Halved Market Valuations: Can China's Healthcare IT Sector Stage a Comeback?

In February 2022, Huazhuo Technology, a new-generation healthcare IT company, secured RMB 100 million in investment. At the time, Qiming Venture Partners, the investor, stated that they were betting on Huazhuo’s potential to become China’s “Epic.”

Logically, aiming to rival top-tier industry players should be the norm across all sectors. However, in the highly competitive field of healthcare informatics, few peers have set such ambitious goals, with most preferring to “rest on their laurels” within their own niches.

The industry as a whole lacks the vitality to strive forward, resulting in slowed development and a lack of core technologies. Despite policy support,Most companies’ revenues are still growing and will continue to do so, but their profitability has significantly weakened.. With no room for future imagination, in the secondary market for healthcare informatization after 2020, it has become common for stock prices to be halved, with most companies trading at a discount of more than 50% from their peak levels.

According to the 2021 annual report data, nine listed companies continued to experience growth, albeit at a significantly slower pace (Source: 2021 Annual Reports of the respective companies).

Investors are not the only ones feeling the pressure of development. During this period, several listed healthcare IT companies have undergone changes in equity ownership: Nanhai Cloud has taken control of Suncare Medical Cloud; Heren Technology has been integrated into the system of Topcare Medical, the leading dental chain operator; and B-Soft Co., Ltd. plans to grant a 10% stake to Philips through strategic cooperation, making Philips its second-largest shareholder.

At the inception of the concept of healthcare informatization, we drew, to some extent, on mature U.S. models for guidance. However, more than two decades later, China has yet to produce a company with a market capitalization in the hundreds of billions that has achieved sustained growth akin to Epic or Cerner; instead, domestic players have collectively fallen into a trap of stagnated development.

Where does the problem lie? And where is the breakthrough point?

When it comes to healthcare informatization, industry insiders inevitably think first of companies with over two decades of history, such as Winning Health Technology Group Co., Ltd., B-Soft Co., Ltd., and Neusoft Corporation. This perception aligns with reality, as more than ten established informatization firms collectively hold over 50% of the market share.

Therefore, some argue that informatization is a sunset industry, with the market’s corporate landscape and future development already set in stone.

Such statements are superficial. From single-disease reporting to the “Thousand Counties Plan”; from auxiliary diagnosis limited to specific scenarios to the construction of cross-regional county-level medical consortia; from the renovation of over 100,000 endpoints to hospital-wide solutions at the scale of hundreds of millions, healthcare informatization is in fact aIn a growth phase, driven by strong policy support, featuring a rich product hierarchy, and characterized by robust demandIn the B2B sector, no single company can monopolize all projects; it sustains both micro-enterprises with a dozen or so employees and listed companies valued at tens of billions.

For such a market, IDC’s projected size for 2022 is RMB 59.34 billion, with continued expansion at an approximate annual growth rate of 12%.

Most of the current industry leaders emerged during an era when hospitals had limited capabilities and lacked awareness of informatization. The fact that medical informatization sits at the upstream end of the industrial chain is its greatest drawback. In the early stages of informatization development, hospitals focused more on improving patient-facing care quality, making B-side informatization products a “luxury.”

However, as China’s healthcare capabilities continue to improve, healthcare informatization—particularly IT infrastructure—has become an essential tool for enhancing medical efficiency, optimizing patient experience, improving hospital management, and advancing scientific research. The disadvantages once associated with the prior status of healthcare informatization have now transformed into its most promising growth opportunity.

We have now entered the era of ecosystem competition. Controlling the Hospital Information System (HIS) and a hospital’s overall information architecture empowers enterprises to build an app store-like platform, onto which various clinical applications can be added. Many companies are striving toward this vision; for instance, Huazhuo Technology and Ewell Technology once aimed to become the “Android of the healthcare IT sector,” valuing the opportunity to serve as platform operators and seize the first-mover advantage in the wave of specialized application development.

A market endowed with multiple favorable factors—scale, policy support, user base, and ecosystem—is poised to give rise to a series of companies with market capitalizations reaching tens or even hundreds of billions.In contrast, the healthcare IT industry is home to thousands of enterprises at its foundational level, with countless companies valued at over RMB 100 million. However, only a select few, such as Winning Health Technology Group Co., Ltd. and B-Soft Co., Ltd., possess the strength to reach a market capitalization of RMB 10 billion.

In other words, the market has the capacity to support several healthcare IT companies with valuations in the hundreds of billions, but due to being mired in various difficulties, no single enterprise has managed to pull ahead decisively.

Liu Zhan (a pseudonym) once served as Deputy General Manager at a healthcare IT startup in southwest China. Upon his departure, he remained composed, noting, “One could live a routine life here, but it was hard to see any potential for breakthrough.”

“Startups always align their business operations with hospital needs: we deliver whatever hospitals require. In turn, hospitals follow policy directives, procuring what policies mandate. Under this incentive structure, companies need only focus on how to meet the prescribed standards more efficiently and cost-effectively. Today, hospital IT departments have become increasingly professional and are no longer as easily misled as in the past. Even if you incur higher costs to develop products with more comprehensive features and richer content, hospitals are rarely willing to pay for these extra efforts unless they address hard demands that deliver genuine value.”

The interplay between the two has led to two somewhat negative outcomes.

On one hand, healthcare IT products are increasingly subject to homogeneous competition. Hospitals are no longer selecting vendors based on undifferentiated offerings; instead, they rely on a “network of relationships” shaped by factors such as geographic proximity, brand recognition, influence, and personal connections. This shift is also the primary reason why Liu Zhan left the healthcare IT sector.

On the other hand, companies have begun to favor doubling down on the complexity of already convoluted IT concepts, substituting genuine product innovation with combinations of technologies and coined terminology. In 2020, Winning Health Technology Group Co., Ltd. and IDC jointly launched the promotion of next-generation Hospital Information Systems (HIS) through their report, “Building a Healthcare Digital Transformation Platform with Middle-Platform Thinking to Break Through the Capability Bottlenecks of Hospital Information Systems.” Other IT vendors, such as Neusoft Corporation and Ctrix Medical, quickly followed suit. However, according to an R&D employee at Neusoft, while healthcare HIS is indeed undergoing upgrades and iterations, there is no clear definition of what constitutes “new” in this context. Consequently, hospitals find it difficult to distinguish whether vendors are merely making minor adjustments to legacy systems or implementing truly disruptive innovations.

Under the combined influence of these two factors,The competitive landscape for traditional products of healthcare IT enterprises is gradually weakening, which is the primary factor contributing to the predicament in healthcare informatization.。

Against this backdrop, large-scale health IT enterprises established in the early stages have carved up the market for HIS and electronic medical record (EMR) infrastructure, leveraging their comprehensive product portfolios and long-standing reputations. Meanwhile, next-generation companies are largely focusing on emerging policy-driven demands (such as big data centers, DRG payment systems, online consultations, day-surgery centers, and emergency care) or novel clinical applications (such as specialty-specific Clinical Decision Support Systems [CDSS] and AI-assisted diagnosis).Few new enterprises are willing to spend years building a basic medical information system that approaches market saturation in order to compete with large corporations. In the absence of market competition, the development of basic medical informatics is driven almost entirely by policy.

The second constraining factor stems from medical data.

The medical big data industry, on which startups are betting, appears to be a sector with limitless potential. According to previous data from Ernst & Young, the market size of medical big data totaled approximately RMB 30.136 billion in 2022. However, due to information silos caused by the lack of data standardization and barriers to data application arising from privacy concerns, the actual volume of big data-related transactions falls far short of expectations.

Specifically, startups seeking to leverage intelligent tools such as deep learning and adaptive learning to develop application-based products face high data acquisition costs, along with challenges including small data volumes from disparate sources, substandard data quality, and incompatible data formats. Vast amounts of data lie buried deep within server rooms, yet remain difficult to utilize due to privacy, security, and other concerns.

The issue of data format mismatch may be gradually resolved in the coming years, whereas data silos resulting from privacy and security concerns require the entire industry to reach a consensus based on a set of secure and compliant regulations before viable solutions can be found. When the medical big data industry experienced its boom, many investors were drawn by the future value of these data assets. However, as evidenced by the withdrawal of Ping An Health Insurance Technology, there remains a considerable gap between turning the vision of medical big data into reality.

The third factor stems from cost constraints.The complex and multifaceted policy requirements have led to increasingly refined demands for hospital information technology products, strengthening the need for system customization and subsequent operations and maintenance. As a result, traditional template-based systems are beginning to lose their competitiveness. In this context, healthcare IT companies will incur higher costs in research, development, and implementation, leading to a decline in the industry’s overall gross profit margin.

Amid the convergence of three compounding factors, although the healthcare IT market continues to see an endless stream of new growth drivers, companies are stretched thin by delivery demands, lacking in both innovation and competitive strength due to the restraining effects of multiple factors.

The “Internet + Healthcare” policy issued by the State Council in the second half of 2018, along with the electronic grading policy, drove healthcare IT companies’ stock prices to high levels in 2019. Since then, market expectations have remained overvalued; the rapid gains witnessed earlier were followed by equally severe declines over the past two years. Currently, the sector is undergoing both a correction and a consolidation phase.

It may be tempting to attribute the correction in the healthcare IT industry to factors such as homogeneous competition, the suppressive effects of standardization on privacy, and rising costs; however, we must also consider the resistance originating from within healthcare IT companies themselves.

Large enterprises whose core business is medical infrastructure development mostly emerged during the system exploration phase centered on finance, or the application exploration phase focused on PACS, RIS, and CIS. The barriers built over ten or even twenty years of business accumulation enable them to better deliver integrated hospital information solutions. This is particularly relevant today, as new campus construction accelerates, the “Thousand Counties Plan” drives hospital upgrades, and traditional HIS systems undergo reform and replacement. Comprehensive solutions ensure data consistency across various hospital scenarios while avoiding the resource drain and prolonged implementation cycles associated with frequent, fragmented procurement.

The WeChat official account “Computer Renaissance” conducted a comprehensive survey of procurement demands in the informatization industry in 2021. Data showed that the value of new orders added in 2021 amounted to RMB 7.161 billion, representing only a modest increase compared to RMB 6.844 billion in 2020.

Among them, leading enterprises (including Winning Health Technology Group Co., Ltd., B-Soft Co., Ltd., Neusoft Corporation, Neusoft Medical Systems, Wonders Information Co., Ltd., SinoCare, and Heren Technology) won a total of RMB 4.578 billion in hospital orders, a year-on-year increase of 0.41%, and RMB 2.583 billion in public health orders, a year-on-year increase of 13.00%.

Industry leader Winning Health Technology Group Co.,Ltd. delivered the best performance in the sector in 2021, with total revenue of RMB 2.75 billion, 583 orders, and 24 orders valued at over RMB 10 million each. B-Soft Co., Ltd. recorded revenue of RMB 1.899 billion, secured 348 orders, including 29 orders valued at over RMB 10 million each. Donghua Software reported revenue of RMB 10.88 billion (across broader industries), with IT-related order value amounting to RMB 1.114 billion, comprising 248 orders, including 35 orders valued at over RMB 10 million each. In short, a few leading enterprises captured the vast majority of orders valued at over RMB 10 million.

Order Status of Leading Enterprises (Compiled from Data by the WeChat Official Account “Computer Renaissance”)

Behind these figures lies the overwhelming dominance of leading enterprises in the informatization market, yet it is precisely this force that has laid the groundwork for the industry’s current landscape.

Although hospitals may have varying needs regarding the same policy, they invariably operate within its overarching framework. Therefore, if a company can provide a sufficiently comprehensive solution to meet hospitals’ infrastructure requirements, it can leverage this offering to continuously secure substantial orders from the healthcare sector.

“At the end of the day, this industry is overly reliant on policy, which has instilled a sense of complacency in healthcare IT companies.”Zeng Rui (a pseudonym) summarized that he, too, had benefited from the boom in healthcare informatization.

“The root of this problem does not lie entirely with enterprises. The United States has a highly developed healthcare information technology sector because it serves a fully competitive system dominated by private hospitals, which requires vendors to provide strategic solutions that help hospitals minimize costs and maximize efficiency as much as possible. In China, however, most hospitals with enterprise-wide Hospital Information System (HIS) needs do not have to worry about patient acquisition. For the vast majority of these hospitals, the primary incentive for cost reduction and efficiency improvement comes from policy directives, thereby leaving enterprises with little motivation to innovate.”

“Since 2018, policy-driven incentives have continuously accelerated the in-depth digital transformation of the healthcare sector, with multi-million-yuan orders becoming the norm. Since then, IT enterprises with mature product portfolios have been propelled into the spotlight and continue to reap the benefits to this day,” Zeng Rui explained to VCBeat. “Although this transformation has been underway for four years, it is not yet halfway complete. Moreover, these systems are not a one-time purchase for lifetime use; given the typical iteration cycle of hardware and software, hospitals will require significant upgrades within at most ten years.”

Here we can provide the answer to the second question, namelyTo move away from the inflection point,Healthcare IT companies must keep pace with policy developments while reducing their total reliance on them; however, shedding such comprehensive dependence does not necessarily enable these enterprises to reach a turning point.

The current crisis in healthcare informatics stems from the combination of industry reshuffling driven by external factors and inertia caused by internal ones. This is particularly true for companies still entrenched in traditional healthcare IT systems; the architectures they once built are now too massive to pivot, making it difficult for them to bear the significant costs associated with innovation.

In the words of Chen Hong (a pseudonym), a medical IT expert: “Some enterprises spent ten years building their first curve; why would they be willing to spend another decade investing in the second curve? For companies that have invested too deeply in basic informatization, why would they be willing to make massive additional investments to move upstream and serve insurance companies and pharmaceutical firms?”

Laziness Can Be Overcome.Healthcare IT vendors have accumulated invaluable medical data and foundational infrastructure during the course of building out their systems. The key question is: How can they leverage these resources to chart a promising future that aligns with their unique circumstances?

Based on the current response strategies adopted by companies in the industry, there are three mainstream approaches.

One strategy is to bet on the inevitability of technological advancement and keep pace with the times by developing next-generation systems. This approach is suitable for large enterprises with strong cash flows, such as Winning Health’s Winex, B-Soft’s Huikang Cloud 2.0, and Neusoft Group’s new-generation HIS. These companies can afford the high costs of trial and error and ensure that their products are rapidly deployed in hospitals once implementation is complete.

Second, companies are exploring upstream segments of the industry chain while maintaining their existing system operations. For instance, they integrate AI-assisted diagnostic tools into existing RIS and PACS systems, and leverage NLP algorithms to empower electronic medical record (EMR) systems with intelligent data entry and smart quality control. While many enterprises have made attempts in this area, some have only dabbled superficially, whereas others regard these applications as key growth drivers for future development.

This is a path that pioneers have already traversed. A review of the revenue composition of leading U.S. health IT companies such as Cerner and Epic reveals that specialized applications and data-driven services now account for over 50% of their total revenue, with this segment boasting gross margins exceeding 70%. Therefore, medical IT applications and their associated SaaS models are highly likely to secure a significant share in the future revenue streams of healthcare informatization enterprises.

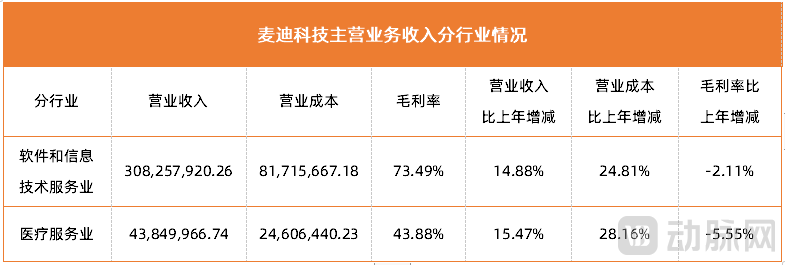

The third approach is cross-industry expansion, exploring new possibilities beyond traditional informatization. Winning Health Technology Group Co., Ltd. represents a case of relatively modest diversification, shifting its strategic focus to the “Internet + Healthcare” sector, which lies adjacent to health IT. Its ultimate goal is to create a closed-loop ecosystem integrating medical care, pharmaceuticals, and insurance. In contrast, Madison Medical Information has pursued a more ambitious cross-industry strategy. In 2019, it entered the assisted reproductive technology (ART) services market by acquiring Haikou Mary Hospital, thereby establishing a dual-business framework encompassing both healthcare informatization and medical services.

Medicom's 2021 Revenue from Core Business by Industry Sector

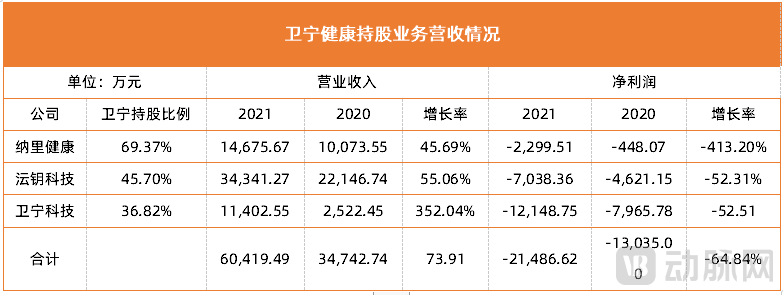

Winning Health 2021 Revenue from Equity-Holding Businesses

To date, various companies have repeatedly disclosed the performance results of their new businesses, with final outcomes varying significantly across different models.

Although Winning Health Technology Group Co.,Ltd.’s “Internet + Healthcare” system has incurred losses for consecutive years, it may eventually deliver value equivalent to that of its first curve after several years of investment; meanwhile, although Medicalsystem Co., Ltd. has achieved growth in both revenue and profit, this does not necessarily imply that its cross-industry success is sustainable.

Within a limited timeframe, it is impossible to determine who will ultimately prevail amidst the transformation. However, it is predictable that the new generation of healthcare IT companies, having entered a period of industry reshuffling, are already poised to make their move. If established enterprises fail to break free from their comprehensive reliance on policy support, they will struggle to defend their existing market share and risk being eliminated prematurely.