Leading Orthopedic Firms Move Upstream: Material Platforms Emerge as Strategic Frontier Amid Intensified Domestic Substitution

As the centralized procurement advances, orthopedic companiesProfitaffected byCompression, while industry concentration has increased significantly. As the market undergoes accelerated consolidation, how can orthopedic companies seek breakthroughs and reestablish their position within the industry?

There are two strategic directions to pursue: first, actively promote reasonable price reductions for products to compete in the volume-based procurement (VBP) market; second, lay out emerging, higher-tech fields such as orthopedic surgical robots and digital orthopedics, accelerating innovative R&D. While both defensive and offensive strategies have their pros and cons, expanding into new territories and capturing incremental market share appears “superior” compared to merely defending existing strongholds.

Among them, many companies have begun to focus on upstream raw materials. Orthopedic implants have high requirements for the biological and mechanical properties of materials, and the quality of material properties directly affects the final performance of the implants. Looking at the development of the industry, materials science has been driving the progress of orthopedics. Orthopedic raw materials have evolved from early ordinary metals to metal alloys, ceramics, polymers, and other types, while orthopedic implants have gradually progressed from structural replacement to functional replacement, steadily achieving higher treatment goals.

Therefore, orthopedic companies are extending upstream, with innovative materials as a key focus.

Biomedical materials are substances used to diagnose, treat, repair, or replace damaged tissues and organs in the human body, or to enhance their functions. Based on application scenarios, they can be categorized into orthopedics, neurosurgery, cardiovascular, ophthalmology, stomatology, and other fields.

According to data from Markets and Markets, the global biomedical materials industry is experiencing rapid growth. The global market size for biomedical materials was USD 105.18 billion in 2019 and is projected to reach USD 206.64 billion by 2024, representing a compound annual growth rate (CAGR) of 14.5%. Among these, orthopedic biomedical materials hold the largest market share.

From the perspective of the orthopedics market, age is a significant factor influencing skeletal diseases; for instance, as individuals age, their bone repair capacity gradually declines. Therefore, with the accelerating aging of the global population, the growth potential of the orthopedics market is evident. According to forecasts by Evaluate MedTech, orthopedics remains the fourth-largest segment within the global healthcare market, with its market size valued at approximately $36.5 billion in 2020 and projected to reach $47.1 billion by 2024.

Driven by a large population base and rising health awareness and purchasing power, China’s orthopedic medical device market presents substantial opportunities. According to data from the Southern Medical Institute and Huaxi Jishi, the market size of orthopedic implants in China grew from RMB 11.7 billion in 2013 to RMB 36.0 billion in 2020, representing a compound annual growth rate (CAGR) of 17.14%, significantly outpacing the global average.

In the face of such substantial market demand, prices in the upstream raw materials market have risen accordingly. So, what is the current state of development of orthopedic raw materials in China?

Research Accelerates, but Commercialization Pathways Remain Unclear

In recent years, orthopedics has seen continuous development in implant materials, manufacturing processes, product intelligence, and clinical applications. Among these advancements, the variety of implant materials has gradually expanded, with their performance being continuously optimized. The progression from early medical-grade stainless steel to cobalt-based alloys, titanium-based alloys, and further to polymer materials, shape-memory metals, and ceramics has provided effective support for the growth of the orthopedic industry.

In the pre-application phase, China boasts abundant and leading research in orthopedic biomaterials. According to a bibliometric analysis of global literature on biomaterials in orthopedics published in the journal Chinese Journal of Tissue Engineering Research, papers from China account for 29% of the total, ranking first worldwide. Institutions with high publication outputs include Sichuan University, Fourth Military Medical University, Shanghai Jiao Tong University Affiliated Sixth People’s Hospital, and Zhejiang University.

An industry insider stated, “From the perspective of technological research, China has numerous research institutes and teams dedicated to biomedical materials, with a high volume of published papers and patents and strong citation rates, placing it at a relatively leading position globally. However, there are shortcomings in translation from research to commercialization. The transition from research to medical products requires consideration of multifaceted factors, particularly exhibiting weaknesses in integration with clinical applications.”

China’s biomedical materials industry suffers from a weak link between technological innovation and industrial development. The primary “bottlenecks” include technologies that fail to meet market demands, a disconnect between technology and management, inadequate engineering capabilities, and insufficient capital investment. These issues have led to slow translation of research outcomes and a low level of industrialization, which is one of the key factors contributing to China’s heavy reliance on imports for high-end biomedical materials.

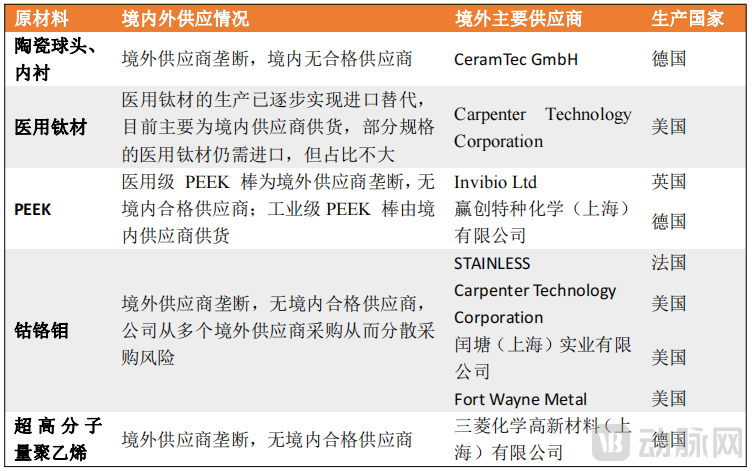

High-end raw materials rely on imports, with suppliers exhibiting a concentrated or monopolistic landscape.

In China’s orthopedic industry chain, the upstream raw materials sector lacks dominant market leaders, and there is a high reliance on overseas imports for high-end materials. An analysis of information disclosed in the prospectuses or annual reports of several leading domestic orthopedic companies reveals that many of them face risks associated with concentrated suppliers of key raw materials or dependence on a single supplier.

For example, Weigao Orthopaedics sources a portion of the core raw materials for its joint-related products, namely ceramic femoral heads and liners, as well as ultra-high-molecular-weight polyethylene (UHMWPE), primarily from a single supplier. Double Medical also faces the risk of supplier concentration for its key raw materials, which include various types of polyurethane tubing, medical-grade platinum rings, polycarbonate, medical-grade metals, and bone cement.

Meanwhile, foreign manufacturers dominate the vast majority of the market share for materials such as medical-grade ceramics, medical titanium alloys, PEEK, cobalt-chromium-molybdenum alloys, and ultra-high-molecular-weight polyethylene (UHMWPE). Taking ceramics as an example, Germany’s CeramTec GmbH is the undisputed hidden leader in the field of ceramic materials. Major domestic and international joint replacement manufacturers—including Johnson & Johnson, Smith & Nephew, Stryker, Zimmer Biomet, AK Medical, Chunli Medical, and Weigao Orthopaedics—all source their ceramic liners and femoral heads from this company.

As one of the manufacturers with the most comprehensive orthopedic product portfolio in China, Weigao Orthopaedics ranks first among domestic companies and fifth industry-wide in overall market share within the domestic orthopedic implant medical device sector, holding leading positions in all sub-segments. Taking Weigao Orthopaedics’ importation of major raw materials as an example, certain core raw materials exhibit a reliance on imports.

Source: Weigao Orthopedics (688161) Prospectus

Furthermore, Weigao Orthopedics’ prospectus stated: “The Company’s reliance on imports for certain core raw materials is consistent with industry characteristics and does not differ substantially from those of comparable peers in the same industry.” This suggests that there is still significant room for growth in the domestic supply of raw materials for orthopedic implants.

In 2021, at the 9th China Orthopedics, Biomaterials, and Digital-Intelligent Healthcare Industry Investment Summit, Professor Hong Youliang from the National Engineering Research Center for Biomaterials at Sichuan University stated, “As a critical component of the orthopedic industry, biomaterials face pivotal challenges in sustaining innovation and addressing material limitations, which are essential to breaking through the bottlenecks in domestic substitution.”

For implantable medical devices, infection, rejection, and the release of harmful ions are major challenges that must be addressed. These issues have not yet been effectively resolved on a global scale, with millions of people worldwide suffering harm from rejection and infections each year. Therefore, looking to the future, orthopedic implant materials require further development in terms of safety and functionality.

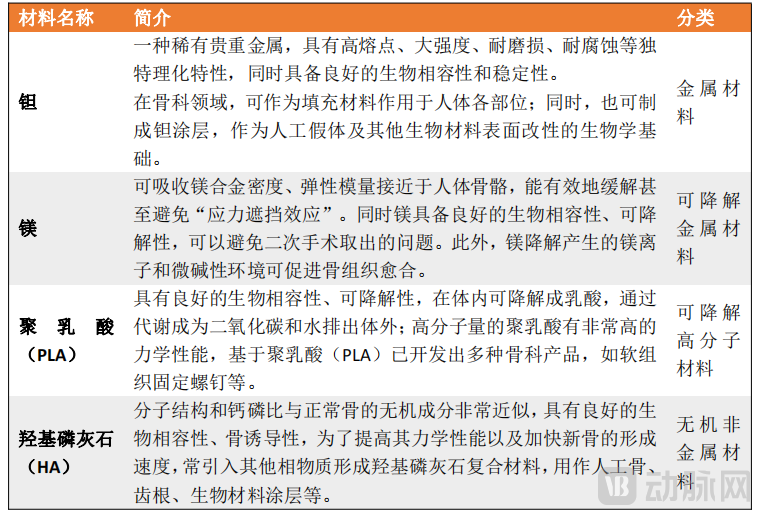

Ideal orthopedic implant materials should possess favorable biological properties, such as good biocompatibility, bioactivity, and corrosion resistance, as well as robust mechanical properties, including high fatigue strength, strong mechanical stability, and resistance to friction and wear. The current status of several representative materials is as follows:

These materials and their composites have become a focal point in orthopedic raw material research, garnering policy guidance and support due to their excellent mechanical and biological properties. Taking biodegradable magnesium alloys as an example, currently marketed products are predominantly from overseas and have narrow indications. In 2020, China’s National Medical Products Administration (NMPA) initiated the development of the “Technical Review Guidelines for the Registration of Biodegradable Magnesium Alloy Orthopedic Implants” to accelerate the market approval and clinical application of related products.

As national emphasis continues to grow and the development of the full orthopedic industry chain advances, the field of orthopedic raw materials has seen not only leading orthopedic device manufacturers extending upstream into raw materials, but also the emergence of a cohort of innovative companies leveraging materials research to expand into practical applications.

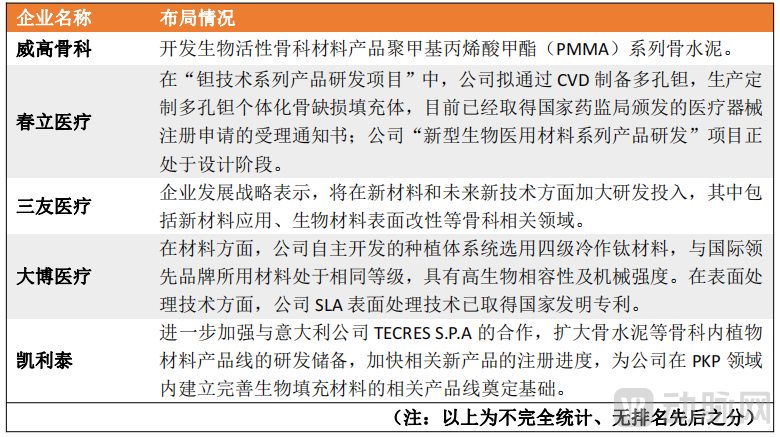

Seizing the Incremental Raw Material Market: Leading Medical Device Companies Are Successively Expanding Their Presence

Taking Chunli Medical as an example of leading orthopedic device companies, public information indicates that it has conducted research and development on porous tantalum materials, magnesium materials, and others. Notably, the project “Development and Clinical Application of Porous Tantalum Bone Repair Materials and Implantable Products,” led by Chunli Medical in its application, was approved by the Ministry of Science and Technology as a key special project under the 2020 National Key R&D Program for “Research and Development of Biomedical Materials and Tissue/Organ Repair and Replacement.”

Chunli Medical’s strategic entry into the upstream orthopedic raw materials sector is driven by two key factors. First, given the stringent requirements for orthopedic implant materials, the adoption of novel materials can enhance product performance and establish a competitive moat. Second, it strengthens the company’s bargaining power in cost control. According to its 2021 annual report, the shift from external procurement to in-house production of key raw materials, such as cobalt blanks and titanium blanks, reduced material costs and boosted the company’s overall gross profit margin.

Material-Related Layouts of Leading Enterprises Source: Official company websites and online resources

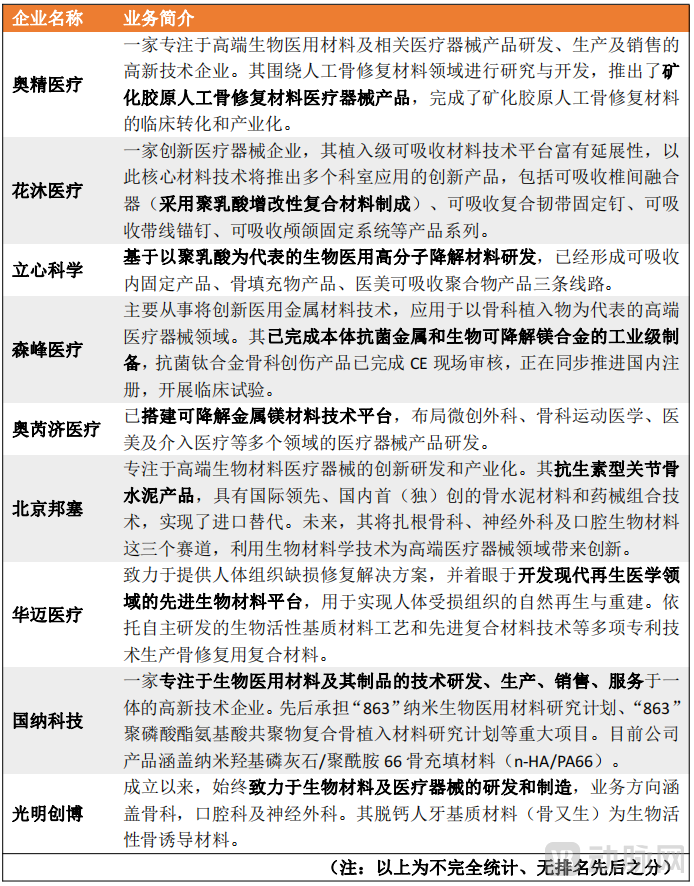

Building a Core Materials Platform: “New” Enterprises Forge Diversified Product Pathways

As import substitution advances, a cohort of companies focused on the research and development of materials and related devices has emerged in the orthopedics sector, with varying establishment dates. Among them, Allgens Medical serves as a representative example of extending material research into practical applications. The company is primarily engaged in the research and development, production, and sales of mineralized collagen artificial bone repair materials. It is one of the few domestic companies capable of providing artificial bone repair materials for the filling and regenerative repair of various bone defects throughout the body in clinical settings, and it possesses full-chain operational capabilities encompassing R&D, production, and sales.

The tight integration of “materials and products” has become a defining characteristic and competitive advantage for such companies. Leveraging their technical expertise in material properties, these enterprises can enhance the performance advantages of their products. Furthermore, by establishing material platforms, they can extend the benefits of advanced materials to a broader range of clinical applications, rather than being confined solely to the orthopedic market.

Furthermore, the biomedical materials industry is a knowledge-intensive, multidisciplinary sector that imposes stringent requirements on production environments, manufacturing processes, and quality control. Consequently, new entrants struggle to achieve sufficient technological accumulation and R&D capabilities in the short term.

“Material-Product” Related Enterprise Layout Overview Source: Compiled from Publicly Available Online Information

Overall, the biomedical materials industry is characterized by high capital intensity, elevated risk, broad technological scope, prolonged R&D cycles, and complex, multi-stage processes. A review of these companies reveals that they typically collaborate closely with research institutions; for instance, some possess an inherent capability for translating scientific achievements into commercial applications, while others actively participate in major projects at national, provincial, and municipal levels.

In mid-April 2021, with the joint support of the National Medical Products Administration (NMPA), the National Health Commission, the Ministry of Industry and Information Technology, and the Ministry of Science and Technology, 21 entities—including the Center for Medical Device Evaluation of the NMPA, the China Academy of Information and Communications Technology, the China National Center for Biotechnology Development, and the National Center for Nanoscience and Technology—jointly established the Biomaterials Innovation Cooperation Platform. The platform is dedicated to building an innovative system that deeply integrates biomaterials with related medical devices, thereby promoting the successful translation and application of scientific and technological achievements in the field of biomaterials.

Material innovation has become a key direction for companies to enhance their innovative capabilities against the backdrop of centralized procurement in orthopedics and the substitution of imported products with domestically produced ones. In the future, research in the field of materials may propel Chinese manufacturers even further forward.