% compared to 2020. The vast majority of the company’s revenue was derived from its VenusA-Valve and VenusA-Plus products. Sales revenue from these two TAVR products amounted to RMB 405 million, a 49% increase from 2020, accounting for 97.4% of Venus Medtech’s total revenue.

VenusA-Valve and VenusA-Plus maintained rapid growth in the Chinese market, with approximately 3,600 procedures performed throughout the year, covering 360 hospitals or medical centers across China. The market share of terminal procedure volume reached nearly 70%, representing a decline from the over 80% market share in 2020, primarily due to the successive approvals of similar products. For reference, the number of TAVR procedures in China exceeded 6,500 in 2021.

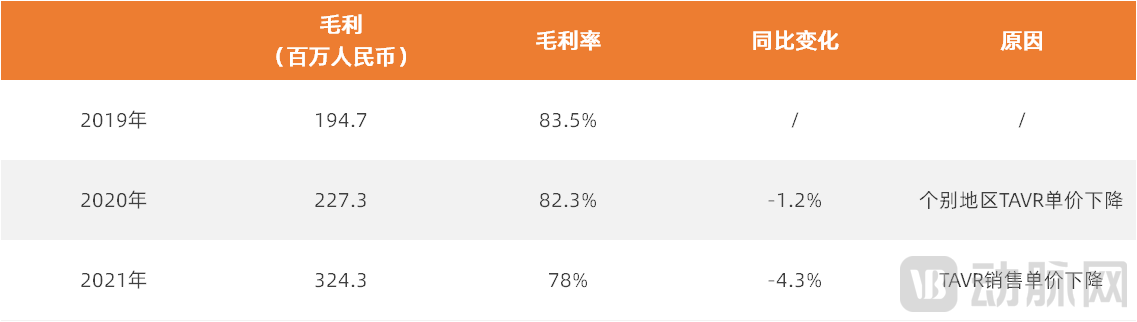

Meanwhile, Venus Medtech’s gross profit in 2021 was RMB 324 million, representing a year-on-year increase of 42.7% compared with 2020. However, the company’s gross margin declined from 82.3% in 2020 to 78% in 2021, primarily due to a decrease in the average selling price of TAVR products.Amid an increasing number of participants in the TAVR market, Venus Medtech reduced the unit price of its VenusA-Valve product to expand the market share of its second-generation TAVR products, thereby leading to a decline in the company’s gross profit margin.

In the prospectus filed by MicroPort CardioFlow at the end of 2020, it was mentioned that the unit price of Venus Medtech’s VenusA-Valve was approximately RMB 248,000. By comparison, the unit price of MicroPort CardioFlow’s VitaFlow was RMB 196,000, and that of Jiecheng Medical’s J-Valve was RMB 260,000. Although MicroPort CardioFlow’s TAVR product had the lowest unit price, which facilitated its clinical adoption, this also impacted the company’s gross profit margin. As the first product approved in China with the most robust clinical evidence, Venus Medtech’s VenusA-Valve initiated a price war, which may influence industry pricing standards.

Venus Medtech’s Gross Profit Source: Venus Medtech 2021 Annual Report

Furthermore, sales of Venus Medtech’s TriGUARD3 cerebral embolic protection device in the European market also increased, contributing RMB 9.38 million in revenue. As central nervous system injury is a serious complication that may arise from TAVR procedures, TriGUARD3 helps prevent cerebral embolism by covering the patient’s entire ascending aortic arch. This product can be paired with Venus Medtech’s TAVR devices to provide a more comprehensive solution for aortic valve disease.

In addition, Venus Medtech’s VenusP-Valve transcatheter pulmonary valve replacement (TPVR) system received CE MDR certification and was launched in April 2022, marking the first valve product from China to be approved in the European Union. Subsequently, the VenusP-Valve obtained FDA approval for two humanitarian use cases in the United States.

The VenusP-Valve has been in clinical use for nine years and has been approved by the NMPA to enter the Special Examination Procedure for Innovative Medical Devices. It is currently in the clinical trial or marketing application stage in several major countries worldwide. Leveraging Venus Medtech’s commercial foundation in the European market, the VenusP-Valve is expected to contribute new revenue next year.

MicroPort CardioFlow’s Gross Margin Rises as TAVR Products Trade Volume for Price

In early 2021, MicroPort CardioFlow, a company deeply entrenched in the field of structural heart disease devices, went public. By the end of 2021, the company’s annual revenue had increased by 93.2% year-on-year from RMB 103 million in 2020 to RMB 200 million in 2021. This growth was primarily driven by expanded sales of the company’s TAVR product, VitaFlow, and the commercialization of VitaFlow Liberty.

MicroPort CardioFlow commenced the commercialization of VitaFlow in China in August 2019. The product was registered in Argentina and Thailand in 2020, with commercial implantations performed in six hospitals in Argentina in 2021. VitaFlow Liberty, the company’s second-generation TAVR product, received approval from the NMPA in August 2021 and its commercialization began in September 2021.

As of the end of 2021, 308 hospitals in China had adopted VitaFlow and VitaFlow Liberty for TAVR procedures, with the majority being Grade A tertiary hospitals in first- and second-tier cities. In terms of market share, MicroPort CardioFlow held a leading position in more than 180 of these hospitals.

It is worth noting that,In 2021, MicroPort CardioFlow’s gross profit was RMB 118 million, compared with RMB 45 million in 2020, representing a year-on-year increase of 161.5%. The gross profit margin in 2021 was 59.1%, up by 15.4 percentage points from 43.7% in 2020.

In 2021, MicroPort CardioFlow significantly reduced its annual loss by lowering costs and expanding sales volume. However, its gross profit margin remained relatively low compared to the approximately 80% gross profit margins of Venus Medtech and Peijia Medical. Although these two competitors have faced market competition with a trend toward product price reductions, the overall magnitude has been limited; thus, MicroPort CardioFlow still needs to achieve breakthroughs in sales volume.

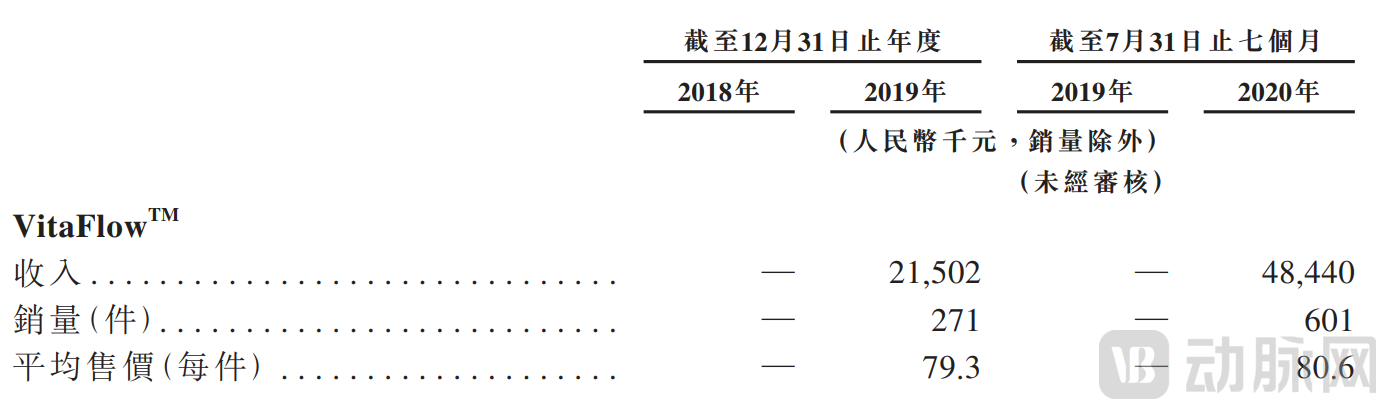

At the time of its initial public offering, MicroPort CardioFlow adopted a strategy of competing on price, capturing market share with a unit price below RMB 200,000. Rather than selling products directly to hospitals, the company leveraged MicroPort’s sales network and distributed its products through a traditional consignment model, with a portion of the revenue flowing to distributors. According to MicroPort CardioFlow’s prospectus, the ex-factory price of VitaFlow was approximately RMB 80,000, while the end-user price stood at RMB 196,000.

Average Selling Price of VitaFlow Source: MicroPort CardioFlow Prospectus

As of the end of 2021, MicroPort CardioFlow had a total of 25 distributors. The company’s distribution costs increased by 126.5%, from RMB 51 million as of the end of 2020 to RMB 116 million as of the end of 2021, primarily due to increased marketing activities and staff costs associated with the promotion of VitaFlow and VitaFlow Liberty.

Peijia Medical Sees Dual Growth in Neurointerventional and Valve Businesses, with R&D Expenses Surging 331.4% Year-on-Year

Among the three listed cardiac valve companies in China, Peijia Medical is the fastest-growing in terms of revenue. By the end of 2021, Peijia Medical reported total revenue of RMB 136 million, compared with RMB 38 million in the same period of 2020, representing a year-on-year increase of 253.2%. Meanwhile, the company’s gross profit rose from RMB 25 million in 2020 to RMB 95 million in 2021, a year-on-year increase of 279.2%.Notably, the transcatheter valve therapy business achieved a gross profit margin of 82.8%, demonstrating significant cost advantages in the market.

Peijia Medical operates two major business segments: heart valve and neurointerventional procedures. In 2021, the company’s transcatheter valve therapy and neurointerventional businesses generated revenues of RMB 41 million and RMB 94 million, respectively, with the valve business segment accounting for approximately 30.6% of total revenue.

As of the end of 2021, Peijia Medical’s first-generation TAVR product, TaurusOne, and its second-generation retrievable TAVR product, TaurusElite, had been adopted by 95 hospitals (equivalent to 102 centers). Meanwhile, the sales volume of the company’s TAVR products reached 452 sets in the first year following regulatory approval.

Peijia Medical demonstrates strong commercialization capabilities, with two of its heart valve products approved and their market promotion accelerated within a single year. Following the NMPA approval of its first-generation TAVR product, TaurusOne, in April 2021, the second-generation TAVR product, TaurusElite, was launched in June 2021. It obtained the national medical device coding within 50 days. As of August 28, the product had been submitted for review in 21 provinces, listed on procurement platforms in 11 provinces, and successfully included in the Guizhou Provincial Medical Insurance reimbursement list. The majority of the company’s TAVR sales revenue is derived from its second-generation retrievable product.

Meanwhile, Peijia Medical’s annual net loss decreased significantly, from RMB 2.068 billion in the same period of 2020 to RMB 574 million in 2021, representing a year-on-year decline of 72.2%. Moreover,The company's loss in 2021 was primarily attributable to a substantial increase in R&D expenses, which rose by 331.4% year-on-year compared to 2020.

Overall, China’s heart valve market is characterized by a large volume, rapid growth, and low penetration. In 2019, approximately 2,400 transcatheter aortic valve replacement (TAVR) procedures were performed in China, representing a penetration rate of 0.3%, while the number of patients eligible for TAVR was approximately 767,000. In the same year, the United States performed approximately 66,800 TAVR procedures, with a penetration rate of 23.4%.

Affected by the pandemic, the number of TAVR procedures in China was approximately 3,500 in 2020, rising to over 6,500 in 2021, representing a near doubling. Meanwhile, an analysis of the annual performance of three listed heart valve companies reveals that, driven by strong marketing and commercialization capabilities, the TAVR segment generated substantial revenue, with products rapidly adopted in clinical practice following regulatory approval.

From the perspective of clinical demand, indications for TAVR have been expanded, with domestic and international guidelines indicating that TAVR procedures can be used in patients at intermediate and low surgical risk. In terms of competitive landscape, four Chinese manufacturers and two imported brands currently occupy China’s TAVR market, but no single player has yet established a dominant position.

However, the challenge of market expansion also lies before TAVR companies. Although the application volume of TAVR products from the three major players has increased significantly, it has still not met corporate expectations.Venus Medtech completed approximately 3,600 procedures in total throughout 2021, whereas the company’s 2021 guidance was 4,000–4,500 cases (with a floor of 4,000 cases).

First,China has a limited number of end-user hospitals.Due to the complexity of TAVR procedures, only hospitals capable of performing over 400 PCI cases annually are qualified to conduct them. TAVR entails a high technical threshold and a prolonged learning curve for physicians. Furthermore, each procedure requires multidisciplinary collaboration among cardiology, anesthesiology, echocardiography, and pulmonology departments. Consequently, these procedures remain concentrated in Grade A tertiary hospitals located in first- and second-tier cities.

Secondly,TAVR Procedures Are ExpensiveIn the Chinese market, TAVR has not yet been included in the national medical insurance scheme. In early 2022, the Shanghai Municipal Medical Insurance Bureau incorporated TAVR medical services into its reimbursement coverage, setting the fee standard at RMB 5,200 with a patient co-payment rate of 10%. Generally, the cost of TAVR procedures is relatively high, with the total procedural cost amounting to approximately RMB 300,000, of which RMB 200,000 is attributed to consumables. Although this policy does not cover the cost of TAVR devices, the reduction in medical service fees will further promote the adoption of TAVR procedures.

However, in May 2022, the Shanghai Healthcare Security Administration issued the “Notice on the Pilot Implementation of Performance-Based Payment for Certain Medical Consumables,” proposing a pilot performance-based payment model for folded heart valve consumables. Under this policy, TAVR consumables are included in the medical insurance coverage at an 80% reimbursement rate, with immediate procedural success rates or the incidence of severe perioperative complications incorporated into the assessment criteria. This measure will drive the rapid adoption of high-performance TAVR products.

Intensified Competition, Price ReductionsThese challenges also confront domestic TAVR companies. Edwards Lifesciences, a global TAVR giant, has prioritized China as a key region for its overseas expansion. From September 2020 to July 2021, its TAVR products were used in more than 200 cases in China. Following NMPA approval of Medtronic’s third-generation TAVR product, Evolut PRO, in late 2021, commercial implantation will also be gradually rolled out.

Beyond the increasingly crowded TAVR landscape, companies are shifting their focus to the mitral and tricuspid valve sectors, aiming to provide more comprehensive solutions for valvular heart disease. The product portfolios of the three major TAVR players are also expanding beyond TAVR, with these initiatives accounting for the majority of their R&D expenditures.

Globally, the field of aortic valve disease treatment is relatively mature, whereas mitral and tricuspid valve interventions remain in their early stages and are becoming a key focus for domestic companies’ strategic layouts.Academician Ge Junbo, Chief Physician at Zhongshan Hospital Affiliated to Fudan University, believes that the future structural heart disease market will be primarily driven by mitral and tricuspid valves.

Venus Medtech has enriched its mitral and tricuspid valve portfolios through acquisitions and investments, in addition to its robust TAVR business. Within a year, the company acquired two enterprises and established a joint venture subsidiary with an overseas partner.

In December 2021, Venus Medtech acquired Cardiovalve, a company specializing in transcatheter mitral and tricuspid valve therapies, for $266 million. The acquisition was completed in early 2022, making Cardiovalve a wholly-owned subsidiary of Venus Medtech.

Cardiovalve’s Cardiovalve System is a transcatheter interventional valve replacement product capable of simultaneously treating mitral regurgitation and tricuspid regurgitation. For the indication of mitral regurgitation, the Cardiovalve System was granted Breakthrough Device designation by the U.S. FDA in 2020 and had previously entered the Early Feasibility Study phase.

In October 2021, Venus Medtech signed an agreement with Nuocheng Medical to acquire the company for a maximum consideration of RMB 493 million, thereby obtaining its Liwen RF Radiofrequency Ablation System. Developed based on the “Liwen Procedure” invented by Professor Liu Liwen from the Department of Ultrasound at Xijing Hospital of Air Force Medical University, this system is designed for hypertrophic cardiomyopathy. It employs full ultrasound guidance, with the ablation needle inserted percutaneously through the intercostal space via the cardiac apex to access the interventricular septal myocardium from the epicardium, enabling radiofrequency ablation. This is the world’s first radiofrequency ablation device specifically designed for myocardial ablation.

Also in 2021, Venus Medtech participated in the investment of Dejin Medical, a company that developed China’s first transapical interventional device for mitral regurgitation, MitralStitch; China’s first transfemoral venous mitral valve repair device, DragonFly-M; and China’s first transfemoral venous tricuspid valve repair device, DragonFly-T.

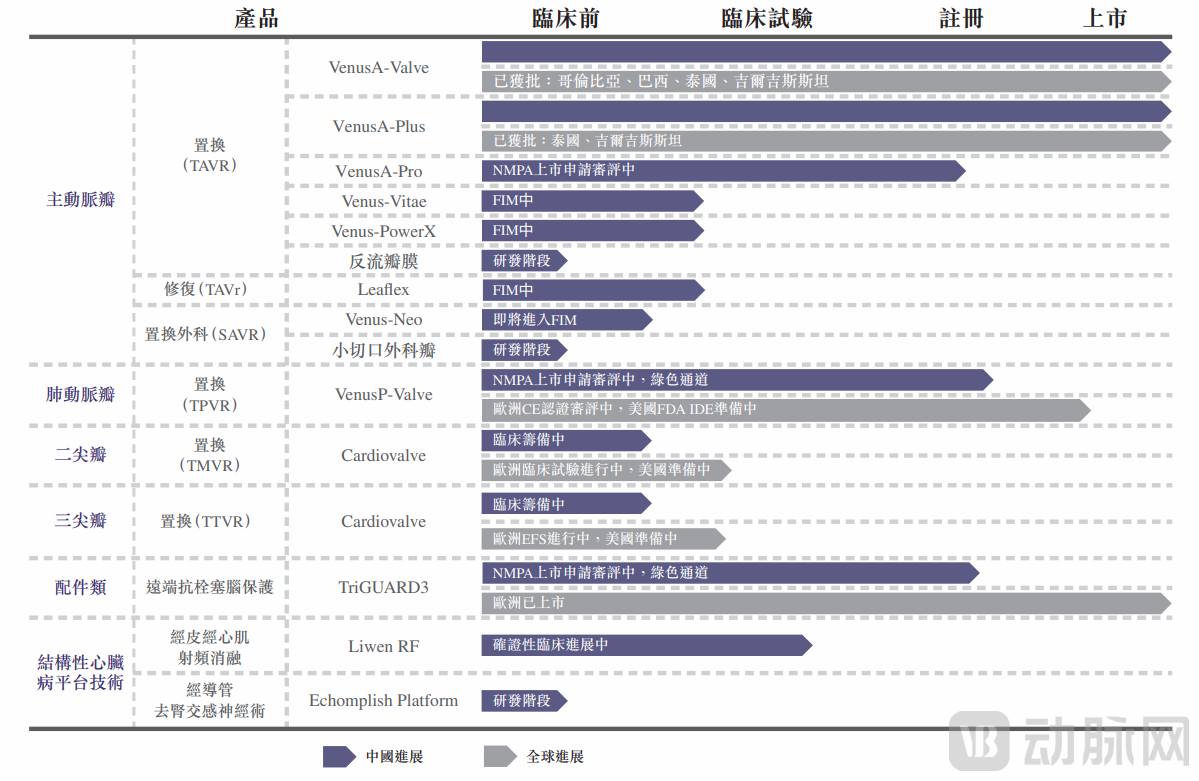

Venus Medtech’s Product Portfolio Source: Venus Medtech 2021 Annual Report

Venus Medtech’s mitral valve replacement device, Limbus, is in the preparatory stage for exploratory clinical trials, while its tricuspid valve replacement device is under development. The aforementioned acquisitions and investments will further enhance Venus Medtech’s product portfolio.Currently, Venus Medtech has established a comprehensive solution for structural heart disease, covering valvular heart diseases involving the aortic, pulmonary, mitral, and tricuspid valves, as well as hypertrophic cardiomyopathy, renal denervation for hypertension, and other procedural consumables.

MicroPort CardioFlow has also enriched its business portfolio through capital injections and joint ventures. In November 2021, MicroPort CardioFlow decided to make an additional investment of up to USD 25 million in 4C Medical, which agreed to grant MicroPort CardioFlow exclusive commercial rights for its pre-clinical tricuspid valve product in Mainland China, Hong Kong SAR, Macao SAR, and Taiwan Region of China.

Following the completion of the additional investment, MicroPort CardioFlow became the largest shareholder of 4C Medical and initiated collaboration with 4C Medical on transcatheter mitral valve (TMV) and transcatheter tricuspid valve (TTV) products.

Moreover, MicroPort CardioFlow co-founded Shanghai Weidun Medical, which has a total registered share capital of RMB 50 million. MicroPort CardioFlow contributed RMB 17 million, accounting for 35% of Shanghai Weidun’s registered share capital.

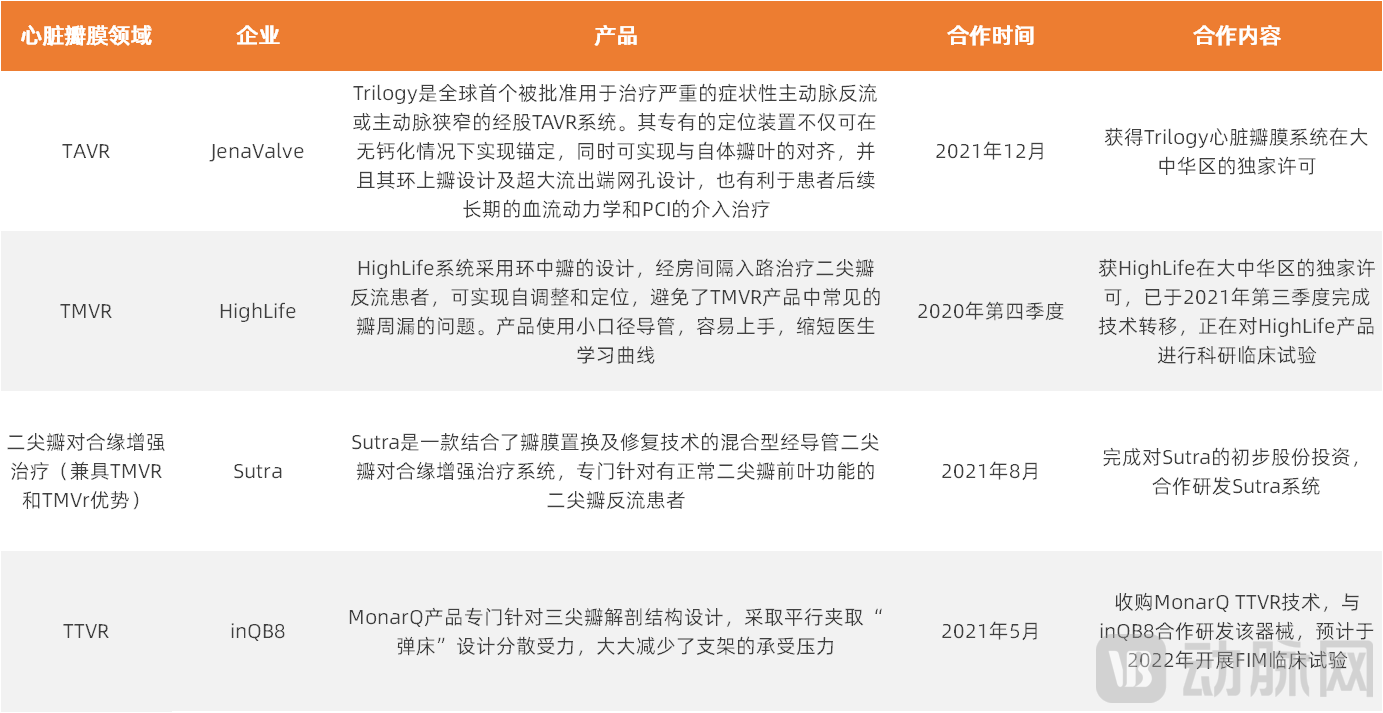

In Peijia Medical’s 2021 R&D expenditure, which grew by 331.4%, the majority consisted of upfront and milestone payments for four business development (BD) projects, totaling RMB 314 million and accounting for approximately 70% of total R&D spending. Through these four BD projects, Peijia Medical has established its presence in the fields of transcatheter aortic valve replacement, mitral valve replacement, tricuspid valve replacement, and mitral leaflet edge-to-edge repair.

Peijia Medical's 4 BD Projects in 2021 Source: Public Information

Among them, Peijia Medical has obtained the exclusive license for the Trilogy transcatheter heart valve system in the Greater China region. Trilogy is the world’s first TAVR system approved for the treatment of severe symptomatic aortic regurgitation or aortic stenosis.

Aortic regurgitation is one of the most common aortic valve diseases. According to Frost & Sullivan, there were approximately 27 million patients with aortic regurgitation worldwide in 2020, including about 3.9 million in China. However, currently approved transcatheter aortic valve replacement (TAVR) products in China are indicated only for aortic stenosis, leaving the clinical need for the treatment of aortic regurgitation unmet.

Currently, among the three listed heart valve companies, Peijia Medical has a more comprehensive product portfolio in the valve segment. In the field of aortic valves, Peijia Medical has developed four generations of TAVR products and a non-implantable shockwave valve therapy system. In the mitral valve field, the company has established a presence in TMVR, TMVr, and edge-to-edge repair technologies. In the tricuspid valve field, the company is simultaneously developing both replacement and repair products.

An analysis of the industrial layouts of the three TAVR giants reveals that, within China’s current market landscape, a standalone TAVR product is insufficient to meet corporate development needs. Consequently, providing solutions that cover a broader range of valvular heart diseases or complications associated with valve surgery has become a key strategic focus. Products targeting the mitral and tricuspid valves are poised to become the second growth curve for these three industry leaders.

References:

Peijia Medical: Fastest Progress in Next-Gen TAVR Products, Comprehensive Mitral and Tricuspid Valve Portfolio, Market Competitive Landscape Far from Settled

"Peijia Medical 2021 Annual Report"

“MicroPort CardioFlow 2021 Annual Report”

"Venus Medtech 2021 Annual Report"